|

市場調査レポート

商品コード

1683499

中国のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 279 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

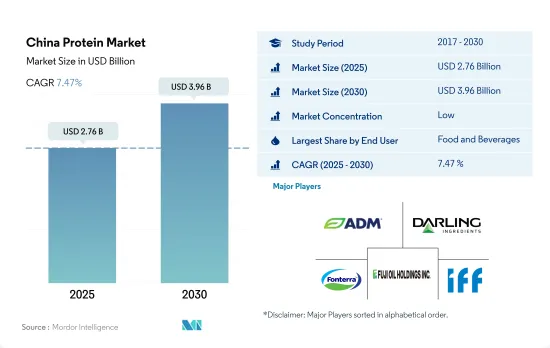

中国のたんぱく質市場規模は2025年に27億6,000万米ドルと推計され、2030年には39億6,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは7.47%で成長する見込みです。

たんぱく質の機能性に対する需要の高まりと、たんぱく質が豊富な食事に対する意識が、国内における飲食品セグメントの市場シェア拡大につながっています。

- 飲食品セグメントにおけるたんぱく質の需要は、主にたんぱく質の機能性に対する需要の増加やたんぱく質が豊富な食生活に対する意識などの要因によって牽引されています。飲食品部門では、2022年には肉/鶏肉/シーフードおよび肉代替製品部門が36.5%の主要数量シェアを占め、乳製品および乳製品代替製品部門が17.9%でこれに続きます。同セグメントは予測期間中、CAGR 6.83%と予測され、金額成長率で他の用途を上回りそうです。

- 動物飼料セグメントは市場で第2位のシェアを占めています。このセグメントは予測期間中、名目CAGR 8.56%(金額ベース)で市場を牽引すると予測されています。大豆粕は、動物用飼料、特に単胃動物用の飼料に使用される一般的なたんぱく質源の中で最も高いリジン消化率(91%)を持つため、植物性たんぱく質は動物用飼料産業で主に使用されています。高品質の大豆を給餌された家畜はより健康で、人間が消費するタンパク源としても豊富です。

- たんぱく質市場ではサプリメントが大きなシェアを占めており、スポーツ栄養のサブセグメントが市場を大きく支配しています。予測期間中のCAGRは金額ベースで3.09%と予測されています。中国の国家栄養計画(2017-2030)および健康中国2030構想の継続的な実行は、スポーツフィットネスの推進に役立ち、それによってたんぱく質市場に高い需要を引き出すと予想されます。これを受けて、中国ではスポーツに参加したりジムに通ったりする若年層が増えている一方、高齢者はスクエアダンスのような身体活動を取り入れています。

中国のたんぱく質市場動向

動物性たんぱく質の消費拡大が原料部門の主要企業にチャンスをもたらす

- グラフは、中国における一人当たりの動物性たんぱく質消費量を示しています。以前は、牛乳や乳製品(乳たんぱく質を含む)は子供や高齢者向けの食品と考えられていたため、中国全土の成人は主に牛乳や乳製品を無視していました。しかし、この動向は近年変わってきています。14億人近い人口を抱える中国は、今や世界第2位の乳製品消費国となりました。中国は、ニュージーランドを拠点とする酪農家からドイツの酪農家まで、さまざまな国から製品を輸入しています。中国の動物性たんぱく質市場は、健康志向の高い人々の高品質なたんぱく質原料に対する大きな需要を目の当たりにしてきました。一人当たりの消費量は2016年の40グラムから2021年には45.1グラムに増加します。

- 中国では有機乳たんぱく質が最も広く消費されています。オーガニック分野はダイナミックな需要を目の当たりにしており、約57%の母親がオーガニック製品を検討しています。Arla Foodsは、2021年にNutrilacシリーズの機能性たんぱく質原料を使用した2つの革新的な「オーガニック子供用スナック」コンセプトを発表しました。フォンテラ社は、非常にソフトで咀嚼時間が比較的短いミルクたんぱく質バーSureProteinTM SoftBar 1000を発売しました。

- 中国市場では、食品用途でのコラーゲンたんぱく質の需要が急速に伸びています。この製品は欧米諸国ではすでに定着し、販売されています。中国での需要は、美容志向の栄養製品が与える影響に対する意識の高まりに後押しされています。この動向は中国では「口腔美容」または「美食」として知られています。中国はアジア太平洋で最大のホエイたんぱく質市場です。ホエイたんぱく質は様々な体重管理や美容製品の製造に広く使用されているため、中国のパーソナルケア市場はホエイたんぱく質需要の増加を目の当たりにしました。

中国の国内食肉生産は、アフリカ豚熱の発生により増加した

- 牛、鶏、豚の骨付き肉、牛や山羊の生乳、牛のスキムミルク、乾燥ホエイパウダーが動物性たんぱく質の生産量を構成しており、グラフにも同じデータが示されています。中国人の食事指導では、1日300gの乳製品摂取を推奨しています。米国は301条関税撤廃の実施後、脱脂粉乳、チーズ、ホエイパウダーを輸出しています。中国政府はチーズ、乳清、バターなどの乳製品加工品を良質なタンパク源として奨励しています。

- 2020年、中国の生乳生産量はCOVID-19の大流行により緩やかな伸びを示しました。これは主に輸送制限と乳製品加工活動の減少によるものです。生産量の減少は主に小規模農場で見られました。大規模農場は大手乳業メーカーとの契約酪農のため影響は少なく、流動乳を含むほとんどの乳製品の生産量は2020年に5%~11%減少しました。USDAによれば、中国の流動乳の輸入量は2021年には98万MTに増加します。中国への流動乳の主要供給国は欧州連合で、ニュージーランドがこれに続きます。

- 中国の国内牛肉生産は、アフリカ豚熱の発生により増加しました。牛肉は中国では、サラダや加工された調理済みミールパックに入ったヘルシーなたんぱく質の選択肢として宣伝されました。2022年12月、中国の全国農業農村事務会議は、同国の5ヵ年計画における豚肉の年間生産目標を、現在の生産量を約35%上回る5,500万トンとすることを決定しました。全国の牛と豚は大規模な繁殖と生産を目的としているため、コラーゲン生産に十分な原料を提供しています。

中国たんぱく質産業の概要

中国たんぱく質市場は断片化されており、上位5社で16.36%を占めています。この市場の主要企業は以下の通りです。Archer Daniels Midland Company, Darling Ingredients Inc., Fonterra Co-operative Group Limited, FUJI OIL HOLDINGS INC. and International Flavors & Fragrances, Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 植物

- 生産動向

- 動物

- 植物

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 原料

- 動物

- たんぱく質タイプ別

- カゼインおよびカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫たんぱく質

- ミルクたんぱく質

- ホエイたんぱく質

- その他の動物性たんぱく質

- 微生物

- たんぱく質タイプ別

- 藻類たんぱく質

- マイコたんぱく質

- 植物

- たんぱく質タイプ別

- ヘンプ・たんぱく質

- エンドウ豆たんぱく質

- ジャガイモ・たんぱく質

- 米たんぱく質

- 大豆たんぱく質

- 小麦たんぱく質

- その他の植物性たんぱく質

- 動物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Archer Daniels Midland Company

- Darling Ingredients Inc.

- Fonterra Co-operative Group Limited

- Foodchem International Corporation

- FUJI OIL HOLDINGS INC.

- Gansu Hua'an Biotechnology Group

- International Flavors & Fragrances, Inc.

- Linxia Huaan Biological Products Co. Ltd

- Luohe Wulong Gelatin Co. Ltd

- Shandong Jianyuan Bioengineering Co. Ltd

- Shandong Yuwang Industrial Co. Ltd

- Wilmar International Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The China Protein Market size is estimated at 2.76 billion USD in 2025, and is expected to reach 3.96 billion USD by 2030, growing at a CAGR of 7.47% during the forecast period (2025-2030).

The increasing demand for protein functionalities and awareness about protein-rich diets, has led to an increased market share of food and beverage segment in the country

- The demand for proteins in the food and beverage segment is primarily driven by factors such as increasing demand for protein functionalities and awareness about protein-rich diets. In the food and beverage category, the meat/poultry/seafood and meat alternative products segment accounted for the major volume share of 36.5% in 2022, followed by the dairy and dairy alternative products segment with 17.9%. The segment is likely to outpace other applications in terms of value growth rate, with a projected CAGR of 6.83%, during the forecast period.

- The animal feed segment occupied the second-largest share of the market. The segment is anticipated to drive the market with a nominal CAGR of 8.56%, by value, during the forecast period. Plant proteins are majorly occupied in the animal feed industry as soybean meal has the highest lysine digestibility (91%) of any of the commonly available protein sources used in animal feed formulations, particularly for monogastric species. Livestock fed with high-quality soy is healthier and a richer source of protein for human consumption.

- The supplements hold a significant share of the protein market, and the sports nutrition sub-segment majorly dominates the market. It is projected to register a CAGR of 3.09%, by value, during the forecast period. The ongoing execution of China's National Nutrition Plan (2017-2030) and the Healthy China 2030 initiative is expected to help propel sports fitness and thereby draw high demand for the protein market. In response, a growing number of younger people in China are participating in sports and going to the gym, while older people are embracing physical activities like square dancing.

China Protein Market Trends

Animal protein's consumption growth fuels opportunities for key players in the ingredients segment

- The graph given depicts the per capita consumption of animal protein in China. In the past, adults across China mainly ignored milk and dairy products (including milk protein) because they were seen as food for children or the elderly. However, this trend has changed in recent years. The nation of nearly 1,400 million people is now the second-largest consumer of dairy products in the world. China imports products from various other countries, ranging from New Zealand-based dairies to German industries. The Chinese animal protein market has witnessed a huge demand for high-quality protein ingredients from health-conscious people. The per capita consumption increased from 40 grams in 2016 to 45.1 grams in 2021.

- Organic milk protein is most widely consumed in China. The organic segment witnesses a dynamic demand, with around 57% of mothers considering organic products. Arla Foods introduced two innovative 'organic kiddies snack' concepts by using its Nutrilac range of functional protein ingredients in 2021. Fonterra launched SureProteinTM SoftBar 1000, a milk protein bar that is exceptionally soft and has a relatively short chew time.

- The Chinese market is witnessing rapid growth in the demand for collagen protein in food applications. This product is already well-established and marketed in Western countries. Its demand in China is being fueled by the rising awareness of the impact of beauty-oriented nutritional products. This trend is known as "oral beauty" or "beautiful eating" in China. China is the largest market for whey protein in Asia-Pacific. The Chinese personal care market witnessed an increase in the demand for whey protein as it is widely used in the production of various weight management and beauty products.

China's domestic meat production increased due to the outbreak of African Swine Fever

- Meat from cattle, chicken, and pig with bone, raw milk from cattle and goats, skim milk of cows, and dry whey powder make up the production of animal protein, and the same data is given in the graph. The Dietary Guidance for Chinese Residents recommends a daily intake of 300 grams of dairy products. The US exports skimmed milk powder, cheese, and whey powder following the implementation of the Section 301 tariff exclusion. The Chinese government promotes processed dairy products, including cheese, whey, and butter, as good sources of protein.

- In 2020, milk production in China witnessed moderate growth due to the COVID-19 pandemic. This was mainly due to transport restrictions and reduced dairy processing activities. The fall in production was mainly observed in small farms. Large farms were less affected due to contract farming with major dairy manufacturers. The production of most dairy products, including fluid milk, dropped by 5%-11% in 2020. China's import of fluid milk increased to 980,000 MT in 2021, as per the USDA. The European Union is the major supplier of fluid milk to China, followed by New Zealand.

- China's domestic beef production increased due to the outbreak of African Swine Fever. Beef was promoted in China as a healthy protein option in salads or processed ready-to-eat meal packs. In December 2022, China's National Conference of Agricultural and Rural Affairs decided to set an annual pork production target of 55 million metric tons for the country's five-year plan, which is approximately 35% above the current production rate. Cattle and pigs across the country account for large-scale breeding and production purposes, thereby providing sufficient raw material for collagen production.

China Protein Industry Overview

The China Protein Market is fragmented, with the top five companies occupying 16.36%. The major players in this market are Archer Daniels Midland Company, Darling Ingredients Inc., Fonterra Co-operative Group Limited, FUJI OIL HOLDINGS INC. and International Flavors & Fragrances, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 China

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Darling Ingredients Inc.

- 5.4.3 Fonterra Co-operative Group Limited

- 5.4.4 Foodchem International Corporation

- 5.4.5 FUJI OIL HOLDINGS INC.

- 5.4.6 Gansu Hua'an Biotechnology Group

- 5.4.7 International Flavors & Fragrances, Inc.

- 5.4.8 Linxia Huaan Biological Products Co. Ltd

- 5.4.9 Luohe Wulong Gelatin Co. Ltd

- 5.4.10 Shandong Jianyuan Bioengineering Co. Ltd

- 5.4.11 Shandong Yuwang Industrial Co. Ltd

- 5.4.12 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms