|

市場調査レポート

商品コード

1683950

インドの自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)India Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 188 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

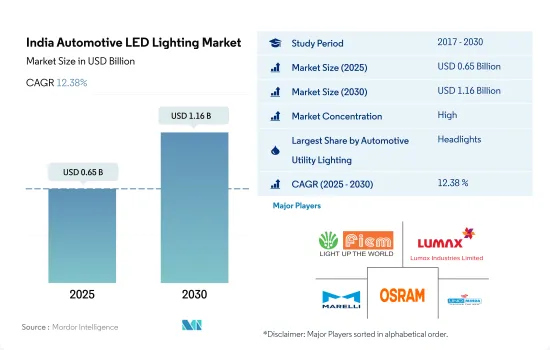

インドの自動車用LED照明市場規模は、2025年に6億5,000万米ドルと推定され、2030年には11億6,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは12.38%で成長します。

市場金額ではヘッドライトが最も高いシェアを占める見込み

- 2017年の金額シェアでは、ヘッドライトが過半数を占め、方向指示灯とDRLがこれに続きます。予測期間中、ヘッドライトとDRLの市場シェアは変わらず、方向指示器用信号灯は若干減少すると予想されます。インドの自動車用照明市場の最大の動向は、前照灯にプロジェクター・ライト付きのDRL(昼間走行用ランプ)を追加することです。Tata、Hyundai、Mahindraは、今後の自動車にLEDプロジェクターライトを統合する数少ない人気のある例です。フォグLEDランプの普及率は、事故動向の増加とともに上昇すると予想されます。雨天、霧、ひょう・みぞれなどの悪天候下での事故は、2021年の交通事故全体の16.8%を占め、前年比12.6%増加しました。

- 数量シェアでは、2017年は方向指示器用信号灯が過半数を占め、ヘッドライト、ストップライトと続きます。これらのライトの市場シェアは変動が少なく、今後も変わらないと予想されます。方向指示灯は、あらゆる車種において軽微な事故から大きな事故まで影響を受ける確率が高く、交換が必要な主要部品です。2017年には合計4,64,910件の交通事故が発生したが、2021年には4,12,432件に減少しました。これは、方向指示信号灯の数量が年々減少していることも示しています。

- 拡張と革新の面では、2022年9月、Marelliは南インドのBangaloreに新しい技術研究開発センターを発足させ、エレクトロニクス用機械設計シミュレーションにおける同社の革新能力を高め、自動車用照明製品に向けて前進しています。

インドの自動車用LED照明市場動向

国産自動車ブランドが経済的な乗用車と商用車を推進

- インドの自動車生産台数は、2022年に2,747万台となり、2023年には2,906万台に達すると予想されています。COVID-19の発生は自動車産業全体の経営に影響を与えました。2020年4月、自動車産業は完全に停止し、販売も記録されませんでした。販売は2020年5月に開始されたが、それでも2019年の同時点をはるかに下回っていました。インド自動車工業会(SIAM)の計算によると、この操業停止の決定により、1日あたり2,300カロールインドルピー(2億7,707万米ドル)の生産損失が生じた。しかし、市場は2021年に回復し、予測期間を通じてプラス成長が見込まれます。

- TATA Motors、Mahindra &Mahindra、Ashok Leyland Ltd、Maruti Suzuki、Bajaj Auto Ltdなどがインドのトップ自動車メーカーです。インドの自動車産業は拡大しており、代替燃料を重視し、環境に優しい燃料で車両経済性を向上させています。例えば、タタ・モーターズは、スマートシティにおける現在と将来の旅客輸送ニーズを満たすため、代替燃料で駆動する乗用車、スターバス電気バスを発表しました。LED照明の省エネ性能と高ルーメン出力により、車両への採用が進んでいます。

- 自動車の照明は、依然として重要な要素です。照明は車両の内外装の美観を高めると同時に、車両の安全性にも貢献します。例えば、2021年9月、インドでは50社以上の企業がLEDなどの生産連動型奨励金の申請書を提出し、6,000カロールインドルピー(7億2,200万米ドル)の投資額が提案されました。企業や政府によるこのような投資は、インドにおけるLED照明の全体的な普及を促進すると予想されます。

政府の政策が充電ステーション網の拡大に貢献

- 現在、インドは発展段階にあります。2023年3月までに国内で稼働している公共充電ステーション(PCS)は6,586カ所です。インド政府は一貫して、電気自動車向けのイニシアチブを導入することで、インドをEV産業の重要なプレーヤーの1つに確立するというコミットメントを示しています。

- インドが発展するにつれて、電気自動車産業も急成長しており、100%直接投資、新しい製造工場、充電インフラ整備の推進が可能になっています。政府は、FAME-II、PLI SCHEME、バッテリー交換政策、電気モビリティ特区、EV減税などの資本補助金を提供することで、EV充電ステーションの設置を促進しています。2019年4月には、50万台のE-3輪車、7,000台のE-バス、5万5,000台のE-乗用車、100万台のE-2輪車を支援するため、12億465万米ドルの予算でFAME II計画が導入されました。その目的は、インドにおける電気自動車の普及を促進することでした。この計画は2022年に終了する予定でした。2021年9月には、電気自動車と水素燃料電池車の製造を増やすための自動車セクター向けPLIスキーム(生産連動型インセンティブ・スキーム)が閣議決定されました。

- さらに、PLIスキームの付加価値として、LED照明市場への投資は40%から75%程度になると予想されます。これにより、もともとインドで製造されていなかった部品やサブアセンブリの製造も行われることになります。政府によるこのような投資は、車載用LEDを含むインドのLED照明市場全体を牽引すると予想されます。また、インドにおけるEV需要のさらなる拡大は、EV充電インフラの需要を押し上げ、予測期間中に自動車用LEDのニーズを生み出すと予想されます。

インドの自動車用LED照明産業の概要

インドの自動車用LED照明市場はかなり統合されており、上位5社で80.99%を占めています。この市場の主要企業は以下の通りです。自動車用LED照明Fiem Industries Ltd., Lumax Industries, Marelli Holdings, OSRAM GmbH. and Uno Minda Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

- デイタイム・ランニング・ライト(DRL)

- 方向指示器

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Fiem Industries Ltd.

- HELLA GmbH & Co. KGaA

- HYUNDAI MOBIS

- Lumax Industries

- Marelli Holdings Co., Ltd.

- Neolite ZKW Lightings Pvt. Ltd

- OSRAM GmbH.

- Uno Minda Limited

- Valeo

- Varroc Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The India Automotive LED Lighting Market size is estimated at 0.65 billion USD in 2025, and is expected to reach 1.16 billion USD by 2030, growing at a CAGR of 12.38% during the forecast period (2025-2030).

Headlights are expected to hold the highest share by market value

- In terms of value share, in 2017, headlights accounted for the majority, followed by directional signal lights and DRL. The market share is expected to remain the same for headlights and DRL during the forecast period, with a small reduction in directional signal lights. The biggest trend in India's automotive lighting market is the addition of DRLs (daytime running lamps) with projector lights in frontal lighting. Tata, Hyundai, and Mahindra are among the few popular examples of integrating LED projector lights in upcoming vehicles. The fog LED lamp penetration rate is expected to increase with increasing accident trends. Accidents under adverse weather conditions such as rainy, foggy, and hail/sleet accounted for 16.8% of total road accidents in 2021, an increase of 12.6% from the prior year.

- In terms of volume share, in 2017, directional signal lights accounted for the majority, followed by headlights and stoplights. The market share is expected to remain the same with less fluctuation for these lights. Directional signal lights are the prime part with a high probability of getting affected in minor to major accidents in all types of vehicles and require replacement. In 2017, a total of 4,64,910 road accidents occurred, while in 2021, it decreased to 4,12,432. This also indicated the decrease in the volume of directional signal light every year.

- In terms of expansion and innovations, in September 2022, Marelli inaugurated its new Technical R&D Center in Bangalore, South India, boosting the company's innovation capability in Mechanical Design Simulations for Electronics and moving forward for automotive lighting products.

India Automotive LED Lighting Market Trends

Homegrown automotive brands are promoting economical passenger and commercial vehicles

- The total automobile vehicle production in India stood at 27.47 million units in 2022, and it was expected to reach 29.06 million units in 2023. The COVID-19 outbreak impacted the auto industry's entire operations. In April 2020, the auto industry was completely shut down, and no sales were recorded. Sales started in May 2020, but even then, they were far lower than they had been at the same point in 2019. According to a calculation by the Society of Indian Automobile Manufacturers (SIAM), the shutdown decision caused a daily output loss of INR 2,300 crore (USD 277.07 million). However, the market rebounded in 2021, and it is projected to witness positive growth throughout the forecast period.

- TATA Motors, Mahindra & Mahindra, Ashok Leyland Ltd, Maruti Suzuki, and Bajaj Auto Ltd, among others, are the country's top automakers. India's automotive industry is expanding, with businesses emphasizing alternative fuels and improving the vehicle economy with eco-friendly fuels. For instance, Tata Motors introduced the Starbus Electric Bus, a passenger vehicle driven by alternative fuels, to satisfy the present and future passenger transportation needs in smart cities. Due to the energy-saving capabilities and high-lumen output of LED lights, they are being increasingly adopted in vehicles.

- Vehicle lighting is still a crucial component. Lighting enhances the aesthetic appeal of a vehicle's interior and exterior while contributing to vehicle safety. For instance, in September 2021, more than 50 companies in India submitted applications for production-linked incentives for LEDs and other products, with a proposed investment of INR 6,000 crores (USD 722 million). Such investments by companies and the government are expected to drive the overall adoption of LED lighting in India.

Government policies are helping extend the network of charging stations

- Currently, India is in its developing phase. By March 2023, there were 6,586 public charging stations (PCS) operational in the country. The Government of India consistently demonstrates its commitment to establishing India as one of the significant players in the EV industry by introducing initiatives for electric vehicles.

- As India is developing, the electric vehicle industry is also picking pace, with the possibility of 100% FDI, new manufacturing plants, and an increased push to improve charging infrastructure. The government is promoting the installation of EV charging stations by providing capital subsidies, including FAME-II, PLI SCHEME, Battery Switching Policy, Special Electric Mobility Zone, and tax reduction on EVs. In April 2019, the FAME II plan was introduced with an USD 1204.65 million budget to support 500,000 e-three-wheelers, 7,000 e-buses, 55,000 e-passenger vehicles, and a million e-two-wheelers. The purpose was to encourage electric vehicle adoption in India. The plan was supposed to end in 2022. In September 2021, a PLI Scheme, or Production-Linked Incentive Scheme, for the automotive sector was approved by the Cabinet to increase the manufacturing of electric and hydrogen fuel cell vehicles.

- Additionally, as a value addition under the PLI scheme, investments in the LED lighting market are expected to be around 40% to 75%. This would also result in the manufacturing of components or sub-assemblies that were originally not manufactured in India. Such investments by the government are expected to drive the overall LED lighting market in India, including automotive LEDs. Further growing demand for EVs in India is expected to boost the demand for EV charging infrastructure, which would also create the need for automotive LEDs during the forecast period.

India Automotive LED Lighting Industry Overview

The India Automotive LED Lighting Market is fairly consolidated, with the top five companies occupying 80.99%. The major players in this market are Fiem Industries Ltd., Lumax Industries, Marelli Holdings Co., Ltd., OSRAM GmbH. and Uno Minda Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 India

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Fiem Industries Ltd.

- 6.4.2 HELLA GmbH & Co. KGaA

- 6.4.3 HYUNDAI MOBIS

- 6.4.4 Lumax Industries

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Neolite ZKW Lightings Pvt. Ltd

- 6.4.7 OSRAM GmbH.

- 6.4.8 Uno Minda Limited

- 6.4.9 Valeo

- 6.4.10 Varroc Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms