|

市場調査レポート

商品コード

1693877

中国の代替乳製品:市場シェア分析、産業動向と統計、成長予測(2025~2030年)China Dairy Alternatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の代替乳製品:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 168 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

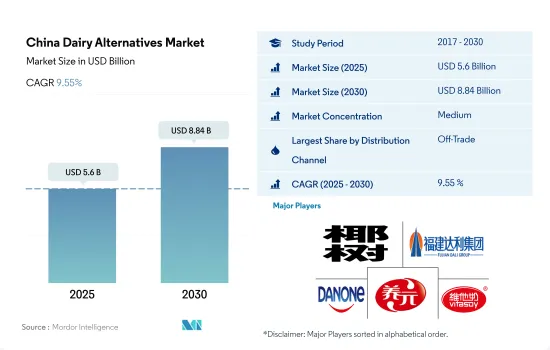

中国の代替乳製品市場規模は2025年に56億米ドルと推定され、2030年には88億4,000万米ドルに達し、予測期間(2025~2030年)のCAGRは9.55%で成長すると予測されます。

市場を牽引するのは取引外の小売チャネルが牽引する植物性ミルク販売の持続的成長

- 国内における代替乳製品の売上の大半は、非売品チャネルが占めています。商業外チャネルの中では、スーパーマーケットとハイパーマーケットが中国の代替乳製品市場で最大の流通チャネルです。これらのチャネルは、特に大都市や開拓都市に近接しているため、市場で入手可能な多種多様な製品の中から消費者の購入決定に影響を与えるという利点があります。2023年には、スーパーマーケットとハイパーマーケットが金額シェアの71%を占めました。

- オンラインチャネルは、オフトレードセグメントで最も急成長するチャネルになると予想されます。2023~2025年の前年比成長率は18%と予測されます。利便性は、より多くの代替乳製品食料品をオンラインで購入するように移行した買い物客の主要動機です。

- 中国全土で拡大するストリートフード文化は、予測期間中、チーズ、牛乳、デザートのような代替乳製品品のオントレード消費を促進すると予想されます。ファーストフードブランドとヴィーガンカフェを含むいくつかのカフェが、国内の飲食品フランチャイズの状況を支配しています。オンチャネルを通じた代替乳製品の販売額は、2022~2025年にかけて20%成長すると予測されます。

- すべての代替乳製品の中で、植物性ミルクは2022年のオフトレードとオントレードの小売チャネルを通じた販売額の大半を占め、シェアは97%でした。食生活における代替乳製品品の消費拡大により、これらの製品の消費はオフトレードとオントレードの両方の形態で促進されると予想されます。オフチャネルを通じた代替乳製品品の消費は、2024~2027年の間に28.9%成長すると予測されます。

中国の代替乳製品市場動向

動物や持続可能性への関心の高まりと食生活の変化が、同国の代替乳製品品消費に大きな影響を与えています。

- 菜食主義者の人口増加に伴い、菜食主義者のライフスタイルが中国で支持を集めています。2022年、中国におけるヴィーガンとベジタリアンの割合は約5~6%と推定されます。これは、同国における西洋文化の影響力の高まりにより、ここ2~3年で大幅に増加しました。北京、香港、上海、深セン、広州、成都といった中国の大都市には、菜食主義者向けの製品を扱うスーパーマーケットが軒を連ねています。代替乳製品の中でも、豆乳、アーモンドミルク、オートミルクといった植物由来のミルクが、2022年には中国全土で過半数のシェアを占めています。中国は、代替乳製品ミルクの消費量においてアジア太平洋の主要国です。植物性ミルクの中でも、大豆飲料は、大豆消費の長年の伝統と広く入手可能なことから、中国では伝統的に最も人気があります。2022年末までに、中国の大豆生産量は1,750万トンを超えました。

- 中国人がバターを含む非乳製品をますます採用する主要動機の1つは、動物や持続可能性への関心の高まりであり、次いで食生活の変化です。ナッツ・バターには天然の健康的な脂肪が含まれているため、ナッツとナッツ・バターは健康的な食生活の維持に大きく貢献しています。ナッツベースのバターの一人当たり消費量は予測期間中に増加すると予測されます。中国では、フリーフロム乳製品の消費が堅調に推移すると予測されます。中国人口の92%以上が、鼓腸や下痢など、乳製品に含まれる乳糖に対するアレルギー反応を持っています。ヨーグルト製品は発酵中に乳糖の大部分を分解し、起こりうるアレルギー反応を大幅に緩和します。そのため、植物性ヨーグルトの消費は予測期間中により速い速度で成長すると予想されます。

中国の代替乳製品産業概要

中国の代替乳製品市場は適度に統合されており、上位5社で57.46%を占めています。この市場の主要企業は、Coconut Palm Group、Dali Foods Group、Danone SA、Hebei Yangyuan Zhihui Beverage、Vitasoy International Holdings Ltdなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産

- 代替乳製品-原料生産

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- 非乳製品バター

- 非乳製品ミルク

- 製品タイプ別

- アーモンドミルク

- ココナッツミルク

- オートミルク

- 豆乳

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Blue Diamond Growers

- Califia Farms LLC

- Coconut Palm Group Co. Ltd

- Dali Foods Group Co. Ltd

- Danone SA

- Fraser and Neave Ltd

- Hebei Yangyuan Zhihui Beverage Co. Ltd

- Inner Mongolia Yili Industrial Group Co. Ltd

- Oatly Group AB

- Vitasoy International Holdings Ltd

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The China Dairy Alternatives Market size is estimated at 5.6 billion USD in 2025, and is expected to reach 8.84 billion USD by 2030, growing at a CAGR of 9.55% during the forecast period (2025-2030).

Market is driven by sustainable growth in sales of plant-based milk led by off-trade retail channels

- The off-trade channel accounts for the majority of sales of dairy alternative products in the country. Among off-trade channels, supermarkets and hypermarkets are the largest distribution channels in the Chinese dairy alternatives market. The proximity of these channels, especially in large and developed cities, gives them the added advantage of influencing the consumer's decision to purchase from among the large variety of products available in the market. In 2023, supermarkets and hypermarkets accounted for 71% of the value share.

- The online channel is expected to be the fastest-growing channel in the off-trade segment. It is projected to register a Y-o-Y growth value of 18% during 2023-2025. Convenience is the primary motivation for shoppers who have transitioned to shopping for more dairy alternative groceries online.

- Expanding street food culture across China is anticipated to drive the on-trade consumption of dairy alternative products like cheese, milk, and desserts during the forecast period. Fast-food brands and several cafes, including vegan cafes, dominate the landscape for food and beverage franchises in the country. The sales value of dairy alternative products through the on-trade channel is anticipated to grow by 20% in 2025 from 2022.

- Among all dairy alternative products, plant-based milk accounted for the majority share of sales through off-trade and on-trade retail channels in 2022, with a 97% share. The growing consumption of dairy alternative products in diets is anticipated to drive consumption of these products through both off-trade and on-trade modes. The consumption of dairy alternatives through off-trade channels is anticipated to grow by 28.9% during 2024-2027.

China Dairy Alternatives Market Trends

Growing concern for animals and sustainability followed by changing dietary habits is largely impacting dairy alternatives consumption in the country

- The vegan lifestyle is gaining traction in China in line with the growing vegan population. In 2022, the percentage of vegan and vegetarian populations in China was estimated to be about 5-6%. This increased significantly in the last 2-3 years due to the growing influence of Western culture in the country. The larger cities in China, such as Beijing, Hong Kong, Shanghai, Shenzhen, Guangzhou, and Chengdu, all have supermarkets stocking vegan products.Among dairy alternatives, plant-based milk like soy, almond, and oat milk held the majority share across the country in 2022. China is the leading country across the APAC region in terms of consumption of dairy alternative milk. Among plant-based milk, soy drinks have traditionally been the most popular in China due to the long-standing tradition of soy consumption and its wide availability. By the end of 2022, China produced over 17.5 million metric tons of soybeans.

- One of the key motivations for the Chinese population increasingly adopting non-dairy products, including butter, is growing concerns for animals and sustainability, followed by changes in dietary habits. Nuts and nut butter contribute significantly toward maintaining a healthy diet as nut butter contains natural and healthy fats. The per capita consumption of nut-based butter is estimated to increase over the forecast period.Strong consumption is projected for free-from dairy products in China. More than 92% of the Chinese population has allergic reactions to lactose in dairy products, including flatulence and diarrhea. Yogurt products break down a large portion of lactose during fermentation, greatly mitigating possible allergic reactions. Thus, consumption of plant-based yogurt is expected to grow at a faster rate during the forecast period.

China Dairy Alternatives Industry Overview

The China Dairy Alternatives Market is moderately consolidated, with the top five companies occupying 57.46%. The major players in this market are Coconut Palm Group Co. Ltd, Dali Foods Group Co. Ltd, Danone SA, Hebei Yangyuan Zhihui Beverage Co. Ltd and Vitasoy International Holdings Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Non-Dairy Butter

- 5.1.2 Non-Dairy Milk

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Almond Milk

- 5.1.2.1.2 Coconut Milk

- 5.1.2.1.3 Oat Milk

- 5.1.2.1.4 Soy Milk

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Blue Diamond Growers

- 6.4.2 Califia Farms LLC

- 6.4.3 Coconut Palm Group Co. Ltd

- 6.4.4 Dali Foods Group Co. Ltd

- 6.4.5 Danone SA

- 6.4.6 Fraser and Neave Ltd

- 6.4.7 Hebei Yangyuan Zhihui Beverage Co. Ltd

- 6.4.8 Inner Mongolia Yili Industrial Group Co. Ltd

- 6.4.9 Oatly Group AB

- 6.4.10 Vitasoy International Holdings Ltd

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms