|

市場調査レポート

商品コード

1690975

北米の大豆たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の大豆たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 211 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

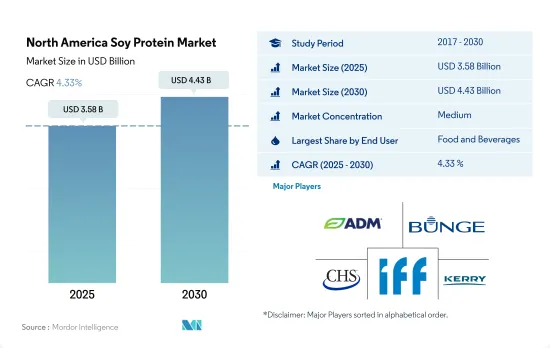

北米の大豆たんぱく質の市場規模は2025年に35億8,000万米ドルと推定・予測され、2030年には44億3,000万米ドルに達し、予測期間(2025-2030年)のCAGRは4.33%で成長すると予測されています。

F&B分野は、大豆たんぱく質の高い栄養特性により、大豆たんぱく質の主要用途となっています。

- 2022年には、飲食品セグメントが金額シェアでトップのエンドユーザーセグメントに浮上しました。このセグメントの中では、食肉とその代替品、特に大豆タンパク質を利用したものが46%と最も高いシェアを占めています。大豆タンパク質はその汎用性で知られ、塊、細切れ、細片といった肉のような食感を作り出すのに役立っており、肉を使わない選択肢の魅力を高めています。注目すべきは、2021年にはアメリカ人の4分の1が健康と環境への懸念を理由に植物由来の代替肉に目を向け、このサブセグメントの成長をさらに後押ししていることです。

- 動物飼料部門では、主に濃縮タイプの大豆タンパク質が重要な役割を果たしています。その人気の理由は、消化しやすさ、保存期間の長さ、強力なタンパク質強化といった特性にあります。その結果、大豆たんぱく質は反芻動物や豚から家禽や養殖まで、さまざまな家畜の飼料に欠かせないたん白源となっています。この動向は、動物飼料における大豆タンパク質の重要性に対するこの地域の認識の高まりと一致しています。予測によると、このエンドユーザーセグメントは北米市場の予測期間中に3.20%のCAGRで安定的に推移します。

- サプリメントは急速な成長を遂げ、予測期間中のCAGRは5.92%と予測されます。この急成長の背景には、消費者のフィットネスに対する関心の高まり、特にスポーツ栄養とパフォーマンス栄養に対する関心の高まりがあります。フィットネス愛好家や菜食主義のジム通いが増え、筋肉増強のためにプロテインに頼る人が増えているため、サプリメントの需要が増加しています。特に女性アスリートは、エルゴジェニック補助食品として大豆たんぱく質パウダーを利用しており、パフォーマンスを高めるだけでなく、筋肉の回復を早め、骨粗しょう症などの症状にも効果が期待できます。

米国は政府の積極的な取り組みにより大きなシェアを占める

- 2022年には、米国が北米の大豆たんぱく質市場を牽引し、大豆たんぱく質の消費拡大を目指した政府の強力なイニシアチブとプロモーションが後押ししました。飲食品部門と飼料部門が合計で最大のシェアを占め、前者は51.1%、後者は47.8%でした。特筆すべきは、大豆タンパク質の重要な消費者である養鶏産業の繁栄が極めて重要な役割を果たしたことです。例えば、ブロイラー、その他の鶏、七面鳥を含む一人当たりの鶏肉消費量は、2016年の107.6ポンドから2021年には113.4ポンドに増加します。

- 飲食品では、肉、鶏肉、魚介類、およびそれらの代替食品が、2022年には42.5%の市場シェアを占める。健康志向の高まる消費者は、健康を促進する製品に軸足を移しています。この変化は、伝統的な肉食の悪影響に対する意識の高まりによるところが大きいです。その結果、代替肉や類似肉への需要が近年急増しています。

- 2022年には米国が先陣を切ったが、カナダとメキシコもこれに続いた。メキシコは大豆たんぱく質市場では黎明期にあるが、特に急成長している飲食品分野を考えると、有望な成長見通しを示しています。伝統的な、しばしば肉中心の食品を好む傾向が強いメキシコのメーカーは、肉の特性、食感、風味、香りを再現するために技術革新を進めています。その結果、メキシコ大豆たんぱく質市場の飲食品分野は予測期間中に5.40%という最も速いCAGRで推移する見込みです。

北米の大豆たんぱく質市場動向

植物性タンパク質消費の成長が原料業界の主要企業に機会を与える

- 2017年から2022年にかけて、同地域では投資と技術革新に牽引され、一人当たりの植物性タンパク質消費量が2.42%増加しました。この急増は主に、動物愛護への懸念が主な動機となってビーガンまたはベジタリアン食にシフトする消費者の増加によって促進されました。2020年には、さらに約960万人の米国人が植物ベースの食生活を採用し、米国人口の3%近くを占めることになります。COVID-19の大流行後、植物性タンパク質の消費量が急増したが、これは動物性タンパク質のウイルス汚染に対する懸念や、動物性と植物性の両方を含むタンパク質配合の一般的な増加も一因となっています。

- ほとんどのアメリカ人は肉の摂取量を減らしてはいるが、厳格な菜食主義やベジタリアンというよりは、フレキシタリアン的な食事に傾いています。植物性タンパク質は、スポーツ栄養学や肉の代替品として重要な用途を見出しています。特に大豆と乳清タンパク質は、飲食品、サプリメント、スポーツ栄養に広く使われています。2021年までに、米国の消費者の36%が大豆タンパク質をよく知り、摂取したことがあり、ホエイ・プロテインを試したことがある人の割合は31%とやや低いです。

- カナダは第2位のフレキシタリアン人口を誇り、消費者の間でフレキシタリアニズムと菜食主義への大きなシフトが見られます。この動向は、メーカーが植物性タンパク質市場をさらに革新する絶好の機会を提供しています。2021年、カナダ政府は、持続可能で高品質な植物性タンパク質に対する消費者の欲求の高まりに合わせて、同国の豆類・特別栽培作物農家を強化するために430万米ドル以上を拠出することを約束しました。

米国は北米の大豆生産量の90%以上を占める

- 米国とカナダは北米最大の大豆生産国です。米国は世界全体の大豆生産量の約3分の1を生産し、ブラジルとアルゼンチンが僅差で続きます。2021年には1億1,988万トンの大豆を生産し、世界の大豆生産量の31%を占めました。世界的に取引される商品である大豆は、温帯および熱帯気候で生育し、タンパク質と植物油の重要な供給源となっています。食品消費パターンの変化、ベジタリアンタンパク源への嗜好の高まり、食品要件の進化が、米国の大豆タンパク質原料市場を促進する主な要因です。

- しかし、国内のニーズに応えるため、米国は2023年に279億4,000万米ドルの大豆を輸出しました。中国、欧州、メキシコ、日本、インドネシアが米国産大豆の主な輸出先として浮上しました。米国の農家は技術革新を受け入れ、再生農業とバイオテクノロジーを活用して、国内外の需要に応えています。全米大豆委員会(United Soybean Board)は農家と協力し、効率と大豆の品質を向上させるベストプラクティスを推進しています。

- カナダは北米で第3位の大豆生産国であるが、特にケベック州、マニトバ州、マリタイムズ州、サスカチュワン州南東部、アルバータ州南部などの地域で、大豆が換金作物として脚光を浴びています。カナダには200種類の登録大豆品種があり、その80%は除草剤耐性です。

北米の大豆たんぱく質産業概要

北米の大豆たんぱく質市場は適度に統合されており、上位5社で54.20%を占めています。この市場の主要企業は以下の通りです。Archer Daniels Midland Company, Bunge Limited, CHS Inc., International Flavors & Fragrances, Inc. and Kerry Group PLC(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- カナダ

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 単離液

- テクスチャー/加水分解

- エンドユーザー

- 飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養および医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

第5章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- A. Costantino & C. SpA

- Archer Daniels Midland Company

- Bunge Limited

- CHS Inc.

- Farbest-Tallman Foods Corporation

- Foodchem International Corporation

- International Flavors & Fragrances, Inc.

- Kerry Group PLC

- The Scoular Company

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The North America Soy Protein Market size is estimated at 3.58 billion USD in 2025, and is expected to reach 4.43 billion USD by 2030, growing at a CAGR of 4.33% during the forecast period (2025-2030).

The F&B segment has major applications of soy protein due to the form's high nutritional properties

- In 2022, the food and beverages segment emerged as the top end user segment by value share. Within this segment, meat and its alternatives, particularly those utilizing soy proteins, commanded the highest share of 46%. Soy proteins, known for their versatility, are instrumental in creating meat-like textures such as chunks, shreds, and strips, enhancing the appeal of meat-free options. Notably, in 2021, a quarter of Americans turned to plant-based meat alternatives, citing health and environmental concerns, further fueling this sub-segment's growth.

- In the animal feed segment, soy proteins, predominantly in concentrate form, play a pivotal role. Their popularity stems from attributes like easy digestibility, extended shelf-life, and potent protein fortification. As a result, soy proteins have become the go-to protein source in the diets of various farm animals, from ruminants and pigs to poultry and aquaculture. This trend aligns with the region's increasing recognition of soy proteins' significance in animal feed. Projections indicate this end user segment will see a steady CAGR of 3.20% over the forecast period in the North American market.

- Supplements are poised for rapid growth, with a projected CAGR of 5.92% over the forecast period. This surge is fueled by a heightened interest in fitness among consumers, particularly in sports and performance nutrition. With a growing number of fitness enthusiasts and vegan gym-goers relying on proteins for muscle-building, the demand for supplements is on the rise. Female athletes, in particular, are turning to soy protein powder as an ergogenic aid, not only to boost performance but also to hasten muscle recovery, offering potential benefits in conditions like osteoporosis.

The United States holds a significant market share owing to favorable government initiatives

- In 2022, the United States led the North American soy protein market, buoyed by robust government initiatives and promotions aimed at bolstering soy protein consumption. The food and beverages segment, along with the animal feed segment, collectively commanded the largest share, with the former at 51.1% and the latter at 47.8%. Notably, the thriving poultry industry, a significant consumer of soy protein, played a pivotal role. For instance, per capita poultry consumption, encompassing broilers, other chickens, and turkeys, climbed from 107.6 pounds in 2016 to 113.4 pounds in 2021.

- Within the food and beverage landscape, meat, poultry, seafood, and their alternatives held a commanding 42.5% market share in 2022. Consumers, increasingly health-conscious, are pivoting toward products that promote well-being. This shift is largely attributed to a heightened awareness of the adverse effects of traditional meat consumption. Consequently, the demand for meat alternatives and analogs has surged in recent years.

- While the United States led the pack in 2022, Canada and Mexico followed suit. Mexico, although in its infancy in the soy protein market, shows promising growth prospects, especially given its burgeoning food and beverages segment. With a strong inclination toward traditional, often meat-centric, foods, Mexican manufacturers are innovating to replicate meat's properties, texture, flavor, and aroma. Consequently, the food and beverages segment of the Mexican soy protein market is poised to witness the swiftest CAGR of 5.40% during the forecast period.

North America Soy Protein Market Trends

Plant protein consumption growth fuels opportunities for key players in the ingredients industry

- From 2017 to 2022, the region saw a 2.42% increase in per capita plant protein consumption, driven by investments and innovations. This surge was primarily fueled by a growing number of consumers shifting toward vegan or vegetarian diets, largely motivated by concerns for animal welfare. Notably, in 2020, approximately 9.6 million more Americans adopted plant-based diets, constituting nearly 3% of the US population. After the COVID-19 pandemic, plant protein consumption surged, partly due to concerns over viral contamination in animal-sourced proteins and a general increase in protein blends, including both animal and plant sources.

- While most Americans are reducing their meat intake, they are not eliminating it, leaning more toward a flexitarian diet than strict veganism or vegetarianism. Plant proteins find significant usage in sports nutrition and as meat alternatives. Soy and whey proteins, in particular, are prevalent in food and beverage, supplements, and sports nutrition. By 2021, 36% of US consumers were familiar with and had consumed soy protein, with a slightly lower share of 31% having tried whey protein.

- Canada boasts the second-largest flexitarian population, showcasing a significant shift toward flexitarianism and veganism among consumers. This trend presents a ripe opportunity for manufacturers to further innovate in the plant protein market. In 2021, the Canadian government pledged over USD 4.3 million to bolster the country's pulse and special crop farmers, aligning with the rising consumer appetite for sustainable, high-quality plant-based proteins.

The United States produces more than 90% of all soybeans in North America

- The United States and Canada are the largest soybean producers in North America. The United States produces about one-third of the total soybeans globally, followed closely by Brazil and Argentina. In 2021, the country produced 119.88 million metric tons of soybeans, accounting for a 31% share of global soybean production. Soy, a globally traded commodity, thrives in temperate and tropical climates, serving as a vital source of protein and vegetable oils. Shifting food consumption patterns, a growing preference for vegetarian protein sources, and evolving food requirements are key drivers driving the US soy protein ingredients market.

- However, catering to domestic needs, the United States exported soybeans worth USD 27.94 billion in 2023. China, Europe, Mexico, Japan, and Indonesia emerged as primary destinations for US soybean exports. Farmers in the United States are embracing innovation and leveraging regenerative agriculture and biotechnology to meet domestic and international demands. The United Soybean Board collaborates with farmers, promoting best practices to enhance efficiency and bean quality.

- Canada, while being the third-largest producer of soybeans in North America, has seen soybeans gain prominence as a cash crop, particularly in regions like Quebec, Manitoba, the Maritimes, southeast Saskatchewan, and southern Alberta. Canada boasts 200 registered soybean varieties, with a significant 80% being herbicide-tolerant.

North America Soy Protein Industry Overview

The North America Soy Protein Market is moderately consolidated, with the top five companies occupying 54.20%. The major players in this market are Archer Daniels Midland Company, Bunge Limited, CHS Inc., International Flavors & Fragrances, Inc. and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 Canada

- 3.4.2 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Supplements

- 4.2.3.1 By Sub End User

- 4.2.3.1.1 Baby Food and Infant Formula

- 4.2.3.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.3.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.3.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 Bunge Limited

- 5.4.4 CHS Inc.

- 5.4.5 Farbest-Tallman Foods Corporation

- 5.4.6 Foodchem International Corporation

- 5.4.7 International Flavors & Fragrances, Inc.

- 5.4.8 Kerry Group PLC

- 5.4.9 The Scoular Company

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms