|

市場調査レポート

商品コード

1690983

欧州の大豆たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の大豆たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

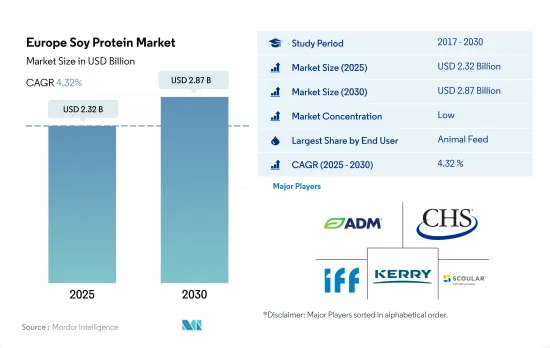

欧州の大豆たんぱく質市場規模は2025年に23億2,000万米ドルと推定され、2030年には28億7,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは4.32%で成長すると予測されています。

動物飼料セグメントは、その適合性と消化性の要因から大きな市場シェアを占めています。

- 大豆たんぱく質は、動物飼料産業において予測期間中に金額ベースでCAGR 2.65%を記録すると予測されます。欧州連合(EU)は毎年1,850万トンの大豆粕を輸入しており、そのうち95%は家畜への給餌用です。動物飼料用大豆たんぱく質の需要は、政府の取り組みとメーカーの競争力強化によって大きく伸びた。例えば、欧州配合飼料産業連盟(FEFAC)が発表したプロテイン・プランは、大豆たんぱく質を含む動物飼料業界における植物性たん白の需要を大幅に押し上げました。

- F&B産業はもう一つの主要なエンドユーザー・セグメントであり、主にRTE/RTC食品のサブセグメントにおける需要の急増によって牽引されています。従って、このセグメントは金額ベースで8.99%の最速CAGRで推移すると予測されます。欧州では、フレキシタリアン人口は近年130万人から約260万人に倍増し、2020年には人口の3.2%を占める。ベジタリアン、ペスカタリアン、フレキシタリアンの合計は、2020年には人口の約30.9%を占める。大豆たんぱく質は動物性食品の代替品としても機能し、高い消化率、優れたアミノ酸プロファイル、低レベルの抗栄養因子、長い保存性など、数多くの機能性を提供します。

- 大豆たんぱく質はサプリメント分野で大きなシェアを占めています。予測期間中、金額ベースで6.19%の成長を記録すると予測されています。大豆たんぱく質は、コレステロール値を下げる性質があり、栄養価の高い食物繊維を含んでいます。2021年には、高コレステロール血症に罹患している欧州人が約250万人いた。大豆たんぱく質の市場は、サプリメント分野における栄養価の上昇と健康上の利点により、需要の増加を示しました。

ロシアが欧州市場を独占しており、その主な要因は大規模な消費者ベースとF&Bセグメントからの高い需要です。

- 2020年、ロシアの大豆たんぱく質市場は前年比3倍の大幅な伸びを示し、金額で8%の増加を記録しました。この急成長の主な要因は、同国の原材料価格の上昇です。大豆の輸出関税導入などロシア政府の努力にもかかわらず、中央連邦管区の価格は上昇を続けた。その結果、大豆たんぱく質価格(特にSPI)は2020年に0.21%上昇し、過去4年間の平均上昇率0.16%を上回りました。

- 予測期間中のCAGRは5.14%と予測され、金額ベースではフランスが市場をリードする見通しです。フランスは、2022年からたんぱく質を多く含む作物、特に大豆の栽培面積を40%拡大する野心的な計画を発表しており、今後10年間でこの栽培面積を倍増させることを目標としています。この戦略的な動きは、大豆たんぱく質の価格を下げ、売上を強化することを目的としています。さらに、AFNOR(フランス規格協会)は、国内で販売される大豆ジュースは、100mlあたり最低3.2gの大豆たんぱく質を含み、乳製品の痕跡がないことを義務付けています。この規制は、国内メーカーに有利な機会をもたらします。

- 2022年現在、ロシアはこの地域における大豆たんぱく質の主要消費国としての地位を維持しています。予測期間中のCAGRは4.29%で、この優位性は維持されます。ロシアの大豆たんぱく質に対する意欲は、その大規模な消費者基盤に大きく後押しされており、2020年には飲食品(F&B)分野だけで44.35%の数量シェアを占める。大豆を動物性たんぱく質に代わる手頃で健康的な食品と考える消費者が増えており、大豆製品の需要は今後数年で急増すると予想されます。

欧州の大豆たんぱく質市場動向

植物性たんぱく質消費の成長が市場の主要企業に機会を提供

- 菜食主義への消費者シフトが市場を牽引しています。信頼性の高い植物性たんぱく質製品が提供する機能的効率性とコスト競争力は、多種多様な加工食品への利用を増加させています。大豆由来の植物性たんぱく質は、あらゆる年齢層にとって健康的であり、体の健康維持に役立つと考えられています。代替植物性たんぱく質は、飲食品業界で広く利用されています。

- この地域には、食生活を植物性たんぱく質源に切り替えようとする消費者の間で未開発の可能性があります。例えば、4年以内に菜食主義者の数は2016年の130万人から2020年には260万人に倍増します。しかし、市場は技術革新の欠如や公共政策の制限といった課題に直面しています。遺伝子組み換え作物の存在の可能性、製品構成に使用される原材料の原産地に対する疑念、作物への除草剤の使用の可能性など、イタリアの消費者の移行を妨げている側面がまだいくつかあります。

- 植物性たんぱく質は、食品の栄養価や機能性を高め、おいしさを提供します。同市場では、地域全体で植物性食品の消費が約45~50%増加しています。例えば、Bolthouse Farms社は、コールドプレスジュースやビーガンプロテインシェイクを含む「1915 Organic」ブランドラインで飲料製品レンジを拡大しました。また、プロテイン・メーカーは、この地域における大豆たんぱく質などの植物性タンパク源の消費向上に影響を与える戦略的プログラムを開始しようとしています。例えば、Donau Sojaは2023年に欧州のプロテイン戦略を開発し、この地域における大豆の入手可能性に影響を与えました。

大豆生産の減少は欧州の価格に影響を与えると予想される

- 2017年の世界の大豆生産量に占める欧州の割合は約12%でした。2021年には、同地域で1,000万トン近くの大豆が生産され、そのうち80%が飼料用でした。同地域では主に大豆ミールと大豆ケーキを輸入し、飼料として利用しています。多くの欧州諸国は不可欠な積み替えハブであり、輸入の一部が豆として再輸出されるか、加工された後に大豆ミールや油として輸出されることを意味しています。2018年7月、中国は大豆を含む米国からの輸入品に25%の関税を課しました。その結果、米国の余剰分はラテンアメリカや欧州の他の国々に輸出されました。

- FEFAC調達ガイドラインに準拠した大豆の消費量は、2019年の42.2%から2020年には43.8%に増加しました。同じ期間に、認証された無転換大豆の割合は25.3%から25.9%へとわずかに上昇しました。同地域では、非遺伝子組み換え大豆に対する需要も認識されています。欧州諸国からの非遺伝子組換え大豆の需要が伸びているにもかかわらず、2016年には世界全体の66.1%を占め、世界最大の大豆消費国としての役割を担っていることから、中国ではVSS適合大豆の需要が伸びています。

- 欧州では消費者の嗜好が変化しており、食肉に代わる植物性たんぱく質製品を食生活に取り入れています。この要因は、豆腐、大豆ベースの乳製品代替品、植物性食肉加工品など、同地域における大豆ベースの製品の消費に大きく寄与しています。植物由来の食品・飲料製品の売上高は、2018年の24億ユーロから2020年には36億ユーロへと49%増加します。

欧州の大豆たんぱく質産業の概要

欧州の大豆たんぱく質市場は断片化されており、上位5社で25.65%を占めています。この市場の主要企業は以下の通りです。 Archer Daniels Midland Company, CHS Inc., International Flavors & Fragrances Inc., Kerry Group PLC and The Scoular Company(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 単離液

- テクスチャー/加水分解

- エンドユーザー

- 飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他欧州

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- A. Costantino & C. SpA

- Archer Daniels Midland Company

- CHS Inc.

- Fuji Oil Group

- International Flavors & Fragrances Inc.

- Kerry Group PLC

- The Scoular Company

- Wilmar International Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Soy Protein Market size is estimated at 2.32 billion USD in 2025, and is expected to reach 2.87 billion USD by 2030, growing at a CAGR of 4.32% during the forecast period (2025-2030).

The animal feed segment holds a significant market share due to its suitability and digestibility factors

- Soy protein is projected to register a CAGR of 2.65% by value during the forecast period in the animal feed industry. The European Union imports 18.5 million tonnes of soybean meal every year, of which 95% goes toward feeding animals. The demand for soy protein in animal feed witnessed a major push due to government initiatives and manufacturers' increased competitiveness. For instance, the Protein Plan announced by the European Federation of the Compound Feed Industry (FEFAC) boosted the demand for plant proteins significantly in the animal feed industry, including soy protein.

- The F&B industry is another key end-user segment, primarily driven by the surging demand in the RTE/RTC foods sub-segment. Thus, the segment is projected to witness the fastest CAGR of 8.99% by value. In Europe, the flexitarian population has doubled from 1.3 million to around 2.6 million in recent years, representing 3.2% of the population in 2020. Vegetarians, pescatarians, and flexitarians, the group in total, represented about 30.9% of the population in 2020. Soy protein also serves as an alternative to animal-derived meals and provides numerous functionalities like high digestibility, a great amino acid profile, a low level of anti-nutritional factors, and long shelf life.

- Soy protein holds a significant share of the supplements segment. It is projected to register a growth of 6.19% by value during the forecast period. Soy protein has the properties of lowering cholesterol levels and its high nutritional fiber content. In 2021, there were about 2.5 million Europeans affected with hypercholesterolemia. The market for soy protein witnessed an increase in demand due to the rising nutritional values and health benefits in the supplements segment.

Russia dominates the European market, majorly driven by a large consumer base and high demand from the F&B segment

- In 2020, the soy protein market in Russia saw a significant three-fold year-on-year growth, recording an 8% increase in value. This surge was primarily attributed to the country's rising raw material prices. Despite the Russian government's efforts, including the introduction of export customs duties on soybeans, prices in the Central Federal District continued to climb. Consequently, soy protein prices, specifically SPI, rose by 0.21% in 2020, outpacing the 0.16% average growth seen in the preceding four years.

- France is poised to lead the market in terms of value, with a projected CAGR of 5.14% over the forecast period. The nation had announced ambitious plans to expand its cultivation of protein-rich crops, notably soy, by 40% starting in 2022, with a goal to double this acreage over the next decade. This strategic move aims to drive down soy protein prices, thereby bolstering sales. Additionally, AFNOR (Association Francaise de Normalization) has mandated that domestically sold soy juices contain a minimum of 3.2 g of soy protein per 100 ml and must be free from any dairy traces. This regulation presents a lucrative opportunity for manufacturers in the country.

- As of 2022, Russia retained its position as the leading consumer of soy protein in the region. The country is set to maintain this dominance, with a CAGR of 4.29% over the forecast period. Russia's appetite for soy protein is largely fueled by its sizable consumer base, with the food and beverage (F&B) segment alone commanding a 44.35% volume share in 2020. With a growing number of consumers viewing soybeans as an affordable and healthy alternative to animal proteins, the demand for soy products is expected to surge in the coming years.

Europe Soy Protein Market Trends

The growth in plant protein consumption provides opportunities for key players in the market

- The consumer shift toward vegan diets majorly drives the market. The functional efficiency and cost competitiveness offered by reliable plant protein products are increasing their utilization in a wide variety of processed foods. Plant protein from soy is considered healthy for all age groups and helps keep the body fit. Plant-based protein alternatives are being widely used in the food and beverage industry.

- The region has untapped potential among consumers willing to switch their diets to plant-based protein sources. For instance, within four years, the number of vegans doubled from 1.3 million in 2016 to 2.6 million in 2020. However, the market faces challenges, such as a lack of innovation and restrictions on public policy. There are still a few aspects holding back Italian consumers from making the shift, such as the possible presence of GMOs, doubts over the origin of raw materials used in the product's composition, and the possible use of herbicides on crops.

- Plant protein enhances food items' nutritional and functional values and provides good taste. The market observed an increase of around 45-50% in the consumption of plant-based food across the region. For instance, Bolthouse Farms expanded its beverage range with the "1915 Organic" brand line, which includes cold-pressed juices and vegan protein shakes. Also, protein manufacturers are trying to initiate strategic programs that will impact the improvement of consumption of plant protein sources such as soy protein in the region. For instance, Donau Soja developed a Protein Strategy for Europe in 2023, impacting the availability of soybeans in the region.

The decline in soy production is expected to impact prices in Europe

- Europe accounted for about 12% of the global soybean production in 2017. In 2021, nearly 10 MMT of soybean was produced in the region, of which 80% accounted for animal feed usage. It mainly imports soy meal and cake to be used as animal feed. Many European countries are essential trans-shipment hubs, implying that a portion of their imports is re-exported as beans or processed and then exported as soy meal and oil. In July 2018, China imposed a 25% tariff on imports from the United States, including soybeans. The resulting US surplus was then exported to other countries in Latin America and Europe.

- The consumption of soy that complies with the FEFAC Sourcing Guidelines increased from 42.2% in 2019 to 43.8% in 2020. In the same time frame, the proportion of certified conversion-free soy climbed marginally from 25.3% to 25.9%. The region also has a recognizable demand for non-GM soybeans. Despite the growing demand for non-GM soybeans from European countries, there is a growing demand for VSS-compliant soybeans in China, given the country's role as the world's largest soybean consumer, accounting for 66.1% of the global total in 2016.

- There is a shift in consumer preferences in Europe, as they are adding plant-based protein products to their diets that act as meat substitutes, owing to the increasing concerns by governments about the environmental and health impacts of producing and consuming animal meat. This factor substantially benefits the consumption of soybean-based products in the region, including tofu, soybean-based dairy substitutes, and processed plant-based meat products. There was an increase in the sales of plant-based food and drink products from EUR 2.4 billion in 2018 to EUR 3.6 billion in 2020, a growth of 49%.

Europe Soy Protein Industry Overview

The Europe Soy Protein Market is fragmented, with the top five companies occupying 25.65%. The major players in this market are Archer Daniels Midland Company, CHS Inc., International Flavors & Fragrances Inc., Kerry Group PLC and The Scoular Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 France

- 3.4.2 Germany

- 3.4.3 Italy

- 3.4.4 United Kingdom

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Belgium

- 4.3.2 France

- 4.3.3 Germany

- 4.3.4 Italy

- 4.3.5 Netherlands

- 4.3.6 Russia

- 4.3.7 Spain

- 4.3.8 Turkey

- 4.3.9 United Kingdom

- 4.3.10 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 CHS Inc.

- 5.4.4 Fuji Oil Group

- 5.4.5 International Flavors & Fragrances Inc.

- 5.4.6 Kerry Group PLC

- 5.4.7 The Scoular Company

- 5.4.8 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms