北米のアラミド繊維:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Aramid Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640586

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

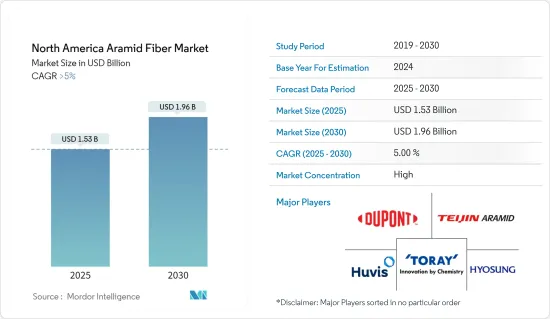

北米のアラミド繊維市場規模は、2025年に15億3,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは5%を超え、2030年には19億6,000万米ドルに達すると予測されています。

北米のアラミド繊維市場は、COVID-19パンデミックの悪影響を受けました。米国はCOVIDパンデミックの影響を最も大きく受けた地域です。COVIDパンデミックは米国、カナダ、メキシコで操業停止となり、自動車、電気・電子、航空宇宙、防衛の各エンドユーザー産業に影響を与え、アラミド繊維市場に影響を与えました。しかし、規制解除後、市場は順調に回復しました。自動車、電気・電子機器、航空宇宙・防衛産業におけるアラミド繊維消費の増加により、市場は大幅に回復しました。

主要ハイライト

- 短期的には、航空宇宙・防衛産業における軽量材料需要の増加、自動車産業における軽量材料需要の増加、鉄鋼材料の潜在的な代替材料としてのアラミド繊維の使用量の増加が市場を牽引するとみられます。

- アラミド繊維の非生分解性という性質と原料価格の上昇が市場成長の妨げとなっています。

- アラミド材料の製造技術の進歩は、予測期間中に市場に機会をもたらすと予想されます。

- 米国は、自動車、航空宇宙・防衛、電気・電子のエンドユーザー産業からのアラミド繊維需要の高まりにより、市場を独占すると予想されます。また、予測期間中に最も高いCAGRで推移する見込みです。

北米のアラミド繊維市場動向

航空宇宙・防衛エンドユーザー産業が市場を独占

- アラミドは、熱気球やグライダーから戦闘機、旅客機、スペースシャトルに至るまで、あらゆる航空機や宇宙船の部品や構造用途に使用されています。アラミド繊維は一般的に、主翼アセンブリ、ヘリコプターのローターブレード、座席プロペラ、計器や内部部品のエンクロージャーなどに使用されています。

- 航空宇宙産業では、民間航空機の全天候型運航や視覚システムの強化のため、各新世代航空機の製造にアラミド繊維を使用する割合が年々高まっています。さらに、温度安定性や耐久性といった特性は、今後数年間の航空宇宙用複合材料市場の成長をさらに後押しすると考えられます。

- 米国は、北米地域の航空機OEMにとって重要な市場のひとつです。AirbusとBoeingが同国最大の航空機メーカーです。例えば、Airbusは2023年に735機の民間航空機を納入し、2022年比で11%増加しました。1,835機のA320ファミリーと300機のA350ファミリーを含む2,319機のグロス受注(2,094機のネット受注)。同様に、BoeingもBoeing Max 8を57機受注しており、2025年までの納入が見込まれています。

- 運輸統計局のデータによると、2022年、米国の航空会社は8億5,300万人の旅客を運び、2021年の6億7,400万人と比べて30%の成長率を示しました。そのため、複数の航空会社が、増加する航空旅客需要に対応するため、保有機材を拡大し、先進的機能を備えた航空機を調達しています。

- メキシコは、北米航空宇宙産業における有力企業のひとつです。メキシコの航空宇宙製造業は現在、エンジン、貨物ドア、胴体、エンジン部品、着陸装置アセンブリ、接続システム、その他航空機の機能に不可欠な多くの部品に至るまで、あらゆるものを生産しています。

- メキシコでは航空機を利用する乗客が増加しています。そのため、同国では新型民間航空機の需要が増加しています。メキシコ航空宇宙産業連盟(FEMIA)によると、メキシコの航空宇宙産業部門は、2004年には100社であった製造会社や組織が、2022年半ばには368社に増加します。今日、これらの企業には主に民間航空機の製造業者や整備・修理・オーバーホール施設(MRO)が含まれます。

- したがって、航空宇宙・防衛産業の成長がこの地域のアラミド繊維市場を牽引すると予想されます。

市場を独占する米国

- 北米地域のアラミド繊維市場は米国が支配的です。米国は最も急速に台頭している経済国のひとつであり、今日では世界最大の生産国のひとつとなっています。同国の製造部門は同国経済に大きく貢献しています。

- 米国は、この地域のアラミド繊維の重要な市場のひとつです。アラミド繊維は、航空宇宙や防衛といった様々なエンドユーザー産業で使用されています。自動車、電気・電子機器、スポーツ用品などです。米国では、自動車と航空宇宙セクターが大きな市場成長を記録し、同国のアラミド繊維市場を牽引しています。

- 米国のエレクトロニクス市場は世界最大であり、調査対象市場の主要な潜在市場の一つとなっています。米国では、主にハイエンド製品の開発に注力するため、製造工場や開発センターの数が大幅に増加しています。

- 米国では、エレクトロニクス産業における技術の進歩や研究開発活動における技術革新のペースが速いため、より新しく高速なエレクトロニクス製品への需要が高まっています。消費者技術協会によると、米国の消費者向け電子機器/技術販売による小売売上高は、2021年の4,610億米ドルに対し、2022年には5,050億米ドルになると推定されています。売上の伸びは、同国の電子機器セグメントによるアラミド繊維の消費強化の推定値です。

- 米国の自動車産業は中国に次いで2番目に大きく、地域と世界の自動車市場に大きく貢献しています。同国には、南北アメリカ、欧州、アジア太平洋の他の経済圏に自動車を生産・輸出する大手自動車メーカーがあります。

- OICA(The Organisation Internationale des Constructeurs d'Automobiles)によると、同国の自動車生産台数は2021年の90億600万台に対し、2022年には1,006万台に達し、成長率は10%に達します。

- 全体として、自動車やエレクトロニクスなどの産業の成長が、予測期間中の同国のアラミド繊維市場を牽引すると考えられます。

北米のアラミド繊維産業概要

北米のアラミド繊維市場は統合された性質を持っています。同市場の主要企業(順不同)には、Dupont、Huvis Corp、HYOSUNG、Teijin Aramid、TORAY INDUSTRIES, INC.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 航空宇宙・防衛産業における軽量材料の需要増加

- 自動車産業における軽量材料の需要増加

- 鉄鋼材料の代替となりうるアラミド繊維の使用増加

- 抑制要因

- アラミド繊維の非生分解性

- 原料価格の上昇

- 産業のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ

- パラ系アラミド

- メタ系アラミド

- エンドユーザー産業

- 航空宇宙・防衛

- 自動車

- 電気・電子

- スポーツ用品

- その他のエンドユーザー産業(石油・ガス、通信など)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Aramid Hpm, LLC.

- Bally Ribbon Mills

- Dupont

- Huvis Corp

- HYOSUNG

- KERMEL

- Shenma Industrial Co. Ltd.

- Teijin Aramid

- TORAY INDUSTRIES, INC.

- Yantai Tayho Advanced Materials Co.,Ltd.

第7章 市場機会と今後の動向

- アラミド材料製造技術の進歩

- その他の機会

目次

The North America Aramid Fiber Market size is estimated at USD 1.53 billion in 2025, and is expected to reach USD 1.96 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The North America Aramid Fibers Market had been negatively affected by the COVID-19 pandemic. The United States was worst hit by the COVID pandemic in the region. The COVID pandemic resulted in lockdowns in the United States, Canada, and Mexico, affecting the automotive, electrical and electronics, aerospace, and defense end-user industries, thereby affecting the market for aramid fibers. However, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of aramid fibers in automotive, electrical, and electronics end-user industries.

Key Highlights

- Over the short term, the increasing demand for lightweight materials in aerospace and defense industries, the increase in demand for lightweight materials in the automotive industry, and the rising usage of aramid fibers as a potential substitute for steel materials are excepted to drive the market.

- The non-biodegradable nature of aramid fibers and the increasing prices of raw materials are hindering market growth.

- The advancements in aramid materials manufacturing technology are expected to create opportunities for the market during the forecast period.

- The United States is expected to dominate the market due to the rising demand for aramid fibers from automotive, aerospace and defense, electrical, and electronics end-user industries. It is also expected to register the highest CAGR during the forecast period.

North America Aramid Fiber Market Trends

Aerospace and Defense End-User Industry to Dominated the Market

- Aramids are used for components and structural applications in all aircraft and spacecraft, ranging from hot air balloons and gliders to fighter planes, passenger airliners, and space shuttles. The aramid fibers are generally used in wing assemblies, helicopter rotor blades, seat propellers, and enclosures for instruments and internal parts.

- Every year, the aerospace industry uses a higher proportion of aramid fibers in constructing each new generation of aircraft due to the provision of an all-weather operation of commercial aircraft and enhanced vision systems. Moreover, characteristics such as temperature stability and durability will further fuel the growth of the aerospace composites market over the coming years.

- The United States is one of the significant markets for OEMs of airplanes in the North American region. Airbus and Boeing are the largest manufacturers of airplanes in the country. For instance, Airbus delivered 735 commercial aircraft in 2023, an 11% increase on 2022. 2,319 gross orders (2,094 net), including 1,835 A320 Family and 300 A350 Family aircraft. Similarly, Boeing Aeroplane OEM company received orders for 57 Boeing Max 8 jets, with delivery expected through 2025.

- According to data from the Bureau of Transportation Statistics, in 2022, airlines in the United States carried 853 million passengers at a growth rate of 30% compared to 674 million passengers in 2021. Thus, several airline companies are expanding their fleet and procuring aircraft with advanced capabilities to cater to the increasing air passenger demand.

- Mexico is one of the prominent players in the North American Aerospace Industry. Aerospace manufacturing in Mexico now produces everything from engines, cargo doors, fuselages, engine parts, landing gear assemblies, connection systems, and many other components essential for an aircraft to function.

- The number of passengers traveling by airplane is increasing in Mexico. Thus, the demand for new civil aircraft is increasing in the country. According to Mexican Aerospace Industry Federation, A.C. (FEMIA), Mexico's aerospace sector grew from 100 manufacturing firms and organizations in 2004 to 368 by mid-2022. Today these firms primarily include manufacturers and maintenance-repair-overhaul facilities (MROs) for civil aircraft.

- Thus, the aerospace and defense industry growth is expected to drive the region's aramid fibers market.

United States to Dominate the Market

- The United States dominated the aramid fiber market in the North American region. The United States is one of the fastest emerging economies and has become one of the biggest production houses in the world today. The country's manufacturing sector is one of the significant contributors to the country's economy.

- The United States is one of the region's significant markets for Aramid Fibers. These are sued in various end-user industries such as aerospace and defense: Automotive, electric and electronics, and sporting goods. In the United States, the automotive and aerospace sectors registered significant market growth, thereby driving the market for aramid fibers in the country.

- The United States electronics market is the largest in the world, acting as one of the leading potential zones for the market studied. There is a significant increase in the number of manufacturing plants and development centers in the United States, primarily due to the focus on developing high-end products.

- In the United States, the rapid pace of innovation in terms of the advancement of technologies and R&D activities in the electronics industry is driving the demand for newer and faster electronic products. According to the Consumer Technology Association, the retail revenue from consumer electronics/technology sales in the United States was estimated at USD 505 billion in 2022, compared to USD 461 billion in 2021. the growth in sales is an estimation of enhanced consumption of aramid fibers from the electronics segment of the country.

- The automobile industry in the United States is the second-largest after China, contributing significantly to the regional and global automobile markets. The country houses major automakers producing and exporting vehicles to other economies in the Americas, Europe, and the Asia Pacific.

- According to OICA (The Organisation Internationale des Constructeurs d'Automobiles), vehicle production in the country reached a total of 10.06 million units in 2022, compared to 9006 million units manufactured in 2021, at a growth rate of 10%.

- Overall, the growth of industries such as automotive and electronics will likely drive the market for aramid fibers in the country during the forecast period.

North America Aramid Fiber Industry Overview

The North America aramid fiber market is consolidated in nature. Some of the key players in the market (not in any particular order) include Dupont, Huvis Corp, HYOSUNG, Teijin Aramid, and TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Light Weight Materials in Aerospace and Defense Industries

- 4.1.2 The Increase in Demand for Light Weight Materials in Automotive Industry

- 4.1.3 The Rising Usage of Aramid Fibers as a Potential Substitute for Steel Materials

- 4.2 Restraints

- 4.2.1 Non-Biodegradable Nature of Aramid Fibers

- 4.2.2 The Increasing Prices of Rawmaterials

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Para-aramid

- 5.1.2 Meta-aramid

- 5.2 End-user Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive

- 5.2.3 Electrical and Electronics

- 5.2.4 Sporting Goods

- 5.2.5 Other End-user Industries (Oil & Gas, Telecommunication, etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aramid Hpm, LLC.

- 6.4.2 Bally Ribbon Mills

- 6.4.3 Dupont

- 6.4.4 Huvis Corp

- 6.4.5 HYOSUNG

- 6.4.6 KERMEL

- 6.4.7 Shenma Industrial Co. Ltd.

- 6.4.8 Teijin Aramid

- 6.4.9 TORAY INDUSTRIES, INC.

- 6.4.10 Yantai Tayho Advanced Materials Co.,Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Aramid Materials Manufacturing Technology

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日