|

市場調査レポート

商品コード

1690987

ドイツの大豆タンパク質- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Germany Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの大豆タンパク質- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

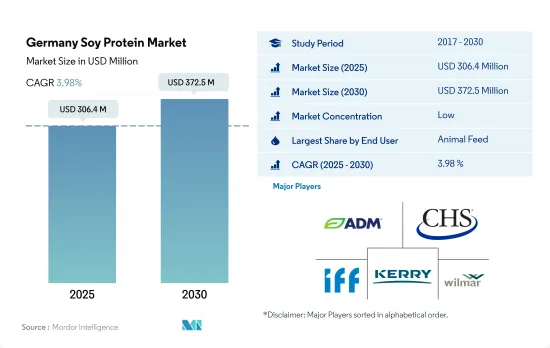

ドイツの大豆タンパク質市場規模は2025年に3億640万米ドルと推定され、2030年には3億7,250万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.98%で成長します。

大豆タンパク質のアミノ酸バランスとフィットネス産業の成長がセグメント収益に影響

- 動物飼料は引き続き大豆タンパク質の国内主要用途セグメントであり、予測期間中のCAGRは金額ベースで3.84%と予測されます。製造業者は常に、高品質でコスト効率が高く、ラベルに表示しやすい新規のタンパク質原料を探しており、大豆タンパク質の成長を牽引しています。大豆粕は、この地域の動物用飼料製剤に使用される主要タンパク質・アミノ酸源です。大豆タンパク質粉末は、コンパニオンアニマルフード、子牛の代用乳、幼すう動物用飼料(子豚用飼料など)、水産養殖用飼料に栄養面と機能面の両方のメリットをもたらします。特に、抗原性が低く消化しやすいことが要求される流動食や乾燥食の用途に適しています。

- F&Bセグメントは第2位の市場シェアを占め、予測期間のCAGRは金額ベースで2.96%と予測されています。大豆タンパク質は、肉や乳製品の代替製品に幅広く応用されています。大豆タンパク質は、産業の継続的な技術革新により、肉代替製品に広く使用されています。フレキシタリアンは2021年にドイツ人口の31.1%を占め、約1,671万人のグループを構成しています。同地域におけるヴィーガンとフレキシタリアン消費者の増加は、肉代替製品産業における大豆タンパク質需要を押し上げました。

- サプリメントセグメントは市場で最も急成長しているエンドユーザーセグメントであり、予測期間中に数量ベースでCAGR 7.93%を記録すると予測されています。2021年、ドイツには949万2,000以上のヘルス&フィットネスクラブが存在しました。フィットネス産業では、トレーニング後の筋肉や組織の修復に使用される栄養補助食品において、様々なタンパク質成分の使用量が急速に増加しています。したがって、大豆タンパク質粉末は市場でより多くの需要を獲得しています。

ドイツの大豆タンパク質市場動向

植物性タンパク質の消費拡大が原料セグメントの主要企業に機会を与える

- ドイツの植物性タンパク質市場は、その機能的効率性、大豆、小麦、エンドウ豆などの信頼性の高い植物性タンパク質製品が提供するコスト競合、様々な加工食品への応用の増加により、消費者のヴィーガン食への転換が進んでいることが牽引しています。大豆タンパク質はあらゆる年齢層にとって健康的であり、適切な身体機能の維持に役立つと考えられています。代替植物性タンパク質は、飲食品やサプリメントセグメントで広く使用されています。これらは大豆、小麦、その他の野菜などの供給源から得られるが、これらは飲食品セグメントに欠かせないものであり、ドイツにおける植物性タンパク質消費を後押ししています。より多くの消費者がヴィーガン食を好むようになり、ドイツにおけるヴィーガン人口は倍増し、2016~2020年にかけて260万人に達し、人口の3.2%を占めるようになりました。

- 食肉消費を抑制することで肥満や糖尿病などの様々な疾病を減少させようとする政府の好意的な施策により、小麦タンパク質への消費者シフトが進む可能性があります。ドイツでは人口の少なくとも7.2%が糖尿病を患っており、そのほとんどが2型糖尿病です。糖尿病患者の数は、今後20年間で大幅に増加すると予想されています。

- クリーンラベル原料への需要の高まりと食品当局による厳しい表示規制により、食品メーカーは天然原料の採用を余儀なくされています。そのため、同市場で事業を展開する原料メーカーは、増大する需要に対応し競争上の優位性を獲得するため、革新的な原料の開発に注力しています。ドイツではヴィーガン食品の需要が高まっており、乳糖不耐症の消費者も増加しています。その結果、植物性タンパク質全体の消費量は2017年の47gから2022年には53gに増加しました。

大豆タンパク質が日常消費の一部として受け入れられるようになったため、ドイツの大豆生産量は10年間で10倍に増加しました。

- ドイツの大豆生産量は、食生活の一部として大豆を受け入れる消費者の増加に伴い、ここ数年で急速に増加しました。ドイツでは2020年に約9万4,100トンの大豆が収穫され、これは過去最大の量となりました。収量が減少したにもかかわらず、2020年の生産量は平均で12%増加し、2018年と比較して60%も増加しました。ドイツの大豆生産は、生産面積の着実な拡大により、2012年以降10倍以上に増加しています。2020年収穫の大豆面積は32,900ヘクタールで、前年比14%増となりました。一方、収量は若干減少しました。

- 過去数十年間で、大豆栽培は爆発的に増加し、1960年の約1,700万トンから現在では3億トンを超えています。例えば、大豆の約25~30%は国内で生産されています。収量が最も減少したのはドイツ西部です。ノルトライン=ヴェストファーレン州の収穫量は前年より約25%減少し、ヘッセン州の収穫量は20%減少しました。しかし、ヘッセン州とメクレンブルク=西ポメラニア州の生産地域は2020年に大幅に拡大したため、同地域の大豆生産量は2019年よりも増加しました。南ドイツの収量もわずかに減少し、東ドイツの収量は大幅に増加しました。ザクセン=アンハルト州は130%増の23.2デシトン/ヘクタールと最大の伸びを記録しました。

- この地域では遺伝子組み換え作物への需要が増加しており、生産量の大半を占めています。大量の遺伝子組み換え大豆は、ドイツや欧州連合(EU)ではそのように表示されなければならないが、食品トラフを経由してスーパーマーケットの棚に無表示で並ぶ。ドイツの栽培農業従事者は、10℃以下の気温にも耐えられるよう、耐寒性豆の栽培を計画しています。

ドイツの大豆タンパク質産業概要

ドイツの大豆タンパク質市場はセグメント化されており、上位5社で24.96%を占めています。この市場の主要企業は、 Archer Daniels Midland Company、CHS Inc.、International Flavors & Fragrances Inc.、Kerry Group PLC、Wilmar International Ltdなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- ドイツ

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 単離液

- テクスチャー/加水分解

- エンドユーザー

- 飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- A. Costantino & C. SpA

- Archer Daniels Midland Company

- Brenntag SE

- CHS Inc.

- Foodchem International Corporation

- Fuji Oil Group

- International Flavors & Fragrances Inc.

- Kerry Group PLC

- The Scoular Company

- Wilmar International Ltd

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Germany Soy Protein Market size is estimated at 306.4 million USD in 2025, and is expected to reach 372.5 million USD by 2030, growing at a CAGR of 3.98% during the forecast period (2025-2030).

Growing fitness industry with balance of amino acids in soy proteins influence the segmental revenue

- Animal feed remained the country's leading application sector for soy protein, and it is projected to register a CAGR of 3.84% by value in the forecast period. Manufacturers are constantly looking for novel protein ingredients that are high-quality, cost-effective, and label-friendly, driving the growth of soy protein. Soybean meal is the main source of protein and amino acids used in animal feed formulations in the region. Soy protein powders provide both nutritional and functional benefits in companion animal foods, calf milk replacers, young animal feed (such as feed for piglets), and aquaculture diets. It is especially suited for liquid and dry food applications where low antigenicity and easy digestibility are required.

- The F&B segment holds the second major market share and is projected to register a CAGR of 2.96% by value in the forecast period. Soy proteins have a wide range of applications in meat- and dairy-alternative products. Soy protein was widely used in meat alternatives due to the industry's ongoing innovation. Flexitarians accounted for 31.1% of the German population in 2021, making up a group of approximately 16.71 million people. The increase in vegan and flexitarian consumers in the region boosted the soy protein demand in the meat alternative products industry.

- The supplements segment is anticipated to be the fastest-growing end-user segment in the market, projected to register a CAGR of 7.93% by volume during the forecast period. In 2021, there were more than 9,492 thousand health and fitness clubs in Germany. The fitness industry is rapidly increasing the usage of various protein ingredients in nutritional supplements used for muscle or tissue repair after workouts. Thus, soy protein powders are gaining more demand in the market.

Germany Soy Protein Market Trends

The consumption growth of plant protein fuels opportunities for key players in the ingredients segment

- The German plant protein market is driven by consumers' increasing conversion toward vegan diets due to their functional efficiency, the cost competitiveness offered by reliable plant protein products such as soy, wheat, and pea, and their increasing application in various processed foods. Soy protein is considered healthy for all age groups and helps maintain proper body functions. Plant-based protein alternatives are widely used in the food and beverage and supplement segments. They can be derived from sources such as soy, wheat, and other vegetables, which are essential parts of the food and beverage segment, boosting plant protein consumption in Germany. As more consumers increased their preference for vegan diets, the number of vegans in Germany doubled, reaching 2.6 million people and accounting for 3.2% of the population from 2016 to 2020.

- Favorable government policies to reduce various diseases, such as obesity and diabetes, by controlling meat consumption may result in a growing consumer shift toward wheat protein. At least 7.2% of the population in Germany has diabetes, most of them type 2 diabetes. The number of people with diabetes is expected to increase significantly over the next two decades.

- The growing demand for clean-label ingredients and stringent labeling regulations by food authorities are compelling food manufacturers to adopt natural ingredients. Thus, ingredient manufacturers operating in the market focus on developing innovative ingredients to cater to the growing demand and achieve a competitive advantage. Germany has a rising demand for vegan food products and an increasing number of lactose-intolerant consumers. As a result, the overall plant protein consumption increased from 47 g in 2017 to 53 g in 2022.

Owing to the increased acceptance of soy protein as a part of daily consumption, Germany's soybean production increased tenfold in a decade

- Soybean production in Germany increased rapidly over the years, with an increase in the number of consumers accepting the crop as part of their diet. Around 94,100 tons of soybeans were harvested in Germany in 2020, which was recorded as the largest quantity ever. Production grew by 12% on average in 2020 despite lower yields and increased to as much as 60% compared to 2018. German soybean production has increased more than tenfold since 2012 due to a steady expansion in the production area. The soybean area for the 2020 harvest amounted to 32,900 hectares, up by 14% Y-o-Y. On the other hand, yields were slightly lower.

- Over past decades, soy cultivation has exploded, from around 17 million metric tons in 1960 to more than 300 million today. For instance, around 25-30% of soy is domestically produced. Western Germany saw the strongest drop in yields. North Rhine-Westphalia harvested around 25% less than the previous year, whereas yields in Hesse fell by 20%. However, since the production areas in Hesse and Mecklenburg-Western Pomerania significantly expanded in 2020, soybean output in the regions was larger than in 2019. Yields in South Germany were also slightly down, and those in Eastern Germany rose considerably. Saxony-Anhalt registered the biggest increase at 130% to 23.2 decitonnes per hectare.

- The demand for genetically modified crops is increasing in the region, catching up with most of the production in the area. Large quantities of genetically engineered soy, which has to be marked as such in Germany and the European Union, make their way unmarked onto the supermarket shelves via the food trough. German cultivators are planning to cultivate cold-proof beans so that the crop can tolerate temperatures below 10 °C.

Germany Soy Protein Industry Overview

The Germany Soy Protein Market is fragmented, with the top five companies occupying 24.96%. The major players in this market are Archer Daniels Midland Company, CHS Inc., International Flavors & Fragrances Inc., Kerry Group PLC and Wilmar International Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 Germany

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Supplements

- 4.2.3.1 By Sub End User

- 4.2.3.1.1 Baby Food and Infant Formula

- 4.2.3.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.3.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 Brenntag SE

- 5.4.4 CHS Inc.

- 5.4.5 Foodchem International Corporation

- 5.4.6 Fuji Oil Group

- 5.4.7 International Flavors & Fragrances Inc.

- 5.4.8 Kerry Group PLC

- 5.4.9 The Scoular Company

- 5.4.10 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms