|

市場調査レポート

商品コード

1550296

インドネシアのプラスチック包装フィルム市場:シェア分析、産業動向、成長予測(2024年~2029年)Indonesia Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアのプラスチック包装フィルム市場:シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 107 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

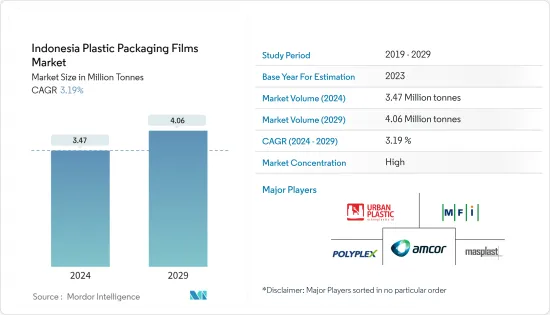

インドネシアのプラスチック包装フィルム市場規模は2024年に347万トンと推定され、2029年には406万トンに達し、予測期間(2024-2029年)のCAGRは3.19%で成長すると予測されます。

主なハイライト

- 先進パッケージングの増加とエンドユーザー産業の包装用途が市場を押し上げる大きな要因となっています。インドネシアでは、コンビニエンス製品の使用などの消費者行動動向により、1人当たりの包装材の使用量が増加しています。

- プラスチック包装フィルムが機能するための新しい方法を導入することは、インドネシアの包装産業に大きな影響を与えます。耐久性があり汎用性の高いプラスチック包装フィルムは、食品や医薬品から消費財に至るまで、あらゆる産業でますます支持されています。その適応性の高さが、多様化への需要を煽っています。

- さらに、複数のコンビニエンスストアが存在する食品業界は、近代的な小売チャネルの中でも最大級のセクターです。コンビニエンスストアは住宅地に近いため、店舗数は今後も拡大すると予測されます。食品パッケージに対する需要の高まりに伴い、プラスチック包装フィルムのような包装オプションに関する市場は大幅に拡大すると思われます。

- 環境法もプラスチック包装フィルムの拡大を妨げると予想されます。インドネシア政府は、プラスチック廃棄物を管理し、プラスチックのリサイクルを促進するための規制を実施しています。海洋廃棄物管理に関する2018年大統領規則第83号は、海洋プラスチック廃棄物の問題を管理し、環境への影響を低下させることを目的としています。

主なハイライト

- さらに、政府は2025年までに廃棄物管理70%、廃棄物削減30%という目標に向けて取り組んでいます。また、政府は2030年までに「廃棄物ゼロ」を目標に掲げ、製品のライフサイクルの川上から川下までの廃棄物問題に取り組んでいます。こうした政府の取り組みやプラスチック汚染は、予測期間中に調査される市場に影響を与える可能性があります。

インドネシアのプラスチック包装フィルム市場動向

ポリエチレン・セグメントが著しい成長を遂げる見込み

- 環境問題に対する意識の高まりにより、持続可能な包装への需要が高まっています。リサイクル可能な生分解性PEフィルムの技術革新は、こうした消費者や規制当局の要求に沿ったものです。

- 2023年6月、インドネシアの環境・林業大臣は、2029年までに使い捨てプラスチックフィルム製品を禁止する意向を発表しました。使い捨てプラスチックの段階的廃止に伴い、市場では再利用可能で堅牢なパッケージング・ソリューションに対する需要が急増することが予想されます。

- ポリエチレン(PE)包装フィルムは、その耐久性と適応性が評価され、その代替品として台頭し、市場の需要に拍車をかけています。この変化は、持続可能性と環境責任を求める世界の動向と一致しており、PE包装フィルムの成長見通しをさらに後押ししています。

- eコマース販売の急増は出荷製品の増加につながり、耐久性と保護性に優れた包装材料への需要を高めています。ポリエチレン包装フィルムは軽量で柔軟性があり、保護性に優れているため、eコマース包装に最適です。

- インドネシアは東南アジア最大級の小売eコマース市場を誇っており、カナダ農業・農業・食品省(Agriculture and Agri-Food Canada)はこれを強調しています。2021年、インドネシアの小売eコマース売上高は373億4,000万米ドルに達し、2017年の約5倍になった。小売eコマースの売上高は、2026年までに904億7,000万米ドルに達すると予想されています。

著しい成長を見せる食品セグメント

- 多層フィルム、ハイバリアフィルム、生分解性フィルムといった包装技術の革新は、プラスチック包装の機能性と持続可能性を高めています。これらの進歩は、保存期間の延長や食品安全性の向上といった食品業界特有のニーズに対応しています。

- 業界関係者の重要なステップのひとつは、持続可能な環境のためのインドネシア包装リサイクル協会(PRAISE)の設立です。コカ・コーラ・インドネシア、Indian Food Sukses McMar、ネスレ・インドネシア、テトラパック・インドネシア、Tirta Investama、ユニリーバ・インドネシア財団がこの非営利団体を設立しました。

- 2030年、インドネシアはプラスチック包装廃棄物を価値ある資源に転換し、経済的、社会的、環境的な利点を育むことで、持続可能な生態系を確立することを目指しました。

- 加工肉、シーフード、代替肉の売上が伸びていることは、便利で、すぐに食べられ、調理が簡単な食品に対する消費者の嗜好が高まっていることを示しています。これらの製品は、効率的で信頼性の高い包装ソリューションを必要とし、プラスチック包装フィルムの需要を牽引しています。

- 米国農務省が2023年7月に発表した記事によると、インドネシアにおける加工肉、魚介類、代替肉の小売売上高は、2017年の14億3,190万米ドルから2022年には19億7,680万米ドルへと大幅に増加しており、これらの製品に対する需要の高まりを浮き彫りにしています。

インドネシアのプラスチック包装フィルム産業概要

インドネシアのプラスチック包装フィルム市場は統合されており、以下のような大手企業が数社あります。 Amcor Group GmbH, PT Polyplex Films Indonesia, and PT. Urban Plastik Indonesia and PT MC PET Film Indonesia occupy most of the market share. Several companies in the Nordic are forging alliances and engaging in mergers to bolster their market presence.

- 2024年3月:INEOS Olefins &Polymers Europe、PepsiCo、Amcorの3社は共同で、再生プラスチックを50%使用した革新的なスナック菓子包装ソリューションをSunbitesクリスピーに導入しました。両社は、このパッケージが最先端のリサイクルプロセスによってプラスチック廃棄物を食品用素材に変換して製造されることを明らかにしました。

- 2023年3月:イーパック・フレキシブル・パッケージング社は、PFASとプラスチック包装に関する全ての州の期限を早期に遵守することを発表しました。2023年、いくつかの州は包装材へのポリフルオロアルキル物質(PFAS)の意図的添加を禁止する法規制の施行を開始しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- HoReCaと食品産業の急成長

- 市場抑制要因

- 明確なリサイクル計画の欠如と環境課題

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料・スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他のエンドユーザー産業用途(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- PT Polyplex Films Indonesia

- PT. Urban Plastik Indonesia

- PT MC PET Film Indonesia

- PT MASPLAST POLY FILM

- Amcor Group GmbH

- ePac Holdings, LLC.

- PT. Dinakara Putra.

- Pt Trias Sentosa TBK

- Pt Indopoly Swakarsa Industry TBK

- Pt Argha Karya Prima Industry

第8章 リサイクルと持続可能性の展望

第9章 市場の将来展望

The Indonesia Plastic Packaging Films Market size is estimated at 3.47 Million tonnes in 2024, and is expected to reach 4.06 Million tonnes by 2029, growing at a CAGR of 3.19% during the forecast period (2024-2029).

Key Highlights

- The increasing advancements and end-user industry packaging applications are the significant factors pushing the market. In Indonesia, the use of packaging per person is rising due to consumer behavior trends, such as the use of convenience products.

- Implementing new ways for plastic packaging films to function significantly impacts Indonesia's packaging industry. Durable and versatile plastic packaging films are increasingly favored across industries, from food and pharmaceuticals to consumer goods. Their adaptability fuels the demand for diversification.

- Moreover, with multiple convenience stores, the food industry is one of the largest sectors among modern retail channels. They are projected to continue to expand in terms of the number of outlets, as they are closer to residential areas. With the rising demand for food packages, the market would escalate significantly regarding packaging options like plastic packaging films.

- Environmental laws are also anticipated to hinder the expansion of plastic packaging films. The government of Indonesia has enforced regulations to manage plastic waste and promote plastic recycling. Presidential Regulation Number 83 of 2018 on marine waste management governs the issue of marine plastic waste and aims to lower its impact on the environment.

- Further, the government is working towards its target of 70% waste management and 30% waste reduction by 2025. Also, the government is devoted to addressing waste from the upstream and downstream life cycle of products, targeting "zero waste" by 2030. Such government initiatives and plastic pollution might impact the market studied over the forecast period.

Key Highlights

Indonesia Plastic Packaging Films Market Trends

Polyethylene Segment is Expected to Witness Significant Growth

- Growing awareness of environmental issues is leading to increased demand for sustainable packaging. Innovations in recyclable and biodegradable PE films align with these consumer and regulatory demands.

- In June 2023, Indonesia's Environment and Forestry Minister announced intentions to ban single-use plastic film products by 2029. With the phasing out of single-use plastics, the market is set to witness a surge in demand for reusable and robust packaging solutions.

- Polyethylene (PE) packaging films, prized for their durability and adaptability, are poised to emerge as a favored substitute, fueling their market demand. This shift aligns with global trends towards sustainability and environmental responsibility, further bolstering the growth prospects for PE packaging films.

- The surge in e-commerce sales leads to a higher volume of shipped products, increasing the demand for durable and protective packaging materials. Polyethylene packaging films are ideal for e-commerce packaging due to their lightweight, flexibility, and protective qualities.

- Indonesia boasts one of Southeast Asia's largest retail e-commerce markets, as highlighted by Agriculture and Agri-Food Canada. In 2021, retail e-commerce sales in Indonesia reached USD 37.34 billion, almost five times higher than in 2017. Retail e-commerce sales are anticipated to reach USD 90.47 billion by 2026.

Food Segment to Show Significant Growth

- Innovations in packaging technology, such as multi-layer films, high-barrier films, and biodegradable films, are enhancing the functionality and sustainability of plastic packaging. These advancements cater to the specific needs of the food industry, such as extended shelf life and improved food safety.

- One of the industry insiders' critical steps was establishing the Indonesian Packaging and Recycling Association for Sustainable Environment (PRAISE). Coca-Cola Indonesia, Indian Food Sukses McMar, Nestle Indonesia, Tetra Pak Indonesia, Tirta Investama, and Unilever Indonesia Foundation founded this non-profit organization.

- In 2030, Indonesia aimed to establish a sustainable ecosystem by converting plastic packaging waste into valuable resources, fostering economic, social, and environmental advantages.

- The rising sales of processed meat, seafood, and meat alternatives indicate a growing consumer preference for convenient, ready-to-eat, and easy-to-cook food products. These products require efficient and reliable packaging solutions, driving the demand for plastic packaging films.

- According to an article published by the United States Department of Agriculture in July 2023, the significant increase in retail sales of processed meat, seafood, and alternatives to meat in Indonesia from USD 1,431.9 million in 2017 to USD 1,976.8 million in 2022 highlights a growing demand for these products.

Indonesia Plastic Packaging Films Industry Overview

Indonesia's plastic packaging films market is consolidated, with a few major players such as Amcor Group GmbH, PT Polyplex Films Indonesia, and PT. Urban Plastik Indonesia and PT MC PET Film Indonesia occupy most of the market share. Several companies in the Nordic are forging alliances and engaging in mergers to bolster their market presence.

- March 2024: INEOS Olefins & Polymers Europe, PepsiCo, and Amcor have collaborated to introduce an innovative snack packaging solution for Sunbites crisps, which integrates 50% recycled plastic. The companies revealed that the packaging is manufactured by converting plastic waste into food-grade material through a cutting-edge recycling process.

- March 2023: ePac Flexible Packaging has announced its early compliance with all state deadlines concerning PFAS and plastic packaging. In 2023, several states started enforcing laws and regulations prohibiting the intentional addition of polyfluoroalkyl substances (PFAS) in packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Growth of HoReCa and Food Industry

- 5.2 Market Restraints

- 5.2.1 Lack of Defined Recycling Plans Coupled with Environmental Challenges

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene (Biaxially Oriented Polypropylene (BOPP), Cast Polypropylene (CPP))

- 6.1.2 Polyethylene (Low-density Polyethylene (LDPE), Linear Low-density Polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy & Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, and Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care & Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-user Industry Applications (Agricultural, Chemical, etc.)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 PT Polyplex Films Indonesia

- 7.1.2 PT. Urban Plastik Indonesia

- 7.1.3 PT MC PET Film Indonesia

- 7.1.4 PT MASPLAST POLY FILM

- 7.1.5 Amcor Group GmbH

- 7.1.6 ePac Holdings, LLC.

- 7.1.7 PT. Dinakara Putra.

- 7.1.8 Pt Trias Sentosa TBK

- 7.1.9 Pt Indopoly Swakarsa Industry TBK

- 7.1.10 Pt Argha Karya Prima Industry