|

市場調査レポート

商品コード

1684030

英国の菓子類:市場シェア分析、産業動向、成長予測(2025年~2030年)UK Confectionery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の菓子類:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 242 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

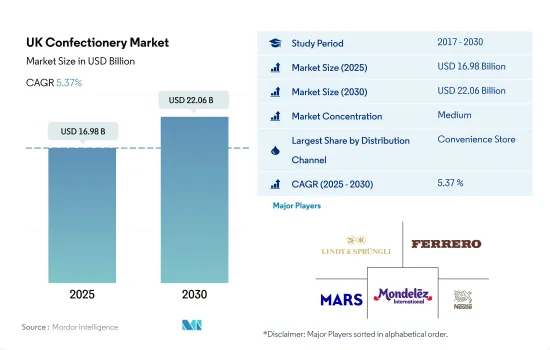

英国の菓子類市場規模は2025年に169億8,000万米ドルと推計され、2030年には220億6,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは5.37%で成長すると予測されます。

スーパーマーケット、ハイパーマーケット、コンビニエンスストアは、営業時間が長く、幅広い菓子ブランドを扱っているため、合計で市場シェアの75%以上を占める。

- コンビニエンスストアは国内における菓子類の主要流通チャネルです。コンビニエンスストアを通じた菓子類の販売額は、2023年には前年比4.3%増加しました。この成長の主な要因は、近代的な店舗に比べてアクセスが容易で営業時間が長いことです。こうした要因が菓子類の売上を押し上げています。

- スーパーマーケットとハイパーマーケットは、コンビニエンスストアに次いで広く好まれている流通チャネルです。スーパーマーケットとハイパーマーケットを通じた菓子類の販売額は、2021年から2023年にかけて9.42%の成長率を記録しました。これらの小売チャネルは、提供されるブランドの品揃えの豊富さ、棚面積の広さ、頻繁な価格プロモーション、スーパーマーケットやハイパーマーケットで広く入手可能なチョコレート、キャンディー、無糖ガム、スナックバーなどの菓子類に対する需要の高まりにより、強い地位を占めています。

- スーパーマーケットでは菓子類を大量に購入すると割引価格が適用されます。アルディ、テスコ、アスダ、セインズベリー、モリソンズなどの主要スーパーマーケット・チェーンは、英国で650g入りのチョコレートを5.24米ドル、100g入りを1.78米ドル、382g入りを4.57米ドルで販売しています。また、これらの小売チャネルは、消費者がオンライン・ウェブサイトから商品を購入すると、キャッシュバックや特典を提供しています。

- オンライン小売チャネルは、利便性、割引料金、1日配達オプションなどの要因により、予測期間中に最も高い成長率を示すと予想されます。オンライン小売チャネルを通じた菓子類の販売額は、2023年から2030年にかけてCAGR 5.95%を記録すると予測されます。

英国の菓子類市場の動向

英国全土で高級菓子類が幅広く入手可能であることと相まって、包装形態の革新が売上を牽引しています。

- 英国では菓子類の消費は年齢層別に高く、特にチョコレートの消費は25~34歳に多いです。2022年には、1週間あたり1人当たり平均5.2米ドルが充填チョコレート・バーに、5.2米ドルが固形チョコレート・バーに費やされていることがわかりました。英国では、菓子類の大半は25歳から45歳の消費者によって消費されており、34歳以上の消費者は18歳から34歳の消費者よりも多くの菓子を購入しています。英国では、菓子類を楽しむ頻度は週に3~4回という傾向があります。さらに、23%が家族への贈り物として購入し、33%までは食料品の買い物の際に必ず買い物かごに入れています。

- 菓子類では、消費者は主にブランド・ロイヤルティの影響を受けています。英国では、Z世代とミレニアル世代の消費者が、他の年齢層の中で最も高いブランド・ロイヤルティを公言しています。英国の消費者の約73%が、特定の小売店、ブランド、店舗に「忠実」であると考えています。パッケージは、菓子類にとって2番目に重要な製品属性であり、購入の可能性を決定します。英国の消費者の約65%が革新的なパッケージに魅力を感じていることが確認されています。菓子類では、リンツ、マース、フェレロ、キャドバリーなどの人気ブランドが高いシェアを占めています。これらのブランドは、消費者層を拡大するため、ボール、バー、サークルなど様々な形態で製品を提供しています。

- 2023年の菓子類は売上高が上昇しました。売上の伸びは、消費者の食習慣の変化と関連しています。2023年、菓子類では、油っこいスナック菓子よりもスナックバーが好まれ、かなりの数量が人気を集めました。2023年のチョコレート製品の平均価格の前年比成長率は2.34米ドルと評価され、これも2.1%の上昇でした。製品価格の変動は、穀類、穀物、砂糖などの原材料価格の上下と関連しています。その他、原材料の輸出入なども菓子類の価格に影響を与えました。英国では、2023年のチョコレート菓子の平均販売価格は6.54米ドル、砂糖菓子のそれは9.36米ドルでした。2022年、年間平均消費者物価指数(CPI)によると、砂糖、ジャム、シロップ、砂糖菓子類の物価指数は英国で110.1指数ポイントでした。

- 英国では、菓子類ではチョコレートが人気のお菓子です。しかし、その健康上の利点や潜在的な欠点については考慮が必要です。チョコレートは2023年には英国人口の92%が消費しています。

英国の菓子類産業の概要

英国の菓子類市場は適度に統合されており、上位5社で47.96%を占めています。この市場の主要企業は以下の通り。 Chocoladefabriken Lindt & Sprungli AG, Ferrero International SA, Mars Incorporated, Mondelez International Inc. and Nestle SA.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子

- チョコレート

- 菓子類別

- ダークチョコレート

- ミルク&ホワイトチョコレート

- ガム

- 菓子類別

- バブルガム

- チューインガム

- 砂糖含有量別

- 砂糖入りチューインガム

- 無糖チューインガム

- スナック菓子

- 菓子類別

- シリアル・バー

- フルーツ&ナッツバー

- プロテイン・バー

- 砂糖菓子類

- 菓子類別

- ハードキャンディー

- ロリポップ

- ミント

- パスティル、グミ、ゼリー

- トフィーとヌガー

- その他

- チョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Alfred Ritter GmbH & Co. KG

- Arcor S.A.I.C

- August Storck KG

- Barry Callebaut AG

- Chocoladefabriken Lindt & Sprungli AG

- Confiserie Leonidas SA

- Ferrero International SA

- HARIBO Holding GmbH & Co. KG

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Pimlico Confectioneries Ltd

- Polo del Gusto SRL

- Swizzels Matlow Ltd

- The Hershey Company

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The UK Confectionery Market size is estimated at 16.98 billion USD in 2025, and is expected to reach 22.06 billion USD by 2030, growing at a CAGR of 5.37% during the forecast period (2025-2030).

Supermarkets, hypermarkets, and convenience stores collectively account for more than 75% of the market share due to their longer opening hours and access to a wide range of confectionery brands

- Convenience stores are the leading distribution channels for confectionery products in the country. The sales value of confectionery products through convenience stores increased by 4.3% in 2023 compared to the previous year. The major factor behind this growth was the ease of access and longer opening hours compared to modern stores. These factors boost the sales of confectionery products.

- Supermarkets and hypermarkets are the second most widely preferred distribution channels after convenience stores. The sales value of confectionery products through supermarkets and hypermarkets registered a growth rate of 9.42% from 2021 to 2023. These retail channels have a strong position due to the wide selection of brands offered, considerable shelf space, frequent price promotions, and the rising demand for confectionery products such as chocolates, candies, sugar-free gums, snack bars, and others that are widely accessible at supermarkets and hypermarkets.

- Supermarkets offer discounted prices for bulk purchases of confectioneries. Key supermarket chains, including Aldi, Tesco, Asda, Sainsbury, and Morrisons, sell 650 g of chocolate boxes for USD 5.24, 100 g boxes for USD 1.78, and 382 g boxes for USD 4.57 in the United Kingdom. These retail channels also offer cashback and rewards when consumers buy products from their online websites.

- Online retail channels are expected to grow at the highest rate during the forecast period due to factors such as convenience, discounted rates, and one-day delivery options. The sales value of confectionery products through online retail channels is anticipated to register a CAGR of 5.95% from 2023 to 2030.

UK Confectionery Market Trends

Innovation in packaging formats, coupled with the wide availability of premium confectionery products across the United Kingdom, drives sales

- The consumption of confectionery products is high in individuals of different ages in the United Kingdom, with chocolate consumption being particularly prevalent among those aged 25 to 34. In 2022, it was found that an average of USD 5.2 was spent on filled chocolate bars per person per week, and USD 5.2 was spent on solid chocolate bars. In the United Kingdom, the majority of confectionery products are consumed by consumers between 25 and 45 years of age, with those aged 34 and over purchasing more candy than those aged 18 to 34. Individuals in the United Kingdom tend to enjoy confectionery products at a frequency of 3-4 times per week. Additionally, 23% purchase it as a gift for family members, and up to 33% always place it in their shopping cart when they go grocery shopping.

- Under the confectionery section, consumers are mainly affected by brand loyalty. In the United Kingdom, Gen Z and Millennial consumers professed the highest brand loyalty among other age groups. About 73% of UK consumers consider themselves "loyal" to certain retailers, brands, and stores. Packaging is considered the second most important product attribute for confectionery products, which determines the likelihood of purchasing. It is observed that around 65% of consumers in the United Kingdom are attracted to innovative packaging. Popular brands, including Lindt, Mars, Ferrero, Cadbury, etc., hold the highest share in the confectionery segment. These brands have been offering their products in various formats, such as balls, bars, and circles, to expand their consumer base.

- In 2023, confectionery products in 2023 witnessed a hike in their sales. The sales growth was linked to the changing eating habits of consumers. In 2023, under the confectionery segment, snack bars gained a significant volume of popularity as people preferred them over oily snacks. On average, the Y-o-Y growth of the prices of chocolate products was valued at USD 2.34 in 2023, which was also a hike of 2.1%. The fluctuation in the price of the products was connected with the rise and fall in the prices of its raw materials, including cereals, grains, and sugar. Other factors, such as exporting and importing raw materials, also affected the prices of confectionery products. In the United Kingdom, in 2023, the average selling price of chocolate confections was USD 6.54, while that of sugar confections was USD 9.36. In 2022, as per the annual average Consumer Price Index (CPI), the price index value of sugar, jams, syrups, and sugar confectionery items was measured at 110.1 index points in the United Kingdom.

- In the United Kingdom, under the confectionery segment, chocolate is a popular treat enjoyed by individuals. However, there are considerations regarding its health benefits and potential drawbacks. Chocolates were consumed by 92% of the UK population in 2023.

UK Confectionery Industry Overview

The UK Confectionery Market is moderately consolidated, with the top five companies occupying 47.96%. The major players in this market are Chocoladefabriken Lindt & Sprungli AG, Ferrero International SA, Mars Incorporated, Mondelez International Inc. and Nestle SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confections

- 5.1.1 Chocolate

- 5.1.1.1 By Confectionery Variant

- 5.1.1.1.1 Dark Chocolate

- 5.1.1.1.2 Milk and White Chocolate

- 5.1.2 Gums

- 5.1.2.1 By Confectionery Variant

- 5.1.2.1.1 Bubble Gum

- 5.1.2.1.2 Chewing Gum

- 5.1.2.1.2.1 By Sugar Content

- 5.1.2.1.2.1.1 Sugar Chewing Gum

- 5.1.2.1.2.1.2 Sugar-free Chewing Gum

- 5.1.3 Snack Bar

- 5.1.3.1 By Confectionery Variant

- 5.1.3.1.1 Cereal Bar

- 5.1.3.1.2 Fruit & Nut Bar

- 5.1.3.1.3 Protein Bar

- 5.1.4 Sugar Confectionery

- 5.1.4.1 By Confectionery Variant

- 5.1.4.1.1 Hard Candy

- 5.1.4.1.2 Lollipops

- 5.1.4.1.3 Mints

- 5.1.4.1.4 Pastilles, Gummies, and Jellies

- 5.1.4.1.5 Toffees and Nougats

- 5.1.4.1.6 Others

- 5.1.1 Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Alfred Ritter GmbH & Co. KG

- 6.4.2 Arcor S.A.I.C

- 6.4.3 August Storck KG

- 6.4.4 Barry Callebaut AG

- 6.4.5 Chocoladefabriken Lindt & Sprungli AG

- 6.4.6 Confiserie Leonidas SA

- 6.4.7 Ferrero International SA

- 6.4.8 HARIBO Holding GmbH & Co. KG

- 6.4.9 Mars Incorporated

- 6.4.10 Mondelez International Inc.

- 6.4.11 Nestle SA

- 6.4.12 Pimlico Confectioneries Ltd

- 6.4.13 Polo del Gusto SRL

- 6.4.14 Swizzels Matlow Ltd

- 6.4.15 The Hershey Company

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms