|

市場調査レポート

商品コード

1910432

包装フィルム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Packaging Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 包装フィルム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

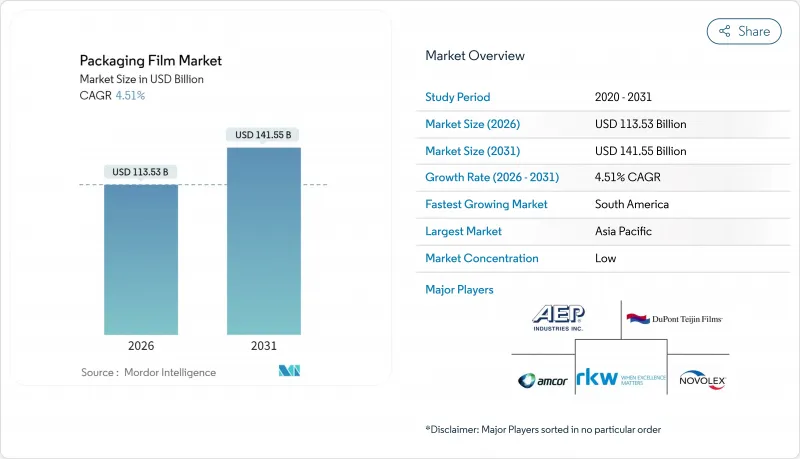

包装フィルム市場は2025年に1,086億3,000万米ドルと評価され、2026年の1,135億3,000万米ドルから2031年までに1,415億5,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは4.51%と見込まれます。

軽量な電子商取引用輸送資材への需要の高まり、欧州におけるリサイクル可能性に関する規制の強化、新興アジア太平洋経済圏におけるコールドチェーンの急速な拡大が、着実な成長の勢いを支えています。多層バリア技術革新、抗菌マスターバッチ、化学的リサイクル原料に関する合意がプレミアム成長分野を支える一方、戦略的な合併により、世界の主要コンバーター間の規模の優位性がさらに強調されています。

世界の包装フィルム市場の動向と洞察

電子商取引の急成長が軽量配送フィルムの需要を牽引

小包量の増加に伴い、ブランド各社は配送用包装の薄肉化を推進。耐落下性を維持しつつ容積重量を最大30%削減しています。PAC Worldwide社のEco PACジャケットシステムは、配送用封筒の自動化とフルフィルメントセンターの人件費削減を実現し、コスト効率とリサイクル目標を両立させます。二重シール式宅配袋は、顧客ロイヤルティに不可欠なリバースロジスティクスプログラムを支援します。短納期グラフィックはデジタル印刷機を活用し、ブランドエンゲージメントを強化するテーマ別プロモーションを実現。高額な版代を回避します。これらの要因が相まって、包装フィルム市場は世界の小売デジタル化の主要受益者として地位を強化しています。

EUによる単一素材リサイクルフィルムの推進

包装および包装廃棄物規制により、2030年までにプラスチック製食品包装の再生材含有率30%達成と完全リサイクル性が義務付けられ、ポリオレフィン単層ラミネートへの移行が加速しています。モパック社の80%再生ポリエチレン(rPE)含有認証構造は商業的実用性を実証し、コンバーター各社は脱墨・洗浄システムを導入して規制対応を推進。拡大生産者責任(EPR)費用は、クローズドループ回収を可能にする設計を促進する材料コストの梃子となります。規制期限が迫る中、包装フィルム市場では性能とリサイクル性を両立させる標準設計ルールが採用されつつあります。

北米および欧州におけるプラスチック禁止・課税

使い捨て製品への課税やPFAS禁止により、仕様の急激な見直しが迫られ、中規模工場では研究開発予算が逼迫し、顧客の認証サイクルが長期化しています。政策導入のばらつきにより、ブランドが地域ごとの旧式ラミネート材の廃止期限に対応するため、在庫計画が複雑化しています。

セグメント分析

ポリエチレンは、優れたコストパフォーマンスと幅広い加工性を背景に、2025年においても包装フィルム市場で42.10%のシェアを維持します。高密度グレードは半硬質用途に、LDPEおよびLLDPEはブローフィルム用途の大半を支えます。バイオプラスチックは、政策動向とブランドの公約強化により、2031年まで堅調なCAGR7.75%を記録する見込みです。バイオプラスチック製品の包装フィルム市場規模は、原料のスケールアップが順調に進めば、10年以内に数十億米ドル規模に達すると予測されます。ポリプロピレンの二軸延伸製品は、高級菓子包装向けに透明性と剛性で競争力を発揮します。PET層はレトルト用途で寸法安定性を確保し、高ガスバリア性を求める場合には酸化アルミニウムコーティングと組み合わせられることが多くあります。化学的リサイクル技術の進展により、新規原料と同等の特性を有するクローズドループPEが実現されつつあり、チタンケイ酸塩触媒技術は現在パイロットスケール段階にあります。ブロック共重合PLAの革新により脆性が低減され、生鮮食品用パウチ向けにバイオベース率80%の代替品が提供されています。

ポリエチレン加工メーカーは、高速成形充填シールラインに不可欠な特性であるシール透過汚染性能を向上させるメタロセン系触媒への投資を進めています。包装フィルム市場は、コスト効率と持続可能性の要請とのバランスを模索しており、既存メーカーが生産量を維持する一方、特殊バイオポリマーが規制要件や消費者嗜好の変化に対応しています。

多層構造は層ごとの機能性により機械的・光学的・バリア特性を最適化し、2025年には売上高の56.20%を占めました。医薬品物流やレトルト食品分野で長期保存が求められる中、EVOHまたはAlOx層を組み込んだバリア積層材はCAGR6.14%で拡大中です。一方、回収プロセスが簡易な化学組成を要求する分野(特に北米の店舗回収リサイクル)では単層フィルムが依然重要性を維持しています。

共押出機にはインライン延伸装置を追加し、機械方向延伸PEラミネートを製造することで、リサイクル性を満たしつつ耐穿刺性を維持します。ナノクレイ分散液は同等厚みで酸素透過率を60%低減し、さらなる薄肉化への道を開きます。層厚スキャナーはプロファイル精度を向上させ、起動時の廃棄物を最小限に抑えることで、包装フィルム市場参入企業の収益性向上に直結する歩留まり改善を実現します。

地域別分析

アジア太平洋地域は、豊富な樹脂供給、競争力のある労働力、広大な消費者基盤に支えられ、2025年においても包装フィルム市場の37.00%のシェアを維持しました。中国の過剰包装規制「GB/T 31268-2024」は、小包重量制限を満たす超軽量パウチの需要を喚起しています。タイとインドネシアでは、試験プロトコルを標準化し、現地の押出技術の高度化を促進する食品接触規制の調和が実施されています。JPFLフィルムズなどのインド企業は、国内および輸出機会を獲得するため、年間6万トンのBOPP生産能力を追加しました。日本と韓国はバリアコーティングの研究開発を推進し、オーストラリアは使用済みリサイクル素材の使用率向上に重点を置いています。

欧州ではPPWRの再生可能性及び再生材含有率基準を満たすため、変革的な投資サイクルに直面しています。コンスタンティア・フレキシブルズによるアリュフレックスパック買収は箔加工技術の統合と東南欧地域での基盤強化につながりました。ブランド各社は消費者向け廃棄手順のQRコード化を導入し、回収品の純度向上を図っています。英国とドイツでは化学的リサイクル回収拠点の試験運用が開始され、再生ポリエチレン(rPE)の統合を推進しています。

北米では成熟した電子商取引ネットワークと政策の明確化が進んでいます。PFAS(パーフルオロアルキル物質)使用禁止期限により、コンバーターは金属化BOPPやAlOx PETへ移行。カナダは原料コスト優位性を活かし主要輸出国としての地位を維持。メキシコの施設は国内スナック市場と米国南部バリューチェーンの両方に供給しています。

南米は2031年までに7.60%という最速のCAGRを記録。高バリアフィルムを必要とする農産物輸出が牽引役です。OPP FILM COLOMBIA社とGDM Plasticos社の投資によりBOPP・CPPの生産基盤が拡大。地域資金機関はエコデザイン研究所を支援し、包装フィルム市場における新たな成長フロンティアとしての地位を確立しています。

中東・アフリカ地域では、都市部小売業の拡大により堅調な二桁の数量増加が見込まれます。サウジアラビアとアラブ首長国連邦では、調達選択を導く再生可能プラスチックの義務化が導入され、南アフリカの確立されたコンバーターはコスト最適化製品で広範な大陸市場にサービスを提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引の急成長が軽量輸送用フィルムの需要を牽引

- EUによる単一素材リサイクル可能フィルムの推進

- 新興アジア太平洋地域におけるコールドチェーン包装食品の成長

- 小ロットのパーソナライズ包装を可能にするデジタル印刷

- 食肉用フィルム向け抗菌添加剤マスターバッチ

- 食品グレード再生ポリエチレン(rPE)向け化学的リサイクル原料供給契約

- 市場抑制要因

- 北米および欧州におけるプラスチック禁止措置/課税

- 変動するバージン樹脂価格

- バイオベースフィルムのバリア限界

- 極薄フィルムによるコンバーターのダウンタイム

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因が市場に与える影響

第5章 市場規模と成長予測

- 素材タイプ別

- ポリエチレン

- 高密度ポリエチレン(HDPE)

- 低密度ポリエチレン(LDPE)

- 直鎖状低密度ポリエチレン(LLDPE)

- ポリプロピレン

- ポリエステル(BOPET)

- バイオプラスチック

- その他の素材タイプ

- ポリエチレン

- 映画構造別

- モノレイヤー

- 多層構造(2~3層)

- バリア多層構造(3層以上)

- 用途別

- 食品・飲料

- 医薬品・医療

- パーソナルケアおよび化粧品

- 耐久消費財および電子機器

- 産業および機関向け

- 農業および園芸

- その他のアプリケーション

- 用途別フォーマット

- バッグとポーチ

- ラップおよび蓋用フィルム

- ラベルとスリーブ

- ブリスター包装および小袋包装

- シュリンクラップおよびストレッチラップ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- シンガポール

- マレーシア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Jindal Poly Films Ltd

- Cosmo Films Ltd

- Uflex Ltd

- Huhtamaki Oyj

- ProAmpac Holdings

- Novolex Holdings

- AEP Industries

- RKW SE

- Toray Plastics

- Coveris Holdings

- Sigma Plastics Group

- SRF Limited

- Klockner Pentaplast

- Taghleef Industries

- Polyplex Corporation

- Transcontinental Inc.

- Dupont Teijin Films