|

市場調査レポート

商品コード

1686647

アフリカの乳製品代替:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Africa Dairy Alternatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの乳製品代替:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 197 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

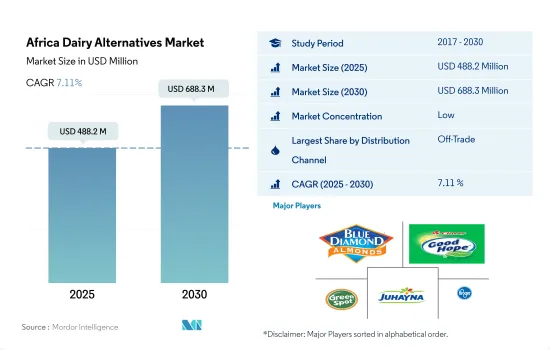

アフリカの乳製品代替市場規模は2025年に4億8,820万米ドルと推定され、2030年には6億8,830万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは7.11%で成長すると予測されます。

スーパーマーケットとハイパーマーケットでは、乳製品代替売り場の多様性強化が売上急増の原動力となります。

- スーパーマーケットとハイパーマーケットは、アフリカにおける乳製品代替品の主要な域外流通チャネルです。2022年には、スーパーマーケットとハイパーマーケットのサブセグメント全体における乳製品代替品の販売量は、商外チャネルを通じた販売量の50%を占めています。スーパーマーケットとハイパーマーケットを通じた販売は、2024~2027年の期間中に23%の金額で拡大し、2027年には2億7,228万米ドルの市場金額に達すると予測されます。これらのチャネルに対する消費者の嗜好は、季節的なオファー、大量購入の割引、乳製品代替製品の専用コーナーによる多様な製品へのアクセスによってもたらされます。

- コンビニエンスストアは、乳製品代替を購入するためにスーパーマーケットやハイパーマーケットに次いで広く選ばれている商外流通チャネルです。このサブセグメントは、2022年に商外チャネルを通じて行われた販売量全体の36%を占めました。プライベートブランドへの幅広いリーチと容易なアクセスが、消費者が他の小売チャネルよりも伝統的な食料品店を好む原動力となっています。コンビニエンスストアを通じた乳製品代替の販売額は、2024年から2027年にかけて22%の成長が見込まれます。

- オンラインチャネルを通じた乳製品代替の販売額は、2023年から2026年にかけて49.5%と最も高い成長を記録すると予測されます。インターネット利用者の増加は、乳製品代替品購入におけるオンラインチャネルの役割の進化に影響を与えています。アフリカのインターネット利用は2019年から2021年にかけて23%増加しました。2021年12月現在、アフリカのインターネット普及率は43%です。エジプトや南アフリカなどの主要国で食料品宅配アプリが増加していることも、予測期間中にオンラインチャネルを通じた販売を促進すると予測されます。

南アフリカとエジプトの消費者による菜食志向の高まりが市場成長を促進

- エジプトと南アフリカは乳製品代替品の主要地域市場であり、2022年にはアフリカ全体の販売量の66%を占めました。植物性食品に対する消費者の志向の高まりと、タンパク質と必須栄養素のニーズを満たすための植物性ミルクやチーズなどの乳製品代替品の消費が、この地域全体の乳製品代替品産業の成長を加速させると予想される主な要因です。

- 南アフリカでは、乳製品代替品の販売額は2024~2027年の間に23%拡大し、2027年には2億7,360万米ドルに達すると推定されます。この成長は、同国における菜食主義の増加に起因しています。南アフリカは、菜食主義者の人口で世界の上位30カ国に入っています。2019年以降、3万人以上の南アフリカ人がVeganuaryに登録しています。南アフリカでは、豆乳やアーモンドミルクなどの植物性ミルクが非常に好まれています。南アフリカにおける一人当たりの豆乳消費量は、2023年には0.07kgに達すると予想されています。

- アフリカのその他の地域セグメントにおける乳製品代替の売上高は、2023~2026年の間に22%の金額成長が見込まれます。アルジェリア、ケニア、ガーナといった国々が地域セグメントの成長に貢献しています。ガーナ、マラウイ、ザンビアを含むほとんどの国では、2023年までに人口の98~100%以上が乳糖不耐症に罹患すると予想されています。また、菜食主義者を支援する取り組みも行われており、これが市場の成長を後押ししています。例えば、ウガンダの人々は動物性食品の生産や消費によって感染症にかかることが多いです。動物性食品の消費を避け、減らし、植物性食品の消費を増やすために、アトラス・ヴィーガン・コミュニティは、子供たちを人獣共通感染症から守るために、初のヴィーガン・スクールを始めました。

アフリカの乳製品代替市場動向

アフリカにおける乳製品代替品の消費は、菜食主義者の増加、乳糖不耐症の有病率の上昇、消費者の栄養選択に対する意識の高まりにより増加しています。

- アフリカにおける様々なタイプの乳製品代替製品の消費は、菜食主義者の増加によりここ数年で増加しています。例えば、ほとんどの南アフリカ人は、食事から乳製品と肉をすべてカットするベジタリアンという生き方を試しています。ヴィーガンライフスタイルを促進するため、国内ではヴィーガンの展示会や見本市、音楽フェスティバルが開催されています。動物愛護の向上や、こうした意識を強化するための政府の取り組みが活発化していることも、乳製品代替の消費を後押ししている主な要因です。

- 乳糖不耐症の増加も、消費者が乳製品代替に切り替える理由のひとつです。例えば、南アフリカ、アンゴラ、カメルーン、ガーナ、ナイジェリア、ウガンダといったアフリカ諸国の多くでは、人口の80%以上が乳糖不耐症の問題に直面しています。

- ここ数年、この地域の消費者は、栄養の選択に対する意識が高まっています。多忙なライフスタイルのため、消費者の購買決定は製品の栄養価に左右され、同地域の植物性ミルク需要を牽引しています。消費者、特に牛乳にアレルギーのある消費者は、植物性乳製品の消費に熱心です。さまざまな植物性ミルクの中で、豆乳とアーモンドミルクは2022年にこの地域全体の大半のシェアを占めました。非乳製品バターの一人当たり消費量は、2023年から2024年の間に1.21%増加すると予想されます。消費者が非乳製品バターを採用する主な動機は、動物や持続可能性への配慮であり、次いで食生活の変化です。しかし、ヨーグルト、チーズ、アイスクリームといった他の乳製品代替製品カテゴリーはまだ初期段階にあります。

アフリカの乳製品代替産業概要

アフリカの乳製品代替市場は断片化されており、上位5社で5.54%を占めています。この市場の主要企業は以下の通りです。Blue Diamond Growers, Good Hope International Beverages(Pty)Ltd, Green Spot, Juhayna Food Industries and The Kroger Co.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原材料/商品生産

- 乳製品代替-原材料生産

- 規制の枠組み

- エジプト

- 南アフリカ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- 非乳製品バター

- 非乳製品ミルク

- 製品タイプ別

- アーモンドミルク

- ココナッツミルク

- オートミルク

- 豆乳

- 非乳製品ヨーグルト

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Blue Diamond Growers

- Danone SA

- Dewfresh Pty Ltd

- Earth&Co

- Good Hope International Beverages(Pty)Ltd

- Green Spot Co. Ltd

- Jetlak Foods Limited

- Juhayna Food Industries

- SunOpta Inc.

- The Kroger Co.

- Yokos Pty Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Africa Dairy Alternatives Market size is estimated at 488.2 million USD in 2025, and is expected to reach 688.3 million USD by 2030, growing at a CAGR of 7.11% during the forecast period (2025-2030).

Supermarkets and hypermarkets witness a soaring sales growth fueled by enhanced diversity in dairy alternatives aisle

- Supermarkets and hypermarkets are the region's leading off-trade distribution channels for dairy alternatives in Africa. In 2022, volume sales of dairy alternatives across the supermarkets and hypermarkets sub-segment accounted for 50% of sales through off-trade channels. Sales through supermarkets and hypermarkets are anticipated to expand at a value of 23% during the period 2024-2027 to reach a market value of USD 272.28 million in 2027. Consumer preference for these channels is driven by seasonal offers, discounts on bulk purchases, and access to diversified products through a dedicated section of dairy alternative products.

- Convenience stores are the second most widely preferred off-trade distribution channels after supermarkets and hypermarkets to purchase dairy alternatives. The sub-segment accounted for a 36% share of the overall volume sales conducted through off-trade channels in 2022. The broader reach and easy access to private-label brands drive consumer preferences for traditional grocery stores over other retail channels. The sales value of dairy alternatives through convenience stores is anticipated to grow by 22% from 2024 to 2027.

- The sales of dairy alternatives through online channels are projected to record the highest growth in value, amounting to 49.5%, during 2023-2026. The increasing number of internet users influences the evolving role of online channels in dairy alternative product purchases. Internet use in Africa increased by 23% from 2019 to 2021. As of December 2021, the internet penetration rate in Africa was 43%. The increasing number of grocery delivery apps across key countries such as Egypt and South Africa is also anticipated to drive sales through online channels during the forecast period.

Rising inclination towards Veganuary options driven by South Africa's and Egypt consumers is fueling the market growth

- Egypt and South Africa were the major regional markets for dairy alternatives, collectively accounting for a 66% share of volume sales across Africa in 2022. The growing consumer inclination toward plant-based food and the consumption of dairy alternatives, such as plant-based milk and cheese, to meet the protein and essential nutrients needs are the key factors expected to accelerate the growth of the dairy alternatives industry across the region.

- In South Africa, dairy alternative sales are estimated to expand by a value of 23% during the period 2024-2027, reaching USD 273.6 million in 2027. The growth can be attributed to the increasing veganism in the country. South Africa is among the top 30 countries worldwide in terms of its vegan population. Over 30,000 South Africans have signed up for Veganuary since 2019. Plant-based milk, such as soy and almond milk, is highly preferred in South Africa. The per capita consumption of soy milk in South Africa is expected to reach 0.07 kg in 2023.

- Sales of dairy alternatives in the rest of Africa's regional segment are estimated to grow by a value of 22% during the period 2023-2026. Countries such as Algeria, Kenya, and Ghana are contributing to the growth of the regional segment. Most countries, including Ghana, Malawi, and Zambia, are expected to have over 98-100% of their population suffering from lactose intolerance by 2023. There have also been initiatives to support vegan food, which are fueling market growth. For instance, people in Uganda often contract infections from producing and consuming animal products. To avoid or reduce the consumption of animal-based products and increase the consumption of plant-based foods, Atlas Vegan Community started the first vegan school to protect children from zoonotic disease.

Africa Dairy Alternatives Market Trends

The consumption of dairy alternative products in Africa is increasing due to the growing vegan population, rising prevalence of lactose intolerance, and increased awareness of nutritional choices among consumers

- The consumption of different types of dairy alternative products in Africa has increased over the past few years due to the growing vegan population. For example, most South Africans are experimenting with the vegetarian way of life by cutting all dairy and meat out of their diet. Vegan exhibitions/trade shows and music festivals are being conducted in the country to promote a vegan lifestyle. Improved animal welfare and increasing government initiatives to strengthen this awareness are the other key factors boosting the consumption of dairy alternatives.

- The growing prevalence of lactose intolerance is another reason consumers switch to dairy alternatives. For example, in most African countries like South Africa, Angola, Cameroon, Ghana, Nigeria, and Uganda, more than 80% of the population faces lactose intolerance issues.

- Over the past few years, consumers in the region have become increasingly aware of their nutritional choices. Due to their busy lifestyles, their purchasing decision depends on the product's nutritional value, driving the demand for plant-based milk in the region. Consumers, especially those allergic to milk, are keen to consume plant-based milk products. Among the different plant-based milk, soy and almond milk held the majority share across the region in 2022. The per capita consumption of non-dairy butter is expected to increase by 1.21% during 2023-2024. The key motivations for consumers to adopt non-dairy butter are a concern for animals or sustainability, followed by a change in dietary habits. However, other dairy alternative product categories like yogurt, cheese, and ice cream are still in the nascent stage.

Africa Dairy Alternatives Industry Overview

The Africa Dairy Alternatives Market is fragmented, with the top five companies occupying 5.54%. The major players in this market are Blue Diamond Growers, Good Hope International Beverages (Pty) Ltd, Green Spot Co. Ltd, Juhayna Food Industries and The Kroger Co. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Non-Dairy Butter

- 5.1.2 Non-Dairy Milk

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Almond Milk

- 5.1.2.1.2 Coconut Milk

- 5.1.2.1.3 Oat Milk

- 5.1.2.1.4 Soy Milk

- 5.1.3 Non-Dairy Yogurt

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Egypt

- 5.3.2 Nigeria

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Blue Diamond Growers

- 6.4.2 Danone SA

- 6.4.3 Dewfresh Pty Ltd

- 6.4.4 Earth&Co

- 6.4.5 Good Hope International Beverages (Pty) Ltd

- 6.4.6 Green Spot Co. Ltd

- 6.4.7 Jetlak Foods Limited

- 6.4.8 Juhayna Food Industries

- 6.4.9 SunOpta Inc.

- 6.4.10 The Kroger Co.

- 6.4.11 Yokos Pty Ltd

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms