|

市場調査レポート

商品コード

1693888

中東の代替乳製品:市場シェア分析、産業動向、統計、成長予測(2025~2030年)Middle East Dairy Alternatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東の代替乳製品:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 226 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

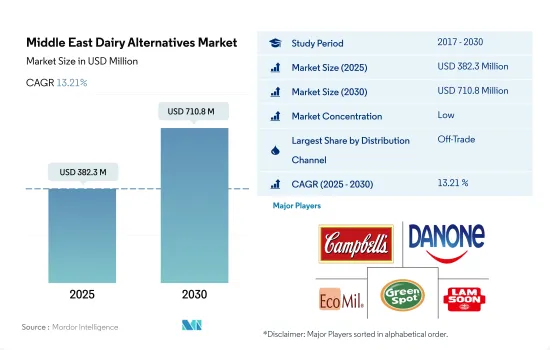

中東の代替乳製品市場規模は2025年に3億8,230万米ドルと推定され、2030年には7億1,080万米ドルに達し、推定・予測期間(2025~2030年)のCAGRは13.21%で成長すると予測されます。

スーパーマーケットとコンビニエンスストアの存在感が乳製品販売を押し上げる

- 2022年、中東の流通チャネルは2021年比で2.69%の成長を遂げました。レビュー期間中(2017~2022年)、取引外小売が中東の小売空間を支配しました。2022年には、商業外小売が81.26%のシェアを占めました。中東では、消費者は乳製品を含まない製品を購入する際の利便性の高さから、オフトレード小売に魅了されています。

- オンチャネル(クイックサービスレストラン)では、乳製品不使用製品の価格は固定されているが、オフチャネルでは消費者はいくつかの選択肢を与えられます。中東では、オフチャネルでは乳製品を様々な価格(低価格、中価格、高価格)で提供しています。これらの小売業者が販売するオートミルクは、2022年には2.78米ドルから35.4米ドルで販売されています。様々な価格で牛乳が入手可能であることは、消費者の購買力を促進します。

- 中東では、オフトレードの小売業者は、無糖、チョコレート、バニラなどの様々なフレーバーを含む、様々な植物由来の乳製品を提供することに注力しています。消費者層を拡大するために、彼らは消費者に製品の詳細(使用されている成分、使用されている種子など)といった製品に関する完全な情報を提供しています。その結果、消費者は取引外の形態で乳飲料を購入します。

- 予測期間中、国民の健康志向の高まりにより、非乳製品の需要は増加すると予想されます。その結果、消費者に対する製品の認知度が高まるため、小売ユニットへの依存度は2025~2026年に6.25%の成長が見込まれます。

植物性製品に対する需要の高まりが市場成長を促進

- 植物性栄養の重要性の高まりに伴う菜食主義者の増加が、同地域における代替乳製品品の需要を牽引しています。サウジアラビア、アラブ首長国連邦、イランは、他の中東諸国と比較して代替乳製品品の消費が著しいです。2022年には、3カ国合計でこの地域の代替乳製品消費全体の46.28%のシェアを占めていました。

- サウジアラビアは同地域における代替乳製品品の主要市場です。非乳製品バターと植物性ミルクが同国で主に消費されている代替乳製品品です。2022年には、両者を合わせて金額シェアの90%以上を占めています。同国では乳糖不耐症人口の増加と牛乳アレルギーの増加が代替乳製品品市場を牽引する重要な要因となっています。2021年現在、サウジアラビア人口の61.96%が牛乳アレルギーを持っています。

- アラブ首長国連邦は、同地域における代替乳製品品の第二の主要市場です。アラブ首長国連邦における代替乳製品品の販売額は、2022年の4,680万米ドルから2025年には6,180万米ドルの成長が見込まれています。アラブ首長国連邦における代替乳製品品の成長には、菜食主義者の増加が大きな要因のひとつとなっています。2021年現在、アラブ首長国連邦の人口の8%以上が菜食主義者です。

- 植物性栄養に対する消費者の高い意識と良好なマクロ経済環境が、イランの代替乳製品品市場を形成する主要因です。イランの代替乳製品品市場の売上高は、2018~2022年にかけて20.3%の成長率を経験しました。

中東の代替乳製品品市場の動向

中東における代替乳製品品の消費の増加は、菜食主義者の増加、動物愛護意識の向上、政府の取り組みに起因します。

- 中東における様々なタイプの代替乳製品の消費は、菜食主義者の増加によりここ数年増加傾向にあります。例えば、2022年にはアラブ首長国連邦の人口の8%以上が菜食主義者でした。ヴィーガンのライフスタイルを促進するために、各国でヴィーガンの展示会/見本市や音楽祭が開催されているほどです。加えて、動物愛護の向上や、この意識を強化するための政府の取り組みが増加していることも、代替乳製品の消費を後押しする重要な要因のひとつです。

- 乳糖不耐症の蔓延も、消費者が代替乳製品に切り替える理由のひとつです。例えばサウジアラビアでは、人口の30%以上が乳糖不耐症の問題に直面しています。サウジアラビアでは、3人に1人が乳糖不耐症とその関連要因、緩和要因について知識があります。

- 同地域の消費者の栄養選択に対する意識は高まっており、多忙なライフスタイルのため、購買決定は製品の栄養価に左右されます。さらに、消費者、特に牛乳アレルギーのある消費者は、植物性ミルク製品の摂取に熱心です。さまざまな植物性ミルク製品の中で、豆乳とアーモンドミルクは2022年にこの地域全体のシェアの大半を占めました。

- 非乳製品バターの一人当たり消費量は、2023~2024年にかけて3.56%増加すると予想されます。消費者が非乳製品バターを採用する主要動機は、動物への配慮や持続可能性に続いて、食生活の変化です。しかし、ヨーグルト、チーズ、アイスクリームのような他の代替乳製品カテゴリーはまだ非常に発展途上の段階にあります。

中東の代替乳製品産業概要

中東の代替乳製品市場はセグメント化されており、上位5社で6.12%を占めています。この市場の主要企業は、Campbell Soup Company、Danone SA、Ecomil、Green Spot、Lam Soon Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産

- 代替乳製品-原料生産

- 規制の枠組み

- サウジアラビア

- アラブ首長国連邦

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- 非乳製品バター

- 非乳製品チーズ

- 非乳製品アイスクリーム

- 非乳製品ミルク

- 製品タイプ別

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- オートミルク

- 豆乳

- 非乳製品ヨーグルト

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- バーレーン

- イラン

- クウェート

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他の中東

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Blue Diamond Growers

- Campbell Soup Company

- Danone SA

- Ecomil

- Eden Foods Inc.

- Green Spot Co. Ltd

- Lam Soon Group

- Oatly Group AB

- Sanitarium Health and Wellbeing Company

- Saudia Dairy and Foodstuff Company(SADAFCO)

- The Bridge Srl

- The Hain Celestial Group Inc.

- Upfield Holdings BV

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50000759

The Middle East Dairy Alternatives Market size is estimated at 382.3 million USD in 2025, and is expected to reach 710.8 million USD by 2030, growing at a CAGR of 13.21% during the forecast period (2025-2030).

Strong presence of supermarkets and convenience stores is boosting the dairy products sales

- In 2022, the distribution channel in the Middle East witnessed a growth of 2.69% compared to 2021. Off-trade retailing dominated the Middle Eastern retail space during the review period (2017-2022). In 2022, off-trade retailing held a share of 81.26%. In the Middle East, consumers are fascinated by off-trade retailing due to the greater convenience they get when purchasing dairy-free products.

- In on-trade channels (quick-service restaurants), the prices are fixed for non-dairy products, while consumers are given several options in off-trade channels. In the Middle East, off-trade channels offer non-dairy products at varied prices (low, medium, and high). Oat milk sold by these retailing units was available from USD 2.78 to USD 35.4 in 2022. The availability of milk at varied prices also promotes the buying power among consumers as they can purchase the products that suit their affordability parameters.

- In the Middle East, off-trade retailers focus on providing various plant-based dairy products, including different flavors such as unsweetened, chocolate, and vanilla. To increase the consumer base, they offer consumers complete information about the products, such as product specifics (ingredient used, seed used, and others). As a result, consumers purchase milk beverages through off-trade modes.

- During the forecast period, the demand for non-dairy products is expected to increase due to the rising health consciousness among the population. As a result, the dependency on retailing units is expected to observe growth during 2025-2026 by 6.25% due to higher visibility of the product to consumers.

Growing demand for plant-based products is fueling the market growth

- The rise in the vegan population concerning the rising importance of plant-based nutrition drives the demand for dairy alternatives in the region. Saudi Arabia, United Arab Emirates, and Iran exhibit significant dairy alternative consumption compared to other Middle Eastern countries. In 2022, three countries collectively held a 46.28% share of the overall dairy alternative consumption in the region.

- Saudi Arabia is the leading market for dairy alternatives in the region. Non-dairy butter and plant-based milk are majorly consumed dairy alternative products in the country. In 2022, both combinedly accounted for more than 90% of the value share. The growing lactose-intolerant population and increasing cow's milk allergy in the country have been significant factors driving the dairy alternatives market. As of 2021, 61.96% of the Saudi Arabian population had a milk allergy.

- The United Arab Emirates is the second leading market for dairy alternatives in the region. The sales value of dairy alternatives in the United Arab Emirates is anticipated to grow by USD 61.8 million in 2025, up from USD 46.8 million in 2022. The Increasing vegan population is one of the major factors for the growth of dairy alternatives in the United Arab Emirates. As of 2021, more than 8% of the United Arab Emirates population was vegan.

- High consumer awareness about plant-based nutrition and favorable macroeconomic environments are the key factors shaping the Irani dairy alternatives market. The sales of the dairy alternatives market in Iran experienced a growth rate of 20.3% from 2018 to 2022.

Middle East Dairy Alternatives Market Trends

The increase in consumption of dairy alternative products in the Middle East can be attributed to the growing vegan population, improved animal welfare awareness, and government initiatives

- The consumption of different types of dairy alternative products in the Middle East has been on the rise for the past few years due to the growing vegan population. For example, in 2022, more than 8% of the UAE population was vegan. There are even vegan exhibitions/trade shows and music festivals being conducted in different countries to promote vegan lifestyles. In addition, improved animal welfare and increasing government initiatives to strengthen this awareness are among the other key factors boosting the consumption of dairy alternatives.

- The growing prevalence of lactose intolerance is another reason consumers switch to dairy alternatives. For example, in Saudi Arabia, more than 30% of the population is facing lactose intolerance issues. One out of each three people in Saudi Arabia is knowledgeable regarding lactose intolerance disorder and its related factors and relieving factors.

- Consumers in the region are becoming increasingly aware of their nutritional choices, and owing to their busy lifestyles, their purchasing decision is dependent on the nutritional value of the product, which is driving the demand for plant-based milk in the region. Further, consumers, especially those who are allergic to milk, are keen to consume plant-based milk products. Among the different plant-based milk products, soy milk and almond milk held the majority of share across the region in 2022.

- The per capita consumption of non-dairy butter is expected to increase by 3.56% in 2023-2024. The key motivations for the consumers to adopt non-dairy butter are a concern for animals or sustainability followed by the change in dietary habits. However, other dairy alternative product categories like yogurt, cheese, and ice cream are still at a very nascent stage.

Middle East Dairy Alternatives Industry Overview

The Middle East Dairy Alternatives Market is fragmented, with the top five companies occupying 6.12%. The major players in this market are Campbell Soup Company, Danone SA, Ecomil, Green Spot Co. Ltd and Lam Soon Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 Saudi Arabia

- 4.3.2 United Arab Emirates

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Non-Dairy Butter

- 5.1.2 Non-Dairy Cheese

- 5.1.3 Non-Dairy Ice Cream

- 5.1.4 Non-Dairy Milk

- 5.1.4.1 By Product Type

- 5.1.4.1.1 Almond Milk

- 5.1.4.1.2 Cashew Milk

- 5.1.4.1.3 Coconut Milk

- 5.1.4.1.4 Oat Milk

- 5.1.4.1.5 Soy Milk

- 5.1.5 Non-Dairy Yogurt

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Bahrain

- 5.3.2 Iran

- 5.3.3 Kuwait

- 5.3.4 Oman

- 5.3.5 Qatar

- 5.3.6 Saudi Arabia

- 5.3.7 United Arab Emirates

- 5.3.8 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Blue Diamond Growers

- 6.4.2 Campbell Soup Company

- 6.4.3 Danone SA

- 6.4.4 Ecomil

- 6.4.5 Eden Foods Inc.

- 6.4.6 Green Spot Co. Ltd

- 6.4.7 Lam Soon Group

- 6.4.8 Oatly Group AB

- 6.4.9 Sanitarium Health and Wellbeing Company

- 6.4.10 Saudia Dairy and Foodstuff Company (SADAFCO)

- 6.4.11 The Bridge Srl

- 6.4.12 The Hain Celestial Group Inc.

- 6.4.13 Upfield Holdings BV

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms