|

市場調査レポート

商品コード

1550233

ドイツのプラスチック包装フィルム:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Germany Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツのプラスチック包装フィルム:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

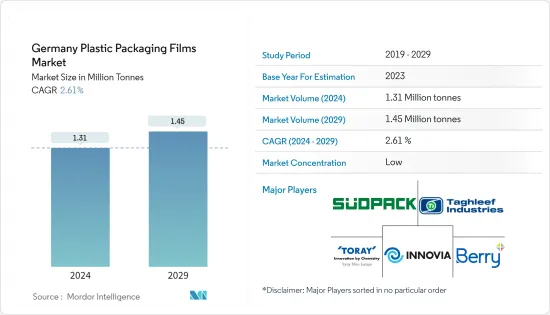

ドイツのプラスチック包装フィルム市場規模は2024年に131万トンと推定され、2029年には145万トンに達し、予測期間(2024-2029年)のCAGRは2.61%で成長すると予測されます。

主なハイライト

- プラスチックフィルムパッケージング市場は、様々な要因が重なって成長を遂げています。軽量で利便性の高いパッケージングに対する需要の急増、持続可能性に対する消費者の関心の高まり、賞味期限と製品保護を強化する技術の進歩などです。その他の特典としては、ドイツでは飲食品、医薬品、パーソナルケアなど様々な業界でプラスチックフィルム包装の採用が増加していることが挙げられます。

- プラスチックフィルム包装のドイツ市場は、主に食品包装への応用に牽引され、大幅な急成長を遂げる見通しです。この高騰は、硬質プラスチック包装から軟質プラスチック包装へのシフトを促進するダウンガウジングの増加傾向に起因しています。肉、果物、野菜、魚介類などの生鮮食品への食欲が高まるにつれ、バリアフィルムへの需要が高まっています。この需要は、小売業者、製造業者、消費者が一体となって、製品の賞味期限を延ばし、包装の無駄を最小化することを目指していることから、さらに拍車がかかっています。

- この地域の消費者は都会的なライフスタイルを取り入れており、便利な包装への需要が急増しています。消費者は軽量で使い勝手の良いソリューションを求めています。これに対しベンダーは、こうした進化する需要に応え、拡大するベンダー小売情勢の中で競争力を維持できるようなパッケージ作りに軸足を移しています。フレキシブルパウチのような軽い素材への移行は、こうした需要に応え、大幅な省エネルギーを実現します。このシフトは、消費者やブランドによる環境に優しい製品への意欲の高まりによってさらに加速し、すべての市場セグメントで生分解性プラスチックの使用を促進しています。さらに、優れた素材と機能におけるバイオプラスチック業界の絶え間ない技術革新は、消費者の意識の高まりによって後押しされています。

- 2024年3月、欧州連合理事会と欧州議会は、欧州連合の包装および包装廃棄物規則に関する交渉を最終決定しました。この法律は、野心的な廃棄物削減目標を設定し、域内で販売されるすべての包装をリサイクル可能なものとし、リサイクルのためのラベルを明示することを義務付けています。また、包装サイズの小型化、プラスチック包装の最低リサイクル率、再利用可能性の目標、特定の包装形態の禁止も規定されています。これらの厳しい措置は、欧州のプラスチック業界に大きな課題を突きつけています。この規制の主な目的は、EUにおける環境フットプリントを大幅に削減し、循環型経済を促進することです。この規制は、包装設計と材料における革新と持続可能性に拍車をかけることを目的としています。

- この地域にはプラスチック包装を規制する法律があるが、これらの法律は技術革新の機会も提供しています。企業は高度なリサイクル技術の開発や、新しいバイオベースのプラスチックフィルムの発売などに注力することができ、環境への影響を減らし、規制要件を満たすことができます。さらに、こうしたイノベーションは、持続可能なパッケージング・ソリューションに対する消費者の需要の高まりに対応し、ブランドの評判を高めることで、市場の成長を促進すると期待されています。

ドイツのプラスチック包装フィルム市場動向

ポリエチレンセグメントが大きな市場シェアを占める

- ポリエチレン(PE)は、その多様な物理的特性で珍重され、この地域の支配的なプラスチック材料として際立っています。ポリエチレンの普及は、他のプラスチックとは一線を画す生産コスト効率の高さに起因しています。ポリエチレンは一次包装用プラスチックの中で最も軟化点が低く、エネルギー消費量を削減できます。LDPEとLLDPEは、軟包装分野でPEと並んで広く普及している2種類のプラスチックです。ポリ袋、フィルム、ジオメンブレンの製造に広く使用されているポリエチレンは、その軽量性、部分的な結晶化度、耐薬品性、最小限の吸湿性、遮音性などの特筆すべき特徴で称賛されています。

- 柔軟性、高い防湿性、耐久性で知られるポリエチレンは、低温性能にも優れています。ポリエチレンは、追加のコーティングなしで密封できるユニークな能力が際立っています。この素材は、単独で使用しても、他の素材と組み合わせて使用しても、強固なバリアを形成します。さらに、その環境に優しい性質は、包装フィルムメーカーにますますアピールし、持続可能性への懸念に対応しています。

- 製品の視認性は購買決定に大きく影響します。消費者は透明な包装で陳列された製品に惹かれ、様々な業界でポリテンフィルムの需要を牽引しています。透明な包装は、消費者が購入前に製品を見ることができ、信頼を築き、販売の可能性を高める。ポリエチレンバリアフィルムのメーカーは、より大きな市場シェアを獲得するため、透明性を優先する傾向が強まっています。

- この動向は特に飲食品業界で顕著であり、透明包装は製品の品質と鮮度を表示するために不可欠です。ドイツにおける包装活動の急増は、ポリテンベースの包装用フィルムの需要増加の重要な原動力となっています。ドイツの包装業界の収益は、2020年の34億6,927万米ドルから2023年には38億3,429万米ドルに急増し、2025年には39億3,022万米ドルにさらに上昇すると予測されています。この成長は、飲食品、医薬品、消費財など様々なエンドユーザー産業で透明包装ソリューションの採用が増加していることに起因しています。

- 現在、欧州全域でポリエチレン価格が引き下げられており、ポリエチレンバリアフィルムメーカーにとって大きな成長機会となっています。こうした価格低下により、メーカーはより高い利幅を確保し、増収への道を開くことができます。原料価格の低下によるコスト削減分は、研究開発に再投資することができ、製品の品質と技術革新を強化することができます。このような価格競争上の優位性により、メーカーは顧客により魅力的な価格を提供することで市場シェアを拡大することもできます。

市場で大きなシェアを占めると予想される食品セグメント

- ドイツでは、焼き菓子、菓子類、コンビニエンス・フードに対する食欲が高まっており、軟包装、特にポリエチレン製バリア・フィルムの需要を牽引しています。ポリエチレン製バリアフィルムは水分バリア機能を持ち、製品の賞味期限を延ばすのに重要な役割を果たしています。開封しやすい包装に対する消費者の嗜好が強いことから、プラスチック・フィルム・ソリューションは、特に調理済み食品やコンビニエンス・フード向けの包装で優位を占めています。

- この地域における食品消費の増加は、多様な食品に合わせたプラスチックフィルムの需要増加の決定的な原動力となっています。この動向に拍車をかけているのは、食品の安全性を確保し、保存期間を延ばし、製品の見栄えを良くする、より優れたパッケージング・ソリューションへのニーズです。消費者が健康志向を強め、利便性を求めるようになるにつれ、食品包装用プラスチックフィルム市場は拡大を続け、技術革新と成長の機会を提供しています。

- ドイツでは、食品に対する消費支出が顕著な上昇を見せ、消費動向のエスカレートに牽引されて2019年の1,766億4,000万米ドルから2023年には2,199億4,000万米ドルに上昇しました。この増加は、可処分所得の増加、食生活の嗜好の変化、人口の拡大といった要因の影響を受けて、多様な食品に対する需要が拡大していることを反映しています。この動向は、食品関連企業や投資家にとって市場の潜在性が大きいことを示しています。

- さらに、ドイツにおける一人当たりの食費の増加は、多様な食品の市場が急成長していることを示唆しており、軟包装部門に絶好の機会をもたらしています。この成長の原動力となっているのは、すぐに食べられる食事やスナック、高級食品に対する消費者の需要の増加です。プラスチック包装メーカーは、利便性、品質、持続可能性、ブランド訴求に対する消費者の需要に合わせて製品を調整することで、この動向から利益を得る立場にあります。さらに、パッケージング技術や素材の先進化は、製品の保存性をさらに高め、環境への影響を減らすことができ、環境にやさしいソリューションを重視する傾向が強まっていることと一致します。

- ドイツは、インターネット利用率の急速な上昇に後押しされ、欧州のeコマース展望のフロントランナーとして台頭しています。2023年までに、eコマースはすでにドイツ市場の80%に浸透しています。さらに、同国のオンライン・コミュニティは、2020年の6,240万人から2025年には6,840万人に拡大するとみられています。注目すべきは、eコマースにおけるプラスチックフィルム包装の人気の高まりです。その魅力は、保護性と耐久性の高さにあり、商品を破損や漏れから効果的に保護し、束ねられた商品を安全に保つことができます。このようなeコマースの急増はまた、効率的なプラスチックフィルム包装の必要性をさらに強調し、オンライン食品配達の需要を強化しています。

ドイツのプラスチック包装フィルム産業概要

ドイツのプラスチック包装フィルム市場は断片化されており、Innovia Films(CCL Industries Inc.), TORAY FILMS EUROPE, Berry Global Inc.この市場の特徴は、製品の差別化が低いこと、製品の普及が進んでいること、競合が多いことです。

- 2024年4月ベリー世界のフレキシブル部門は、欧州の重要な3施設でリサイクル能力を増強しました。この動きは、再生ポリマーのSustaneシリーズの生産を強化するための、より広範な全欧州的イニシアチブの一環です。同社は、ヒーナー工場(英国)、シュタインフェルト工場(ドイツ)、ズジエショヴィツェ工場(ポーランド)に戦略的に最新設備を導入しました。この戦略的拡大により、ベリーの再生プラスチック生産量は年間約6,600トン増加します。さらにベリーは、この拡張は単に量だけの問題ではないと強調しています。再生プラスチックの品質を高めるためです。この品質向上は、ベリーのフレキシブルフィルム・ソリューションのCircularシリーズに利益をもたらし、これらの製品がその特徴である強度、耐久性、保護品質を維持することを確実にします。

- 2023年11月ベリー世界は、Omni Xtraポリエチレンクリングフィルムの最新版を発表しました。このアップグレードフィルムは、従来のポリ塩化ビニル(PVC)製クリングフィルムに代わる、より環境に優しく効率的なフィルムです。野菜や果物の包装から肉、鶏肉、惣菜の包装まで様々な用途に対応するオムニ・エクストラ+は、イノベーションと持続可能性に対するベリーのコミットメントを強調するものです。

- 2023年7月ダウとクロックナー・ペンタプラストは、多層真空フィルムであるKP Flexivacを共同で発表しました。この革新的な製品は特筆すべきマイルストーンを達成した:この革新的な製品は、リサイクルセンターCyclosHTPとリサイクルアライアンスInterserohによって100%リサイクル可能なPEとして認定されました。KP Flexivacは、骨付きの生肉や鶏肉のカット肉を包装するために特別に設計されています。密閉シールと堅牢なフィルムにより、最適な食品保護と安全性が確保され、サプライチェーン全体で品質が維持されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションへの需要の高まり

- 各業界における需要の急増は、プラスチックフィルムの成長の可能性を示す

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(PP)(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料、スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他最終用途(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- TORAY FILMS EUROPE

- Bauerschmidt Plastics GmbH

- Innovia Films(CCL Industries Inc.)

- Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- Berry Global Inc.

- Klockner Pentaplast

- SUDPACK Holding GmbH

- DUO PLAST AG

- Taghleef Industries

- Cosmo Films

- Jindal Films Europe

- SRF LIMITED

第8章 投資分析

第9章 市場の将来

The Germany Plastic Packaging Films Market size is estimated at 1.31 Million tonnes in 2024, and is expected to reach 1.45 Million tonnes by 2029, growing at a CAGR of 2.61% during the forecast period (2024-2029).

Key Highlights

- The plastic film packaging market is witnessing growth propelled by a confluence of factors. These include a surging demand for lightweight and convenient packaging, a heightened consumer focus on sustainability, and technological advancements to enhance shelf life and product protection. Additionally, the market benefits from the increasing adoption of plastic film packaging in various industries, such as food and beverage, pharmaceuticals, and personal care, in Germany.

- The German market for plastic film packaging is poised to witness a significant surge, primarily driven by its applications in food packaging. This surge is attributed to the rising trend of downgauging, facilitating a shift from rigid to flexible plastic packaging. With an increasing appetite for fresh produce like meat, fruits, vegetables, and seafood, there is a heightened demand for barrier films. This demand is further fueled by a collective push from retailers, manufacturers, and consumers, all aiming to prolong product shelf life and minimize packaging waste.

- The region's consumers, embracing urban lifestyles, are fueling a surge in the demand for convenient packaging. They seek lightweight, user-friendly solutions. In response, vendors are pivoting toward crafting packaging that meets these evolving demands and helps them stay competitive in the expanding organized retail landscape. Transitioning to lighter materials, like flexible pouches, meets these demands and offers significant energy-saving advantages. This shift is further amplified by an increasing appetite for eco-friendly products from consumers and brands, propelling the use of biodegradable plastics across all market segments. Moreover, the bioplastics industry's continuous innovation in superior materials and functions is bolstered by increased consumer awareness.

- In March 2024, the Council of the European Union and the European Parliament finalized negotiations on the European Union's Packaging and Packaging Waste Regulation. This legislation sets ambitious waste reduction targets, mandating that all packaging sold in the region be recyclable and clearly labeled for recycling. It also stipulates smaller packaging sizes, minimum recycled content for plastic packaging, reusability targets, and bans on specific packaging formats. These stringent measures pose a significant challenge to the European plastics industry. The regulation's primary goal is to markedly reduce the environmental footprint and foster a circular economy in the European Union. It aims to spur innovation and sustainability in packaging design and materials.

- While the region has laws governing plastic packaging, these laws also present opportunities for innovation. Companies can focus on developing advanced recycling techniques and launching new bio-based plastic films, which can help reduce environmental impact and meet regulatory requirements. Additionally, these innovations are expected to drive market growth by catering to the increasing consumer demand for sustainable packaging solutions and enhancing brand reputation.

Germany Plastic Packaging Films Market Trends

Polyethylene Segment to Hold Significant Market Share

- Polyethylene (PE) stands out as the dominant plastic material in the region, prized for its diverse physical properties. Its widespread adoption can be attributed to the cost-efficiency of its production, setting it apart from other plastics. Polyethylene boasts the lowest softening point among primary packaging plastics, reducing energy consumption. LDPE and LLDPE are the two other prevalent variants alongside PE in the flexible packaging sector. Widely employed in making plastic bags, films, and geomembranes, polyethylene is lauded for its lightweight nature, partial crystallinity, and notable traits, such as chemical resistance, minimal moisture absorption, and sound insulation.

- Polyethylene, known for its flexibility, high moisture barrier, and durability, also excels in low-temperature performance. It stands out for its unique ability to seal without additional coatings. This material forms a robust barrier, whether used alone or in combination with others. Moreover, its eco-friendly nature increasingly appeals to packaging film manufacturers, addressing sustainability concerns.

- Product visibility significantly influences purchasing decisions. Consumers gravitate toward products showcased in transparent packaging, driving the demand for polythene films across various industries. Transparent packaging allows consumers to see the product before purchasing, which builds trust and increases the likelihood of a sale. Manufacturers of polyethylene barrier films are increasingly prioritizing transparency to capture a larger market share.

- This trend is particularly evident in the food and beverage industry, where clear packaging is essential for displaying product quality and freshness. The surge in packaging activities in Germany is a crucial driver for the rising demand for polythene-based packaging films. The revenue of the packaging industry in Germany surged from USD 3,469.27 million in 2020 to USD 3,834.29 million in 2023, and it is projected to climb further to USD 3,930.22 million by 2025. This growth is attributed to the increasing adoption of transparent packaging solutions by various end-user industries, including food and beverage, pharmaceuticals, and consumer goods.

- Current reductions in polyethylene prices across Europe present a significant growth opportunity for manufacturers of polyethylene barrier films. These lowered prices enable manufacturers to secure higher margins and pave the way for increased revenues. The cost savings from lower raw material prices can be reinvested into research and development, enhancing product quality and innovation. This competitive pricing advantage may also allow manufacturers to expand their market share by offering more attractive pricing to customers.

Food Segment Expected to Hold Significant Share in the Market

- A rising appetite for baked goods, confectionery, and convenience foods in Germany drives the demand for flexible packaging, notably polyethylene barrier films. These films, with their moisture-barrier properties, play a crucial role in extending the shelf life of products. Given the strong consumer preference for easy-to-open packaging, Plastic film solutions dominate the packaging landscape, especially for ready-to-eat or convenience foods.

- Rising food consumption in the region is a crucial driver behind the increasing demand for plastic films tailored to diverse food products. This trend is fueled by the need for better packaging solutions that ensure food safety, extend shelf life, and enhance product presentation. As consumers become more health-conscious and seek convenience, the market for plastic films in food packaging continues to expand, offering opportunities for innovation and growth.

- In Germany, consumer spending on food witnessed a notable rise, climbing from USD 176.64 billion in 2019 to USD 219.94 billion in 2023, driven by escalating consumption trends. This increase reflects a growing demand for diverse food products, influenced by factors such as higher disposable incomes, changing dietary preferences, and an expanding population. The trend indicates a robust market potential for food-related businesses and investors.

- Further, the rise in per capita food expenditure in Germany signals a burgeoning market for diverse food products, presenting a ripe opportunity for the flexible packaging sector. This growth is driven by increasing consumer demand for ready-to-eat meals, snacks, and premium food items. Plastic packaging manufacturers stand to benefit from this trend by tailoring their offerings to match consumer demands for convenience, quality, sustainability, and brand appeal. Additionally, advancements in packaging technology and materials can further enhance product shelf life and reduce environmental impact, aligning with the growing emphasis on eco-friendly solutions.

- Germany emerges as a frontrunner in Europe's e-commerce landscape, fueled by a rapid rise in internet usage. By 2023, e-commerce had already permeated 80% of the German market. Additionally, the nation's online community is set to expand from 62.4 million in 2020 to 68.4 million by 2025. Noteworthy is the rising popularity of plastic film packaging in e-commerce. Its allure stems from heightened protection and durability, effectively shielding products from damage and leaks and ensuring bundled items remain secure. This surge in e-commerce is also bolstering the demand for online food delivery, further emphasizing the need for efficient plastic film packaging.

Germany Plastic Packaging Films Industry Overview

The German plastic Packaging Films market is fragmented, with several global and regional players, such as Innovia Films (CCL Industries Inc.), TORAY FILMS EUROPE, Berry Global Inc., SUDPACK Holding GmbH, and Taghleef Industries, vying for attention in a contested market space. This market is characterized by low product differentiation, growing product penetration, and high competition.

- April 2024: Berry Global's Flexibles division ramped up its recycling capacity in three critical European facilities. This move is part of a broader pan-European initiative to bolster the production of its Sustane line of recycled polymers. The company has strategically deployed cutting-edge equipment at its Heanor (United Kingdom), Steinfeld (Germany), and Zdzieszowice (Poland) plants. This strategic expansion will boost Berry's annual recycled plastic output by around 6,600 metric tonnes. Moreover, Berry emphasizes that this expansion is not just about quantity. It is about enhancing the quality of recyclates. This quality boost will benefit Berry's Circular Range of flexible film solutions, ensuring these products maintain their hallmark strength, durability, and protective qualities.

- November 2023: Berry Global unveiled its latest Omni Xtra polyethylene clingfilm iteration, now dubbed Omni Xtra+. This upgraded film is a greener and more efficient substitute for conventional polyvinyl chloride (PVC) cling films. Tailored for various applications, from packaging fruits and vegetables to meats, poultry, and deli items, the Omni Xtra+ underscores Berry's commitment to innovation and sustainability.

- July 2023 - Dow and Klockner Pentaplast have jointly introduced KP Flexivac, a multi-layer vacuum film. This innovative product has achieved a notable milestone: It has been certified as 100% recyclable PE by the recycling center CyclosHTP and the recycling alliance Interseroh. KP Flexivac is designed explicitly to package bone-in fresh meat and poultry cuts. Its hermetical seal and robust film ensure optimal food protection and safety, maintaining quality across the entire supply chain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Surging Demand Across Industries Signals Growth Potential for Plastic Films

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation Toward Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy and Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, and Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings and Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care and Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-use Industry Applications (Agricultural, Chemical, Etc.)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TORAY FILMS EUROPE

- 7.1.2 Bauerschmidt Plastics GmbH

- 7.1.3 Innovia Films (CCL Industries Inc.)

- 7.1.4 Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- 7.1.5 Berry Global Inc.

- 7.1.6 Klockner Pentaplast

- 7.1.7 SUDPACK Holding GmbH

- 7.1.8 DUO PLAST AG

- 7.1.9 Taghleef Industries

- 7.1.10 Cosmo Films

- 7.1.11 Jindal Films Europe

- 7.1.12 SRF LIMITED