|

市場調査レポート

商品コード

1683179

欧州の菓子類市場:市場シェア分析、産業動向、成長予測(2025~2030年)Europe Confectionery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の菓子類市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 289 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

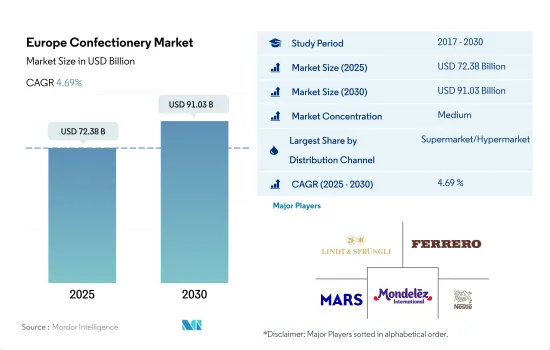

欧州の菓子類の市場規模は2025年に723億8,000万米ドルと推定・予測され、2030年には910億3,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは4.69%で成長すると予測されます。

スーパーマーケットとコンビニエンスストアは合計で市場シェアの75%以上を占めます。

- この地域の菓子類販売では、スーパーマーケット/ハイパーマーケットが常に主導権を握っています。チョコレートは主にスーパーマーケットやハイパーマーケットを通じて販売されており、2022年の市場数量シェアは50.89%です。菓子類の専用棚における戦略的な商品ポジショニングは、潜在的消費者の衝動買い行動に影響を与えます。Casino Supermarkets、Carrefour、Super U、Lidlは、この地域の大手食品スーパーです。これらの事業者の全国的なネットワークにより、地元の菓子類ブランドや主流菓子類ブランドへのアクセスが容易になっています。2023年現在、リドルはドイツとフランスでそれぞれ3,000店と1,500店以上を展開しています。Carrefourはこの地域で約2,869のスーパーマーケットを運営しています。

- コンビニエンスストアは、スーパーマーケット、ハイパーマーケットに次いで、菓子類の購入に広く選ばれている流通チャネルです。コンビニエンスストアを通じた菓子類の数量は、2024年には38.96%のシェアを記録すると推定されます。プライベートブランドへのアクセスが容易なため、消費者は他の小売チャネルよりも伝統的食料品店を好みます。スナックバーの売上はコンビニエンスストアを通じて最も高いCAGRで成長し、2030年には17億6,198万米ドルに達すると推定されます。

- オンラインチャネルは菓子類の流通チャネルとして最も急成長しており、予測期間中の予想CAGRは金額ベースで6.13%です。インターネット利用者の増加は、食料品購入におけるオンラインチャネルの役割の進化に影響を与えています。2022年には、16~74歳の欧州消費者の68%が個人的な用途でオンライン商品またはサービスを購入しています。

ドイツ、英国、フランスにおけるチョコレートとキャンディの高い消費が欧州の菓子類市場の成長に貢献

- 英国とドイツがこの地域の主要市場であり、フランスとロシアがこれに続きます。ドイツと英国は、2023年の菓子類数量全体の39.21%を占めています。美味しくて便利な嗜好性間食に対する消費者の嗜好が、この地域の主要な市場促進要因であることが確認されています。2022年には、ドイツのスナッカーの72%が毎週キャンディーとチョコレートバーを消費しています。ドイツでは、チョコレートの売上高は予測期間中に4.98%のCAGRを記録し、2030年には139億3,701万米ドルの売上高に達すると予測されます。

- フランスでは、菓子類市場は大規模なカカオ加工とチョコレート製造産業によって特徴付けられています。2022年の菓子類全体の消費に占めるチョコレートのシェアは68.68%でした。簡単に調理できる食品への消費者シフトが、予測期間中のスナックバー需要を促進すると予測されます。2022年には、フランスの消費者の44%が家庭での朝食の一部としてクイックフードを好みました。

- トルコとスペインは、欧州で最も急成長している菓子類市場です。トルコ市場は、金額ベースで2023~2030年にCAGR 5.69%で拡大すると予測されています。トルコでは、宗教的な祭事や結婚式、祝賀の際の贈り物として砂糖菓子類が伝統的に人気があることが、同市場の成長を後押ししています。

- スペインでは、チョコレートと砂糖菓子が菓子類のトップセラーであり、2023年の数量シェアは合計で93.674%でした。健康的な間食傾向がスペインにおけるダークチョコレートと砂糖不使用の菓子類の消費を促進すると予想されます。2021年には、55.4%の消費者がより健康的な食品に支出することを好んでいます。ダークチョコレートの数量は予測期間中にCAGR 5.98%を記録すると予測されます。

欧州の菓子類市場の動向

砂糖不使用、クリーンラベル、天然、オーガニックといったヘルシーな菓子類が地域全体で導入された結果、売上が増加しました。

- 欧州における菓子類の消費は、祝祭日、休日、贈答に関連するものが多く、年間を通じて安定した需要をもたらしています。欧州の人々はチョコレートの世界の主要消費者であり、高品質のチョコレートや、持続可能で倫理的な取引を証明する側面を持つ製品をますます求めるようになっています。

- 2022年にドイツで販売されたチョコレート菓子類の80%以上が、サステイナブル方法で生産されたカカオを使用しています。Lidl、Aldi、REWEといったドイツの大手小売業者は、100%サステイナブルカカオのチョコレートのみを販売することを約束しています。

- 欧州では、プレミアムチョコレートや職人技を駆使したチョコレートへの関心が高まっています。2022年には、英国のチョコレート購入者の4分の1が、自分用に高級ブランドのチョコレートを購入し、同国の消費者の44%がギフトとしてそれらのチョコレートを購入しています。

- 2022年、ドイツの消費者の55%はミルクチョコレートを好みます。しかし、ダークチョコレートが最も急成長するセグメントとなる見込みです。スイスでは66%の消費者がダークチョコレートを好みます。ダークチョコレートの消費は、健康的な製品を求める消費者の嗜好が原動力となっています。

欧州の菓子類産業概要

欧州の菓子類市場は適度に統合されており、上位5社で49.92%を占めています。この市場の主要企業は、Chocoladefabriken Lindt & Sprungli AG、Ferrero International SA、Mars Incorporated、Mondelez International Inc.、Nestle SAです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子

- チョコレート

- 菓子類別

- ダークチョコレート

- ミルク&ホワイトチョコレート

- ガム

- 菓子類別

- バブルガム

- チューインガム

- 砂糖含有量別

- 砂糖入りチューインガム

- 無糖チューインガム

- スナック菓子

- 菓子類別

- シリアルバー

- フルーツ&ナッツバー

- プロテインバー

- 砂糖菓子類

- 菓子類別

- ハードキャンディー

- ロリポップ

- ミント

- パスティル、グミ、ゼリー

- トフィーとヌガー

- その他

- チョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット

- その他

- 国名

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- スイス

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- August Storck KG

- Chocoladefabriken Lindt & Sprungli AG

- Confiserie Leonidas SA

- Delica AG

- Ferrero International SA

- HARIBO Holding GmbH & Co. KG

- Mars Incorporated

- Meiji Holdings Company Ltd

- Mondelez International Inc.

- Nestle SA

- Perfetti Van Melle BV

- Sirio Pharma Co. Ltd

- The Otmuchow Group

- Valrhona Chocolate

- YIldIz Holding AS

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Confectionery Market size is estimated at 72.38 billion USD in 2025, and is expected to reach 91.03 billion USD by 2030, growing at a CAGR of 4.69% during the forecast period (2025-2030).

Supermarkets and convenience stores collectively account for more than 75% of the market share as nationwide store chains allow broader reach and easy access to multiple brands

- Supermarkets/hypermarkets have always maintained a strong lead in the sales of confectionery in the region. Chocolate is largely sold confection through supermarkets and hypermarkets, with a market volume share of 50.89% in 2022. Strategic product positioning on the dedicated shelves for the confectionery category influences impulse purchase behavior among potential consumers. Casino Supermarkets, Carrefour, Super U, and Lidl are some of the leading grocery store operators in the region. A nationwide network of these operators allows easy access to local and mainstream confectionery brands. As of 2023, Lidl operated more than 3,000 and 1,500 stores in Germany and France, respectively. Carrefour operates around 2,869 supermarkets across the region.

- Convenience stores are the second most widely preferred distribution channel after supermarkets and hypermarkets for purchasing confectionery. The volume sales of confectionery through convenience stores is estimated to register a 38.96% volume share in 2024. The broader reach and easy access to private label brands drive the consumer preference for traditional grocery stores over other retail channels. Snack bar sales are estimated to grow at the highest CAGR through convenience stores, reaching a sales value of USD 1,761.98 million in 2030.

- The online channel is projected to be the fastest-growing distribution channel for confectionery, with an anticipated CAGR of 6.13% in terms of value during the forecast period. The increasing number of internet users influences the evolving role of online channels in grocery purchases. In 2022, 68% of European consumers aged 16 to 74 bought online goods or services for personal use.

High consumption of chocolates and candy across Germany, the United Kingdom, and France contributes to the growth of the confectionery market in Europe

- The United Kingdom and Germany are identified as the major markets in the region, followed by France and Russia. Germany and the United Kingdom collectively accounted for a 39.21% share of the overall confectionery sales volume across the region in 2023. Consumer preference for tasty and convenient indulgent snacking is identified as the key market driver in the region. In 2022, 72% of German snackers consumed candy and chocolate bars every week. In Germany, chocolate sales are anticipated to register the highest CAGR of 4.98% during the forecast period to reach a sales value of USD 13,937.01 million in 2030.

- In France, the confectionery market is characterized by the large cocoa-processing and chocolate-manufacturing industry. Chocolate had a 68.68% share of the overall confectionery consumption in 2022. Consumer shift toward easy-to-prepare food is estimated to foster the demand for snack bars during the forecast period. In 2022, 44% of French consumers preferred quick food as part of at-home breakfasts.

- Turkey and Spain are identified as the fastest-growing confectionery markets in Europe. The Turkish market is anticipated to expand at a CAGR of 5.69% during 2023-2030 in terms of value. The traditional popularity of sugar confectionery as gifts during religious festivals, wedding ceremonies, and celebrations fuels the market's growth in Turkey.

- In Spain, chocolate and sugar confectionery are top-selling confections and collectively had a volume share of 93.674% in 2023. A healthy snacking trend is anticipated to promote the consumption of dark chocolates and sugar-free confectionery in Spain. In 2021, 55.4% of consumers preferred to spend more on healthier food options. Dark chocolate sales volume is anticipated to register a CAGR of 5.98% during the forecast period.

Europe Confectionery Market Trends

The introduction of healthy variants like sugar-free, clean-label, natural, and organic confectionery products across the region resulted in higher sales

- The consumption of confectionery products in Europe is majorly associated with celebrations, holidays, and gift-giving, leading to consistent demand throughout the year. Europeans are the world's main consumers of chocolate and increasingly demand high-quality chocolates, as well as products that hold aspects that prove their sustainable and ethical trade.

- More than 80% of all chocolate confectionery sold in Germany in 2022 was made using sustainably produced cocoa. Large German retailers such as Lidl, Aldi, and REWE have committed themselves to only sell 100% sustainable cocoa chocolates.

- There is a growing interest in premium and artisanal chocolates in Europe. In 2022, a quarter of chocolate buyers in the United Kingdom paid more for a luxury brand of chocolate for themselves, while 44% of consumers in the country purchased those chocolates as a gift.

- In 2022, 55% of consumers in Germany preferred milk chocolate. However, dark chocolate is expected to be the fastest-growing segment. In Switzerland, 66% of consumers preferred dark chocolate. Consumption of dark chocolate is driven by consumer preferences for healthy products.

Europe Confectionery Industry Overview

The Europe Confectionery Market is moderately consolidated, with the top five companies occupying 49.92%. The major players in this market are Chocoladefabriken Lindt & Sprungli AG, Ferrero International SA, Mars Incorporated, Mondelez International Inc. and Nestle SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confections

- 5.1.1 Chocolate

- 5.1.1.1 By Confectionery Variant

- 5.1.1.1.1 Dark Chocolate

- 5.1.1.1.2 Milk and White Chocolate

- 5.1.2 Gums

- 5.1.2.1 By Confectionery Variant

- 5.1.2.1.1 Bubble Gum

- 5.1.2.1.2 Chewing Gum

- 5.1.2.1.2.1 By Sugar Content

- 5.1.2.1.2.1.1 Sugar Chewing Gum

- 5.1.2.1.2.1.2 Sugar-free Chewing Gum

- 5.1.3 Snack Bar

- 5.1.3.1 By Confectionery Variant

- 5.1.3.1.1 Cereal Bar

- 5.1.3.1.2 Fruit & Nut Bar

- 5.1.3.1.3 Protein Bar

- 5.1.4 Sugar Confectionery

- 5.1.4.1 By Confectionery Variant

- 5.1.4.1.1 Hard Candy

- 5.1.4.1.2 Lollipops

- 5.1.4.1.3 Mints

- 5.1.4.1.4 Pastilles, Gummies, and Jellies

- 5.1.4.1.5 Toffees and Nougats

- 5.1.4.1.6 Others

- 5.1.1 Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Belgium

- 5.3.2 France

- 5.3.3 Germany

- 5.3.4 Italy

- 5.3.5 Netherlands

- 5.3.6 Russia

- 5.3.7 Spain

- 5.3.8 Switzerland

- 5.3.9 Turkey

- 5.3.10 United Kingdom

- 5.3.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 August Storck KG

- 6.4.2 Chocoladefabriken Lindt & Sprungli AG

- 6.4.3 Confiserie Leonidas SA

- 6.4.4 Delica AG

- 6.4.5 Ferrero International SA

- 6.4.6 HARIBO Holding GmbH & Co. KG

- 6.4.7 Mars Incorporated

- 6.4.8 Meiji Holdings Company Ltd

- 6.4.9 Mondelez International Inc.

- 6.4.10 Nestle SA

- 6.4.11 Perfetti Van Melle BV

- 6.4.12 Sirio Pharma Co. Ltd

- 6.4.13 The Otmuchow Group

- 6.4.14 Valrhona Chocolate

- 6.4.15 YIldIz Holding AS

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms