|

市場調査レポート

商品コード

1851525

アラミド繊維:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Aramid Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アラミド繊維:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月02日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

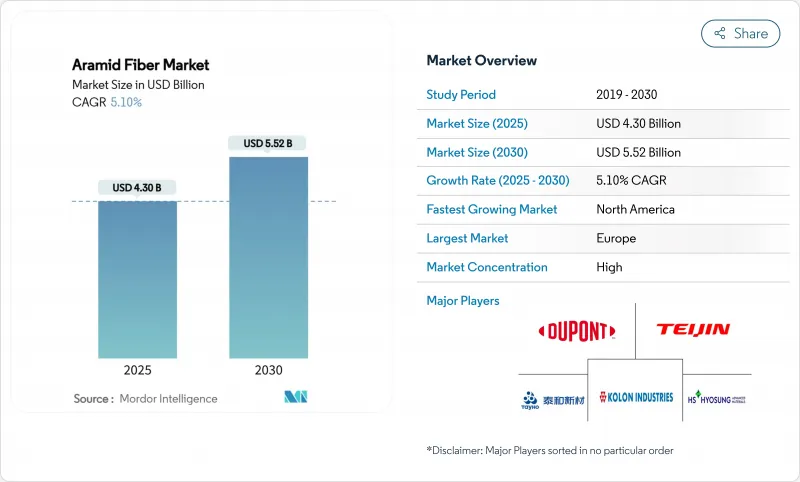

アラミド繊維市場規模は2025年に43億米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは5.10%で、2030年には55億2,000万米ドルに達すると予測されます。

自動車、航空宇宙、電気通信、高度な個人用保護具への普及が需要を高める一方、繊維の強度対重量比と熱安定性が長期的な関連性を支えています。電動モビリティにおける材料の軽量化目標、5Gネットワークの構築、極超音速および宇宙プログラムへの投資の増加は、継続的に商機を拡大します。同時に、主にMPDとPPDの原料価格変動が利幅を圧迫し、大手メーカーによる垂直統合の動きを促しています。知的財産の制約がさらに競合の力学を形成し、研究開発に資金を供給し、クロスライセンスの枠組みをうまく利用できる既存企業の地位を確固たるものにしています。

世界のアラミド繊維市場の動向と洞察

アジアの製造拠点で高まるPPE安全義務化

中国、インド、東南アジアの新興経済圏で産業安全規則の施行が進み、アラミド強化手袋、ヘルメット、耐熱作業着の注文が増加しています。アラミド複合材料で作られた産業用ヘルメットは、ABS製のものより耐衝撃性が37%高く、この性能差が工場での採用を加速させています。パラ系アラミドを使用した耐切創性手袋は、レベル5の保護性能を30%の軽量化で実現し、連続着用時の快適性を向上させています。メタ系アラミドを使用した難燃性作業着は、425℃でも構造的完全性を維持し、より厳しい鋳造や石油化学の安全基準に適合しています。このため、この地域に製品を供給するメーカーは、アラミド糸と生地の割り当てを増やし、アラミド繊維市場の成長プロファイルを強化しています。

アラミドで強化された軽量EVタイヤのEUグリーン・ディール推進

欧州の自動車メーカーが、電気自動車の航続距離を延ばすために車体質量を削減するタイヤ再設計プログラムを加速。アラミドで強化されたタイヤカーカスは、最大25%の軽量化を実現し、グリーンディールの輸送の脱炭素化目標に直結します。1kg削減するごとに0.7kmの航続距離延長が可能であるため、OEMはポリエステルやスチールコードの代わりにアラミドを使用するようになります。コンパウンドメーカーは、転がり抵抗を下げながらも耐久性を維持するアラミド入りゴムミックスを製品化しており、欧州や間もなく北米でもアラミド繊維市場の需要を強化しています。

MPDとPPDの原料価格の乱高下

原油価格の高騰と地域的な供給の混乱は、MPDとPPDのコストカーブを上昇させ、生産者のマージンを圧迫し、長期契約を不安に陥れます。米国商務省は、芳香族ジアミンを、地政学的に生産が集中する化学的に重要な原料のひとつに挙げており、供給安全保障上のリスクを高めています。メーカーは、バイオベースの中間体やアラミドスクラップのクローズドループ回収を模索することで対抗しているが、目先の変動が依然としてアラミド繊維市場の成長の勢いを削いでいます。

セグメント分析

2024年のアラミド繊維市場シェアはパラ系アラミドが65%を占め、防弾、航空宇宙、摩擦材の需要に支えられています。パラ系アラミド糸は3.8GPaに近い引張強度を持ち、防護服や航空ハニカムでの地位を維持しています。米国における国防予算の増額と、軽量自動車用複合材料への新たな関心により、パラ系アラミドはアラミド繊維市場において安定した数量パイプラインを確保しています。東レの韓国拠点における3,000トンの生産能力増強などの大規模な投資は、この繊維クラスへの資本配分の規模を裏付けています。

メタ系アラミドは、ベースは小さいもの、2030年までのCAGRが5.42%と最も速い軌道を描いています。先進的な湿式紡糸フィラメントは現在、引張強度が1,255MPaに達し、長時間の紫外線暴露後も90%以上の強度を維持するため、送電線カバーのような屋外用途の可能性が広がります。メタ系アラミドは、難燃性織物、絶縁紙、ろ過バッグに使用され、エレクトロニクス、産業安全、環境保護における熱安定性の要求に応えています。メタ系アラミド繊維市場規模は、アジア全域での半導体生産能力の拡大やEUのグリーン転換プロジェクトによって堅調に拡大すると予測され、価格だけでなく素材の特性が顧客の転換を決定するという競争力学が形成されています。

湿式紡糸は2024年にアラミド繊維市場シェアの60%を占め、CAGR 5.87%で引き続き主要市場を上回る。このプロセスは均質なポリマー凝固を提供し、電気紙や濾過媒体の必須条件である高い誘電安定性を達成する均一な密度の繊維を生産します。アップグレードされた溶剤リサイクル・モジュールは、排出量とコストを削減し、持続可能性を重視するエンドユーザーにも採用されています。湿式紡績品のアラミド繊維市場規模は、電化とフィルターメディア需要の伸びに伴って拡大すると予測されます。

ドライジェット湿式紡糸は、連鎖配向が極端な引張指標を駆動するパラ系アラミドには依然として不可欠です。ポリイミド類似体の実験では、最大2.72GPaの引張強度と114GPaを超える弾性率を示しており、将来のパラ系アラミド強化のための道筋が確認されています。全体的なシェアは小さいが、このプロセスはハイエンドのバリスティック糸供給を支えており、防衛省や高級スポーツ用品ブランドのニーズに合致しています。スループット効率と溶剤捕捉技術を目指した継続的なラインのアップグレードが、アラミド繊維市場へのニッチな貢献を守るであろう。

地域分析

2024年のアラミド繊維市場の35%は欧州が占める。厳格な労働者安全法、ISOに準拠した火炎規格、欧州連合のグリーン・ディールが、自動車や産業現場での高価値採用を後押ししています。輸出志向の自動車基盤を持つドイツがこの地域の数量拡大をリードし、フランスとオランダは高度ろ過と航空宇宙用ラミネートに特化しています。電気自動車用バッテリー工場に対する政府の優遇措置は、ポリマー複合材の採用をさらに刺激します。

北米は2025~2030年のCAGRが5.34%と最も速いです。連邦国防予算はパラ系アラミド弾道弾材料の継続的な需要につながる一方、NASAと民間打ち上げプロバイダーはメタ系アラミド熱シールドに投資を振り向ける。米国の通信事業者は、ハリケーンの影響を受けやすい回廊を横断する航空ファイバー・バックボーンを更新し、暴風雨による損傷を軽減するためにアラミド強度の部材を指定しています。カナダも、鉱業やエネルギー・インフラを中心に、公共安全に重点を置いた同様の動向を示しています。

アジア太平洋は、アラミド繊維市場の次のフロンティアとなります。中国は、輸入への依存を減らすために国内生産を拡大し、10年代半ばまでにパラアラミドの自給を目標としています。スマート工場、EVバッテリー工場、再生可能インフラストラクチャーの大量建設により、軽量で耐熱性の高い素材への需要が増大します。日本と韓国は半導体と5Gハードウェアのハイテク展開に磨きをかけ、アラミドが提供する誘電安定性と機械的弾力性を必要としています。インドのMake-in-India防衛プログラムと労働安全規範の更新は、地域のPPEと防具の消費を拡大し、地域の成長に厚みを加えます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アジアの製造拠点で高まるPPE安全義務化

- アラミドで強化された軽量EV用タイヤのEUグリーンディール推進

- アラミド強化光ファイバーケーブルの需要を高める5G展開の急増

- 各国による国防費の増加

- 極超音速と宇宙防衛への投資がメタアラミド遮熱シールドの消費を押し上げる

- 市場抑制要因

- MPDとPPD原料の価格変動

- パラアラミド新規参入を阻む特許クロスライセンスの壁

- 高い生産コスト

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 業界間の競争

第5章 市場規模と成長予測

- 製品タイプ別

- パラアラミド

- メタアラミド

- 紡績工程別

- 湿式紡績

- ドライジェット湿式紡糸

- 用途別

- セキュリティおよび保護装置

- 摩擦材・ブレーキ材

- 光ファイバーケーブル

- 航空宇宙部品

- 自動車用複合材料

- 電気絶縁

- その他(工業用ろ過、ゴム・タイヤ補強)

- エンドユーザー産業別

- 安全および保護装置

- 航空宇宙

- 自動車

- エレクトロニクスと通信

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Aramid Hpm, LLC.

- China National Bluestar(Group)Co. Ltd.

- DuPont

- HS HYOSUNG ADVANCED MATERIALS

- Huvis Corp.

- Kolon Industries, Inc.

- Sinochem Internation Corporation

- SINOPEC YIZHENG CHEMICAL FIBRE LIMITED

- SRO Aramid

- Suzhou Zhaoda Specially Fiber Technical Co.,Ltd.

- TAEKWANG INDUSTRIAL CO., LTD.

- Teijin Limited

- Toray Industries Inc.

- TOYOBO MC Corporation

- Wuxi City Shengte Carbon Fiber Products Co.,Ltd

- X-FIPER NEW MATERIAL CO.,LTD

- Yantai Tayho Advanced Materials Co.,Ltd.