|

市場調査レポート

商品コード

1692023

インドの大豆プロテイン- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの大豆プロテイン- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

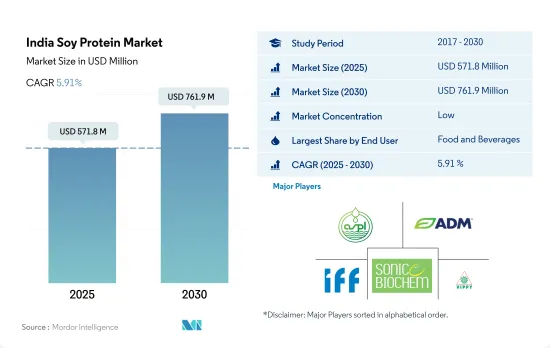

インドの大豆プロテイン市場規模は2025年に5億7,180万米ドルと推計され、2030年には7億6,190万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは5.91%で成長します。

タンパク質強化への嗜好の高まりとその適性が動物飼料と飲食品分野を牽引

- F&B分野は市場の大半の用途シェアを占めています。予測期間中、数量ベースでCAGR 6.06%を記録する見込みです。パーソナルケアと化粧品は、予測期間中に最も急成長するエンドユーザー・セグメントで、数量ベースのCAGRは8.25%と予想されます。インドはアジア太平洋で最もベジタリアンの数が多く、植物性タンパク質への需要を促進しています。2022年現在、インド人の24%が厳格なベジタリアンであり、9%がビーガン、8%がペスカタリアンです。肉の代替品や乳製品の代替品に対する需要の高まりや、ベジタリアニズムやビーガニズムの高まりが、飲食品需要を牽引しています。ヘルシーで外出先での食事オプションへの嗜好の高まりも市場拡大に寄与しています。2021年には、インド人の約70%が、全体的な健康と免疫力を向上させ、ストレスと不安を軽減するために、食生活の変化を優先させたいと考えていました。

- 大豆タンパク質は主に、F&Bセグメントにおける肉や乳製品の代替製品に使用されています。F&Bセグメントにおける数量シェアの約44.22%は肉および肉代替品、37.04%は乳製品および乳製品代替品です。大豆は強力な豆類であり、高水準のタンパク質とその他の栄養素を含むため、肉の代替が容易です。また、消化しやすく、肉のような食感もあります。タンパク質、カルシウム、ビタミンA・D、ビタミンBの含有量が牛乳に匹敵するため、大豆強化牛乳も人気があります。植物性タンパク質原料の使用における主な動向は、高タンパク質含有原料の入手可能性であるため、持続可能な供給源と提供される原料中のタンパク質の質に重点が移っています。

インドの大豆プロテイン市場動向

インドは植物性タンパク質の消費量において主要市場のひとつに浮上しつつあります。

- 大豆、米、エンドウ豆、小麦などの主要な植物性タンパク質の生産量の増加は、その供給源からのタンパク質原料の入手可能性に影響を及ぼしています。国内では多くの植物性食品が主食として消費されているが、革新的な食品の開発におけるこれらのタンパク質原料の用途の増加が消費をさらに押し上げています。インターネットに精通した若い世代の間でビーガンのインフルエンサーの数と関与能力が高まっており、2023年時点でビーガン食は健康的(74%)、環境に良い(72%)、倫理的に健全(73%)であると信じていることも、インドにおけるビーガン傾向の上昇に極めて重要であることが証明されています。これらは、植物性タンパク質の需要増加の一因となっています。

- 植物性タンパク質に対する認識が高まるにつれ、インドの消費者、特に若い世代は植物性タンパク質を強化した食品に目を向けています。例えば、2024年現在、インド人の50%近くが植物性乳製品に精通しており、27.5%が肉の代替品について認識しています。こうした製品の認知度は、大都市圏と月収10万インドルピー(1,200米ドル)から15万インドルピー(1,800米ドル)の個人で最も顕著です。過去6ヵ月間に植物性ミルクを購入した人のうち、82%が再度購入する意向を示し、ビーガンミートについても72%が同様の意向を示しています。

- さらに、2022年から2023年にかけて、インドの人口のかなりの部分、80%近くが1日のタンパク質摂取量が不足しており、大多数(90%)が1日に推奨されるタンパク質の必要量を知りませんでした。このようなアンメットニーズから、植物性タンパク質に対する需要の増加が強く予測され、この栄養ギャップを満たすための持続可能で潜在的により利用しやすい代替食品が提供されます。

インドは世界の大豆生産量トップ5のひとつ

- 大豆は世界で最も重要なマメ科植物であり、植物種子油とタンパク質の最大の供給源です。官民の会社が協力して様々な技術を開発し、農家と直接関わることで、農家所得の向上と大豆収量の増加を図っています。2014年、マハラシュトラ州では大豆の生産量が減少を続けていたため、マハラシュトラ州政府と総合農業開発のための官民パートナーシップ(PPPIAD)は、ADMと共同で大豆栽培に新技術を導入し、農家の収量増加を支援しました。大豆は、インドの主要な油糧種子作物となっています。大豆を原料とする食品は一般に健康上の利点があり、高品質のタンパク質を安価に摂取できます。この作物には、国内の貧困層で蔓延しているタンパク質栄養失調を解消する可能性があります。

- 大豆の栽培面積は1,100万ha、生産量は1,153万トンで、マディヤ・プラデシュ州、マハラシュトラ州、ラジャスタン州、カルナタカ州、チャッティースガル州、テランガナ州の天水生態系におけるVertitsol栽培の場合、生産性は10.45q/ha(QE 2015-16)を記録しています。生産性には大きなばらつきがあり、カルナタカ州とチャティスガル州の9.5q/haからテランガナ州の14.8q/haまで、主に農場レベルの非効率が原因です。2020年のカリフシーズン、大豆栽培は120haで行われ、収量は約10万5,000トンでした。

- 地元の農家は、認証種子の不足とその法外な価格のために困難に直面しました。そのため、マハラシュトラ州やラジャスタン州など一部の州の農家は、市場の品薄を避けるために自家採種を行いました。主な大豆生産州は、マディヤ・プラデシュ州、マハラシュトラ州、ラジャスタン州、カルナタカ州、アンドラ・プラデシュ州、チャッティースガル州です。

インドの大豆プロテイン産業概要

インドの大豆プロテイン市場は断片化されており、上位5社で8.78%を占めています。この市場の主要企業は以下の通り。 Agro Solvent Products Pvt. Ltd, Archer Daniels Midland Company, International Flavors & Fragrances Inc., Sonic Biochem Extractions Pvt. Ltd and Vippy Industries Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 単離液

- テクスチャー/加水分解

- エンドユーザー

- 飼料

- 食品・飲料

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養および医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Agro Solvent Products Pvt. Ltd

- Archer Daniels Midland Company

- International Flavors & Fragrances Inc.

- Rejoice Life Ingredients

- Sonic Biochem Extractions Pvt. Ltd

- Vippy Industries Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The India Soy Protein Market size is estimated at 571.8 million USD in 2025, and is expected to reach 761.9 million USD by 2030, growing at a CAGR of 5.91% during the forecast period (2025-2030).

Increasing preference for protein fortification and it's suitability drives the animal feed and food and beverages sector

- The F&B segment controls the majority application share of the market. It is expected to record a CAGR of 6.06%, by volume, over the forecast period. Personal care and cosmetics is expected to be the fastest-growing end-user segment during the forecast period, with a CAGR of 8.25% by volume. India has the highest number of vegetarians in Asia-Pacific, fueling the country's demand for plant-based proteins. As of 2022, 24% of Indians were strictly vegetarian, 9% were vegan, and 8% were pescatarian. The growing demand for meat alternatives and dairy alternatives, as well as the rising vegetarianism and veganism, is driving the demand for food and beverages. The growing preference for healthy, on-the-go meal options is also contributing to market expansion. In 2021, approximately 70% of Indians were willing to prioritize dietary changes to improve their overall health and immunity and reduce stress and anxiety.

- Soy protein is primarily used for meat and dairy alternative products in the F&B segment. About 44.22% of the volume share in the F&B segment was held by meat and meat alternatives and 37.04% by dairy and dairy alternatives. Soybeans are powerful legumes with high levels of protein and other nutrients that can easily replace meat. They also offer easy digestibility and meat-like texture. Soy-fortified milk is also popular since its protein, calcium, vitamins A and D, and vitamin B content is comparable to cow's milk. The main trend in the use of plant protein ingredients has been the availability of high protein content ingredients, so the emphasis has shifted to sustainable sources and the quality of the protein in the ingredients offered.

India Soy Protein Market Trends

India emerging as one of the major markets in terms of plant protein consumption

- Increased production of major plant proteins, like soybean, rice, pea, and wheat, is impacting availability of protein ingredients from the sources. Although many plant products are consumed as staple foods in the country, the increased applications of these protein ingredients in developing innovative foods are further boosting their consumption. The increasing number and engagement capability of vegan influencers among the internet-savvy young generation, who also believed that a vegan diet is healthy (74%), good for the environment (72%), and ethically sound (73%) as of 2023, has proven to be pivotal in the rise of the veganism trend in India. These are among the factors contributing to the rising demand for plant-based protein.

- With the increasing awareness of plant proteins, Indian consumers, especially younger generations, are turning toward plant protein-fortified foods. For instance, as of 2024, nearly 50% of Indians are familiar with plant-based dairy products, and 27.5% are aware of meat alternatives. Awareness of these products is most prominent in metropolitan areas and among individuals with monthly incomes ranging from INR 100,000 (USD 1,200) to INR 150,000 (USD 1,800). Among those who purchased plant-based milk in the previous six months, 82% expressed a willingness to buy it again, with a comparable 72% indicating the same for vegan meat.

- Moreover, in 2022-2023, a significant portion of India's population, nearly 80%, was deficient in daily protein intake, and a vast majority (90%) was unaware of their recommended daily protein needs. This unmet need fuels a strong forecast for increased demand for plant-based proteins, offering a sustainable and potentially more accessible alternative to meet this nutritional gap.

India is one of the top five soybean producers in the world

- Soybean is the world's most important seed legume, being the largest source of vegetable seed oil and protein. Public and private companies are collaborating to develop various techniques and directly engaging with farmers to enhance farm incomes and increase soybean yield. In 2014, as soybean production continued to decline in Maharashtra, the State Government of Maharashtra and the Public-Private Partnership for Integrated Agriculture Development (PPPIAD) introduced new technologies in collaboration with ADM for soybean cultivation that aided farmers in increasing their yields. Soybean has turned out to be a major oilseed crop in India. The food derived from soybeans generally provides health benefits and is a cheaper source of high-quality protein. The crop has the potential to eliminate protein malnutrition prevailing in poor sections of society in the country.

- Soybean is cultivated over an area of 11.00 million ha, with a production of 11.53 million tons, registering productivity of 10.45 q/ha (QE 2015-16) under Vertitsol in the rainfed ecosystem in Madhya Pradesh, Maharashtra, Rajasthan, Karnataka, Chhattisgarh, and Telangana. There are wide variations in productivity, ranging from 9.5 q/ha in Karnataka and Chhattisgarh to 14.8 q/ha in Telangana, primarily due to farm-level inefficiencies. In the 2020 Kharif season, soybean cultivation took place in a 120-lakh-hectare area, with a yield of around 105 lakh tons.

- Local farmers encountered difficulties due to a lack of certified seeds and their exorbitant prices. Thus, farmers in a few states like Maharashtra and Rajasthan produced their own seeds to avoid market scarcity. The major soybean-growing states are Madhya Pradesh, Maharashtra, Rajasthan, Karnataka, Andhra Pradesh, and Chhattisgarh.

India Soy Protein Industry Overview

The India Soy Protein Market is fragmented, with the top five companies occupying 8.78%. The major players in this market are Agro Solvent Products Pvt. Ltd, Archer Daniels Midland Company, International Flavors & Fragrances Inc., Sonic Biochem Extractions Pvt. Ltd and Vippy Industries Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 India

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Supplements

- 4.2.3.1 By Sub End User

- 4.2.3.1.1 Baby Food and Infant Formula

- 4.2.3.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.3.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agro Solvent Products Pvt. Ltd

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 International Flavors & Fragrances Inc.

- 5.4.4 Rejoice Life Ingredients

- 5.4.5 Sonic Biochem Extractions Pvt. Ltd

- 5.4.6 Vippy Industries Limited

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms