北米の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 196 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683961

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

北米の自動車用LED照明市場規模は、2025年に21億8,000万米ドルと推定され、2030年には30億4,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは6.84%で成長します。

事故動向の高まり、フォグLEDランプの普及率、電気自動車の販売増加が市場成長を牽引

- 金額ベースでは、2022年にヘッドライトが大きなシェアを占め、次いでその他(小型LEDライト、LEDナンバープレートライト、フォグランプ、室内LEDライト)、方向指示灯(DSL)、昼間走行用ライト、ストップランプが続きます。市場シェアはすべてのライトで横ばい、その他とDSLは若干減少、ヘッドライトは伸びると予想されます。事故動向の上昇に伴い、フォグLEDランプの普及率も上昇すると予想されます。米国では、自動車事故による死亡者数が2022年にはパンデミック前の死亡率に比べ推定4万6,000人に達し、22%近く増加します。

- 数量ベースでは、2022年に方向指示灯が大きなシェアを占め、次いでヘッドライト、その他(小型LEDライト、LEDナンバープレートライト、フォグランプ、室内LEDライト)、ストップランプの順となっています。外灯は、あらゆるタイプの自動車において、軽微な事故から大きな事故まで影響を受ける確率が高く、交換が必要な主要部品です。

- 2022年の軽自動車新車販売台数は1,370万台に達しました。2022年の新車販売台数は前年比8.2%減となったが、これは主にマイクロチップ不足の継続とさらなるサプライチェーンの混乱によるものです。2022年の全新車販売台数に占めるハイブリッド車、プラグインハイブリッド車、バッテリー電気自動車(BEV)の割合は12.3%となり、2021年から2.7%増加しました。このように、自動車販売台数の増加により、LED照明の需要が増加しました。

新興諸国におけるEVの開発と地域の自動車産業を発展させる有利な法律がLED照明の需要を促進

- 金額ベースでは、2022年に米国のLED照明市場がシェアの大半を占め、次いで北米地域(RONA)が続きます。市場シェアは、米国が減少し、北米その他が増加すると予想され、今後数年間は変動が少ないです。米国の国内自動車生産台数は、2021年の910万台から2022年には1,006万台に増加します。自動車生産には乗用車と商用車が含まれます。カナダでは、2022年の自動車生産台数は2021年比で10.2%増加し、120万台となりました。国内自動車生産台数の増加は、市場に自動車用LEDの需要増をもたらします。

- EVの需要は北米の多くの国で伸びた。メキシコの2022年の新車販売台数は108万台で、2021年から7%改善し、米国のEV販売台数は2022年に65%増加しました。

- 自動車産業のサブセクターでは、米国とメキシコの商業サービスは、OE部品、アフターマーケット、電気自動車(EV)部品で力強い機会を経験しました。メキシコのOEMおよびアフターマーケット向け自動車部品の生産額は、2020年の784億米ドルから2021年には947億米ドルに増加し、2022年には1,010億米ドル以上に達すると予想されます。

- 米国・メキシコ・カナダ協定(USMCA)は2020年7月1日に発効しました。USMCAの要件は、自動車の内容物の75%を北米で生産し、中核となる自動車部品は米国、カナダ、メキシコのいずれかを原産地とすることです。EVの採用や現地の自動車産業を発展させるための有利な法律など、上記の要因を考慮すると、今後数年間、北米全域でLEDの成長が期待されます。

北米自動車用LED照明市場動向

LED市場を牽引するのはEVとバッテリーメーカーによる自動車生産台数増加のための投資

- 北米の自動車総生産台数は2022年に1,454万台、2023年には1,506万台に達すると予想されています。北米における最大の製造部門のひとつが自動車部門です。しかし、COVID-19パンデミックは、この地域の自動車産業に2つの大きな衝撃を与え、2020年と2021年の生産、販売、対外貿易に大きな悪影響を及ぼしました。このように、自動車のサプライチェーンと生産の混乱は、この地域のLED照明事業にマイナスの影響を与えました。

- 3月の米国の軽自動車生産台数は前年同月比で31%近く減少しました。4月末に1週間稼働した工場は1つだけであったため、より高いレベルの軽自動車生産が必要でした。自動車業界からは、供給網に関する懸念の声も上がりました。ドイツのサプライヤーであるZFは米国に施設を有しており、2020年5月末までに全世界の雇用を10%削減する計画を明らかにしました。世界のサプライチェーンの混乱が米国の製造に影響を与えた:メルセデス・ベンツはアラバマ州バンス工場を4月27日に再開したが、部品不足のため、5月15日に生産を一時停止せざるを得なくなりました。この混乱は、自動車産業で使用される半導体に落ち込みをもたらしました。

- さらに、北米では政府主導でEV需要が急増しています。インフレ削減法が2022年8月に成立し、その時点から2023年3月までの間に、主要なEVおよび電池メーカーが北米のEVサプライチェーンへの少なくとも520億米ドル相当の投資を発表しました。このような消費者とメーカーの利益につながる取り組みは、同地域のLED照明事業を後押しすると思われます。

電気自動車の販売とLED照明の成長を促進する政府投資

- 北米地域におけるEV販売の大部分は米国、カナダ、メキシコからもたらされています。2022年、米国のBEV販売台数は2021年比で65%増加し、テスラがEV市場を独占し続けています。2022年のメキシコの販売台数は、総販売台数109万台のうち完全電気自動車はわずか0.5%で、この割合は中国、欧州、米国など他の市場を大きく下回っています。カナダでは、2022年第4四半期にバッテリー電気自動車(BEV)だけで2万7,754台、プラグインハイブリッド電気自動車(PHEV)で5,645台の新規登録がありました。

- さらに拡大するために、米国政府は2021年に1兆ドル規模のインフラ法案を発表し、2030年までに公共EV充電器を50万台増設するために75億米ドルを割り当て、また米国内で組み立てられたEVを購入すると7,500米ドルの税制優遇を提供することで、EV製造への投資を行いました。また、EVの主要企業の1つであるテスラは、2024年末までに米国で約3,500カ所のスーパーチャージャーステーションと4,000カ所のレベル2充電ドックを、すべてのブランドの電気自動車に提供することを約束しました。

- GMカナダは、インガソールとオシャワの製造施設を改造するためにカナダに20億米ドル以上を投資し、2022年末までに電気自動車を生産する予定です。2030年までに、米国ではジョージア州、ケンタッキー州、ミシガン州が電気自動車用バッテリー製造の大半を占めると予想されています。この電気自動車用バッテリー製造能力は、年間1,000万~1,300万個の全電気自動車用バッテリーの生産を促進し、米国を世界のEV競争相手として位置づけると思われます。このように、上記のような事例は、EVの需要増加による新しい発電所の開発と生産につながり、この地域の自動車用LEDの需要を押し上げます。

北米の自動車用LED照明産業概要

北米の自動車用LED照明市場は適度に統合されており、上位5社で52.69%を占めています。この市場の主要企業は以下の通りです。GRUPO ANTOLIN IRAUSA, S.A., KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH. and Stanley Electric(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

- 日中走行用ライト(DRL)

- 方向指示器

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

- 国名

- 米国

- その他北米地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- GRUPO ANTOLIN IRAUSA, S.A.

- HELLA GmbH & Co. KGaA(FORVIA)

- Hyundai Mobis

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Stanley Electric Co., Ltd.

- Valeo

- ZKW Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

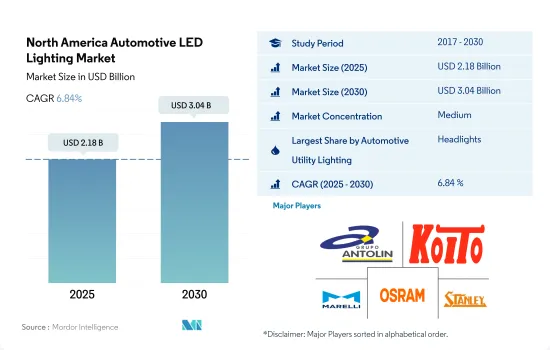

The North America Automotive LED Lighting Market size is estimated at 2.18 billion USD in 2025, and is expected to reach 3.04 billion USD by 2030, growing at a CAGR of 6.84% during the forecast period (2025-2030).

Rising accident trend, penetration rate of fog LED lamps, and increasing sales of electric vehicles drive market growth

- In terms of value, in 2022, headlights accounted for a major share, followed by others (miniature LED lights, LED license plate lights, fog lights, and interior LED lights), directional signal lights (DSLs), daytime running lights, and stop lights. The market share is expected to remain the same for all lights, with a small reduction in others and DSLs, and grow for headlights. With the rising accident trend, the penetration rate of fog LED lamps is anticipated to rise. In the US, the number of motor vehicle deaths reached an estimated 46,000 in 2022 compared to the pre-pandemic death rate, an increase of nearly 22%.

- In terms of volume, in 2022, directional signal lights accounted for a major share, followed by headlights, others (miniature LED lights, LED license plate lights, fog lights, and interior LED lights), and stop lights. External lights are the prime parts that have a high probability of getting affected in minor to major accidents in all types of vehicles and require replacement.

- The year 2022 ended with new light-vehicle sales reaching 13.7 million units. The Y-o-Y 2022 sales decreased by 8.2% compared to 2021, with the decrease primarily attributed to the ongoing microchip shortage and additional supply chain disruptions. With sales of hybrid, plug-in hybrid, and battery electric vehicles (BEVs) accounting for 12.3% of all new vehicle sales in 2022, an increase of 2.7% from 2021, alternative fuel vehicles gained market share. Thus, the increase in vehicle sales resulted in an increase in the requirement for LED lights.

Adoption of EVs across countries and favorable laws to develop local automotive industry drive the demand for LED lighting

- In terms of value, in 2022, the US LED light market accounted for the majority of the share, followed by the Rest of North America (RONA). The market share is expected to decline for the US and increase for the Rest of North America, with less fluctuation in the coming years. The domestic vehicle production in the US increased from 9.1 million units in 2021 to 10.06 million units in 2022. The vehicle production includes cars and commercial vehicles. In Canada, in 2022, vehicle production increased by 10.2% compared to 2021, accounting for 1.2 million units. The increase in domestic vehicle production creates more demand for automotive LEDs in the market.

- The demand for EVs grew across many countries in North America. Mexico saw 1.08 million new car sales in 2022, a 7% improvement from 2021, and US EV sales increased by 65% in 2022.

- In sub-sectors of the automotive industry, the US and Mexican commercial services experienced strong opportunities in OE parts, aftermarket, and electric vehicle (EV) parts. The value of Mexican automotive parts for OEMs and aftermarket production increased from USD 78.4 billion in 2020 to USD 94.7 billion in 2021, and it is expected to reach more than USD 101 billion by 2022.

- The United States, Mexico, Canada Agreement (USMCA) went into effect on July 1, 2020. The USMCA requirement stated that 75% of a vehicle's content must be produced in North America and that core auto parts originate from the United States, Canada, or Mexico. Considering the above-mentioned factors, such as the adoption of EVs and favorable laws to develop the local automotive industry, the growth of LEDs is expected across North America in the coming years.

North America Automotive LED Lighting Market Trends

The LED market is driven by investments by EVs and battery producers to increase automotive production

- The total automobile vehicle production in North America was 14.54 million units in 2022, and it is expected to reach 15.06 million units in 2023. One of the biggest manufacturing sectors in North America is the automotive sector. However, the COVID-19 pandemic caused two significant shocks to the region's automobile industry, which had a significant negative impact on production, sales, and foreign trade in 2020 and 2021. Thus, the disruption in the supply chain and production of automotive vehicles negatively affected the LED lighting business in the region.

- March saw an almost 31% year-over-year fall in the US light car production. Only one plant was operating for one week at the end of April, so there needed to be a higher level of light vehicle production. The auto industry also voiced concerns regarding its supply networks. ZF, a German supplier, has facilities in the United States and revealed plans to reduce its global employment by 10% by the end of May 2020. Several worldwide supply chain disruptions impacted manufacturing in the United States: Mercedes-Benz resumed its Vance, Alabama, facility on April 27; however, due to a scarcity of parts, production had to be briefly halted on May 15. This disruption created a downfall in semiconductors used in the automotive industry.

- Further, the demand for EVs is rapidly increasing in North America due to government initiatives. The Inflation Reduction Act was passed in August 2022, and between that time and March 2023, major EV and battery producers announced investments in North American EV supply chains worth at least USD 52 billion. Such initiatives in the interest of consumers and manufacturers will boost the LED lighting business in the region.

Government investments to drive the sales of electric vehicle and propel the growth of LED lighting

- Most of the EV sales in the North American region come from the US, Canada, and Mexico. In 2022, US BEV sales increased by 65% compared to 2021, and Tesla continues to dominate the EV market. In 2022, Mexico sales were only 0.5% of 1,090,000 total vehicle sales were fully electric, a percentage that falls well below other markets, such as China, Europe, and the United States. In Canada, during Q4 2022, battery electric vehicles (BEVs) alone had 27,754 new registrations, and plug-in hybrid electric vehicles (PHEVs) had 5,645 new registrations.

- To expand further, the US government issued a trillion-dollar infrastructure bill in 2021 that allocates USD 7.5 billion toward building 500,000 more public EV chargers by 2030 and also made investments in EV manufacturing by providing tax benefits of USD 7,500 for purchasing an EV assembled in the US. Also, Tesla, one of the significant players in EVs, committed to delivering around 3,500 of its US Supercharger stations and 4,000 Level 2 charging docks available to all brands of electric vehicles by the end of 2024.

- GM Canada invested more than USD 2 billion in Canada to transform manufacturing facilities in Ingersoll and Oshawa and expects electric vehicle production by the end of 2022. By 2030, Georgia, Kentucky, and Michigan are expected to dominate electric vehicle battery manufacturing in the United States. This EV battery manufacturing capacity will facilitate the production of 10 to 13 million batteries for all-electric vehicles per year, positioning the United States as a global EV competitor. Thus, the above instances lead to the development and production of new power stations because of the growing demand for EVs, which boosts the demand for automotive LEDs in the region.

North America Automotive LED Lighting Industry Overview

The North America Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 52.69%. The major players in this market are GRUPO ANTOLIN IRAUSA, S.A., KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 United States

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Country

- 5.3.1 United States

- 5.3.2 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Valeo

- 6.4.10 ZKW Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 196 Pages

- 納期

- 2~3営業日