|

市場調査レポート

商品コード

1683829

ドイツの乳製品代替:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Germany Dairy Alternatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの乳製品代替:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 197 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

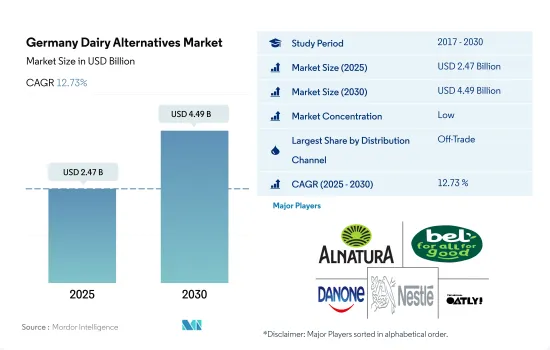

ドイツの乳製品代替の市場規模は2025年に24億7,000万米ドルと推定され、2030年には44億9,000万米ドルに達し、予測期間(2025-2030年)のCAGRは12.73%で成長すると予測されます。

組織小売チャネルの強力な浸透が市場成長を促進

- ドイツの乳製品代替市場の流通チャネルを支配しているのは、非商業部門です。オフトレード・チャネルの中では、オンライン小売のサブセグメントが最も急成長しており、予測期間中のCAGRは15.6%を記録すると予測されています。eコマースの成長により、企業はより大きなターゲット市場にアクセスし、顧客のニーズに効果的に応えることができるようになりました。多くの人々が多忙なスケジュールや2020年の全国的な封鎖により、食品、特に乳製品代替をオンラインで注文するようになりました。乳製品代替の主なeコマース・チャネルは、ダイレクト・トゥ・コンシューマー、クリック・アンド・コレクト、小売食料品配送、コンシェルジュ・サービスの4つです。

- パンデミックの影響で外食店舗が閉鎖されたため、全国のオントレード・チャネルを通じた乳製品代替の販売額は2020年に2%減少しました。同年、ドイツでは機能的レストランは65,090店しか記録されず、2019年から8.49%減少しました。全流通チャネルのデータに基づくと、2022年のドイツ全体の消費量は1人当たり約5.03kgで、乳製品代替の消費量は2017年から3.4kg増加しています。オントレード・チャネルは予測期間中に10.7%のCAGRを記録しそうです。

- オフトレードは、予測期間中にCAGR値15.7%を記録し、最も急成長する流通チャネルになると予測されます。この増加は、スーパーマーケットやオンライン小売店で広く入手可能な乳製品代替製品に対する需要の高まりに伴って予想されます。世界中の主要小売業者が採用しているオムニチャネルアプローチも、乳製品デザート市場を牽引しています。REWE、Edeka、Aldi Sud、Normaなどの小売業者は、オムニチャネル・ショッピング、特に実店舗へのオンライン機能の拡張と統合に注力しています。

ドイツの乳製品代替市場動向

同国におけるビーガン運動の高まりが、ドイツにおける乳製品代替の消費に影響を与える主な要因として浮上しています。

- 欧州におけるビーガン運動はドイツがリードしています。ベルリンとハンブルグは菜食主義者に優しい都市として世界のトップ5にランクインし、ドイツは菜食主義者にとって世界で6番目に良い国となっています。他の欧州諸国と比べても、ベジタリアンとビーガンの割合が最も高い国のひとつです。ドイツでは158万人が菜食主義者であり、800万人以上がベジタリアン料理を食べています。フレキシタリアンはドイツ人口の30%以上を占める。ヴィーガン、ベジタリアン、フレキシタリアンのドイツ人の増加が、植物性食品の市場を牽引しています。

- ドイツ人は2022年に31万8,500トンの代替乳を消費します。ドイツ人口の約3分の1は牛乳を全く飲まず、代替乳を利用しています。2022年のドイツの代替乳消費量は2021年と比較して19.94%増加しました。人口の約32%が2022年には乳製品の消費を減らすつもりです。ドイツの消費者の約48%が、オーガニック、クリーンラベル、アレルゲンフリーの製品は、植物(肉や乳製品の代替品など)に関して重要であると回答しました。2020年にドイツで導入される全飲食品の20%のパッケージにヴィーガンの謳い文句が記載され、2016年の14%から増加しました。ドイツの消費者の間でヴィーガンフレンドリーな料理への需要が高まっていることから、乳製品代替品の消費動向が拡大すると予想されます。欧州のビーガン人口は2016年の130万人から2020年には260万人に増加します。Alpro、Bayerngluck、Oatly、Whole Foods、Miyokoなどの主流ブランドとは別に、伝統的な企業もヴィーガン乳製品市場で地位を確立しており、Soyana、Lord of Tofu、Soyatooなどのレーベルから乳製品代替を提供しています。

ドイツの乳製品代替産業概要

ドイツの乳製品代替市場は断片化されており、上位5社で35.58%を占めています。この市場の主要企業は以下の通り。 AlnaturA Produktions-und Handels GmbH, Bel Group, Danone SA, Nestle SA and Oatly Group AB(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原材料/商品生産

- 乳製品代替-原材料生産

- 規制の枠組み

- ドイツ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- カテゴリー

- 非乳製品バター

- 非乳製品チーズ

- 非乳製品アイスクリーム

- 非乳製品ミルク

- 製品タイプ別

- アーモンドミルク

- カシューミルク

- ココナッツミルク

- ヘーゼルナッツミルク

- ヘンプミルク

- オートミルク

- 豆乳

- 非乳製品ヨーグルト

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)。

- AlnaturA Produktions-und Handels GmbH

- Bel Group

- Danone SA

- Nestle SA

- Oatly Group AB

- Simply V

- Upfield Holdings BV

- VBites Foods Ltd

- Veganz Group

- Wilmersburger GmbH

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 5000405

The Germany Dairy Alternatives Market size is estimated at 2.47 billion USD in 2025, and is expected to reach 4.49 billion USD by 2030, growing at a CAGR of 12.73% during the forecast period (2025-2030).

Strong penetration of organized retail channels fueling the market growth

- The off-trade segment dominates the distribution channels of the German dairy alternatives market. Among off-trade channels, the online retail sub-segment is the fastest-growing one, projected to record a CAGR of 15.6% over the forecast period. The growth of e-commerce has allowed companies to access a larger target market and effectively serve customer needs. Many people started ordering food items, particularly dairy alternatives, online due to their hectic schedules and the nationwide lockdown in 2020. The four main e-commerce channels for dairy alternatives were direct-to-consumer, click-and-collect, retail grocery delivery, and concierge services.

- The sales value of dairy alternatives through on-trade channels across the country declined by 2% in 2020 as foodservice outlets were shut down due to the pandemic. In the same year, Germany recorded only 65,090 functional restaurants, a decrease of 8.49% from 2019. Based on the data from all distribution channels, the overall consumption in Germany was around 5.03 kg per person in 2022, with a 3.4 kg rise in the consumption of dairy alternatives since 2017. The on-trade channel is likely to record a CAGR of 10.7% during the forecast period.

- Off-trade is projected to be the fastest-growing distribution channel, registering a CAGR value of 15.7% during the forecast period. This increase is anticipated in line with the rising demand for dairy alternative products, which are widely accessible at supermarkets and online retailers. The omnichannel approach adopted by major retailers across the globe is also driving the market for dairy desserts. Retailers such as REWE, Edeka, Aldi Sud, and Norma focus on omnichannel shopping, particularly expanding and integrating online capabilities into brick-and-mortar stores.

Germany Dairy Alternatives Market Trends

The rising vegan movement in the country has emerged as a major factor influencing the consumption of dairy alternatives in Germany

- The vegan movement in Europe has seen Germany take the lead. Berlin and Hamburg both rank in the top five cities in the world for vegan friendliness, making Germany the sixth-best nation in the world for vegans. In comparison to other European nations, the nation boasts one of the highest percentages of vegetarians and vegans. In Germany, 1.58 million people follow a vegan diet, and over 8 million people eat vegetarian food. Flexitarians make up more than 30% of the German population. Growing numbers of Germans that are vegan, vegetarian, and flexitarian are driving the market for plant-based goods.

- Germans consumed 318.5 thousand metric tons of milk alternatives in 2022. About one-third of the German population did not drink milk at all but used milk alternatives. German dairy alternatives consumption increased by 19.94% in 2022 compared to 2021. Around 32% of the population intended to consume less dairy in 2022. About 48% of German consumers stated that an organic, clean-label, allergen-free product is significant to them regarding plants (such as meat and dairy substitutes). A vegan claim was made on the packaging of 20% of all food and beverage products introduced in Germany in 2020, up from 14% in 2016. The growing demand for vegan-friendly cuisine among consumers in Germany is anticipated to increase the consumption trends of dairy substitutes. The number of vegans in Europe increased from 1.3 million in 2016 to 2.6 million in 2020. Apart from the mainstream brands such as Alpro, Bayerngluck, Oatly, Whole Foods, and Miyoko, traditional companies have also established themselves in the vegan dairy market, offering dairy alternatives from labels like Soyana, Lord of Tofu, and Soyatoo.

Germany Dairy Alternatives Industry Overview

The Germany Dairy Alternatives Market is fragmented, with the top five companies occupying 35.58%. The major players in this market are AlnaturA Produktions- und Handels GmbH, Bel Group, Danone SA, Nestle SA and Oatly Group AB (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 Germany

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Category

- 5.1.1 Non-Dairy Butter

- 5.1.2 Non-Dairy Cheese

- 5.1.3 Non-Dairy Ice Cream

- 5.1.4 Non-Dairy Milk

- 5.1.4.1 By Product Type

- 5.1.4.1.1 Almond Milk

- 5.1.4.1.2 Cashew Milk

- 5.1.4.1.3 Coconut Milk

- 5.1.4.1.4 Hazelnut Milk

- 5.1.4.1.5 Hemp Milk

- 5.1.4.1.6 Oat Milk

- 5.1.4.1.7 Soy Milk

- 5.1.5 Non-Dairy Yogurt

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Specialist Retailers

- 5.2.1.4 Supermarkets and Hypermarkets

- 5.2.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 AlnaturA Produktions- und Handels GmbH

- 6.4.2 Bel Group

- 6.4.3 Danone SA

- 6.4.4 Nestle SA

- 6.4.5 Oatly Group AB

- 6.4.6 Simply V

- 6.4.7 Upfield Holdings BV

- 6.4.8 VBites Foods Ltd

- 6.4.9 Veganz Group

- 6.4.10 Wilmersburger GmbH

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms