|

市場調査レポート

商品コード

1683503

中東のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Middle East Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 286 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

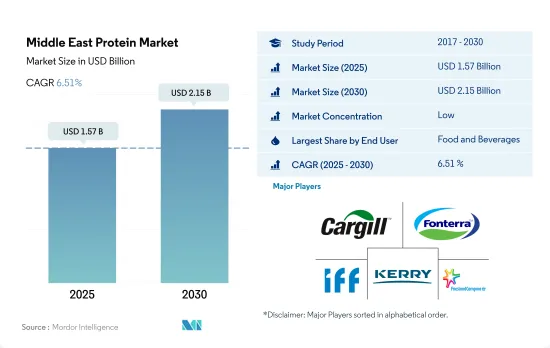

中東のたんぱく質市場規模は2025年に15億7,000万米ドルと推定・予測され、2030年には21億5,000万米ドルに達し、予測期間(2025-2030年)のCAGRは6.51%で成長すると予測されています。

フレキシタリアン消費者の増加がF&Bセグメントのたんぱく質需要を牽引

- 飲食品セグメントは、同地域におけるたんぱく質の用途をリードし、主要な数量シェアと金額シェアを占めました。このシェアは乳製品、飲料、ベーカリー産業による影響が大きく、2023年に中東で消費されたたんぱく質全体の金額シェアの40%以上を占めました。このシェアは主に、飲食品セグメントにおける機能性素材、特にたんぱく質に対する需要の高まりによってもたらされました。

- 飲食品セグメントに続くのは動物飼料セグメントであり、これは植物たんぱく質の応用によって大きく牽引されています。持続可能な植物性たんぱく質源、主に大豆と小麦たんぱく質の含有は、その健康上の利点、優れた消化性、ニュートラルな風味プロファイルにより、このセグメントを大きく牽引しています。したがって、エンドウ豆たんぱく質は動物飼料に幅広く応用される機会があり、動物飼料セグメントにおいて最も急成長する植物たんぱく質タイプになると予想され、2024~2029年のCAGRは金額ベースで5.46%です。

- パーソナルケアと化粧品分野は最も急成長しており、2024~2029年のCAGRは7.03%と予測されます。たんぱく質は、乳液、ジェル、シャンプー、コンディショナー、クリームなど、さまざまな化粧品に使用されています。コラーゲン、エラスチン、ケラチンなどのたんぱく質は、肌や髪の質感を自然に強化する効果が高いため、人気も高まっています。Estee Lauder、Neu Cosmetics DMCC、Guerlainなどの企業は、より効果的で持続可能な代替タンパク源を開発するため、研究開発への投資を増やしています。このような要因が、パーソナルケア製品におけるたんぱく質の成分展望と応用を後押ししており、将来の市場成長を後押しする可能性があります。

人口の半数以上がたんぱく質サプリメントを摂取しているサウジアラビアは、同地域のたんぱく質市場で最大のシェアを占めている

- この地域で最も重要な食事と消費者の動向の一つは、植物性、フレキシタリアン、または減食主義へのシフトであり、その結果、植物性たんぱく質のシェアが最も高くなっています。植物性たんぱく質は、2023年には約82%の適用量を占める。

- 2023年にはサウジアラビアが市場をリードしました。2023年には飲食品と動物飼料セグメントがそれぞれ53%と40%の数量シェアを占め、市場の成長に貢献しました。この成長の背景には、サウジアラビアの製品統合レベルの高さと競合環境の激しさがあります。企業は中小企業を買収することで国内でのプレゼンスを強化し、それによってたんぱく質生産部門と製品ポートフォリオを拡大しています。

- サウジアラビアにおける活動的なライフスタイルの増加は、たんぱく質消費を増加させると予想されます。2021年には、サウジアラビア全土の48.2%の人々が1日30分以上の身体活動やスポーツ活動を行っています。2020年には、身体を動かしている人の約50%がたんぱく質サプリメントを消費しています。活動的な人々の約56.1%が筋肉を増やすためにたんぱく質サプリメントを摂取し、次いで28.6%の人々がたんぱく質不足を補うためにたんぱく質サプリメントを利用しています。

- イランもまた、この地域で顕著なたんぱく質市場のひとつです。2024年から2029年にかけて、金額ベースで最も速いCAGR 8.61%を記録すると予測されています。植物性たんぱく質がイラン市場を独占しており、これは飲食品と動物飼料分野からの需要によるものです。

- アラブ首長国連邦もこの地域の主要なたんぱく質市場で、大豆たんぱく質が牽引しています。大豆たんぱく質は、2023年のUAEたんぱく質市場の金額シェアの53.97%を占めています。大豆たんぱく質は主に動物飼料と飲食品分野によって牽引されています。

中東のたんぱく質市場動向

たんぱく質豊富な食事への志向が消費の伸びを支える

- 中東では、サウジアラビアがこの地域の乳製品市場の70%以上を占め、支配的なプレーヤーに浮上しました。この牙城は、乳製品への旺盛な食欲、健康志向の高まり、スポーツや栄養への関心の高まり(特に若年層)など、さまざまな要因が重なりあって築かれました。多様なフレーバー、栄養価の高さ、持ち運びやすさ、保存期間の長さといった特徴を持つホエイスナックは、スナックの選択肢として支持されています。手軽な一口を求めるミレニアル世代だけでなく、たんぱく質豊富な食生活を目指すシニア層にもアピールしています。

- 中東全域で、スポーツ栄養とサプリメントへの注目が高まっています。最先端の設備と個人に合わせたトレーニングを備えたフィットネスセンターの普及が、より多くの消費者を惹きつけています。アラブ首長国連邦(UAE)では肥満率が際立って高く、15歳以上の男性の約70%、女性の約67%が該当します。現在市場の70%を占めるスポーツ栄養への注目の高まりは、この肥満傾向と闘うための直接的な対応です。

- UAEは、コラーゲン入りの機能性食品や飲食品に対する旺盛な意欲で際立っています。高たんぱく質のコラーゲンペプチドを強化したエネルギー飲料や美容飲料は、UAEだけでなくチュニジアやアルジェリアといった近隣市場でも人気を集めています。これらの飲料は、カフェイン含有量が高いため、従来のレジャー飲料の代替品としての見方が強まっています。特筆すべきは、UAEが輸入に依存していることで、コラーゲンは主に日本とオーストラリアから調達しており、羊由来のものが特に好まれています。一方、サウジアラビアでは、特にフィットネスセンターに頻繁に通う人々の間でサプリメントの消費が急増するという傾向が見られます。

GCC諸国は牛乳と食肉の生産能力向上にさらに力を入れる

- 中東では、鶏、豚、牛の生肉やチルド肉、牛や山羊の生乳、牛の脱脂乳、乳清などの派生品など、さまざまな原材料の生産量がグラフに描かれています。特にアラブ首長国連邦は際立っており、2020年の生乳生産量は164,934TTでした。同国の生乳生産量は大幅に増加し、2020年には164,934TTに達します。特筆すべきは、2009年に22.05%でピークに達した年間成長率が、2020年には1.06%に先細りしたことです。この地域の厳しい気候やコールドチェーン技術の未熟さといった課題が、このセグメントの成長を妨げています。

- これらのハードルを克服するには、最先端の酪農技術を取り入れるだけでなく、重要な牛群管理・農場管理を実施する必要があります。大量注文は乳製品の最良価格を確保します。2020年、動物性たんぱく質の成長率は10%に急上昇し、過去の5年間平均の5%を倍増させる。さらに、食肉や水産業の廃棄物を利用することで、コラーゲンやゼラチンのような動物性たんぱく質が生産されます。しかし、中東の食肉処理場は動物福祉擁護者の間で評判が悪いことは注目に値します。

- 中東への生きた動物の輸出は過去20年間で着実に増加しており、その中でも欧州とオーストラリアは顕著な貢献者です。例えば2019年、西オーストラリア州は主に中東の9カ国に100万頭の生きた羊を出荷し、1億3,600万豪ドルに達しました。このうち、クウェート、カタール、ヨルダンが輸入量の上位に浮上し、それぞれ35%、25%、19%を占めました。この需要の急増は、肉や乳製品に対するこの地域の食欲の増加と、水不足のこれらの国々における温暖化気候による圧力の高まりが主な原因です。

中東のたんぱく質産業の概要

中東のたんぱく質市場は断片化されており、上位5社で15.13%を占めています。この市場の主要企業は以下の通りです。Cargill, Incorporated, Fonterra Co-operative Group Limited, International Flavors & Fragrances Inc., Kerry Group PLC and Royal FrieslandCampina NV(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 植物

- 生産動向

- 動物

- 植物

- 規制の枠組み

- UAEとサウジアラビア

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- ソース

- 動物

- たんぱく質タイプ別

- カゼインおよびカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫たんぱく質

- ミルクたんぱく質

- ホエイたんぱく質

- その他の動物性たんぱく質

- 微生物

- たんぱく質タイプ別

- 藻類たんぱく質

- マイコたんぱく質

- 植物

- たんぱく質タイプ別

- ヘンプたんぱく質

- エンドウ豆たんぱく質

- ポテトたんぱく質

- 米たんぱく質

- 大豆たんぱく質

- 小麦たんぱく質

- その他の植物性たんぱく質

- 動物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- イラン

- サウジアラビア

- アラブ首長国連邦

- その他中東地域

第5章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Cargill, Incorporated

- Croda International Plc

- Fonterra Co-operative Group Limited

- Hilmar Cheese Company Inc.

- International Flavors & Fragrances Inc.

- Kerry Group PLC

- Lactoprot Deutschland GmbH

- MEGGLE GmbH & Co.KG

- Prolactal

- Royal FrieslandCampina NV

- Wilmar International Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Middle East Protein Market size is estimated at 1.57 billion USD in 2025, and is expected to reach 2.15 billion USD by 2030, growing at a CAGR of 6.51% during the forecast period (2025-2030).

The rising number of flexitarian consumers drives demand for proteins from the F&B segment

- The food and beverage segment led the application of proteins in the region, accounting for major volume and value shares. The shares were highly influenced by the dairy, beverages, and bakery industries, which together accounted for more than 40% of the value share of the overall proteins consumed in the Middle East in 2023. This share was primarily driven by the rising demand for functional ingredients, particularly protein, in the food and beverage segment.

- The food and beverage segment is followed by the animal feed segment, which is largely driven by the application of plant proteins. The inclusion of sustainable plant protein sources, mainly soy and wheat proteins, drives the segment significantly due to their health benefits, excellent digestibility, and neutral flavor profile. Hence, pea protein has opportunities for wide applications in animal feed and is anticipated to be the fastest-growing plant protein type in the animal feed segment, with a CAGR of 5.46% by value during 2024-2029.

- The personal care and cosmetics segment is the fastest-growing, with a projected CAGR of 7.03% by value during 2024-2029. Proteins are used in a range of cosmetics products, including emulsions, gels, shampoos, conditioners, and creams. Proteins such as collagen, elastin, and keratin are also gaining popularity due to their higher efficacy in naturally strengthening the skin and hair texture. Companies like Estee Lauder, Neu Cosmetics DMCC, and Guerlain are increasingly investing in R&D to develop more effective and sustainable alternative protein sources. Such factors are boosting the ingredient scope and applications of protein in personal care products, which may aid the growth of the market in the future.

With more than half of its population consuming protein supplements, Saudi Arabia held the maximum share of the region's protein market

- One of the region's most important dietary and consumer trends is the shift toward plant-based, flexitarian, or reducetarian diets, resulting in the highest share of plant proteins. Plant proteins accounted for an applicational volume of around 82% in 2023.

- Saudi Arabia led the market in 2023. The food and beverage and animal feed segments held volume shares of 53% and 40%, respectively, in 2023, contributing to the market's growth. This growth was due to Saudi Arabia's high level of product integration and fiercely competitive environment. Companies are strengthening their domestic presence by acquiring small businesses, thereby expanding their protein production units and product portfolios.

- The rise in active lifestyles in Saudi Arabia is anticipated to increase protein consumption. In 2021, 48.2% of people across Saudi Arabia engaged in physical and sporting activities for at least 30 minutes per day. About 50% of physically active people consumed protein supplements in 2020. About 56.1% of active people consume protein supplements to gain muscles, followed by 28.6% of people using protein supplements to compensate for protein deficiency.

- Iran is also one of the prominent protein markets in the region. It is projected to register the fastest CAGR of 8.61% in terms of value during 2024-2029. Plant protein dominated the Iranian market, driven by the demand from the food and beverage and animal feed segments.

- The United Arab Emirates is another key protein market in the region, led by soy protein. Soy protein accounted for 53.97% of the value share of the UAE protein market in 2023. Soy protein is primarily driven by the animal feed and food and beverage segments.

Middle East Protein Market Trends

The inclination toward a protein-rich diet supports growing consumption

- In the Middle East, Saudi Arabia emerged as the dominant player, commanding over 70% of the region's dairy market. This stronghold is propelled by a confluence of factors: a surging appetite for dairy products, a growing health-conscious consumer base, and a heightened interest in sports and nutrition, especially among the younger demographic. Whey snacks, with their diverse flavors, nutritional benefits, portability, and longer shelf life, are carving a niche as a favored snack choice. They appeal not only to millennials seeking quick bites but also to seniors eyeing protein-rich diets.

- Across the Middle East, a rising emphasis on sports nutrition and supplements is evident. The proliferation of fitness centers, equipped with cutting-edge facilities and personalized training, is luring in more consumers. In the UAE, obesity rates are strikingly high, with approximately 70% of men and 67% of women over 15 falling into this category. The region's heightened focus on sports nutrition, which now constitutes 70% of the market, is a direct response to combatting this obesity trend.

- The UAE stands out for its robust appetite for collagen-infused functional foods and beverages. Energy and beauty drinks, enriched with high-protein collagen peptides, are gaining traction, not just in the UAE but also in neighboring markets like Tunisia and Algeria. These beverages are increasingly viewed as alternatives to traditional leisure drinks, thanks to their elevated caffeine content. Noteworthy is the UAE's reliance on imports, sourcing collagen predominantly from Japan and Australia, with a notable preference for sheep-based variants. Meanwhile, in Saudi Arabia, a rising trend is observed: a surge in supplement consumption, especially among those frequenting fitness centers.

GCC countries to focus more on increasing production capabilities of milk and meat

- In the Middle East, the production of various raw materials, including fresh or chilled meat of chickens, pigs, and cattle, along with raw milk from cattle and goats, skim milk from cows, and derivatives like whey, was depicted in the graph. Specifically, the United Arab Emirates stood out, producing 164,934 TT of milk in 2020. The country's milk output saw a significant uptick, hitting 164,934 TT in 2020. Notably, its annual growth rate, which peaked at 22.05% in 2009, tapered off to 1.06% by 2020. Challenges like harsh climates and nascent cold chain technology in the region hamper this segment's growth.

- Overcoming these hurdles requires not only embracing cutting-edge dairy farming tech but also implementing key herd and farm management practices. Bulk orders secure the best prices for dairy products. In 2020, the growth rate of animal protein surged to 10%, doubling the historical 5-year average of 5%. Additionally, by utilizing meat and marine industry waste, animal proteins like collagen and gelatin are produced. However, it's worth noting that slaughterhouses in the Middle East have garnered a poor reputation among animal welfare advocates.

- Live animal exports to the Middle East have seen a steady climb over the last two decades, with Europe and Australia being notable contributors. For instance, in 2019, Western Australia shipped 1.0 million live sheep to nine countries, predominantly in the Middle East, fetching a value of AUD 136 million. Among these, Kuwait, Qatar, and Jordan emerged as the top importers, accounting for 35%, 25%, and 19% of the volume, respectively. This surge in demand is largely attributed to the region's increasing appetite for meat and dairy, coupled with the mounting pressure from a warming climate in these water-stressed nations.

Middle East Protein Industry Overview

The Middle East Protein Market is fragmented, with the top five companies occupying 15.13%. The major players in this market are Cargill, Incorporated, Fonterra Co-operative Group Limited, International Flavors & Fragrances Inc., Kerry Group PLC and Royal FrieslandCampina NV (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 UAE and Saudi Arabia

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Iran

- 4.3.2 Saudi Arabia

- 4.3.3 United Arab Emirates

- 4.3.4 Rest of Middle East

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Cargill, Incorporated

- 5.4.2 Croda International Plc

- 5.4.3 Fonterra Co-operative Group Limited

- 5.4.4 Hilmar Cheese Company Inc.

- 5.4.5 International Flavors & Fragrances Inc.

- 5.4.6 Kerry Group PLC

- 5.4.7 Lactoprot Deutschland GmbH

- 5.4.8 MEGGLE GmbH & Co.KG

- 5.4.9 Prolactal

- 5.4.10 Royal FrieslandCampina NV

- 5.4.11 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms