アジア太平洋地域のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Asia-Pacific Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 334 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690992

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

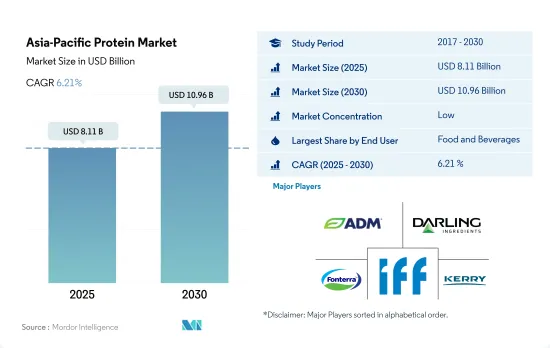

アジア太平洋地域のたんぱく質市場規模は2025年に81億1,000万米ドルと推定され、2030年には109億6,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは6.21%で成長すると予測されます。

菜食主義が台頭する中、動物性不使用製品に対する需要の高まりが飲食品セグメントを牽引し、市場シェアは最大となりました。

- 飲食品は同地域で最大のたんぱく質消費セグメントであり続けた。中でも、ベーカリー、乳製品、代替肉は主要な用途分野であり、2023年に同地域で消費されるたんぱく質の39%の数量シェアを占めました。菜食主義が台頭する中、動物性食品を使用しない製品に対する需要の高まりが、乳製品や食肉代替品用途における植物、特に大豆たんぱく質の統合を引き寄せた。

- このセグメントには、費用対効果と栄養価の高さから植物性たんぱく質に依存している動物飼料セグメントが続いています。アジア太平洋は主要な畜産地域の一つであり、特にインドや中国のような国では、品質重視の動物飼料に対する需要が伸びており、この地域のたんぱく質市場にさらに利益をもたらしています。例えば、現在の牛群数は3億742万頭で、2023年の3億740万頭からわずかに増加しています。大豆たんぱく質は消化性が高く、家畜の飼料に適しているため、小売業者の間で家禽、家畜、水産養殖用の高品質飼料原料として台頭してきています。この大きなシェアにより、大豆たんぱく質の用途は2024年から2029年の間に数量ベースで6.23%のCAGRで推移するとみられています。

- たんぱく質市場ではサプリメントが大きなシェアを占めています。スポーツ栄養サブセグメントが主に市場を独占しており、2024~2029年の間に金額ベースで4.58%のCAGRで推移すると予測されています。たんぱく質市場の成長を支える重要な要素の一つは、スポーツクラブやトレーニング施設の増加とともに、フィットネスやスポーツ文化の人気が拡大していることです。インドでは、2021年に54%の人が頻繁に運動し、30%の人が最先端のアプリケーションやガジェットを利用してフィットネス・ルーティンをアップグレードしました。

たんぱく質の機能性に対する需要の高まりとたんぱく質豊富な食事に対する意識の高まりにより、中国がアジア太平洋のたんぱく質市場をリード

- 国別では、2023年に中国が市場をリードし、主に飲食品分野が牽引しました。たんぱく質の機能性に対する需要の増加とたんぱく質の豊富な食事に対する意識の高まりが、主に飲食品セグメントにおけるたんぱく質需要を牽引しています。中国では、企業は革新的なたんぱく質ベースの製品を小売分野で展開するために多額の投資を行っています。例えば、Cargill、Hoafood、Eat Justは、2019-2023年に中国での植物ベースの事業を拡大しました。中国はまた、この地域で最も速い成長を記録すると予想され、2024~2029年の数量ベースのCAGRは7.09%です。

- 中国に僅差で続いたのはインドで、新興の若年人口と高たんぱく質食への需要が牽引しています。インド・たんぱく質・スコア(IPS)のような取り組みが、消費者のたんぱく質に関する意識をさらに高めています。大豆、エンドウ豆、玄米など、様々な形態の植物性たんぱく質パウダーやサプリメントの台頭が、この需要に寄与しています。大豆、小麦、エンドウ豆の豊富な入手可能性、機能性、菜食主義者向けのタンパク源、低価格が、植物性たんぱく質分野でインドが主導的地位を占める一因となっています。したがって、インドのたんぱく質市場は2019年から2023年にかけて金額ベースで10.19%の成長率を観測しました。

- インドネシアでは、健康、持続可能性、動物福祉に対する消費者の意識の高まりに促され、植物ベースのファーストフードが人気を集めており、国内の多くのフードチェーンがビーガンの動向を採用しています。スターバックス、イケア、バーガーキングなどの企業がビーガン食品を発売しており、インドネシアにおける植物性たんぱく質の需要を押し上げています。したがって、インドネシアの植物性たんぱく質分野は、2024年から2029年にかけて数量ベースで3.29%のCAGRで推移すると予測されます。

アジア太平洋地域のたんぱく質市場動向

動物性たんぱく質消費において、乳清たんぱく質と乳たんぱく質のシェアが高まる見込み

- 日本はアジア市場におけるホエイたんぱく質の主要市場となっています。2020年のオリンピック東京大会やラグビーワールドカップのような、この地域で開催されたスポーツイベントのために、消費者はホエイ製品を選んでいます。日本では、スポーツイベントと高齢者人口の増加が、それぞれスポーツ栄養と高齢者栄養における主なたんぱく質補助食品として血清の消費を促進しています。日本の軍人の間でたんぱく質の利点に対する意識が高まっていることも、ホエイたんぱく質の消費を後押ししています。インドは世界で最も急速に成長している国の一つです。

- 現在、中国の動物性たんぱく質市場は着実な開拓を見せています。中国の生活水準が向上し、食品と医薬品に対する消費者の安全要求も改善されてきました。中国は、過去2年間のアフリカ豚熱による赤字と、過去2年間の動物性たんぱく質の輸入増加により、豚の頭数が40%近く減少しています。

- ホエイタンパク濃縮物は、効率的で消化しやすい加工や安価な用途など、多様な利点を提供し、インドの市場成長に貢献しています。ホエイたんぱく質濃縮物は、スポーツ栄養カテゴリーにおいて幅広い用途があります。インドの若者の間でスポーツ栄養の消費が増加しているため、濃縮乳清たんぱく質の需要も増加しています。同国における一人当たりのホエイタンパク消費量は、2017年の14gから2022年には17.2gに増加しました。

動物性たんぱく質原料メーカーの原料として牛乳と食肉生産が大きく貢献

- この地域の主要な生乳生産国はインドで、次いで中国です。2021年、インドの牛乳生産量は約9,600万トン、中国は約3,500万トンです。濃厚動物飼料施設(CAFO)や酪農生産工場のための工場農場がアジア全域で設立されており、その多くは何千頭もの牛を収容しています。過去10年間で生乳生産量が最も増加したのは東南アジアです。

- COVID-19の混乱で中国の生乳生産と消費が急成長したため、生産性が向上し、この地域の生乳生産量は2021年に7.06%増加しました。輸入も、消費者の需要と中国の製造業への要求により、プラス成長を見せています。乳たんぱく質生産に主に使用される脱脂粉乳は、中国の食品産業が輸入脱脂粉乳に依存しているため増加しています。

- 牛、豚、鶏の動物性たんぱく質は、コラーゲンとゼラチンの生産に使用されます。生産はインドや中国のような国々で大幅に改善されつつあり、政府のイニシアティブと各国での新しい近代的なと畜場の建設によって支えられています。2020年には、アフリカ豚熱が中国の養豚産業に影響を与え続けたため、豚の生産量全体が減少しました。

アジア太平洋地域のたんぱく質産業の概要

アジア太平洋のたんぱく質市場は断片化されており、上位5社で13.91%を占めています。この市場の主要企業は以下の通りです。 Archer Daniels Midland Company, Darling Ingredients Inc., Fonterra Co-operative Group Limited, International Flavors & Fragrances, Inc. and Kerry Group plc(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 植物

- 生産動向

- 動物

- 植物

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 原料

- 動物

- たんぱく質タイプ別

- カゼインとカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫たんぱく質

- ミルクたんぱく質

- ホエイたんぱく質

- その他の動物性たんぱく質

- 微生物

- たんぱく質タイプ別

- 藻類たんぱく質

- マイコたんぱく質

- 植物

- たんぱく質タイプ別

- ヘンプたんぱく質

- エンドウ豆たんぱく質

- ポテトたんぱく質

- 米たんぱく質

- 大豆たんぱく質

- 小麦たんぱく質

- その他の植物性たんぱく質

- 動物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- 韓国

- タイ

- ベトナム

- その他アジア太平洋地域

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Archer Daniels Midland Company

- Corbion Biotech, Inc.

- Darling Ingredients Inc.

- Fonterra Co-operative Group Limited

- Fuji Oil Group

- Glanbia PLC

- Hilmar Cheese Company, Inc.

- International Flavors & Fragrances, Inc.

- Kerry Group plc

- Lacto Japan Co. Ltd.

- Nagata Group Holdings Ltd

- Nitta Gelatin Inc.

- Nutrition Technologies Group

- Tereos SCA

- Wilmar International Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Asia-Pacific Protein Market size is estimated at 8.11 billion USD in 2025, and is expected to reach 10.96 billion USD by 2030, growing at a CAGR of 6.21% during the forecast period (2025-2030).

Growing demand for animal-free products amid rising veganism is driving the food and beverage segment, resulting in the largest market share

- Food and beverage remained the largest protein-consuming segment in the region. Among others, bakery, dairy, and meat alternatives remained the major application areas, capturing a 39% volume share of the protein consumed in the region in 2023. Growing demand for animal-free products amid rising veganism attracted greater integration of plants, especially soy proteins, in dairy and meat imitation applications.

- The segment was followed by the animal feed segment, which relies on plant proteins for their cost-effective and nutritional attributes. Asia-Pacific is one of the major cattle-producing regions, especially countries like India and China, where the demand for quality-centric animal feed is growing, further benefitting the protein market in the region. For instance, currently, the number of cattle herds is 307.42 million heads, marginally up from 307.4 million heads in 2023. Soy protein is emerging as a high-quality feed ingredient for poultry, livestock, and aquaculture among retailers as it is highly digestible, making a good diet for cattle. Due to the significant share, the application of soy protein is set to record a major CAGR of 6.23% by volume during 2024-2029.

- Supplements hold a significant share in the protein market. The sports nutrition sub-segment mainly dominated the market, and it is projected to register a CAGR of 4.58% by value during 2024-2029. One of the key elements supporting the growth of the protein market is the expanding popularity of fitness and sports culture, along with the rising number of sports clubs and training facilities. In India, 54% of people frequently exercised in 2021, and 30% upgraded their fitness routines by utilizing cutting-edge applications and gadgets.

China leads the Asia-Pacific protein market due to the increasing demand for protein functionalities and rising awareness about protein-rich diets

- By country, China led the market in 2023, majorly driven by the food and beverage segment. The increasing demand for protein functionalities and awareness about protein-rich diets primarily drive protein demand in the food and beverage segment. In China, companies are making significant investments in rolling out innovative protein-based products in the retail space. For instance, Cargill, Hoafood, and Eat Just expanded their plant-based operations in China during 2019-2023. China is also anticipated to register the fastest growth in the region, with a CAGR of 7.09% by volume during 2024-2029.

- China was closely followed by India, driven by the emerging young population and their demand for high-protein meals. Initiatives such as India Protein Score (IPS) are further boosting protein-related awareness among consumers. The rise of various forms of plant-based protein powders and supplements, like soy, pea, and brown rice, contributes to this demand. The immense availability, functionality, vegan protein source, and low price of soy, wheat, and peas have contributed to the country's leading position in the plant protein segment. Hence, the Indian protein market observed a growth rate of 10.19% by value from 2019 to 2023.

- In Indonesia, plant-based fast food is gaining popularity, prompted by greater consumer awareness of health, sustainability, and animal welfare, with many food chains across the country adopting the vegan trend. Companies such as Starbucks, Ikea, and Burger King are launching vegan foods, thus boosting the demand for plant-based proteins in Indonesia. Hence, the plant protein segment in Indonesia is projected to register a CAGR of 3.29% by volume during 2024-2029.

Asia-Pacific Protein Market Trends

The share of whey and milk protein is expected to increase in animal protein consumption

- Consumers are opting for whey products due to sporting events that took place in the region, like the Olympic Tokyo Games in 2020 and the Rugby World Cup. The sports events and the growing older population in Japan are driving serum consumption as the main protein supplement in sports nutrition and elderly nutrition, respectively. The increasing awareness about the benefits of proteins among the Japanese military is also boosting the consumption of whey proteins. India is one of the fastest-growing countries in the world.

- Currently, the animal protein market in China is witnessing a steady development. With improved living standards in China, consumer safety requirements for food and drugs have improved. China has seen a decline in its pig herd of almost 40% due to the deficit created by African Swine Fever in the last two years and an increase in the importation of animal proteins during the past two years.

- Whey protein concentrates offer versatile benefits, including efficient and easy-to-digest processing and inexpensive applications, which are contributing to India's market growth. They have a wide range of applications in the sports nutrition category. Owing to the increased consumption of sports nutrition among young Indians, the demand for whey protein concentrate also increased. The per capita consumption of whey protein in the country increased to 17.2g in 2022 from 14g in 2017.

Milk and meat production majorly contributes as raw material for animal protein ingredient manufacturers

- India is the major milk-producing country in the region, followed by China. In 2021, India produced nearly 96 million tons of cow milk, while China produced around 35 million tons. Concentrated animal feeding operations (CAFOs) or factory farms for dairy production plants are being set up across Asia, many housing thousands of cows, by global and new national dairy corporations often working in partnership with governments. The strongest gains in milk production over the past decade have been registered in Southeast Asia.

- China's milk production in the region increased by 7.06% in 2021 due to improved productivity, as the COVID-19 disruption caused China's production and consumption of milk to grow rapidly. Imports are also showing positive growth due to consumer demand and requirements for the manufacturing industries in China. Skim milk powder, which is majorly used for milk protein production, has increased due to the Chinese food industry's dependence on imported skim milk powder.

- Animal protein from cattle, pigs, and chickens is used for collagen and gelatin production. Production is improving significantly in countries like India and China, and it is supported by government initiatives and the construction of new, modern slaughterhouses across the countries. Overall pig production declined in 2020 as African Swine Fever continued to impact China's hog industry.

Asia-Pacific Protein Industry Overview

The Asia-Pacific Protein Market is fragmented, with the top five companies occupying 13.91%. The major players in this market are Archer Daniels Midland Company, Darling Ingredients Inc., Fonterra Co-operative Group Limited, International Flavors & Fragrances, Inc. and Kerry Group plc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 China

- 3.4.3 India

- 3.4.4 Japan

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 New Zealand

- 4.3.8 South Korea

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.3.11 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Corbion Biotech, Inc.

- 5.4.3 Darling Ingredients Inc.

- 5.4.4 Fonterra Co-operative Group Limited

- 5.4.5 Fuji Oil Group

- 5.4.6 Glanbia PLC

- 5.4.7 Hilmar Cheese Company, Inc.

- 5.4.8 International Flavors & Fragrances, Inc.

- 5.4.9 Kerry Group plc

- 5.4.10 Lacto Japan Co. Ltd.

- 5.4.11 Nagata Group Holdings Ltd

- 5.4.12 Nitta Gelatin Inc.

- 5.4.13 Nutrition Technologies Group

- 5.4.14 Tereos SCA

- 5.4.15 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 334 Pages

- 納期

- 2~3営業日