|

|

市場調査レポート

商品コード

1683933

中国の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 182 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

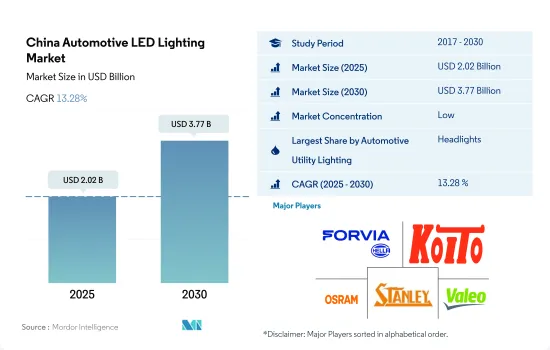

中国の自動車用LED照明市場規模は2025年に20億2,000万米ドルと推定され、2030年には37億7,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは13.28%で成長する見込みです。

自動車へのLEDライト採用で事故件数が減少

- 2023年、中国の自動車照明市場ではヘッドライトが金額シェアの大半を占め、次いでその他と方向指示灯が続きます。予測期間中、方向指示灯とストップランプの市場シェアは変わらず、ヘッドライトは若干減少すると予想されます。市場の新たな動向として、DRL(デイタイム・ランニング・ランプ)とプロジェクター・ライトを組み合わせた前照灯があり、上海汽車や吉利汽車などの有名メーカーが近々発売する自動車に搭載する予定です。また、事故動向の高まりから、フォグLEDランプの普及率向上も見込まれています。2019年の中国の交通事故による負傷者数は256,101人、死亡者数は62,763人で、2016年から大幅に増加しています。

- 数量シェアでは、2022年に方向信号灯が過半数を占め、次いでヘッドライト、その他となっています。これらのライトの市場シェアは変動が少なく、比較的安定して推移すると予想されます。あらゆるタイプの自動車において、方向指示灯は軽微な事故から重大な事故まで影響を受ける可能性が高く、交換が必要な主要部品です。

- 中国の自動車市場は競争が激しく、BYD、上海汽車、吉利汽車、BMW、メルセデス・ベンツといった既存の自動車メーカーと並んで、NIO、XPeng、Li Autoといった中国のNEV(新型電気自動車)新興企業が市場シェアを争っています。電気自動車の追求は、シャオミやバイドゥといったハイテク大手も引き付けています。したがって、NEVの成長はLEDの市場浸透を高めると思われます。

中国自動車用LED照明市場動向

アジア太平洋地域における自動車用LED照明の技術革新の高まりがLED市場全体を押し上げる

- 中国の自動車総生産台数は2022年に4,668万台で、2023年には4,949万台に達すると予想されています。中国の自動車供給業界はCOVID-19によって深刻な影響を受けました。海上輸送は悪影響を受け、重要な自動車部品は、主に工場や組立ラインの閉鎖がもたらした大幅な需要減少のため、大量のコンテナで欧州に送られなくなりました。そのため、航路上のコンテナ船や生産者の船隊は30%減少しました。この自動車部品の混乱は、自動車に使用されるLED照明に悪影響を与えました。

- 上海汽車、吉利汽車、長城汽車、奇瑞汽車、第一汽車集団などは、国内トップクラスの自動車メーカーです。著名な企業の1つである上海汽車は、自動車に使用する人工知能(AI)技術、スマート燃料電池、インテリジェント相互接続に多額の投資を行っています。このような進展により、自動車におけるコネクテッド・テクノロジーとしてのLEDの使用は増加すると予想されます。

- LED照明は環境に優しく、生来のエネルギー効率に優れているため、現在、自動車用途では当然の選択肢と見なされています。LEDライトは、自動車の外観を向上させる革新的な照明コンセプトを生み出すのに役立っています。主要企業は協力して、自動車産業向けの技術的なLED製品を開発しています。例えば、amsオスラムとTactoTekは2022年9月、前衛的なRGBサイドルッカーLED OSIRE E5515を搭載したデモ機を共同開発しました。車内に簡単に組み込むことができ、よりコンパクトなデザインを実現します。このようなイノベーションと自動車用LEDライトへの今後の投資は、予測期間中の市場を牽引すると思われます。

EV需要の高まりが市場成長を牽引

- COVID-19の流行とそれに伴うサプライチェーンの制約にもかかわらず、中国では電気自動車(EV)市場が大きく成長しています。EV販売は、最近の障害や原材料価格の上昇による生産コストの上昇にもかかわらず、急速に増加し続けています。中国には、2022年末時点でEV充電ステーションが約160万カ所、充電ポイントが521万カ所(2022年に建設された259万カ所超を含む)あります。さらに、2022年までに、2022年に建設された675ヵ所を含む1973ヵ所のバッテリー交換ステーションがあり、中国には1万ヵ所以上の電源バッテリー・リサイクル・サービス店舗があります。このように、充電設備の急速な増加は、同国における新エネルギー自動車(NEV)セクターの活況を示しています。

- 中国は、販売台数の伸びが鈍化する中、EVの税制優遇措置を延長する予定です。EVとプラグイン・ハイブリッド車の購入減税は、30万人民元(42062.76米ドル)以下(19万5000人民元(27340.03米ドル)以下)です。それ以上の車両は中国では広く高級車に分類されるため、人々はより手頃な価格のクリーンカーを購入しやすくなります。このような要因によって、中国のEV普及率は高まり、2060年までにネット・ゼロ・エミッションを達成するという目標も達成されると思われます。

- 2023年5月、ロジャースは、国内外の顧客により良いサービスを提供し、電気自動車やハイブリッド車(EV/HEV)、再生可能エネルギー用途に使用されるパワー基板の需要増に対応するため、パワー基板を生産する新工場を中国に建設すると発表しました。この拡張の第一段階は2025年に完了する予定です。自動車メーカー各社は、EVの需要拡大を受けて新エネルギー車の開発・生産にしのぎを削っており、これが自動車用LEDの需要を押し上げています。LEDカーライトはハロゲン電球よりも消費電力が少ないため、EVの省エネと走行距離の延長に役立ちます。

中国の自動車用LED照明産業の概要

中国の自動車用LED照明市場は細分化されており、上位5社で35.95%を占めています。この市場の主要企業は以下の通りです。HELLA GmbH & Co. KGaA(FORVIA), KOITO MANUFACTURING, OSRAM GmbH., Stanley Electric and Valeo(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- #世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

- デイタイムランニングライト(DRL)

- 方向指示灯

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Changzhou Xingyu Automotive Lighting System Co, Ltd.

- Hasco Vision Technology Co., Ltd.

- HELLA GmbH & Co. KGaA(FORVIA)

- HYUNDAI MOBIS

- KOITO MANUFACTURING CO., LTD.

- Nichia Corporation

- OSRAM GmbH.

- Stanley Electric Co., Ltd.

- Sunway Autoparts

- Valeo

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The China Automotive LED Lighting Market size is estimated at 2.02 billion USD in 2025, and is expected to reach 3.77 billion USD by 2030, growing at a CAGR of 13.28% during the forecast period (2025-2030).

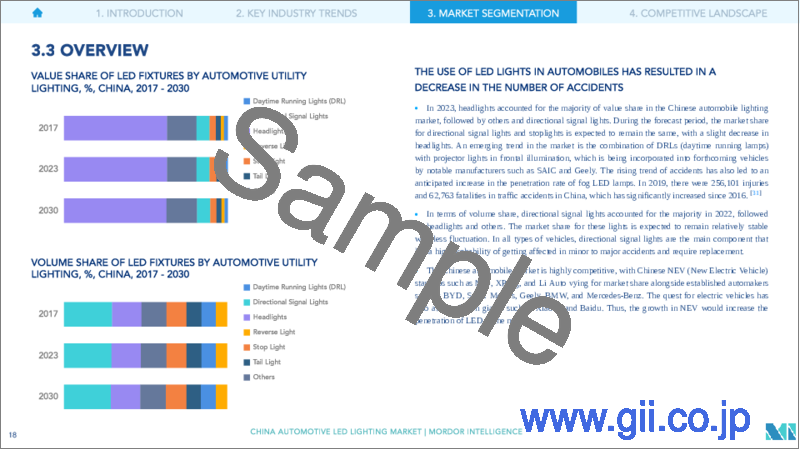

The use of LED lights in automobiles has resulted in a decrease in the number of accidents

- In 2023, headlights accounted for the majority of value share in the Chinese automobile lighting market, followed by others and directional signal lights. During the forecast period, the market share for directional signal lights and stoplights is expected to remain the same, with a slight decrease in headlights. An emerging trend in the market is the combination of DRLs (daytime running lamps) with projector lights in frontal illumination, which is being incorporated into forthcoming vehicles by notable manufacturers such as SAIC and Geely. The rising trend of accidents has also led to an anticipated increase in the penetration rate of fog LED lamps. In 2019, there were 256,101 injuries and 62,763 fatalities in traffic accidents in China, which has significantly increased since 2016.

- In terms of volume share, directional signal lights accounted for the majority in 2022, followed by headlights and others. The market share for these lights is expected to remain relatively stable with less fluctuation. In all types of vehicles, directional signal lights are the main component that has a high probability of getting affected in minor to major accidents and require replacement.

- The Chinese automobile market is highly competitive, with Chinese NEV (New Electric Vehicle) start-ups such as NIO, XPeng, and Li Auto vying for market share alongside established automakers such as BYD, SAIC Motors, Geely, BMW, and Mercedes-Benz. The quest for electric vehicles has also attracted tech giants such as Xiaomi and Baidu. Thus, the growth in NEV would increase the penetration of LED in the market.

China Automotive LED Lighting Market Trends

Growing innovation in automotive LED light in the Asia-Pacific region will boost the overall LED market

- The total automobile vehicle production in China was 46.68 million units in 2022, and it is expected to reach 49.49 million units in 2023. The automotive supply industry in China was severely affected by COVID-19. Maritime transportation was negatively impacted, and critical automotive parts were no longer sent in large quantities of containers to Europe, mainly because of a substantial decline in demand brought on by the closure of plants and assembly lines. Thus, the fleets of container carriers and producers on trade routes decreased by 30%. This disruption in automotive parts negatively impacted LED lights used in automobiles.

- SAIC Motor, Geely, Great Wall Motor, Chery, FAW Group, and other companies are among the nation's top automakers. One prominent business, SAIC Motor, is making significant investments in artificial intelligence (AI) technology, smart fuel cells, and intelligent interconnection for use in automobiles. The use of LEDs as a connected technology in vehicles is anticipated to increase due to this progress.

- Due to LED lights' environmental friendliness and innate energy efficiency, they are currently seen as a natural choice in automotive applications. They help create innovative lighting concepts that enhance a vehicle's looks. Companies are working together to develop technological LED products for the automobile industry. For instance, ams OSRAM and TactoTek collaborated to create a demonstrator in September 2022 that featured an avant-garde RGB side-looker LED OSIRE E5515. It can be easily incorporated into the interior of a car to create a more compact design. Such innovations and future investments in automotive LED lights will drive the market during the forecast period.

Growing demand for EVs drives the market growth

- Despite the COVID-19 pandemic and the ensuing supply chain constraints, the electric vehicle (EV) market has grown significantly in China. EV sales are continuing to increase rapidly despite recent obstacles and rising production costs due to rising raw material prices. China had around 1.6 million EV charging stations and 5.21 million charging points at the end of 2022, including over 2.59 million built in 2022. Furthermore, by 2022, the country had 1,973 battery swapping stations, including 675 built in 2022, adding that China has over 10,000 power battery recycling service outlets. Thus, the rapid growth in charging facilities indicates the booming new energy vehicle (NEV) sector in the country.

- China is set to extend EV tax incentives as sales growth slows. The purchase tax break for EVs and plug-in hybrids costs less than CNY 300,000 (USD 42062.76) (CNY 195,000 (USD 27340.03)). Vehicles over that amount are broadly classed as luxury vehicles in China, making it easier for people to buy more affordable, clean cars. These factors would boost the nation's EV adoption rate and further its goal of reaching net zero emissions by 2060.

- In May 2023, Rogers announced the construction of a new factory in China to produce its power substrates to serve both its local and international clients better and to meet the rising demand for power substrates used in electric and hybrid electric vehicles (EVs/HEVs) and renewable energy applications. The expansion's first phase is expected to be finished in 2025. Automobile manufacturers are racing to develop and produce new energy vehicles because of the growing demand for EVs, which boosts the demand for automotive LEDs. LED car lights can help EVs save energy and extend their driving range, as they consume less power than halogen bulbs.

China Automotive LED Lighting Industry Overview

The China Automotive LED Lighting Market is fragmented, with the top five companies occupying 35.95%. The major players in this market are HELLA GmbH & Co. KGaA (FORVIA), KOITO MANUFACTURING CO., LTD., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 China

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Changzhou Xingyu Automotive Lighting System Co, Ltd.

- 6.4.2 Hasco Vision Technology Co., Ltd.

- 6.4.3 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.4 HYUNDAI MOBIS

- 6.4.5 KOITO MANUFACTURING CO., LTD.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Sunway Autoparts

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms