|

市場調査レポート

商品コード

1683501

南米のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)South America Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のたんぱく質:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 277 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

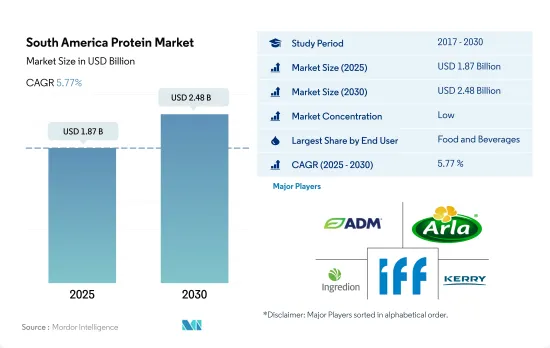

南米のたんぱく質市場規模は2025年に18億7,000万米ドルと推定され、2030年には24億8,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは5.77%で成長する見込みです。

ベーカリーおよび乳製品/乳製品代替製品がたんぱく質の最大の用途であることから、この地域では飲食品部門が主要市場シェアを占めています。

- 南米では、飲食品セグメントがたんぱく質の主要消費者として際立っています。このセグメントの中では、ベーカリー、乳製品、乳製品代替製品が極めて重要であり、2023年の飲食品カテゴリーにおけるたんぱく質市場の46.8%以上を占めています。ゼラチンは、そのたんぱく質含有量で知られ、透明なゲル化・増粘剤であるため、ベーカリーのサブセグメントでは定番となっています。

- 乳製品および乳製品代替品サブセグメントは、たんぱく質の展望における重要なプレーヤーであり、予測期間中に金額ベースで3.90%の安定したCAGRを記録しました。この成長は、チーズ製造におけるカゼインの採用や、乳製品デザートにたんぱく質を強化するという一般的な動向に後押しされています。メーカー各社は、アイスクリームやヨーグルトのような人気製品にたんぱく質強化バージョンを投入することで対応し、「高タンパク」「たんぱく質添加」という消費者の需要を取り込んでいます。この分野では、カゼインとカゼイン酸塩に続いて、乳清たんぱく質と乳たんぱく質が最も利用されている動物性たんぱく質です。これらの用途は栄養学にとどまらず、口当たり、粘度、構造的完全性などの特性を向上させる。

- 一方、動物飼料分野は、たんぱく質の第二の消費者として台頭してきています。植物性たんぱく質、特に大豆は、2024年から2029年にかけて金額ベースで6.21%の堅調なCAGRが見込まれます。大豆の魅力はその一貫した栄養プロファイルにあり、動物用飼料の配合において好ましい選択肢となっています。消化しやすいアミノ酸を豊富に含む濃縮大豆は、脂質と保水性に優れているため、特に鶏のプレスターター食に好まれています。この地域は大豆の生産が盛んであるため、メーカーは動物用飼料の配合に大豆たんぱく質を使用するのが便利でコスト効率も良いと感じています。

スポーツ栄養と栄養補助食品への消費者の関心が高まる中、ブラジルが南米のたんぱく質市場を独占しています。

- 南米のたんぱく質市場は、2024年から2029年にかけて金額ベースで5.31%のCAGRを記録し、大きな成長が見込まれています。ブラジルは、国立衛生監視局(ANIVSA)の栄養補助食品に関する2018年の規制を受けて、市場へのアクセスが急増しました。これらの変更は、ブランドの市場参入を容易にしただけでなく、既存ブランドの繁栄と革新のための環境を促進しました。

- ブラジルは市場のリーダーとして際立っており、植物性たんぱく質への需要が顕著です。この需要の高まりは、ブラジルの高齢化が大きく影響しており、2050年までに高齢化率は3倍になり、約6,600万人に達すると予測されています。健康志向の高まりにより、消費者はより健康的な食生活を選択するようになっています。その結果、ブラジルは2024年から2029年にかけてCAGR 5.95%を記録し、南米の国々を上回ることが予想されます。用途別では、飲食品セグメントが最も大きなシェアを占めており、ベーカリー、肉/肉代替品、乳製品/乳製品代替品の各サブセグメントが2023年の同セグメント需要の77.8%を占めています。

- アルゼンチンはたんぱく質市場で第2位のプレーヤーです。アルゼンチンのたんぱく質市場では、植物性たんぱく質が急成長セグメントとして浮上し、2023年には58.51%の金額シェアを獲得します。同国の消費は動物性たんぱく質に大きく依存しているが、ビーガン、ベジタリアン、フレキシタリアンなど多様な食生活への嗜好の高まりにより、乳製品や肉代替食品などの用途で植物性たんぱく質の需要が増加しています。アルゼンチンでは、植物ベースの動向が近年勢いを増しており、人口の12%がビーガンまたはベジタリアンであると認識しています。

南米のたんぱく質市場動向

たんぱく質豊富な食事への嗜好の高まりが消費に影響

- グラフは、南米各国の一人当たりの動物性たんぱく質消費量を示しています。経済的課題にもかかわらず、南米では健康とウェルネス製品への意欲が高まっています。骨粗鬆症や関節の健康など、運動関連の健康問題に対する懸念は消費者にとって最も重要です。その結果、コラーゲンメーカーはこの需要を満たすため、栄養補助食品メーカーをターゲットにするようになっています。2018年には、ブラジルがこの地域をリードし、健康・ウェルネス製品の消費額は217億米ドルを超えました。この地域はまた、心血管問題や糖尿病などの疾患の急増に取り組んでおり、動物由来の栄養補助食品へのシフトを促しています。

- 南米の消費者は食生活と健康の関連性をより強く認識するようになっており、市場の拡大を後押ししています。機能性食品や栄養強化食品への旺盛な需要に後押しされ、たんぱく質が豊富な食品の売上が急増しています。消費者は日々の食生活において、天然素材やオーガニックの選択肢を明らかに選好しています。特にアルゼンチンでは、2022年までに有機パッケージ食品と飲料の消費が2020年比で125%増加するという驚異的な数字が示されました。

- ブラジル人の化粧品志向は顕著で、業界各社はコラーゲンやゼラチンペプチドへの投資を活発化させています。これらのペプチドは栄養補助食品だけでなく化粧品にも応用されています。最適な肌の健康のために、ブラジル人は2.5グラムのコラーゲンペプチドを摂取するよう勧められています。関節リウマチや骨粗しょう症などの問題により、2020年には死亡率が16%上昇するといった驚くべき健康統計は、今後数年間でコラーゲンペプチドベースのサプリメントの需要が急増すると予想されることを裏付けています。

動物性たんぱく質原料メーカーの原料として、牛乳と食肉の生産が大きく貢献しています。

- グラフは、南米における主要原材料の生産動向を示しています。骨付き牛・豚の生肉、生鮮・冷蔵肉、牛・ヤギの生乳、牛の脱脂乳、乾燥ホエイパウダーなどです。鶏肉生産が課題に直面している一方で、乳たんぱく質、乳清たんぱく質、カゼイン、カゼイン酸塩のような他の動物性たんぱく質は、主原料として牛乳に大きく依存しています。主に悪天候と経済状況による2019年の落ち込みの後、生乳生産は2020年に力強く回復しました。しかし、この明るい勢いは、現在進行中のCOVID-19パンデミックに起因する不確実性によって影を潜めています。アルゼンチンとウルグアイの2020年上半期の累計成長率はそれぞれ8.7%と3.9%でした。さらに、コロンビアやチリといった太平洋沿岸の純輸入国も顕著な生産量の増加を経験しました。

- アルゼンチンはこの地域の重要な生乳生産国として際立っています。しかし、このセクターは、貿易介入主義や重い税負担を特徴とする政府の政策による課題に直面しており、これが経営の複雑化や投資の減少につながっています。こうしたハードルにもかかわらず、アルゼンチンの2021年の生乳総生産量は2020年比で4%増加しました。この地域はまた、食肉処理活動からコラーゲンやゼラチンのような動物性たんぱく質を得ています。一方、ブラジルは、生産効率、疾病管理、サプライチェーンの透明性への投資を重視し、牛肉生産を強化し続けています。特に、ブラジルの牛肉生産性の急上昇は、20年間で1,700万頭近く増加した国の牛群の大幅な増加に大きく起因しています。

南米たんぱく質産業の概要

南米のたんぱく質市場は細分化されており、上位5社で26.67%を占めています。この市場の主要企業は以下の通りです。Archer Daniels Midland Company, Arla Foods amba, Ingredion Incorporated, International Flavors & Fragrances, Inc. and Kerry Group plc(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 植物

- 生産動向

- 動物

- 植物

- 規制の枠組み

- ブラジルとアルゼンチン

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 原料

- 動物

- たんぱく質タイプ別

- カゼインおよびカゼイネート

- コラーゲン

- 卵たんぱく質

- ゼラチン

- 昆虫たんぱく質

- ミルクたんぱく質

- ホエイたんぱく質

- その他の動物性たんぱく質

- 微生物

- たんぱく質タイプ別

- 藻類たんぱく質

- マイコたんぱく質

- 植物

- たんぱく質タイプ別

- ヘンプ・たんぱく質

- エンドウ豆たんぱく質

- ポテトたんぱく質

- 米たんぱく質

- 大豆たんぱく質

- 小麦たんぱく質

- その他の植物性たんぱく質

- 動物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- アルゼンチン

- ブラジル

- その他南米

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Archer Daniels Midland Company

- Arla Foods amba

- Bremil Group

- BRF S.A.

- Gelnex

- Ingredion Incorporated

- International Flavors & Fragrances, Inc.

- Kerry Group plc

- Lactoprot Deutschland GmbH

- Tereos SCA

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The South America Protein Market size is estimated at 1.87 billion USD in 2025, and is expected to reach 2.48 billion USD by 2030, growing at a CAGR of 5.77% during the forecast period (2025-2030).

With bakery and dairy/dairy alternative products seeing the largest application of protein, the food and beverage segment occupied the leading market share in the region

- In South America, the food and beverage segment stands out as the primary consumer of proteins. Within this segment, bakery, dairy, and dairy-alternative products are pivotal, jointly commanding over 46.8% of the protein market in 2023 within the food and beverages category. Gelatin, known for its protein content, is a transparent gelling and thickening agent, making it a staple in the bakery sub-segment.

- The dairy and dairy-alternative sub-segment is a significant player in the protein landscape, which saw a steady CAGR of 3.90% by value during the forecast period. This growth is fueled by the adoption of casein in cheese production and the prevailing trend of fortifying dairy desserts with proteins. Manufacturers are responding by introducing protein-enhanced versions of popular products like ice creams and yogurts, capitalizing on the "high protein" and "added protein" consumer demands. In this segment, whey protein and milk protein, following casein and caseinates, are the most utilized animal proteins. Their applications extend beyond nutrition, enhancing attributes like mouthfeel, viscosity, and structural integrity.

- Meanwhile, the animal feed segment is emerging as the second-largest consumer of proteins. Plant proteins, especially soy, are expected to witness a robust CAGR of 6.21% by value from 2024 to 2029. Soy's appeal lies in its consistent nutritional profile, making it a preferred choice in animal feed formulations. Soy concentrates, rich in easily digestible amino acids, are particularly favored for chicken pre-starter meals, given their benefits in lipid and water retention. With the region boasting significant soy production, manufacturers are finding it both convenient and cost-effective to pivot toward soy proteins in their animal feed formulations.

Brazil is dominating the South American protein market with growing consumer emphasis on sports nutrition and dietary supplements

- The South American protein market is poised for significant growth, registering a CAGR of 5.31% from 2024 to 2029 by value, primarily driven by increased government support to key application industries. Brazil saw a surge in market accessibility following the National Sanitary Surveillance Agency's (ANIVSA) 2018 regulations on dietary supplements. These changes not only facilitated easier market entry for brands but also fostered an environment for existing brands to thrive and innovate.

- Brazil stands out as the market leader, with a pronounced demand for plant proteins. This heightened demand is largely influenced by Brazil's aging population, which is projected to triple by 2050, encompassing approximately 66 million individuals. With rising health consciousness, consumers are pivoting toward healthier dietary choices. Consequently, the country is expected to outpace its South American counterparts, registering a CAGR of 5.95% from 2024 to 2029. In terms of applications, the food and beverage segment accounts for the most significant share, with bakery, meat/meat alternatives, and dairy/dairy alternatives sub-segments collectively accounting for 77.8% of the segment's demand in 2023.

- Argentina is the second-largest player in the protein market. In Argentina's protein market, plant protein emerged as the fastest-growing segment, capturing a 58.51% value share in 2023. While the country heavily relies on animal-based protein for consumption, the rising preference for diverse diets such as vegan, vegetarian, and flexitarian has led to increased demand for plant proteins in applications like dairy and meat alternatives. In Argentina, the plant-based trend has gained momentum in recent years, with 12% of the population identifying as vegan or vegetarian.

South America Protein Market Trends

Increasing preference for protein rich diet to influence consumption

- The graph illustrates the per capita consumption of animal protein across South American countries. Despite economic challenges, South America is witnessing a growing appetite for health and wellness products. Concerns over mobility-related health issues, such as osteoporosis and joint health, are paramount for consumers. Consequently, collagen manufacturers are increasingly targeting dietary supplement producers to meet this demand. In 2018, Brazil led the region, with health and wellness product consumption exceeding USD 21.7 billion. The region is also grappling with a surge in diseases like cardiovascular issues and diabetes, prompting a shift towards animal-based dietary supplements.

- South American consumers are becoming more cognizant of the link between diet and health, propelling the market's expansion. The sales of protein-rich foods are surging, driven by a heightened appetite for functional and fortified foods. Consumers are showing a clear preference for natural and organic options in their daily diets. Notably, by 2022, Argentina saw a staggering 125% rise in organic packaged food and beverage consumption from 2020.

- Brazilians exhibit a pronounced inclination towards cosmetics, prompting industry players to ramp up investments in collagen and gelatin peptides. These peptides find applications not just in dietary supplements but also in cosmetics. For optimal skin health, Brazilians are advised to consume 2.5 grams of collagen peptides. Alarming health statistics, such as a 16% rise in the mortality rate in 2020 due to issues like rheumatoid arthritis and osteoporosis, underscore the anticipated surge in demand for collagen peptide-based supplements in the coming years.

Milk and meat production contributes majorly as raw material for animal protein ingredients manufacturers

- The graph illustrates the production trends of key raw materials in South America, including cattle and pig meat with bone, fresh or chilled; raw milk from cattle and goats; skim milk from cows; and dry whey powder. Notably, while chicken meat production faced challenges, other animal proteins, like milk proteins, whey proteins, casein, and caseinates, rely heavily on milk as their primary raw material. After a dip in 2019, primarily due to adverse weather and economic conditions, milk production rebounded strongly in 2020. However, this positive momentum is now overshadowed by the uncertainties stemming from the ongoing COVID-19 pandemic. Argentina and Uruguay saw year-to-date growth rates of 8.7% and 3.9%, respectively, in the first half of 2020. Additionally, net importing nations on the Pacific coast, such as Colombia and Chile, also experienced notable production upticks.

- Argentina stands out as a significant milk producer in the region. Yet, the sector faces challenges due to government policies, marked by trade interventionism and a heavy tax burden, leading to operational complexities and reduced investments. Despite these hurdles, Argentina managed a 4% increase in total milk output in 2021 compared to 2020. The region also derives animal proteins like collagen and gelatin from its meat slaughtering activities. Brazil, on the other hand, continues to bolster its beef production, emphasizing investments in production efficiency, disease control, and supply chain transparency. Notably, Brazil's beef productivity surge is largely attributed to a substantial increase in its national herd, which grew by nearly 17 million heads over two decades.

South America Protein Industry Overview

The South America Protein Market is fragmented, with the top five companies occupying 26.67%. The major players in this market are Archer Daniels Midland Company, Arla Foods amba, Ingredion Incorporated, International Flavors & Fragrances, Inc. and Kerry Group plc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 Brazil and Argentina

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Rest of South America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Arla Foods amba

- 5.4.3 Bremil Group

- 5.4.4 BRF S.A.

- 5.4.5 Gelnex

- 5.4.6 Ingredion Incorporated

- 5.4.7 International Flavors & Fragrances, Inc.

- 5.4.8 Kerry Group plc

- 5.4.9 Lactoprot Deutschland GmbH

- 5.4.10 Tereos SCA

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms