|

市場調査レポート

商品コード

1683963

南米の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)South America Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 186 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

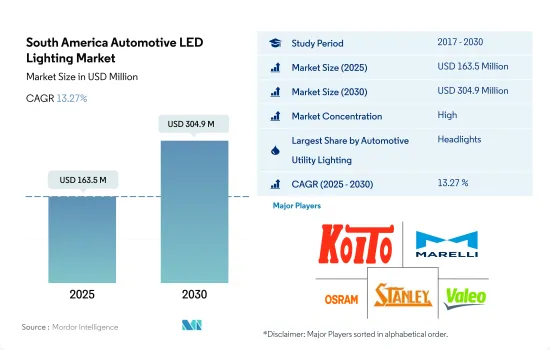

南米の自動車用LED照明市場規模は2025年に1億6,350万米ドルと推定され、2030年には3億490万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは13.27%で成長します。

ヘッドライトが最も高い市場シェアを占める見込み

- 金額ベースでは、2023年にヘッドライトが大半のシェアを占め、フォグランプと方向指示灯がそれに続きます。ヘッドライトと方向指示器用信号灯の市場シェアは予測期間中に上昇すると見込まれます。採用の主な理由は、エネルギー効率と事故防止です。ヘッドライトとして使用されるLED照明は、その高価格にかかわらず、エネルギー消費量を60%削減できるため、市場シェアは拡大します。リオなど市街地の穴ぼこは交通事故の9割の原因であり、それを防ぐためにLEDヘッドライトが採用されています。

- 数量シェアでは、2023年に方向指示灯(DSL)が過半数を占め、次いでヘッドライト、フォグライトと続きます。南米では、事故率の高さと購入者数の多さから、現在乗用車が大半のシェアを占めています。ラテンアメリカとカリブ海諸国(LAC)では交通安全が不十分なため、年間13万人近くの死者と600万人の負傷者が出ており、これには適切なDSLがないことも含まれています。このような要因から、このような照明に対する大きな量的需要があり、今後数年間で増加することが予想されます。

- 南米諸国のEV政策は、EV販売の主要動向であり、間接的にLED照明の需要を増加させています。コスタリカでは、2050年までに軽自動車の新車販売の100%、バスとタクシーの100%をZEV(ゼロ・エミッション・ビークル)にすることになっています。チリでは、2035年までに小型車、都市バス、タクシーの新車販売の100%がEVになります。このような要因が市場を押し上げると予想されます。

南米の自動車用LED照明市場動向

EV販売の増加がLED市場を牽引

- 南米の自動車総生産台数は2022年に512万台、2023年には543万台に達すると予測されます。パンデミックとマイクロ部品の不足がラテンアメリカの自動車セクターに大きな影響を与えています。COVID-19パンデミックのため、ラテンアメリカの主要自動車メーカー2社、メキシコとブラジルは4月に99%という驚異的な落ち込みを見せ、合計でわずか5,569台しか生産しませんでした。どの国よりも米国への輸出に依存しているメキシコからは、4月に2万7,889台しか出荷されていないです。ブラジルは自国市場により関心を持っています。しかし、アルゼンチンへの輸出は多いです。輸出は77%減少しました。自動車事業におけるLED照明の需要は、自動車生産の減少の影響を受けました。

- 南米の自動車メーカーには、フォード・モーター、ゼネラル・モーターズ、ホンダ、BMW、フィアット、シボレー、プジョーなどがあります。ラテンアメリカでは、EVが増加しています。例えば、ラテンアメリカのプレミアムカー購入者が電気自動車の販売台数増加を牽引しています。2021年にはこの地域で2万5,000台近くのEVが販売され、2020年の2倍以上となりました。メキシコからチリまで、2021年のEV販売台数は全自動車販売台数の0.7%を占めたが、地域によってばらつきがあります。ブラジルの販売台数が最も多く(1万3,000台)、コスタリカの割合が最も高かった(全販売台数の2.7%がプラグ付き)。このため、EVを採用する人が増えるにつれて、自動車業界におけるLED照明のニーズが拡大すると予想されます。

LED市場を牽引するのは、同地域でEV販売を推進する政府の取り組み

- 南米のEV市場は大幅に上昇すると予測されています。2022年上半期、同地域の9カ国で電気自動車とハイブリッド車の販売台数が6万7,000台を超えました。同期間、中南米8カ国の販売比率は37.7%増加しました。ブラジルは、南米の自動車市場全体の半分以上を占めています。2022年のブラジル市場の自動車販売台数は91万7,942台で、そのうちBEVは3,843台(0.4%)、HEVとPHEVの両方を含むハイブリッド車は1万9,764台でした。

- この地域は、政府のインセンティブプログラム、従来型燃料の価格上昇、利用可能なEVモデルの拡大などの複合的な要因によって牽引されています。また、南米でのEV販売は、充電インフラの拡大と低排出ガスバンや小型トラックの需要増加によって後押しされています。2022年2月、電化・デジタル化された都市インフラのエコシステムとエネルギー効率化サービスを提供するエネルX SRLは、電気を主なエネルギー源とするあらゆる車両をサポートするラテンアメリカ初の「EVサービスステーション」をチリに開設しました。

- チリ政府は、EV開発規制の基準を設定しています。チリ政府は2021年、2035年以降にチリで販売されるすべての車両を電気自動車にすると表明しました。2022年11月、BYDはブラジルのバイーア州カマカリ市政府と、電気自動車と原料電池の製造工場を設立する意向表明書に調印しました。生産ラインのうち2ラインは2024年10月までに稼動し、もう1ラインは2025年1月に稼動します。このように、上記のような事例は、EV需要の高まりによる新しい発電所の開発と生産につながり、この地域の自動車用LEDの需要を押し上げます。

南米の自動車用LED照明産業概要

南米の自動車用LED照明市場はかなり統合されており、上位5社で134.33%を占めています。この市場の主要企業は以下の通りです。KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH., Stanley Electric and Valeo(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- アルゼンチン

- ブラジル

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

- デイタイム・ランニング・ライト(DRL)

- 方向指示器

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ASX Iluminacao

- HELLA GmbH & Co. KGaA

- HYUNDAI MOBIS

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- NAOEVO Lighting

- OSRAM GmbH.

- SHOCKLIGHT

- Stanley Electric Co., Ltd.

- Valeo

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The South America Automotive LED Lighting Market size is estimated at 163.5 million USD in 2025, and is expected to reach 304.9 million USD by 2030, growing at a CAGR of 13.27% during the forecast period (2025-2030).

Headlights are expected to hold the highest market share

- In terms of value, in 2023, headlights accounted for the majority share, followed by fog lights and directional signal lights. The market share for headlights and directional signal lights is expected to increase during the forecast period. The major reason for their adoption is the energy efficiency and accident prevention. Irrespective of its high price, the market share will increase as LED lighting used as headlights provides a 60% decrease in energy consumption. Potholes in city streets, such as Rio, are the cause of 90% of traffic accidents, and LED headlights are adopted to prevent them.

- In terms of volume share, in 2023, directional signal lights (DSL) accounted for a majority share, followed by headlights and fog lights. In South America, passenger cars currently have the majority share due to the high accident rate and number of buyers in the region. The lack of road safety in Latin America and the Caribbean (LAC) results in nearly 130,000 deaths and six million injuries per year, which also includes a lack of proper DSL. Such a factor indicates major volume demand for such lighting and is expected to increase in the coming years.

- EV policy in South American countries is the major trend adoption for EV sales, which is indirectly increasing the demand for LED lighting. In Costa Rica, 100% of new light vehicle sales and 100% of buses and taxis will be ZEVs (Zero Emission Vehicles) by 2050. In Chile, 100% of new sales of light-duty vehicles, urban buses, and taxis will be EVs by 2035. Such factors are expected to boost the market.

South America Automotive LED Lighting Market Trends

Increasing EV sales to drive the LED market

- The total automobile vehicle production in South America was 5.12 million units in 2022, and it was expected to reach 5.43 million units in 2023. The pandemic and the lack of micro components have had a significant impact on the automotive sector in Latin America. Due to the COVID-19 pandemic, leading two auto producers in Latin America, Mexico, and Brazil had an astounding 99% drop in April, producing just 5,569 vehicles in total. Only 27,889 vehicles were sent from Mexico in April, which is more reliant on exports to the United States than any other country. Brazil is more concerned with its own local market. However, it exports a lot to Argentina. Exports decreased by 77%. The demand for LED lighting in the automotive business was impacted by the decline in auto production.

- South American automakers include Ford Motor Company, General Motors Company, Honda, BMW, Fiat, Chevrolet, and Peugeot. In Latin America, the number of EVs is increasing. For instance, premium car buyers in Latin America are driving an increase in the sales of electric vehicles. Nearly 25,000 EVs were sold in the area in 2021, more than double the amount sold in 2020. From Mexico to Chile, EV sales made up 0.7% of all automobile sales in 2021, with regional variations. Brazil sold the most units (13,000), and Costa Rica had the highest percentage (2.7% of all vehicles sold had a plug). Therefore, it is anticipated that the need for LED lighting in the automobile industry will expand as more people adopt EVs.

The LED market is driven by government initiatives propelling EV sales in the region

- The South American EV market is predicted to rise significantly. In the first half of 2022, 9 countries in the region saw electric and hybrid vehicle sales of more than 67,000 vehicles. In the same period, sales percentage increased by 37.7% in 8 Latin American countries. Brazil accounts for well over half the entire South American vehicle market. In 2022, the Brazilian market saw 917,942 vehicle sales, of which 3,843 were BEVs (0.4%) and 19,764 were hybrids, including both HEVs and PHEVs.

- The region is driven by a combination of factors that include government incentive programs, rising prices for conventional fuels, and a wider range of available EV models. Also, EV sales in South America have been boosted by an expansion of charging infrastructure and increased demand for low-emission vans and small trucks. In February 2022, Enel X SRL, which provides electrified and digitalized urban infrastructure ecosystem and energy efficiency services, opened the first "EV Service Station" in Latin America, located in Chile, to support any vehicle that uses electricity as its primary energy source.

- The Chilean government is setting the standard for EV development regulations. Chile's government stated in 2021 that all vehicles sold in Chile after 2035 will be electric. In November 2022, BYD signed a statement of intent with the municipal government of Camacari in the Brazilian state of Bahia to establish a manufacturing plant for electric vehicles and raw battery materials. Two of its production lines will be operational by October 2024, and the other line will go live in January 2025. Thus, the above instances lead to the development and production of new power stations because of the growing demand for EVs, which boosts the demand for automotive LEDs in the region.

South America Automotive LED Lighting Industry Overview

The South America Automotive LED Lighting Market is fairly consolidated, with the top five companies occupying 134.33%. The major players in this market are KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 Argentina

- 4.11.2 Brazil

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ASX Iluminacao

- 6.4.2 HELLA GmbH & Co. KGaA

- 6.4.3 HYUNDAI MOBIS

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 NAOEVO Lighting

- 6.4.7 OSRAM GmbH.

- 6.4.8 SHOCKLIGHT

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms