|

市場調査レポート

商品コード

1683932

アジア太平洋地域の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia Pacific Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 215 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

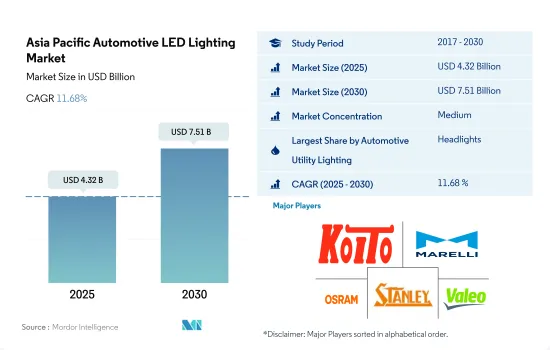

アジア太平洋の自動車用LED照明市場規模は2025年に43億2,000万米ドルと推定され、2030年には75億1,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは11.68%で成長する見込みです。

アジア太平洋地域で事故削減を目的とした自動車用LED照明の技術革新が進み、市場需要を牽引

- 金額シェアでは、2022年にヘッドライトが市場の大半を占め、次いでその他と方向指示灯が続きます。予測期間中、方向指示器と停止灯の市場シェアはほぼ同じで、ヘッドライトの変動は小さいと予想されます。中国は自動車部品製造の主要国であり、予測期間中もその優位性を維持すると予想されます。

- 数量シェアでは、2022年には方向指示灯が大半を占め、次いでヘッドライト、その他となっています。これらのライトの市場シェアは変動が少なく、今後も変わらないと予想されます。Tata、Hyundai、SAIC、Geelyは、LEDプロジェクターライトを今後の自動車に搭載する数少ない主要企業です。事故率の上昇に伴い、LEDフォグランプはより普及すると予想されます。中国、インド、日本などの国々は、LEDランプを自動車に採用することで事故率を下げています。例えば、2017年には合計4,64,910件の交通事故が発生したが、2021年には4,12,432件まで減少しました。このように、車両にLEDランプを使用することで、各国の交通事故による死傷者数を減らすことが期待されます。

- さらに、LEDは自動車の外観を向上させる革新的な照明コンセプトの開発にも貢献しています。各企業は協力して、自動車産業向けの技術的なLED製品を開発しています。例えば、2022年9月、amsオスラムとTactoTekは、前衛的なOSIRE E5515サイドビューRGB LEDを搭載したデモンストレーターの開発における協業を発表しました。車室内に簡単に組み込むことができ、よりコンパクトなデザインになります。自動車用LED照明に対するこのような技術革新と将来の投資は、予測期間中に市場を牽引すると予想されます。

韓国、中国、インド、その他アジア太平洋の主要国におけるEVの成長がLED照明の売上を押し上げると思われます。

- 金額シェアでは、2022年のアジア太平洋自動車用LED照明市場で中国が大半のシェアを占め、日本、インドがこれに続きます。中国の市場シェアは、製造業セクターの成長と国全体の自動車産業における技術革新の増加により、2030年には増加すると予想されます。インドの市場シェアも、国内の自動車企業の大半がEVに投資しており、EVの成長を支援する政府のイニシアチブも高まっていることから、拡大が見込まれます。

- 台数シェアでは、中国が2022年の市場シェアの大半を占め、インド、日本、その他アジア太平洋地域が続きます。韓国は数量シェアで最も低く、予測期間を通じて少数派にとどまると予想されます。中国は世界のその他の地域の輸出入ハブであり、主要な半導体製造業が立地しています。2019年、中国は2,600万台以上の自動車を生産し、その大半は各国に輸出されました。

- 韓国では、2022年の販売台数は2021年に比べて減少しました。これは地政学的問題により中国とロシアでの販売が弱まったためです。しかし、同国ではEVを推進する政府子会社が増加しており、EV自動車産業は今後数年で成長すると予想されます。

- 2021年の電気自動車販売台数の増加は主に中国が牽引し、成長の半分を占めました。このように、EV全体の成長は、LED技術革新の高まりと物流部門の成長とともに、自動車産業におけるLED全体の成長を世界的に高めると予想されます。

アジア太平洋自動車用LED照明市場動向

より多くの電気自動車を販売するためのEVインセンティブの増加がLED市場の成長を牽引

- アジア太平洋地域の自動車総生産台数は、2022年には1億429万台であり、2023年には1億965万台に達すると予測されています。COVID-19の流行はアジア太平洋の自動車市場に大きな影響を与えました。例えば、2019年3月と比較して、ニュージーランドの自動車・商用車販売台数は37%減少しました。2020年3月23日には、ホンダやインダス・モーターといった自動車メーカーがパキスタンでの生産を停止しました。残りのアジア太平洋諸国も同様の状況に陥りました。その結果、COVID-19パンデミックの間、自動車産業におけるLEDの需要は全体的に減少しました。

- TATA Motors、Mahindra &Mahindra、SAIC Motor、吉利汽車、長城汽車、奇瑞汽車、トヨタなどがこの地域の主要自動車メーカーです。これらの企業はすべて、EVの生産に力を入れるようになっています。アジア太平洋では、自動車の技術革新が急速に進んでおり、2022年には中国だけで世界のEV販売台数の約65%を占めると予想されています。LEDはその効率性から、EVでの使用が増えると予測されています。例えば、EVにLEDを搭載すると、バッテリーの消費電流が減少するため、1回の充電で航続距離が6マイルも延びる可能性があります。

- 電気自動車(EV)は、内燃エンジンの代わりに電気モーターを搭載した自動車であり、LEDカーライトと互換性があります。環境へのメリット、ランニングコストの低減、技術の進歩により、EVはこの地域で成長しています。LEDカーライトは最大10,000時間使用できるため、環境への影響を軽減できます。自動車産業におけるLEDライトの数多くの利点により、LEDの需要と成長は予想される期間で増加すると思われます。

バッテリー交換ステーション、バッテリーリサイクルサービス店舗、EV補助金の急成長がLED市場を牽引

- アジア太平洋地域最大の自動車市場である中国は、高性能EVの地域最大の市場でもあり、次いで日本です。アジア太平洋地域の排ガス規制とハイブリッド車・電気自動車への補助金が、電気自動車・ハイブリッド車市場全体のかなりのシェアを獲得するのに役立ちました。中国には、2022年末時点でEV充電ステーションが約160万カ所、充電ポイントが521万カ所(2022年に建設された259万カ所以上を含む)あります。中国は10年以上にわたり、消費者への手厚いインセンティブと自動車メーカーへの補助金でEV産業を推進してきました。例えば、EV購入者は一時期約6万人民元の割引を受けていたが、2022年に終了しました。

- 2022年現在、日本には28,546カ所の充電ステーションがあります。2022年度に日本で販売された輸入電気自動車の台数は、前年比65%増の1万6,464台と過去最高を記録しました。日本で新たに販売された乗用車は361万台で、2022年度中に約7万7,000台がEVでした。インドでは2023年3月までに6586カ所の公共充電ステーション(PCS)が稼働しています。さらに政府は、FAME-II、PLI SCHEME、バッテリースイッチング政策、EV減税などの資本補助金を提供することで、EV充電ステーションの設置を促進しています。2019年4月には、50万台のE-3輪車、7,000台のE-バス、5万5,000台のE-乗用車、100万台のE-2輪車を支援するため、10,000カロールインドルピー(12億米ドル)の予算でFAME II計画が導入されました。その目的は、インドにおける電気自動車の普及を促進することでした。この計画は2022年に終了する予定でした。このように、上記の事例は、発展途上国全体のEV需要の高まりによる新しい発電所の開発と生産につながり、自動車用LEDの需要を押し上げます。

アジア太平洋自動車用LED照明産業概要

アジア太平洋の自動車用LED照明市場は適度に統合されており、上位5社で56.82%を占めています。この市場の主要企業は以下の通りです。KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH., Stanley Electric and Valeo(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- 中国

- インド

- 日本

- 韓国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

- デイタイム・ランニング・ライト(DRL)

- 方向指示灯

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

- 国名

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- GRUPO ANTOLIN IRAUSA, S.A.

- HELLA GmbH & Co. KGaA(FORVIA)

- Hyundai Mobis

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Stanley Electric Co., Ltd.

- Uno Minda Limited

- Valeo

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia Pacific Automotive LED Lighting Market size is estimated at 4.32 billion USD in 2025, and is expected to reach 7.51 billion USD by 2030, growing at a CAGR of 11.68% during the forecast period (2025-2030).

Increasing innovations in LED lighting in automobiles to reduce accidents in Asia-Pacific drive the market demand

- In terms of value share, in 2022, headlights accounted for the majority of the market, followed by others and directional signal lights. The market share is expected to remain almost the same for directional signal lights and stop lights during the forecast period, with a small variation in headlights. China is the major country in terms of manufacturing automotive components, and it is expected to maintain its dominance over the forecasted period.

- In terms of volume share, in 2022, directional signal lights accounted for the majority, followed by headlights and others. The market share is expected to remain the same with less fluctuation for these lights. Tata, Hyundai, SAIC, and Geely are among the few major companies incorporating LED projector lights in their upcoming vehicles. As the accident rate rises, LED fog lamps are expected to become more popular. Countries such as China, India, and Japan have reduced accident rates by using LED lamps in their vehicles. For example, there were a total of 4,64,910 traffic accidents in 2017, but it dropped to 4,12,432 in 2021. Thus, using LED lamps in vehicles is expected to reduce the number of casualties in traffic accidents in countries.

- In addition, LEDs contribute to developing innovative lighting concepts that enhance the appearance of vehicles. Companies work together to develop technical LED products for the automotive industry. For example, in September 2022, ams OSRAM and TactoTek announced their collaboration on the development of a demonstrator featuring the avant-garde OSIRE E5515 side-view RGB LED. It can be easily integrated into the car interior, resulting in a more compact design. Such innovations and future investments in automotive LED lighting are expected to drive the market during the forecast period.

The growth of EVs in South Korea, China, India, and other major countries in Asia-Pacific would boost the sales of LED lights

- In terms of value share, China accounted for the majority of the share of the Asia-Pacific automotive LED lighting market in 2022, followed by Japan and India. The market share is expected to increase for China in 2030 owing to the growth in the manufacturing sector and increasing innovation in automotive industries across the country. The market share of India is also expected to increase as the majority of automotive companies in the country are investing in EVs, and government initiatives to support the growth of EVs are also rising.

- In terms of volume share, China accounted for the majority of the market share in 2022, followed by India, Japan, and the Rest of Asia-Pacific. South Korea has the least volume share, and it is expected to remain in the minority throughout the forecast period. China is the export and import hub for the rest of the world, and major semiconductor manufacturing industries are located in the country. In 2019, China produced more than 26 million vehicles, and the majority of the vehicles were exported to various countries.

- In South Korea, sales were down in 2022 compared to 2021. This was due to weaker sales in China and Russia due to geopolitical issues. However, with rising government subsidiaries to promote EVs in the country, the EV automotive industry is expected to grow in the coming years.

- The increase in electric vehicle sales in 2021 was primarily driven by China, which accounted for half of the growth. Thus, overall EV growth, with rising LED innovation and a growing logistical sector, is expected to increase overall LED growth globally in the automotive industry.

Asia Pacific Automotive LED Lighting Market Trends

Increasing EV incentives to sell more electric vehicles to drive the growth of the LED market

- The total automobile vehicle production in Asia-Pacific was 104.29 million units in 2022, and it was expected to reach 109.65 million units in 2023. The COVID-19 pandemic had a significant effect on the Asia-Pacific automotive market. For instance, compared to March 2019, automotive and commercial vehicle sales in New Zealand were down by 37%. On March 23, 2020, automakers like Honda and Indus Motor stopped producing in Pakistan. The remainder of the Asia-Pacific nations experienced a similar situation. As a result, during the COVID-19 pandemic, the overall demand for LEDs in the automobile industry decreased.

- TATA Motors, Mahindra & Mahindra, SAIC Motor, Geely, Great Wall Motor, Chery, Toyota, and others are major automotive manufacturers in the region. All these companies are increasing their focus on the production of EVs. In Asia-Pacific, automotive innovations are growing rapidly, with China alone expected to account for around 65% of global EV sales in 2022. Due to their efficiency, LEDs are projected to be used more in EVs. For example, when LEDs are fitted on an EV, the decrease in battery current consumption can enhance range by as much as six miles on a single charge.

- Electric vehicles (EVs), automobiles with electric motors instead of internal combustion engines, are compatible with LED car lighting. Due to advantages for the environment, lower running costs, and technological advancements, EVs are growing in the region. Since LED car lights can last up to 10,000 hours, they can reduce environmental impact. The demand for and growth of LEDs will increase in the anticipated term due to the numerous advantages of LED lights in the automobile industry.

Rapid growth of battery swapping station, battery recycling service outlets, and EV subsidies are driving the LED market

- China, the region's largest automobile market, is also the region's largest market for high-performance EVs, followed by Japan. The Asia-Pacific region's emission regulations and subsidies for hybrid and electric vehicles aided it in capturing a sizable share of the overall electric and hybrid vehicle market. China had around 1.6 million EV charging stations and 5.21 million charging points at the end of 2022, including over 2.59 million that were built in 2022. China has been promoting its EV industry for more than a decade with generous incentives to consumers and subsidies to automakers. For instance, buyers received discounts of around CNY 60,000 at one point for purchasing EVs, but those ended in 2022.

- As of 2022, there were 28,546 charging stations in Japan. The number of imported electric vehicles sold in Japan during FY 2022 rose 65% from a year earlier to a record 16,464 units. There were 3.61 million passenger cars newly sold in Japan, and about 77,000 were EVs during FY 2022. By March 2023, there were 6586 public charging stations (PCS) operational in India. Furthermore, the government is promoting the installation of EV charging stations by providing capital subsidies, including FAME-II, PLI SCHEME, Battery Switching Policy, and Tax Reduction on EVs. In April 2019, the FAME II plan was introduced with an INR 10,000 crore (USD 1.2 billion) budget to support 500,000 e-three-wheelers, 7,000 e-buses, 55,000 e-passenger vehicles, and a million e-two-wheelers. The purpose was to encourage electric vehicle adoption in India. The plan was supposed to end in 2022. Thus, the above instances lead to the development and production of new power stations due to the growing demand for EVs across developing nations, which boosts the demand for automotive LEDs.

Asia Pacific Automotive LED Lighting Industry Overview

The Asia Pacific Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 56.82%. The major players in this market are KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 China

- 4.11.2 India

- 4.11.3 Japan

- 4.11.4 South Korea

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Country

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Uno Minda Limited

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms