|

市場調査レポート

商品コード

1687286

菓子類- 市場シェア分析、産業動向・統計、成長予測(2025~2030年)Confectionery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 菓子類- 市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 459 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

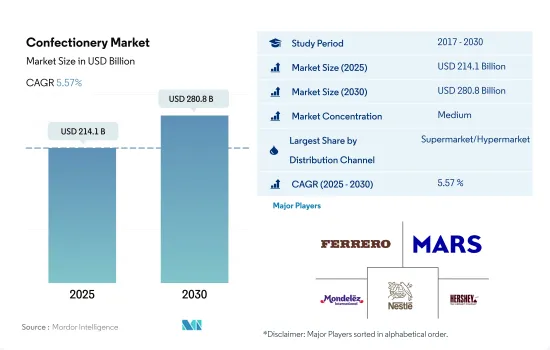

菓子類の市場規模は2025年に2,141億米ドルと推定され、2030年には2,808億米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは5.57%で成長します。

菓子類の世界小売販売ではスーパーマーケットとハイパーマーケットが圧倒的シェアを占め、次いでコンビニエンスストアが続きます。

- 世界の小売セグメントでは、2023年にスーパーマーケットとハイパーマーケットが最大の小売セグメントとされました。菓子類の棚における戦略的な製品ポジショニングは、潜在的消費者の衝動購買行動に影響を与えます。Casino Supermarkets、Carrefour、Super U、Lidlは、この地域の大手食料品店経営者です。金額シェアでは、欧州が2023年の数量シェアで33.6%を獲得し、小売スペースを支配しています。これらの事業者の全国的なネットワークにより、地元や主流の菓子類ブランドへのアクセスが容易になっています。2023年現在、Lidlはドイツで3,000店以上、フランスで1,500店以上を展開しています。Carrefourはこの地域で約2,869のスーパーマーケットを運営しています。

- コンビニエンスストアは、世界の小売業セグメントで2番目に大きな小売業者と考えられています。これは、コンビニエンスストアが消費者により高い利便性を提供できるからです。2023年、Beckerはオンタリオ州で45店舗を所有していることが確認されました。これらの店舗は、革新的なオファーを備えた幅広いチョコレート製品を顧客に提供する傾向があります。北米は、2023年に数量ベースで29.1%のシェアを占め、小売スペースでは第2位の地域と考えられています。

- オンライン小売部門は、2023年に菓子類の小売産業で最も急成長していると考えられています。このセグメントは、2023~2030年の間に7.13%の金額CAGRで推移すると推定されています。消費者はまた、ワンクリックで買い物ができるオンライン小売セグメントを好んでいます。この要因により、消費者は菓子に費やす平均ショッピング時間を容易に管理することができます。

欧州は、美味しくて便利な嗜好品への消費者の嗜好が牽引する菓子類の主要セグメントです。

- 世界の菓子類市場は2018~2023年にかけて金額ベースで3.38%のCAGRを観測しました。天然材料とより少ない砂糖で作られたより健康的な菓子類への動向の高まりが、世界の菓子類市場の成長を後押ししています。そのため、シュガーフリー、ヴィーガン、オーガニックなど、健康に良いことで人気の高い製品の開発が進んでいます。

- その他の地域と比較して、欧州は金額ベースで34.34%の最大シェアを占め、2023年には2022年比で4.03%の成長率を記録しました。ドイツ、フランス、英国、ロシアは菓子類を消費する巨大な消費者基盤を有しており、これがこの地域の需要を牽引しています。美味しくて便利な嗜好性間食に対する消費者の嗜好は、この地域の主要な市場促進要因として認識されています。2022年には、ドイツのスナッカーの72%が毎週キャンディとチョコレートバーを消費しています。また、プレミアムでサステイナブルチョコレートに対する消費者の嗜好は、結果的にこの地域の菓子類の売上拡大につながりました。

- 北米は世界第2位の菓子類市場です。同地域は予測期間(2023~2030年)に金額ベースでCAGR 6.32%を記録すると予測されています。チョコレート菓子類の人気と需要の高まりが市場成長を後押ししています。北米のチョコレート菓子類の消費者はあらゆる年齢層に見られます。2022年には、米国の消費者の49%以上がミルクチョコレートを消費し、ダークチョコレートは34%が消費しました。また、カナダでは、2022年のチョコレートの平均消費量は1人当たり6.4kgでした。カナダの家庭では、年間平均88米ドルを板チョコレートに費やしています。

世界の菓子類市場の動向

祝祭シーズンや特別な日の旺盛な需要が世界の菓子類市場にプラスの影響

- 菓子類の主要消費地域は欧州とアジア太平洋で、北米がこれに続きます。欧州における菓子類の消費は、祝祭日や休日、贈答に関連するものが多く、年間を通じて安定した需要があります。北米では、消費者の5分の1が毎週キャンディを購入しており、2022年には週に何度もキャンディを購入する消費者がわずかに増える(22%)。

- オーガニック、フェアトレード認証、レインフォレスト・アライアンス/UTZ認証の菓子類は、欧州各国で大きな支持を集めています。ドイツ、英国、オランダは、フェアトレード認証のカカオ豆を使ったチョコレートの最大市場です。また、消費者の嗜好は菓子類の味、食感、形式に影響されます。

- 2023年、菓子類は売上高を伸ばしました。売上の伸びは消費者の食習慣の変化に関連しています。2023年には、菓子類ではスナックバーが油の詰まったスナック菓子よりも好まれるようになり、かなりの量の人気を獲得しました。2023年のチョコレート製品の平均価格の前年比成長率は2.34米ドルと評価され、これも2.1%の上昇でした。

- 菓子類セグメントでは、チョコレートは個人が楽しむ人気のお菓子です。その健康上の利点と潜在的な欠点に関する考察があります。チョコレートは、2023年には世界人口の92%によって消費されました。世界中で、菓子類の消費には、健康上の意義など、健康の観点から考慮すべきいくつかの追加要因があります。

菓子類の産業概要

菓子類市場は適度に統合されており、上位5社で44.37%を占めています。この市場の主要企業は、 Ferrero International SA、Mars Incorporated、Mondelez International Inc.、Nestle SA、The Hershey Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子

- チョコレート

- 菓子類別

- ダークチョコレート

- ミルク&ホワイトチョコレート

- ガム

- 菓子類別

- バブルガム

- チューインガム

- 砂糖含有量別

- 砂糖入りチューインガム

- 無糖チューインガム

- スナック菓子

- 菓子類別

- シリアルバー

- フルーツ&ナッツバー

- プロテインバー

- 砂糖菓子類

- 菓子類別

- ハードキャンディ

- ロリポップ

- ミント

- パスティル、グミ、ゼリー

- トフィーとヌガー

- その他

- チョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット

- その他

- 地域

- アフリカ

- 国別

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- 韓国

- その他のアジア太平洋

- 欧州

- 国別

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- スイス

- トルコ

- 英国

- その他の欧州

- 中東

- 国別

- バーレーン

- クウェート

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他の中東

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- その他の南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- August Storck KG

- Chocoladefabriken Lindt & Sprungli AG

- Ferrero International SA

- General Mills Inc.

- HARIBO Holding GmbH & Co. KG

- Kellogg Company

- Lotte Corporation

- Mars Incorporated

- Meiji Holdings Company Ltd

- Mondelez International Inc.

- Nestle SA

- PepsiCo Inc.

- Perfetti Van Melle BV

- The Hershey Company

- YIldIz Holding AS

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 60164

The Confectionery Market size is estimated at 214.1 billion USD in 2025, and is expected to reach 280.8 billion USD by 2030, growing at a CAGR of 5.57% during the forecast period (2025-2030).

Supermarkets and hypermarkets account for the prominent share, followed by convenience stores in the global retail sales of confectionery

- Under the global retailing segment, supermarkets and hypermarkets were considered the largest retailing segment in 2023. Strategic product positioning on the shelves for the confectionery category influences impulse purchase behavior among potential consumers. Casino Supermarkets, Carrefour, Super U, and Lidl are some of the leading grocery store operators in the region. By value share, Europe has been dominating the retailing space by acquiring a share of 33.6% by volume in 2023. A nationwide network of these operators allows easy access to local and mainstream confectionery brands. As of 2023, Lidl operated more than 3,000 stores and 1,500 stores in Germany and France, respectively. Carrefour operates around 2,869 supermarkets across the region.

- Convenience stores are considered the second largest retailers in the global retailing segment. This is because these stores have the capability of offering a greater convenience experience to their consumers. In 2023, it was observed that Becker's was owed 45 stores in Ontario. These stores tend to offer a wide range of chocolate products with innovative offers to their customers. North America is considered the second-largest region for retailing space, holding a share of 29.1% by volume in 2023.

- The online retailing segment was considered the fastest-growing retailing industry for confectionery products in 2023. The segment is estimated to register a value CAGR of 7.13% during 2023-2030. Consumers are also preferring the online retail segment as a one-click shopping platform. Due to this factor, consumers can easily manage the average shopping time spent on confections.

Europe is the leading confectionery segment driven by the consumer preference for tasty and convenient indulgent snacking

- The global confectionery market observed a CAGR of 3.38% during 2018-2023 in terms of value. An increasing trend toward healthier confectionery products made with natural ingredients and less sugar is fueling the growth of the global confectionery market. It has led to the development of products like sugar-free, vegan, and organic, which are popular for their health benefits.

- Compared to other regions, Europe accounted for the largest share of 34.34% in terms of value and registered a growth rate of 4.03% in 2023 compared to 2022. Germany, France, the United Kingdom, and Russia have a huge consumer base for the consumption of confectionery, which will drive the regional demand. Consumer preference for tasty and convenient indulgent snacking is identified as the key market driver in the region. In 2022, 72% of German snackers consumed candy and chocolate bars every week. Also, consumer preference for premium and sustainable chocolate has consequently led to expanding sales of confectioneries in the region.

- North America is the second-largest confectionery market globally. The region is anticipated to register a CAGR of 6.32% in terms of value during the forecast period (2023-2030). The increasing popularity and demand for chocolate confectionery products are propelling the market growth. Consumers of chocolate confectionery in North America can be found in all age groups. In 2022, more than 49% of consumers in the United States consumed milk chocolate, and dark chocolate was consumed by 34% of Americans. Also, in Canada, the average consumption of chocolate stood at 6.4 kg per person in 2022. Canadian households spend an average of USD 88 on chocolate bars per year.

Global Confectionery Market Trends

Strong demand during festive seasons and special occasions positively impacts the confectionery market worldwide

- Europe and Asia-Pacific are the leading confectionery-consuming regions, followed by North America. The consumption of confectionery products in Europe is majorly associated with celebrations, holidays, and gift-giving, leading to consistent demand throughout the year. In North America, one-fifth of consumers bought candy weekly, and slightly more (22%) bought candy multiple times per week in 2022.

- Organic, Fairtrade-certified, and Rainforest Alliance/UTZ-certified confectionery are gaining significant traction across European countries. Germany, the UK, and the Netherlands are the largest markets for chocolates made with Fairtrade-certified cocoa beans. Also, consumer preferences are influenced by the taste, texture, and format of the confectionery.

- In 2023, confectionery products witnessed a hike in their sales. The sales growth was linked to the changing eating habits of consumers. In 2023, under the confectionery segment, snack bars gained a significant volume of popularity as people preferred them over oily-stuffed snacks. On average, the Y-o-Y growth of the prices of chocolate products was valued at USD 2.34 in 2023, which was also a hike of 2.1%.

- Under the confectionery segment, chocolate is a popular treat enjoyed by individuals. There are considerations regarding its health benefits and potential drawbacks. Chocolates were consumed by 92% of the global population in 2023. Across the globe, there are a few additional factors to consider in the context of confectionery consumption from a health perspective, such as their health significance.

Confectionery Industry Overview

The Confectionery Market is moderately consolidated, with the top five companies occupying 44.37%. The major players in this market are Ferrero International SA, Mars Incorporated, Mondelez International Inc., Nestle SA and The Hershey Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confections

- 5.1.1 Chocolate

- 5.1.1.1 By Confectionery Variant

- 5.1.1.1.1 Dark Chocolate

- 5.1.1.1.2 Milk and White Chocolate

- 5.1.2 Gums

- 5.1.2.1 By Confectionery Variant

- 5.1.2.1.1 Bubble Gum

- 5.1.2.1.2 Chewing Gum

- 5.1.2.1.2.1 By Sugar Content

- 5.1.2.1.2.1.1 Sugar Chewing Gum

- 5.1.2.1.2.1.2 Sugar-free Chewing Gum

- 5.1.3 Snack Bar

- 5.1.3.1 By Confectionery Variant

- 5.1.3.1.1 Cereal Bar

- 5.1.3.1.2 Fruit & Nut Bar

- 5.1.3.1.3 Protein Bar

- 5.1.4 Sugar Confectionery

- 5.1.4.1 By Confectionery Variant

- 5.1.4.1.1 Hard Candy

- 5.1.4.1.2 Lollipops

- 5.1.4.1.3 Mints

- 5.1.4.1.4 Pastilles, Gummies, and Jellies

- 5.1.4.1.5 Toffees and Nougats

- 5.1.4.1.6 Others

- 5.1.1 Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Nigeria

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Malaysia

- 5.3.2.1.7 New Zealand

- 5.3.2.1.8 South Korea

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 Belgium

- 5.3.3.1.2 France

- 5.3.3.1.3 Germany

- 5.3.3.1.4 Italy

- 5.3.3.1.5 Netherlands

- 5.3.3.1.6 Russia

- 5.3.3.1.7 Spain

- 5.3.3.1.8 Switzerland

- 5.3.3.1.9 Turkey

- 5.3.3.1.10 United Kingdom

- 5.3.3.1.11 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Bahrain

- 5.3.4.1.2 Kuwait

- 5.3.4.1.3 Oman

- 5.3.4.1.4 Qatar

- 5.3.4.1.5 Saudi Arabia

- 5.3.4.1.6 United Arab Emirates

- 5.3.4.1.7 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 August Storck KG

- 6.4.2 Chocoladefabriken Lindt & Sprungli AG

- 6.4.3 Ferrero International SA

- 6.4.4 General Mills Inc.

- 6.4.5 HARIBO Holding GmbH & Co. KG

- 6.4.6 Kellogg Company

- 6.4.7 Lotte Corporation

- 6.4.8 Mars Incorporated

- 6.4.9 Meiji Holdings Company Ltd

- 6.4.10 Mondelez International Inc.

- 6.4.11 Nestle SA

- 6.4.12 PepsiCo Inc.

- 6.4.13 Perfetti Van Melle BV

- 6.4.14 The Hershey Company

- 6.4.15 YIldIz Holding AS

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms