|

市場調査レポート

商品コード

1686602

アジア太平洋地域の乳製品代替:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Dairy Alternatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の乳製品代替:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 239 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

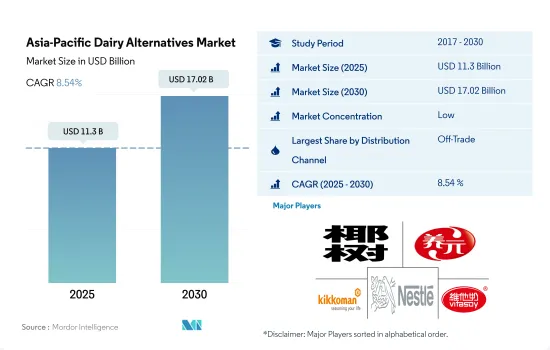

アジア太平洋地域の乳製品代替市場規模は2025年に113億米ドルと推定され、予測期間(2025-2030年)のCAGRは8.54%で成長し、2030年には170億2,000万米ドルに達すると予測されます。

組織小売チャネルの強力な浸透が市場成長を促進

- 同地域の乳製品代替品販売では、商外チャネルが大きな役割を果たしています。取引外チャネルでは、スーパーマーケットとハイパーマーケットがアジア太平洋乳製品代替品市場における最大の流通チャネルです。これらのチャネルは、特に大都市と新興国市場において近接しているため、市場で入手可能な多種多様な製品の中から消費者の購買決定に影響を与えるという利点があります。2022年には、スーパーマーケットとハイパーマーケットのサブセグメントが金額シェアの66.7%を占めました。

- 同地域にはオン・トレード・チャネルの市場はあまりなく、発展途上の段階にあります。消費者は家庭での乳製品代替を好み、レストランや外食店舗で消費することはあまりないです。植物性ミルクや非乳製品バターの人気は高まっており、地域のレストランでは、特にカクテル、スムージー、コーヒー、エスプレッソベースのドリンクの材料として植物性ミルクを使うところもあります。そのため、オン・トレード・チャネルを通じた植物性ミルクの販売額は、2021年と比較して2022年には4.5%増加しました。

- 植物性ミルクは、すべての乳製品代替製品の中でオフ・トレード・チャネルにおけるシェアの大半を占めました。2022年には、植物性ミルクが金額シェアの85%以上を占めました。

- オンライン・チャネルは、オフ・トレード・セグメントで最も急成長する流通チャネルになると予想されます。2023~2025年の前年比成長率は4.6%と予測されます。食料品のオンラインショッピングに移行した買い物客の主な動機は利便性です。

中国、日本、オーストラリアは他のアジア諸国に比べて乳製品代替の消費が著しいです。

- 植物性栄養の重要性が高まった結果、ビーガン人口が増加し、この地域における乳製品代替の需要を牽引しています。中国、日本、オーストラリアは他のアジア諸国に比べて乳製品代替の消費が著しいです。2023年には、この地域の乳製品代替品消費全体の79.77%のシェアをこれらの国が占めています。代替タンパク質に対する消費者の関心の高まりが、中国における乳製品代替の消費を促進する主な要因です。スーパーマーケットやハイパーマーケットとの戦略的提携を通じた世界ブランドの浸透が、中国の消費者が乳製品代替である牛乳やチーズを選ぶように影響を与えています。

- 植物性栄養に対する消費者の高い意識と良好なマクロ経済環境が、オーストラリアの乳製品代替産業を形成する主な要因です。非乳製品バターと植物性ミルクは、オーストラリアのミレニアル世代の消費者に好まれる必須製品です。2022年には、植物性ミルクはオーストラリアで消費される乳製品代替全体の84.76%を占めていました。オーストラリア人は、毎週約半量の代用乳を消費しています。オーストラリアではアーモンドミルクと豆乳の人気が高まっています。2歳以上のオーストラリア人の50%以上がカルシウムやその他のミネラルを十分に摂取していないため、栄養を加えた植物性ミルクに顧客が集まっています。

- インドはベジタリアンの顧客が増加している最も急成長している国です。2021年、インドの参加者数は世界で3番目に多く、約6万人が国際団体Veganuaryのキャンペーンに参加しました。乳製品代替品の販売額は予測期間中にCAGR 9.83%を記録すると予測されます。

アジア太平洋地域の乳製品代替市場動向

乳製品代替品の消費は、乳糖不耐症人口の増加と菜食主義者の大幅な増加により、この地域全体で増加傾向にあります。

- 乳製品代替品の消費は、乳糖不耐症人口の増加と相まってビーガン人口が大幅に増加しているため、地域全体で増加傾向にあります。2021年、韓国では約250万人が菜食主義者でした。これはその後2年間で大幅に増加し、現在も成長を続けています。同様に、オーストラリアは国民一人当たりの菜食主義者の割合が世界で3番目に高いです。

- 乳糖不耐症はアジア諸国、特に東アジアでは一般的で、人口の70~100%近くが乳糖不耐症です。牛乳アレルギーは、幼児によく見られる食物アレルギーのひとつです。日本の消費者の多くは乳糖不耐症で、牛乳や乳製品を摂取していないです。2022年現在、オーストラリアでは、乳幼児の約50人に1人が牛乳アレルギーの兆候を示しています。そのため、植物由来の乳製品に対する需要は、この地域全体で徐々に高まっています。

- 乳製品代替の中でも、豆乳やアーモンドミルクのような植物性ミルクは、2022年の地域市場全体で大半のシェアを占めています。乳製品代替ミルクの消費量では、中国がこの地域の主要国です。植物性ミルクの中では、大豆飲料が伝統的に中国で最も人気があります。アジア太平洋地域では、非乳製品バターの一人当たり消費量は2023年から2024年にかけて3.45%増加すると推定されます。消費者が非乳製品バターを採用する主な動機は、動物への関心の高まりと持続可能性であり、次いで食生活の健康的な変化です。

アジア太平洋地域の乳製品代替産業の概要

アジア太平洋地域の乳製品代替市場は断片化されており、上位5社で36.65%を占めています。この市場の主要企業は以下の通りです。Coconut Palm Group, Hebei Yangyuan Zhihui Beverage, Kikkoman Corporation, Nestle SA and Vitasoy International Holdings Ltd(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原材料/商品生産

- 乳製品代替-原材料生産

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- 非乳製品バター

- 非乳製品チーズ

- 非乳製品アイスクリーム

- 非乳製品ミルク

- 製品タイプ別

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- ヘーゼルナッツミルク

- ヘンプミルク

- オートミルク

- 豆乳

- 非乳製品ヨーグルト

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- パキスタン

- 韓国

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Blue Diamond Growers

- Campbell Soup Company

- Coconut Palm Group Co. Ltd

- Danone SA

- Hebei Yangyuan Zhihui Beverage Co. Ltd

- Kikkoman Corporation

- Nestle SA

- Oatly Group AB

- Sanitarium Health and Wellbeing Company

- The Hershey Company

- Vitasoy International Holdings Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Dairy Alternatives Market size is estimated at 11.3 billion USD in 2025, and is expected to reach 17.02 billion USD by 2030, growing at a CAGR of 8.54% during the forecast period (2025-2030).

Strong penetration of organized retail channels is fueling the market growth

- The off-trade channel plays a major role in the region's sales of dairy alternative products. In the off-trade channels segment, supermarkets and hypermarkets are the largest distribution channels in the Asia-Pacific dairy alternatives market. The proximity factor of these channels, especially in large and developed cities, gives them an added advantage of influencing the consumer's decision to purchase among the large variety of products available in the market. In 2022, the supermarkets and hypermarkets sub-segment accounted for 66.7% of the value share.

- The region does not have a considerable market for on-trade channels and is in the nascent stage. Consumers prefer dairy alternatives at home and are less likely to consume from a restaurant or foodservice outlet. Plant-based milk and non-dairy butter are increasing in popularity, and some regional restaurants use plant-based milk, particularly as an ingredient option in cocktails, smoothies, coffees, and espresso-based drinks. Thus, the sales value of plant-based milk through on-trade channels increased by 4.5% in 2022 compared to 2021.

- Plant-based milk accounted for the majority of share in off-trade channels among all dairy alternative products. In 2022, plant-based milk accounted for more than 85% of the value share.

- Online channel is expected to be the fastest-growing distribution channel in the off-trade segment. It is projected to register a Y-o-Y growth value of 4.6% during 2023-2025. Convenience is the primary motivation for shoppers who have transitioned to shopping for groceries online.

China, Japan, and Australia exhibit significant dairy alternative consumption compared to other Asian countries

- The rise in the vegan population as a result of the rising importance of plant-based nutrition drives the demand for dairy alternatives in the region. China, Japan, and Australia exhibit significant dairy alternative consumption compared to other Asian countries. In 2023, the countries collectively held a 79.77% share of the overall dairy alternative consumption in the region. Rising consumer interest in alternative protein is the key factor driving the consumption of dairy alternatives in China. The penetration of global brands through strategic partnerships with supermarkets and hypermarkets is influencing Chinese consumers to opt for alternative dairy milk and cheese.

- High consumer awareness about plant-based nutrition and favorable macroeconomic environments are the key factors shaping the Australian dairy alternative industry. Non-dairy butter and plant-based milk are essential products preferred by millennial consumers in Australia. In 2022, plant-based milk had an 84.76% share of the overall dairy alternatives consumed in Australia. Australians consumed around half a metric cup of milk substitutes every week. Almond and soy milk are becoming more popular in Australia. Over 50% of Australians aged two and older do not get enough calcium and other minerals, which is attracting customers toward plant milk with added nutrition.

- India is the fastest-growing country with an increasing number of vegetarian customers. In 2021, India had the world's third-highest number of participants, with around 60,000 people joining the campaign, Veganuary, an international organization. The sales value of dairy alternatives is estimated to record a CAGR of 9.83% during the forecast period.

Asia-Pacific Dairy Alternatives Market Trends

The consumption of dairy alternatives is on the rise across the region owing to a significant rise in the vegan population, coupled with a growing lactose-intolerant population

- The consumption of dairy alternatives is on the rise across the region owing to a significant rise in the vegan population, coupled with a growing lactose-intolerant population. In 2021, around 2.5 million people in South Korea followed a vegan diet. This has since increased significantly in the following two years and continues to grow. Similarly, Australia has the third-highest percentage of vegans per capita globally.

- Lactose intolerance is common in Asian countries, particularly in East Asia, where nearly 70-100% of the population has lactose intolerance. Cow milk allergy is one of the common food allergies in young children. Many Japanese consumers are lactose-intolerant and do not consume milk or milk products. As of 2022, in Australia, around one in 50 babies and young children showed signs of an allergy to cow's milk. Therefore, the demand for plant-based dairy products has increased gradually across the region.

- Among dairy alternatives, plant-based milk like soy and almond milk held the majority share across the regional market in 2022. China is the leading country across the region in terms of consumption of dairy alternatives milk. Among plant-based milk, soy drinks have traditionally been the most popular in China due to the country's long-standing tradition of soy consumption and its wide availability. In the Asia-Pacific region, the per capita consumption of non-dairy butter is estimated to increase by 3.45% in 2023-2024. The key motivations for consumers to adopt non-dairy butter are growing concerns for animals and sustainability, followed by a healthier change in dietary habits.

Asia-Pacific Dairy Alternatives Industry Overview

The Asia-Pacific Dairy Alternatives Market is fragmented, with the top five companies occupying 36.65%. The major players in this market are Coconut Palm Group Co. Ltd, Hebei Yangyuan Zhihui Beverage Co. Ltd, Kikkoman Corporation, Nestle SA and Vitasoy International Holdings Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Japan

- 4.3.5 South Korea

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Non-Dairy Butter

- 5.1.2 Non-Dairy Cheese

- 5.1.3 Non-Dairy Ice Cream

- 5.1.4 Non-Dairy Milk

- 5.1.4.1 By Product Type

- 5.1.4.1.1 Almond Milk

- 5.1.4.1.2 Cashew Milk

- 5.1.4.1.3 Coconut Milk

- 5.1.4.1.4 Hazelnut Milk

- 5.1.4.1.5 Hemp Milk

- 5.1.4.1.6 Oat Milk

- 5.1.4.1.7 Soy Milk

- 5.1.5 Non-Dairy Yogurt

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 New Zealand

- 5.3.8 Pakistan

- 5.3.9 South Korea

- 5.3.10 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Blue Diamond Growers

- 6.4.2 Campbell Soup Company

- 6.4.3 Coconut Palm Group Co. Ltd

- 6.4.4 Danone SA

- 6.4.5 Hebei Yangyuan Zhihui Beverage Co. Ltd

- 6.4.6 Kikkoman Corporation

- 6.4.7 Nestle SA

- 6.4.8 Oatly Group AB

- 6.4.9 Sanitarium Health and Wellbeing Company

- 6.4.10 The Hershey Company

- 6.4.11 Vitasoy International Holdings Ltd

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms