英国のプラスチック包装フィルム:市場シェア分析、産業動向、成長予測(2024年~2029年)

United Kingdom Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550278

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

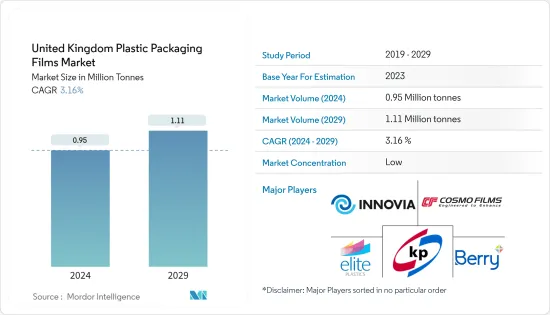

英国のプラスチック包装フィルム市場規模は2024年に95万トンと推定され、2029年には111万トンに達し、予測期間(2024-2029年)のCAGRは3.16%で成長すると予測されます。

主なハイライト

- 高機能フィルムへのニーズの高まりが、英国のプラスチック包装フィルム市場の成長を後押ししています。この市場成長は、食品包装、医薬品、消費財など様々なエンドユーザー産業でバリア要件が高まっていることも背景にあります。加工技術の進歩はプラスチックフィルムの使用を容易にし、生産における適合性とコスト効率を保証します。こうした技術改良により、メーカーは厳しい業界基準を満たし、消費者の進化する需要に応えることができます。

- この地域の消費者は、利便性と食品廃棄物を減らすことへの関心の高まりから、賞味期限の長い製品に惹かれています。プラスチックフィルム包装はその優れたバリア特性により、湿気、酸素、光、その他品質や鮮度を損なう要素から商品を保護します。その結果、飲食品から医薬品、パーソナルケア製品に至るまで、様々な生鮮品の賞味期限を延ばすのに役立っています。さらに、プラスチックフィルム包装は軽量であるため、輸送コストと二酸化炭素排出量を削減し、環境に優しい選択肢となっています。また、プラスチックフィルムの多用途性は、様々な消費者の嗜好や市場の需要に応える革新的なパッケージデザインを可能にします。

- 外出先での消費、世帯数の減少、利便性への要求の高まりは、ますます現代のライフスタイルを定義しています。プラスチックフィルム包装はソリューションであり、軽量で持ち運びができ、リシーラブルという特徴を提供し、これらのライフスタイルに合致しています。シングルサーブやポーションコントロールのフォーマットは、消費者の利便性とポーションコントロールの好みに応え、人気を集めています。さらに、プラスチックフィルム包装の多用途性は、イージーオープン機能や保存期間の延長といった革新的なデザインや機能性を可能にし、消費者や製造業者へのアピールをさらに高めています。

- 英国政府はプラスチック廃棄物を抑制するため、2022年からプラスチック包装税(PPT)を導入しました。この税金は、リサイクル率が30%未満のプラスチック包装を対象としています。この課税は、プラスチック包装を製造する企業に対し、より多くのリサイクル材料を採用するよう強制するもので、埋め立てや焼却に回されるプラスチック廃棄物を削減することを目的としています。2024年4月、この税金は1トン当たり217.85英ポンドに引き上げられます。この税金の収益は、英国のリサイクル・インフラを強化し、プラスチック廃棄物対策に充てられます。これらの規制は市場を再構築する構えで、課題と機会を提示しています。

- 持続可能なプラスチックのクローズドループを確立する上で、リサイクルは極めて重要です。回収、選別技術、革新的なリサイクル方法の進歩により、プラスチックはライフサイクルを通じてその価値を維持することができます。同地域ではリサイクル含有量の目標が義務化されており、廃棄物の削減とリサイクル効率の向上に向けた技術革新と投資の重要性が浮き彫りになっています。

英国のプラスチック包装フィルム市場動向

ポリエチレンセグメントが大きな市場シェアを占める見込み

- ポリエチレンは、その柔軟性、強固な防湿性、シール・ツー・セルフ機能で知られ、パッケージング市場において頼りになる素材です。ポリエチレンは耐久性に優れ、低温下でも優れた性能を発揮します。多くの場合、純粋な形で使用されるか、バリア特性を高めるために他の材料とブレンドされます。特に、その環境に優しい性質が、英国の包装フィルムメーカーの間で人気を博しています。

- PE樹脂の進歩は、バリアフィルムの性能を向上させ、リサイクル可能性の障壁を打ち砕きました。最新のポリエチレン樹脂は、マルチ素材でリサイクル不可能なバリアフィルムをオールPE構造で代用することを許さないです。この構造体はリサイクル可能で、軽量、薄型、耐久性に優れ、加工が容易です。この技術革新は、プラスチック廃棄物を削減し、包装における環境に優しい素材の使用を促進することで、持続可能な取り組みに大きく貢献します。

- 製品の視認性は、消費者の選択を形成する上で極めて重要な役割を果たします。透明包装、特にポリテープフィルムの形態は、多様な産業で需要の高まりを目の当たりにしています。この需要急増の背景には、消費者が購入前に製品を視覚的に評価することを好み、信頼感を醸成して購買意欲を高めていることがあります。その結果、ポリエチレンバリアフィルムの生産者は戦略的に透明性を強調し、市場での存在感を高めています。

- ポリエチレン系包装フィルムの需要は、包装活動の活発化によって飲食品業界で高まっています。透明な包装は、製品の品質と鮮度をアピールする上で極めて重要な役割を果たしています。英国の包装市場の収益は2020年の53億906万米ドルから2023年には55億510万米ドルに増加しました。飲食品、医薬品、消費財などの業界全体で透明包装ソリューションへの嗜好が高まっていることが、主にこの成長を後押ししています。

- ポリエチレンバリアフィルムのリサイクル可能性は、税負担を軽減することでエンドユーザーとメーカーの双方に利益をもたらします。欧州では、リサイクルされていないプラスチックには余分な税金がかかります。さらに、最近の規制では、リサイクル材料が30%未満のプラスチック包装に課税することが義務付けられています。そのため、ポリエチレンバリアフィルムのメーカーは、この地域でこれらの課税を回避することを目指し、持続可能な選択肢を生み出す努力を強めています。

食品と消費者向け製品が市場で大きなシェアを占める見込み

- 英国のプラスチック包装フィルム市場は、急成長する食品産業と民間投資の急増に後押しされて上昇傾向にあります。特に、袋やパウチなどの革新的で完全堆肥化可能なパッケージング・ソリューションの開発が、こうした投資によって進められています。消費者の環境意識が高まるにつれて持続可能な包装オプションへの需要が高まり、市場成長をさらに後押ししています。技術の先進パッケージングは、消費者や規制基準を満たす高品質で柔軟なパッケージングの製造を可能にします。

- 包装のイノベーションは冷凍食品の領域で最も重要です。これらの技術革新は、鮮度を保持し、利用者の利便性を高め、棚の魅力を高めるのに役立ちます。そのためメーカーは、冷凍食品用に特別に設計された特殊なプラスチック包装ソリューションの製造に投資を行っています。この戦略的な動きは、このセグメント特有の需要に対応し、フレキシブルプラスチック包装市場の拡大を後押ししています。

- 英国の食料品小売セクターの市場規模は、2022年の2,696億米ドルから2024年には2,817億米ドルに増加すると予想されています。予測ではさらに急増し、2027年には3,000億米ドルの大台に乗ると予想されています。このような上昇基調は、視認性とリサイクル可能性を原動力とする様々な形態、特にプラスチックフィルムに対する需要の増加により、包装市場を再形成すると予想されます。持続可能で便利な包装ソリューションに対する消費者の嗜好の高まりも、この動向に寄与しています。小売業者は、規制要件や消費者の期待に応えるために革新的な包装技術に投資しており、食料品小売部門における包装市場の成長をさらに促進しています。

- 家庭用品・パーソナルケア市場はこの地域で急成長を遂げており、生産と流通の増加に対応する包装ソリューションが必要とされています。軽量でカスタマイズ可能なデザインで知られるプラスチックフィルム包装は、効率的な包装ソリューションを求める企業にとって最適な選択肢となりつつあります。生活の質の向上、パーソナルケアが自尊心や社会的交流に与えるポジティブな影響、プレミアムブランドや高級ブランドに対する消費者の嗜好の高まりといった要因が、今後数年の市場を牽引していくと思われます。

- 消費者は、高級感のあるパッケージが自慢のパーソナルケア製品や家庭用製品に引き寄せられる傾向が強まっています。このような魅力的で革新的なパッケージは目を引き、購入の意思決定に重要な役割を果たします。美観だけでなく、適切なパーソナルケア用パッケージは、製品を最適な状態に保ち、賞味期限を延ばします。さらに、製品を市場で際立たせる重要な差別化要因でもあります。

英国のプラスチック包装フィルム産業概要

英国のプラスチック包装フィルム市場は断片化されており、Elite Plastics Limited、Innovia Films(CCL Industries Inc.)、Berry Global Inc.、Klockner Pentaplast、Cosmo Filmsなど、複数の世界的・地域的プレーヤーが注目度を競っています。同市場の特徴は、製品の差別化が少ないこと、製品の普及が進んでいること、競合が多いことです。

- 2024年7月:素材開発・製造の大手であるInnovia Filmsは、サステイナブルフィルムのラインナップの拡張を発表しました。この拡張製品「アンコール」は二軸延伸ポリプロピレン(BOPP)フィルムに重点を置き、特に食品に接触する用途に合わせたケミカルリサイクルポリマーの配合に重点を置いています。さらに、Innovia FilmsはPrevented Ocean Plasticと戦略的パートナーシップを結び、POP由来の素材を30%配合した新しいフィルム組成を実現しました。

- 2024年4月ベリー世界のフレキシブル部門は、欧州の3つの重要な施設でリサイクル能力を増強し、再生ポリマーのSustaneラインの生産を強化する欧州全域での取り組みにおいて重要な一歩を踏み出しました。リサイクル素材から作られた高機能フィルムに対する需要の高まりを見据え、ベリー世界はその世界ネットワークを活用してこの事業拡大の陣頭指揮を執る予定です。今回の増強では、ベリーのヒーナー(英国)、シュタインフェルト(ドイツ)、ズジエショヴィツェ(ポーランド)の各拠点に戦略的に配置された最新鋭の設備を導入しました。これにより、ベリーの欧州事業における再生プラスチックの年間生産量は、推定6,600トン増加することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションへの需要の高まり

- 様々な産業におけるプラスチックフィルム需要の増加が成長の可能性を示す

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(PP)(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料・スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他の最終用途(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- Elite Plastics Limited

- Innovia Films(CCL Industries Inc.)

- Berry Global Inc.

- Klockner Pentaplast

- SUDPACK Holding GmbH

- UFlex Europe Ltd

- Cosmo Films

- The Jason Group

- TCL Packaging

- SRF LIMITED

第8章 投資分析

第9章 市場の将来

目次

The United Kingdom Plastic Packaging Films Market size is estimated at 0.95 Million tonnes in 2024, and is expected to reach 1.11 Million tonnes by 2029, growing at a CAGR of 3.16% during the forecast period (2024-2029).

Key Highlights

- The rising need for high-performance films is propelling the growth of the plastic packaging film market in the United Kingdom. This market growth is also driven by heightened barrier requirements across various end-user industries, including food packaging, pharmaceuticals, and consumer goods. Advancements in processing technologies facilitate the use of plastic films, ensuring their suitability and cost efficiency in production. These technological improvements enable manufacturers to meet stringent industry standards and cater to the evolving demands of consumers.

- Consumers in the region gravitate toward products with extended shelf lives, driven by convenience and a growing concern for reducing food waste. With its superior barrier properties, plastic film packaging shields items from moisture, oxygen, light, and other elements that can compromise their quality and freshness. As a result, it is proving instrumental in prolonging the shelf life of a wide array of perishable items, spanning from food and beverages to pharmaceuticals and personal care products. Additionally, the lightweight nature of plastic film packaging reduces transportation costs and carbon emissions, making it an environmentally friendly option. The versatility of plastic film also allows innovative packaging designs that cater to various consumer preferences and market demands.

- On-the-go consumption, smaller households, and rising demand for convenience increasingly define modern lifestyles. Plastic film packaging is a solution, offering lightweight, portable, and resealable features that align with these lifestyles. Single-serve and portion-controlled formats are gaining traction, catering to consumers' convenience and portion-control preferences. Additionally, the versatility of plastic film packaging allows innovative designs and functionalities, such as easy-open features and extended shelf life, further enhancing its appeal to consumers and manufacturers alike.

- The UK government introduced the plastic packaging tax (PPT) to curb plastic waste, effective 2022. This tax targets plastic packaging with less than 30% recycled content. This levy compels companies that produce plastic packaging to adopt more recycled materials, aiming to slash plastic waste destined for landfills or incineration. In April 2024, the tax increased to GBP 217.85 per tonne. The tax's proceeds are earmarked to bolster the UK's recycling infrastructure and combat plastic waste. These regulations are poised to reshape the market, presenting challenges and opportunities.

- Recycling is pivotal in establishing a closed loop for sustainable plastics. Advancements in collection, sorting techniques, and innovative recycling methods ensure that plastic retains its value throughout its lifecycle. As the region has established mandated targets for recycled content, it underscores the importance of innovation and investment in reducing waste and enhancing recycling efficiency.

United Kingdom Plastic Packaging Films Market Trends

The Polyethylene Segment is Expected to Hold a Significant Market Share

- Polyethylene, known for its flexibility, robust moisture barrier, and seal-to-self capability, is a go-to material in the packaging market. It boasts durability and excels even in low temperatures. Often, it is used in its pure form or blended with other materials to enhance its barrier properties. Notably, its eco-friendly nature propels its popularity among packaging film manufacturers in the United Kingdom.

- Advancements in PE resin have enhanced barrier film performance and shattered barriers to recyclability. The newest polyethylene resins do not allow substituting multi-material, non-recyclable barrier films with all-PE structures. The structures are recyclable, lightweight, thin, and durable, making them easy to process. This innovation significantly contributes to sustainability efforts by reducing plastic waste and promoting the use of eco-friendly materials in packaging.

- Product visibility plays a pivotal role in shaping consumer choices. Transparent packaging, particularly in the form of polythene films, is witnessing heightened demand across diverse industries. This surge is fueled by the consumer preference for visually assessing a product before buying, which fosters trust and boosts purchase intent. Consequently, producers of polyethylene barrier films are strategically emphasizing transparency to bolster their market presence.

- The demand for polythene-based packaging films is rising in the food and beverage industry, driven by increased packaging activities. Clear packaging plays a pivotal role in showcasing product quality and freshness. The packaging market's revenue in the United Kingdom increased from USD 5,309.06 million in 2020 to USD 5,505.10 million in 2023. The growing preference for transparent packaging solutions across industries like food and beverage, pharmaceuticals, and consumer goods primarily fuels this growth.

- The recyclability of polyethylene barrier films benefits both end users and manufacturers by reducing tax duties. In Europe, non-recycled plastics incur extra taxes. Moreover, a recent regulation mandates a tax on plastic packaging containing less than 30% recycled material. Consequently, manufacturers of polyethylene barrier films are intensifying efforts to create sustainable options, aiming to sidestep these levies in the region.

Food and Consumer Products are Expected to Hold a Significant Share in the Market

- The plastic packaging film market in the United Kingdom is on the upswing, propelled by a burgeoning food industry and a surge in private investments. Notably, these investments are steering the development of innovative, fully compostable packaging solutions, particularly in bags and pouches. The demand for sustainable packaging options is increasing as consumers become more environmentally conscious, further driving market growth. Technological advancements enable the production of high-quality, flexible packaging that meets consumer and regulatory standards.

- Packaging innovations are paramount in the realm of frozen foods. They help preserve freshness, enhance user convenience, and boost shelf appeal. Consequently, manufacturers are channeling investments into crafting specialized plastic packaging solutions specifically designed for frozen foods. This strategic move caters to the segment's unique demands, propelling the expansion of the flexible plastic packaging market.

- The UK grocery retail sector's value is expected to increase from USD 269.6 billion in 2022 to USD 281.7 billion in 2024. Projections indicate a further surge, with the sector expected to hit the USD 300 billion mark by 2027. This upward trajectory is expected to reshape the packaging market owing to the increasing demand for various modes, notably plastic film, driven by its visibility and recyclability. The increasing consumer preference for sustainable and convenient packaging solutions also contributes to this trend. Retailers are investing in innovative packaging technologies to meet regulatory requirements and consumer expectations, further fueling the growth of the packaging market within the grocery retail sector.

- The household and personal care market is witnessing a surge in the region, necessitating packaging solutions to match the heightened production and distribution. Plastic film packaging, known for its lightweight nature and customizable designs, is becoming the go-to choice for companies seeking efficient packaging solutions. Factors like the enhancement of quality of life, the positive impact of personal care on self-esteem and social interactions, and a growing consumer preference for premium and luxury brands are set to drive the market in the coming years.

- Consumers are increasingly gravitating toward personal care and household products that boast upscale packaging. This attractive and innovative packaging catches the eye and plays a crucial role in influencing purchase decisions. Beyond aesthetics, adequate personal care packaging ensures the product remains in optimal condition, extending its shelf life. Moreover, it is a crucial differentiator, setting products apart in the market.

United Kingdom Plastic Packaging Films Industry Overview

The UK plastic Packaging Films market is fragmented, with several global and regional players, such as Elite Plastics Limited, Innovia Films (CCL Industries Inc.), Berry Global Inc., Klockner Pentaplast, and Cosmo Films, vying for attention. The market is characterized by low product differentiation, growing product penetration, and high competition.

- July 2024: Innovia Films, a leading material developer and producer, unveiled an expansion to its sustainable film lineup. This extension, Encore, focuses on biaxially oriented polypropylene (BOPP) films, emphasizing the incorporation of chemically recycled polymers specifically tailored for food-contact applications. Furthermore, Innovia Films forged a strategic partnership with Prevented Ocean Plastic, resulting in a novel film composition integrating 30% of POP-sourced materials.

- April 2024: Berry Global's flexibles division ramped up its recycling capacity in three critical European facilities, marking a significant step in its pan-European initiative to bolster the production of its Sustane line of recycled polymers. With a keen eye on the rising appetite for high-performance films crafted from recycled materials, Berry Global is expected to leverage its global network to spearhead this expansion. This enhancement introduced cutting-edge equipment strategically stationed at Berry's Heanor (UK), Steinfeld (Germany), and Zdzieszowice (Poland) sites. The move is set to elevate the annual production of recycled plastics across Berry's European operations by an estimated 6,600 metric tonnes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Increasing Demand for Plastic Films Across Various Industries Indicates Growth Potential

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation towards Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-User Industry

- 6.2.1 Food

- 6.2.1.1 Candy & Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, And Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care & Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-use Industry Applications (Agricultural, Chemical, Etc.)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Elite Plastics Limited

- 7.1.2 Innovia Films (CCL Industries Inc.)

- 7.1.3 Berry Global Inc.

- 7.1.4 Klockner Pentaplast

- 7.1.5 SUDPACK Holding GmbH

- 7.1.6 UFlex Europe Ltd

- 7.1.7 Cosmo Films

- 7.1.8 The Jason Group

- 7.1.9 TCL Packaging

- 7.1.10 SRF LIMITED

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日