アジア太平洋地域のアラミド繊維:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Aramid Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639384

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

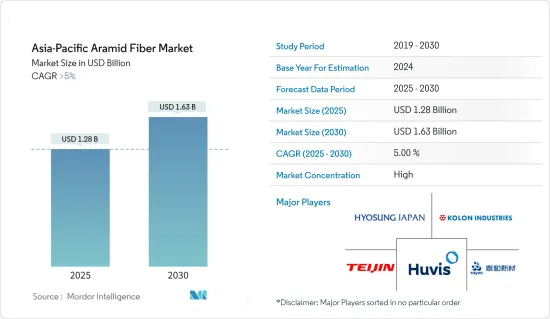

アジア太平洋地域のアラミド繊維の市場規模は、2025年に12億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5%を超え、2030年には16億3,000万米ドルに達すると予測されます。

アジア太平洋地域では、中国やインドのような国々がCOVIDパンデミックの被害を受け、市場に悪影響を与えました。パンデミックの影響で自動車や電子機器の製造活動が一時的に停止し、アラミド繊維の使用量が減少しました。しかし、規制が解除された後、市場は順調に回復しました。航空宇宙、防衛、自動車産業におけるアラミド繊維の消費増加により、市場は大幅に回復しました。

主なハイライト

- 自動車産業における軽量素材需要の増加、インドと中国の国防費の増加、鉄鋼素材の代替となりうるアラミド繊維の使用量の増加が市場を牽引すると予想されます。

- アラミド繊維のより良い代替品が入手可能であることと、アラミド繊維の非生分解性という性質が市場成長の妨げとなっています。

- 航空宇宙分野からの需要の増大とアラミド素材製造技術の進歩は、予測期間中に市場にチャンスをもたらすと予想されます。

- 中国は、航空宇宙・防衛、自動車エンドユーザー産業におけるアラミド繊維の需要増加により、市場を独占すると予想されます。また、予測期間中に最も高いCAGRで推移することが予想されます。

アジア太平洋地域のアラミド繊維市場動向

航空宇宙・防衛エンドユーザー産業が市場を独占

- アラミドは、熱気球やグライダーから戦闘機、旅客機、スペースシャトルに至るまで、あらゆる航空機や宇宙船の部品や構造用途に使用されています。アラミド繊維は一般に、翼アセンブリ、ヘリコプターのローターブレード、座席プロペラ、計器や内部部品のエンクロージャーなどに使用されています。

- 航空宇宙産業では、民間航空機の全天候型運航や視覚システムの強化のため、新世代の航空機を製造する際にアラミド繊維を使用する割合が年々高まっています。さらに、温度安定性や耐久性といった特性は、今後数年間の航空宇宙用複合材料市場の成長をさらに後押しすると思われます。

- 中国とインドは、この地域の航空宇宙・防衛産業にとって最大の市場です。中国は民間航空分野で最も急成長している国になると予想されています。同国の旅客数は前年比9.5%増となる見込みで、既存の民間航空機に加え、さらに6,800機の航空機が必要となります。この増加は、同国におけるアラミド繊維の需要を促進すると予想されます。

- ボーイングとエアバスは、中国で最も著名な民間航空機メーカーです。これらの企業の優位性を低下させるため、中国商用航空公司(COMAC)は国内で民間航空機の製造を開始しました。2022年9月、同社は中国初の国産旅客機を納入しました。さらに、中国商用航空総公司(COMAC)の年間生産能力は、5年間で約150機の国産C919に達します。

- さらに、インドでは新たなヘリコプター製造工場が加わり、ヘリコプターの生産量が増加しています。例えば、ナレンドラ・モディ首相は2023年、カルナタカ州にあるヒンドゥスタン・アエロノーティクス社(HAL)のヘリコプター製造工場を落成させました。この施設では、年間約30機のライト・ユーティリティ・ヘリコプター(LUH)を生産する予定です。段階的に年間60機、90機と増やしていくことも可能です。

- 同様に、インドでも国防費が増加しています。ストックホルム国際平和研究所(SIPRI)によると、2022年のインドの国防支出は814億米ドル(前年は760億米ドル)です。したがって、国防費の増加は同国のアラミド繊維市場を牽引することになります。

- このように、航空宇宙・防衛産業の成長は、この地域のアラミド繊維市場を牽引すると予想されます。

市場を独占する中国

- 中国は、この地域におけるアラミド繊維の重要な市場のひとつです。アラミド繊維は、航空宇宙や防衛など様々なエンドユーザー産業で使用されています。自動車、電気・電子機器、スポーツ用品などです。中国では、自動車と航空宇宙セクターが著しい市場成長を記録し、同国のアラミド繊維市場を牽引しています。

- 中国はこの地域で最大の自動車メーカーです。OICA(The Organisation Internationale des Constructeurs d'Automobiles)によると、中国の自動車生産台数は2022年に2,702万台に達し、前年同期比で3%増加しました。

- さらに、同国の自動車業界では、消費者のバッテリー駆動車への傾斜が高まっており、動向の転換が見られます。さらに、中国政府は2025年までに電気自動車生産の普及率が20%になると予測しています。これは、2022年に過去最高を記録した同国の電気自動車販売動向に反映されています。中国乗用車協会によると、2022年に政府が販売したEVとプラグインは567万台で、2021年に達成した販売台数のほぼ2倍に触れます。

- 中国は、この地域の航空機OEMにとって最大の市場です。ボーイングとエアバスは、中国で最も著名な民間航空機メーカーです。これらの企業の優位性を低下させるため、中国商用航空公司(COMAC)が国内で民間航空機の製造を開始しました。

- さらに、これらの企業の優位性を低下させるために、中国商用航空公司(COMAC)は国内で民間航空機の製造を開始しました。2022年9月、同社は中国初の国産旅客機を納入しました。さらに、中国商用航空総公司(COMAC)の年間生産能力は、5年間で約150機の国産C919です。

- 全体として、自動車や航空宇宙といった産業の成長が、予測期間中に同国のアラミド繊維市場を牽引するとみられます。

アジア太平洋地域のアラミド繊維産業の概要

アジア太平洋地域のアラミド繊維市場は、その性質上、統合されています。同市場の主要企業(順不同)には、Huvis Corp、HYOSUNG JAPAN、Kolon Industries Inc.、Teijin Aramid、Yantai Tayho Advanced Materialsなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車産業における軽量材料の需要増加

- インドと中国の防衛費の増加

- 鉄鋼材料の代替となりうるアラミド繊維の使用量の増加

- 抑制要因

- アラミド繊維のより優れた代替品の入手可能性

- アラミド繊維の非生分解性

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ別

- パラ系アラミド

- メタ系アラミド

- エンドユーザー産業別

- 航空宇宙・防衛

- 自動車

- 電気・電子

- スポーツ用品

- その他のエンドユーザー産業(石油・ガス、通信など)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- アジア太平洋地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- China National Bluestar(Group)Co. Ltd

- Dupont

- Hebei Silicon Valley Chemical Co. Ltd.

- Huvis Corp

- HYOSUNG JAPAN

- KERMEL

- Kolon Industries Inc.

- Shanghai J&S New Materials Co.,ltd

- Teijin Aramid

- TORAY INDUSTRIES, INC.

- X-FIPER New Material Co. Ltd.

- Yantai Tayho Advanced Materials Co.,Ltd.

第7章 市場機会と今後の動向

- 航空宇宙分野からの需要拡大

- アラミド素材製造技術の進歩

目次

The Asia-Pacific Aramid Fiber Market size is estimated at USD 1.28 billion in 2025, and is expected to reach USD 1.63 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

In Asia-Pacific, countries like China and India were worst hit by the COVID pandemic, negatively affecting the market. Automotive and electronic manufacturing activities were temporarily halted due to the pandemic, which had decreased the usage of aramid fibers. However, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of aramid fibers in the Aerospace and, defense, and automotive industries.

Key Highlights

- The increase in demand for lightweight materials in the automotive industry, the rising defense expenditure of India and China, and the increase in the usage of aramid fibers as a potential substitute for steel materials are expected to drive the market.

- The availability of better alternatives for aramid fibers and the non-biodegradable nature of aramid fibers are hindering market growth.

- The growing demand from the aerospace sector and advancements in aramid materials manufacturing technology are expected to create opportunities for the market during the forecast period.

- China is expected to dominate the market due to the rising demand for aramid fibers in the aerospace and defense, automotive end-user industries. It is also expected to register the highest CAGR during the forecast period.

Asia-Pacific Aramid Fibers Market Trends

Aerospace and Defense End-User Industry to Dominated the Market

- Aramids are used for components and structural applications in all aircraft and spacecraft, ranging from hot air balloons and gliders to fighter planes, passenger airliners, and space shuttles. The aramid fibers are generally used in wing assemblies, helicopter rotor blades, seat propellers, and enclosures for instruments and internal parts.

- Every year, the aerospace industry uses a higher proportion of aramid fibers in constructing each new generation of aircraft due to the provision of an all-weather operation of commercial aviation and enhanced vision systems. Moreover, characteristics such as temperature stability and durability will further fuel the growth of the aerospace composites market over the coming years.

- China and India are the region's largest markets for aerospace and defense industries. China is expected to be the fastest-growing country in the civil aviation sector. The government is expected to witness a 9.5% y-o-y passenger growth rate, which will require an additional 6,800 aircraft to add to the existing commercial fleet. This increase is expected to drive the demand for aramid fibers in the country.

- Boeing and Airbus are the most prominent civil aircraft manufacturers in China. To decrease the dominance of these companies Commercial Aviation Corp of China (COMAC) started to manufacture civil aircraft in the country. In September 2022, the company delivered its first homemade passenger jet in China. Furthermore, the reach of the annual production capacity of Commercial Aviation Corp of China (COMAC) is around 150 domestically produced C919 planes in five years.

- Furthermore, the production volume of helicopters is increasing in India with the addition of new helicopter manufacturing plants. For instance, in 2023, Prime Minister Narendra Modi inaugurated the helicopter manufacturing factory of Hindustan Aeronautics Limited (HAL) in Karnataka. The facility will produce around 30 Light Utility Helicopters (LUHs) annually. It can be enhanced to 60 and then 90 per year in a phased manner.

- Similarly, the defense expenditure is increasing in India. According to the Stockholm International Peace Research Institute (SIPRI), in 2022, the defense expenditure in India is registered at USD 81.4 billion, as compared to USD 76 billion expenditure in the previous year. Thus the increase in defense expenditure will drive the market for aramid fibers in the country.

- Thus, the growth in the aerospace and defense industries is expected to drive the market for aramid fibers in the region.

China to Dominate the Market

- China is one of the significant markets for Aramid Fibers in the region. Aramid fibers are used in various end-user industries, such as aerospace and defense. Automotive, electric and electronics, and sporting goods. In China, the automotive and aerospace sectors registered significant market growth, thereby driving the market for aramid fibers in the country.

- China is the largest automotive vehicle manufacturer in the region. According to OICA (The Organisation Internationale des Constructeurs d'Automobiles), automotive vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over the previous year for the same period.

- Moreover, the automobile industry in the country is witnessing switching trends as the consumer inclination toward battery-operated vehicles is on the higher side. Furthermore, the government of China estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the electric vehicle sales trend in the country, which went to a record-breaking high in 2022. As per the China Passenger Car Association, the government sold 5.67 million EVs and plug-ins in 2022, touching almost double the sales figures achieved in 2021.

- China is the largest market for airplane OEMs in the region. Boeing and Airbus are the most prominent civil aircraft manufacturers in China. To decrease the dominance of these companies, the Commercial Aviation Corp of China (COMAC) started to manufacture civil aircraft in the country.

- Furthermore, to decrease the dominance of these companies, the Commercial Aviation Corp of China (COMAC) started to manufacture civil aircraft in the country. In September 2022, the company delivered its first homemade passenger jet in China. Furthermore, the annual production capacity of Commercial Aviation Corp of China (COMAC) is around 150 domestically produced C919 planes in five years.

- Overall, the growth of industries such as automotive and aerospace are likely to drive the market for aramid fibers in the country during the forecast period.

Asia-Pacific Aramid Fibers Industry Overview

The Asia-Pacific aramid fiber market is consolidated in nature. Some of the key players in the market (not in any particular order) include Huvis Corp, HYOSUNG JAPAN, Kolon Industries Inc., Teijin Aramid, and Yantai Tayho Advanced Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 The Increase in Demand for Light Weight Materials in Automotive Industry

- 4.1.2 The Rising Defense Expenditure of India and China

- 4.1.3 The Increase in Usage of Aramid Fibers as a Potential Substitute for Steel Materials

- 4.2 Restraints

- 4.2.1 The Availability of Better Alternatives For Aramid Fibers

- 4.2.2 Non-Biodegradable Nature of Aramid Fibers

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Para-aramid

- 5.1.2 Meta-aramid

- 5.2 End-user Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive

- 5.2.3 Electrical and Electronics

- 5.2.4 Sporting Goods

- 5.2.5 Other End-user Industries (Oil & Gas, Telecommunication, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 China National Bluestar (Group) Co. Ltd

- 6.4.2 Dupont

- 6.4.3 Hebei Silicon Valley Chemical Co. Ltd.

- 6.4.4 Huvis Corp

- 6.4.5 HYOSUNG JAPAN

- 6.4.6 KERMEL

- 6.4.7 Kolon Industries Inc.

- 6.4.8 Shanghai J&S New Materials Co.,ltd

- 6.4.9 Teijin Aramid

- 6.4.10 TORAY INDUSTRIES, INC.

- 6.4.11 X-FIPER New Material Co. Ltd.

- 6.4.12 Yantai Tayho Advanced Materials Co.,Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand from the Aerospace Sector

- 7.2 Advancements in Aramid Materials Manufacturing Technology

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日