|

市場調査レポート

商品コード

1684028

南米の菓子類:市場シェア分析、産業動向&統計、成長動向予測(2025年~2030年)South America Confectionery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の菓子類:市場シェア分析、産業動向&統計、成長動向予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 255 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

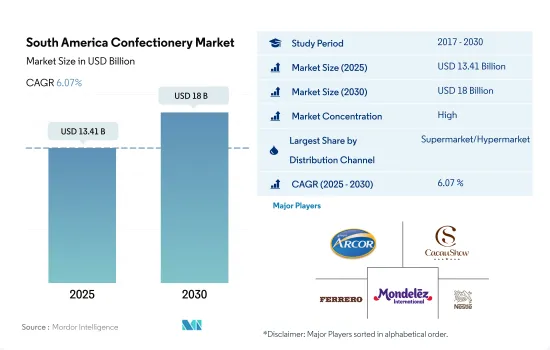

南米の菓子類市場規模は2025年に134億1,000万米ドルと推計され、2030年には180億米ドルに達し、予測期間(2025年~2030年)のCAGRは6.07%で成長すると予測されます。

Jumbo、Metro、Carrefour、Makroといった人気のコンビニエンスストアの存在と近代的な小売チャネルの開発により、コンビニエンスストアやスーパーマーケットを通じた菓子類の販売が促進されています。

- 南米では、流通チャネル部門は2023年に金額ベースで2022年比5.28%の成長率を維持しました。予測される拡大は、市場内で消費者が便利なショッピング施設を好むようになっていることが背景にあります。コンビニエンスストア・セグメントは、2023年には数量ベースで最大の小売単位となりました。この地域で人気のあるコンビニエンスストアには、Jumbo、Metro、Carrefour、Makro、D1、Super Interなどがあります。2028年までに、同地域のコンビニエンスストア部門は数量ベースで6.37%の成長を記録すると推定されます。

- スーパーマーケットとハイパーマーケットは菓子類市場で2番目に大きなチャネルです。このチャネルは、売上高で2022年と比較して2023年には金額で4.77%成長しました。スーパーマーケットやハイパーマーケットのような近代的な小売チャネルの開発により、消費者が高品質のチョコレート製品を購入することが可能になりました。南米諸国では、これらのチャネルが近接しているため、市場で入手可能な多種多様な製品の中から消費者の購入決定に影響を与えるという利点があります。

- オンライン・チャネルは、南米における菓子類消費の流通チャネルとして最も急成長しており、予測期間中の予想CAGRは6.32%です。消費者は、迅速で便利な配達オプションを提供するオンライン・チャネルを好みます。同地域のインターネット普及率の高さも、オンライン・チャネルの需要を後押ししています。2023年7月現在、この地域のすべての国の中で、アルゼンチンとブラジルのインターネット普及率は99%と最も高いです。

パーソナライズされた間食への傾倒と罪悪感のない嗜好の高まりがこの地域の主要市場促進要因であり、ブラジルが市場シェアの60%以上を占める。

- ブラジルは同地域の主要市場であり、アルゼンチンがこれに続きます。便利で嗜好性の高い間食に対する消費者の嗜好の高まりが同地域の主要市場促進要因です。2023年現在、ブラジルの16~34歳の消費者の39%がリラックス/ストレス解消のために間食をとっています。また、35歳以上の消費者の32%が、スナックを食べることで不安に対処できると考えています。

- ブラジルでは、チョコレートが最も消費されている菓子類であり、2023年の菓子類市場全体における数量ベースのシェアは81.72%でした。ブラジルの消費者は、チョコレートをその風味からユニークで欠かせない嗜好品として認識しています。2022年には、消費者の67%が週に1回以上チョコレートを消費しています。スナックバーは同国で最も急成長している分野であり、金額ベースで2023年~2030年のCAGRは7%と予想されます。市場成長の要因は、罪悪感のない嗜好品への消費者のシフトです。2022年には、消費者の81%が健康上のニーズに合わせてカスタマイズされたスナックを好むようになりました。

- アルゼンチンは同地域で最も急成長している菓子類市場です。アルゼンチン市場は予測期間中、金額ベースでCAGR 11.38%で拡大すると予測されます。アルゼンチンは世界有数の間食大国であり、通常の食事時間以外に1日のうち何度も間食が行われます。このことが菓子類市場の成長に寄与しており、砂糖菓子が主に消費され、2023年には数量ベースで73.78%のシェアを占める。パスティーユ、グミ、ゼリー、トフィーが同国で広く消費されている砂糖菓子類で、2023年の数量シェアは合計で68.16%を占める。

- その他南米では、チリとペルーが市場成長を牽引する主要国であり、2022年には合計で販売量の60%以上を占める。

南米の菓子類市場の動向

クリーン・ラベル、ナチュラル、オーガニック・チョコレートなど健康的な商品の導入に伴う広告への旺盛な支出が市場成長を支える

- ブラジルは依然として南米における著名な菓子類消費国です。2022年にはブラジルの人口の75%がチョコレートを消費し、ブラジルの消費者の35%が他のどの飲食物よりもチョコレートを好みました。

- クリエイティブな広告キャンペーンとパッケージは、同地域における菓子の衝動買いに影響を与える最も顕著な要因です。スナックのパッケージや原材料に関しては、消費者にとって持続可能性がますます重要な要素となっています。

- 南米の消費者は高級菓子への関心を高めています。ブラジルでは、2023年時点で消費者の76%が、オーガニック・チョコレートやビーガン・チョコレートなど、高品質でプレミアムなスナック菓子にもっとお金を払うことを望んでいます。経済的要因は、ブラジルの消費者のチョコレート購買行動に影響を与える重要な属性です。

- 低糖または低カロリーのスナック菓子に対する消費者の志向の高まりは、予測期間中に菓子類のヘルシーなバリエーションに有利な機会を創出すると予測されます。2021年には、「砂糖ゼロ」(46%)と「ライト」(55%)が、ブラジルの無糖食品と減糖食品でそれぞれ最も一般的な糖質表示でした。

南米の菓子類産業の概要

南米の菓子類市場はかなり統合されており、上位5社で66.04%を占めています。この市場の主要企業は以下の通り。 Arcor S.A.I.C, Cacau Show, Ferrero International SA, Mondelez International Inc. and Nestle SA.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子

- チョコレート

- 菓子類別

- ダークチョコレート

- ミルク&ホワイトチョコレート

- ガム

- 菓子類別

- バブルガム

- チューインガム

- 砂糖含有量別

- 砂糖入りチューインガム

- 無糖チューインガム

- スナック菓子

- 菓子類別

- シリアル・バー

- フルーツ&ナッツバー

- プロテイン・バー

- 砂糖菓子類

- 菓子類別

- ハードキャンディー

- ロリポップ

- ミント

- パスティル、グミ、ゼリー

- トフィーとヌガー

- その他

- チョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット

- その他

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arcor S.A.I.C

- Barry Callebaut AG

- Cacau Show

- Chocoladefabriken Lindt & Sprungli AG

- Colombina SA

- Dori Alimentos SA

- Ferrero International SA

- Florestal Alimentos SA

- Grupo de Inversiones Suramericana SA

- Kellogg Company

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Perfetti Van Melle BV

- Riclan SA

- The Hershey Company

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001801

The South America Confectionery Market size is estimated at 13.41 billion USD in 2025, and is expected to reach 18 billion USD by 2030, growing at a CAGR of 6.07% during the forecast period (2025-2030).

The presence of popular convenience stores like Jumbo, Metro, Carrefour, and Makro, along with the development of modern retail channels, promotes confectionery sales through convenience stores and supermarkets

- In South America, the distribution channel segment maintained a growth rate of 5.28% by value in 2023 compared to 2022. The projected expansion is driven by consumers' increasing preference for convenient shopping facilities within the market. The convenience store segment was the largest retail unit in terms of volume in 2023. Some of the popular convenience stores in the region are Jumbo, Metro, Carrefour, Makro, D1, and Super Inter. By 2028, the convenience store segment in the region is estimated to register a growth of 6.37% by volume.

- Supermarkets and hypermarkets are the second-largest channels in the confectionery market. The channel grew by 4.77% by value in 2023 compared to 2022 in terms of sales. The development of modern retail channels such as supermarkets and hypermarkets has made it feasible for consumers to purchase high-quality chocolate products. The proximity factor of these channels in the South American countries provides them with an added advantage of influencing the consumer's decision to purchase among the large variety of products available in the market.

- Online channels are the fastest-growing distribution channel for the consumption of confectionery products in South America, registering an anticipated CAGR of 6.32% during the forecast period. Consumers prefer online channels as they provide quick, convenient delivery options. The high internet penetration in the region also drives the demand for online channels. Among all the countries in the region, Argentina and Brazil had the highest internet penetration, at 99%, as of July 2023.

The inclination toward personalized snacking and rising preference for guilt-free indulgence are key market drivers in the region, with Brazil accounting for more than 60% of the market share

- Brazil is identified as the major market in the region, followed by Argentina. The rise in consumer preference for convenient indulgent snacking is identified as the key market driver in the region. As of 2023, 39% of Brazilian consumers aged 16-34 snacked to relax/de-stress. Also, 32% of consumers aged 35+ believed that eating snacks helped them deal with anxiety.

- In Brazil, chocolate was the most consumed confection, with an 81.72% share of the overall confectionery market in 2023 in terms of volume. Brazilians perceive chocolate as a unique and essential indulgent snack due to its flavor. In 2022, 67% of consumers consumed chocolate at least once a week. Snack bar is the fastest growing segment in the country, with an anticipated CAGR of 7% during 2023-2030 in terms of value. The market growth is attributed to the consumer shift toward guilt-free indulgence. In 2022, 81% of consumers preferred personalized snacks as per their health needs.

- Argentina is identified as the fastest-growing confectionery market in the region. The Argentine market is anticipated to expand at a CAGR of 11.38% in terms of value during the forecast period. Argentina is one of the powerhouse snackers globally, where snacking occurs at multiple points during the day alongside regular mealtimes. This, in turn, contributes to the growth of the confectionery market, wherein sugar confectionery is largely consumed, with a share of 73.78% in 2023 in terms of volume. Pastilles, gummies, jellies, and toffees are widely consumed sugar confectionery variants in the country, collectively accounting for 68.16% of the volume share in 2023.

- In the Rest of South America, Chile and Peru are major countries driving the market growth, collectively covering more than 60% of the sales, in terms of volume, in 2022.

South America Confectionery Market Trends

Strong spending on advertising along with the introduction of healthy variants like clean label, natural, and organic chocolates support the market growth

- Brazil remains the prominent confectionery consumer in South America. In 2022, 75% of the Brazilian population consumed chocolate, and 35% of Brazilian consumers preferred chocolate over any other food or drink.

- Creative Advertisement campaigns and packaging are the most prominent factors influencing the impulse buying of confectionery in the region. Sustainability is an increasingly important factor for consumers when it comes to snack packaging and ingredients.

- Consumers in South America are becoming more interested in premium confectionary items. In Brazil, as of 2023, 76% of consumers are willing to pay more for high-quality/premium snacks, including organic chocolates and vegan chocolates. Economic factors are a significant attribute influencing chocolate buying behaviors among consumers in Brazil.

- The rising consumer inclination toward low-sugar or low-calorie snack food is estimated to create lucrative opportunities for healthy variants of confectionery during the forecast period. In 2021, 'Zero sugar' (46%) and 'light' (55%) were the most common sugar claims in sugar-free and reduced-sugar food products, respectively, in Brazil.

South America Confectionery Industry Overview

The South America Confectionery Market is fairly consolidated, with the top five companies occupying 66.04%. The major players in this market are Arcor S.A.I.C, Cacau Show, Ferrero International SA, Mondelez International Inc. and Nestle SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confections

- 5.1.1 Chocolate

- 5.1.1.1 By Confectionery Variant

- 5.1.1.1.1 Dark Chocolate

- 5.1.1.1.2 Milk and White Chocolate

- 5.1.2 Gums

- 5.1.2.1 By Confectionery Variant

- 5.1.2.1.1 Bubble Gum

- 5.1.2.1.2 Chewing Gum

- 5.1.2.1.2.1 By Sugar Content

- 5.1.2.1.2.1.1 Sugar Chewing Gum

- 5.1.2.1.2.1.2 Sugar-free Chewing Gum

- 5.1.3 Snack Bar

- 5.1.3.1 By Confectionery Variant

- 5.1.3.1.1 Cereal Bar

- 5.1.3.1.2 Fruit & Nut Bar

- 5.1.3.1.3 Protein Bar

- 5.1.4 Sugar Confectionery

- 5.1.4.1 By Confectionery Variant

- 5.1.4.1.1 Hard Candy

- 5.1.4.1.2 Lollipops

- 5.1.4.1.3 Mints

- 5.1.4.1.4 Pastilles, Gummies, and Jellies

- 5.1.4.1.5 Toffees and Nougats

- 5.1.4.1.6 Others

- 5.1.1 Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Arcor S.A.I.C

- 6.4.2 Barry Callebaut AG

- 6.4.3 Cacau Show

- 6.4.4 Chocoladefabriken Lindt & Sprungli AG

- 6.4.5 Colombina SA

- 6.4.6 Dori Alimentos SA

- 6.4.7 Ferrero International SA

- 6.4.8 Florestal Alimentos SA

- 6.4.9 Grupo de Inversiones Suramericana SA

- 6.4.10 Kellogg Company

- 6.4.11 Mars Incorporated

- 6.4.12 Mondelez International Inc.

- 6.4.13 Nestle SA

- 6.4.14 Perfetti Van Melle BV

- 6.4.15 Riclan SA

- 6.4.16 The Hershey Company

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms