インドのプラスチック包装フィルム市場:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

India Plastic Packaging Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550249

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

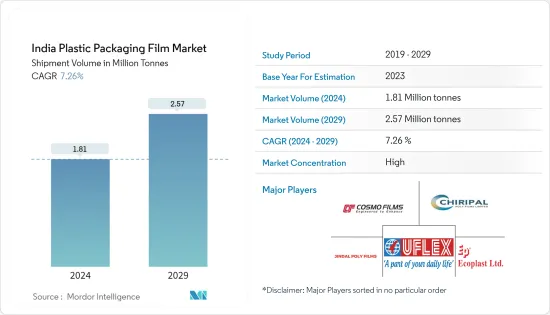

インドのプラスチック包装フィルム市場規模(出荷量ベース)は、2024年の181万トンから2029年には257万トンに拡大し、予測期間(2024-2029年)のCAGRは7.26%と予測されます。

主なハイライト

- インドでは包装食品への需要が高まっており、同時に医薬品の生産が急増しています。プラスチック包装フィルムには、軟質フィルムと硬質フィルムの両方が含まれます。

- 主にポリプロピレンとポリエチレンから作られるプラスチック包装用フィルムは、優れた防湿性を備えています。これらのフィルムは、ノンアルコール飲料から肉や魚介類に至るまで、飲食品の包装に幅広く使用されています。インドでは加工食品や包装食品の需要が急増しているため、飲食品分野では絶え間ない技術革新が中心となっています。

- 市場は大きな課題に直面しているが、その主因は環境問題への関心の高まりに対応した規制基準の進化です。インド政府は、環境破壊を抑制し廃棄物管理を強化するための厳しい規制を制定することで、プラスチック包装廃棄物に対する国民の意識向上に積極的に取り組んでいます。使い捨てプラスチックが環境に与える影響に対する意識の高まりにより、消費者は環境フットプリントを削減し、持続可能性の基準を高めた製品を求めるようになっています。

- フレキシブルフィルムには、生産コストの削減、持続可能性の向上、リサイクル容易性、カスタマイズオプションの増加など、多くの利点があります。市場全体のエンドユーザーが環境に優しい製品包装オプションに惹かれているため、硬質プラスチック包装から軽量で持続可能な包装用フレキシブルフィルムへと需要が大きくシフトしています。

- インドでは牛乳の生産量と消費量が顕著に急増しており、乳製品業界ではフレキシブル包装の需要が急増しています。これらのソリューションは、酪農産業特有のニーズに合わせて調整されており、強固な利点を提供しています。

- 米国農務省海外農業局によると、2023年にインドの国内生乳消費量は2億700万トンを超え、前年の2億200万トンから増加しました。この動向は今後も続くと予想され、乳製品用フレキシブル包装フィルムの需要に貢献しています。フレキシブル包装フィルムは、乳製品業界において製品の鮮度を維持し、賞味期限を延長する上で極めて重要な役割を果たしているため、乳製品業界の成長とともに包装フィルムの需要も増加すると思われます。

インドのプラスチック包装フィルム市場動向

BOPETフィルムの需要増加が見込まれる

- BOPET(二軸延伸ポリエチレンテレフタレート)は、延伸PETから製造されるポリエステルフィルムで、高い引張強度、化学的安定性、寸法安定性、透明性、反射性、ガスや香料のバリア性、電気絶縁性で利用されています。飲食品、食品、パーソナルケア、ホームケア、医薬品、その他消費財や工業製品用のさまざまな包装資材の製造に使用されます。

- 食品ブランドは、似たような商品でごった返すスーパーマーケットの棚で、自社製品を差別化するために熾烈な競争を繰り広げています。パウチパックとフィルムはこの戦略において極めて重要であり、パッケージの魅力を高め、ブランド認知を強化しています。カナダ農業食糧省によると、2023年、インドのチョコレート用パウチとフィルムの小売売上高は2億5,000万米ドルを超えました。2028年までには、この数字はCAGR 12.3%を記録し、約4億5,800万米ドルに急増すると予測されています。これは、今後数年間、インドでフレキシブルパウチの需要が見込まれることを示しています。

- BOPETパッケージングフィルムは、食品産業、特にスタンドアップパウチやレトルトパウチ、蓋フィルム、金属化フィルムに顕著な用途があります。BOPETフィルムの需要急増は、賞味期限延長に対する食品業界の関心の高まりと、サプライチェーン全体を通して食品廃棄を抑制する必要性に対応したものです。

- インド・ブランド・エクイティ財団(IBEF)の報告によると、BOPETフィルムはフレキシブル包装の主要な最終用途であり、世界消費の約60%を占めています。同市場は、世界の足跡をますます拡大しつつあるインドのメーカーが持続的に優位に立つ構えです。

- 数社が積極的に生産能力を拡大しています。2023年1月、Ester Industries Limited(Ester Filmtech Limited)は、テランガナ州にポリエステル(BOPET)フィルム製造工場を新設しました。50エーカーに及ぶこの48,000 MTPAユニットは、推定650カロールインドルピー(7,850万米ドル)のコストで建設されました。工場が本格稼動すれば、約600カロールインドルピー(7,262万米ドル)の収益が見込まれます。

ヘルスケアと製薬セクターの需要増加が市場成長を後押し

- プラスチックフィルムは、その卓越した透明性と透視性で知られ、ヘルスケア製品のクリアな視界を提供し、検査を容易にし、製品のプレゼンテーションを向上させる。その柔軟性により、パウチ、小袋、ブリスターパック、ラベルなど様々な包装形態へのシームレスな変換が可能で、ヘルスケア包装の幅広い要件に対応しています。

- 医薬品とヘルスケアのパッケージングは、封じ込め、医薬品の安全性の確保、ハンドリングとデリバリーにおける製品の識別を容易にします。生命を救う医薬品の販売、液体や剤形、手術器具、血液製剤、粉剤、様々な固形・半固形医薬品の包装において極めて重要な役割を果たしており、長期間にわたり品質を保つのに役立っています。

- インベスト・インディアは、インドの医薬品産業は2024年に650億米ドルになると予測しています。インドは医薬品輸出の中心的存在であり、200カ国以上に輸出されています。特に、インドはアフリカのジェネリック医薬品需要の半分以上を満たし、米国のジェネリック市場の40%を占め、英国の医薬品の4分の1を供給しています。さらに、インドは世界のワクチン市場で60%のシェアを占めており、特にDPT、BCG、麻疹ワクチンの主要供給国として優れています。

- ここ数年、特にCOVID-19以降、インドからの医薬品・ヘルスケア輸出は徐々に増加しています。しかし、インドからの輸出貿易の拡大に伴い、薬局や医療機器の包装用高酸素バリアポリマーフィルムの需要が高まっています。

- インド・ブランド・エクイティ財団(IBEF)の報告書によると、2023会計年度には、インドはジェネリック医薬品生産の世界的リーダーとして浮上し、2018年の173億米ドルから大幅に増加し、約254億米ドルの医薬品を輸出しました。さらに、インドの中間所得層の拡大は、より高い包装基準を要求する輸出の急増と相まって、特に医薬品分野におけるプラスチックフィルム包装需要の顕著な上昇を牽引しています。

インドのプラスチック包装フィルム産業の概要

インドのプラスチックフィルム包装市場は適度に断片化されています。主な市場プレイヤーは、UFlex Limited、Cosmo Films Limited、Jindal Poly Films、Ecoplast Ltd.などです。同市場は、原材料や包装サービスを供給する主要な世界・プレーヤーとローカル・プレーヤーで構成されています。包装とフィルム材料の最新開拓が市場を形成しています。

2024年4月UFlex LimitedはAmplus Phoenix Private Limitedと長期売電契約(PPA)を締結。この契約は、カルナタカ州にあるUFlexの包装用フィルム工場に特化したものです。UFlexは、2035年またはそれ以前にネット・ゼロ・エミッションを達成するというコミットメントの一環として、推定19,000 tCO2eの二酸化炭素排出量削減を目指しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量で持続可能な包装に対する業界全体の需要の高まり

- 食品・医薬品セクターからの堅調な需要が成長を促進

- 市場抑制要因

- プラスチック使用に対する政府の厳しい政策

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品

- ヘルスケア

- パーソナルケア&ホームケア

- 工業用包装

- その他の最終用途産業

- 食品

第7章 競合情勢

- 企業プロファイル

- Chiripal Poly Films

- Cosmo Films Limited

- UFlex Limited

- Jindal Poly Films

- Toray Advanced Film Co. Ltd

- Ecoplast Ltd

- TOPPAN Inc.

- Sealed Air Corporation

- Berry Global Inc.

- Vishakha Polyfab Pvt Ltd

- Supreme Industries Ltd

第8章 投資分析

第9章 市場機会と今後の動向

目次

The India Plastic Packaging Film Market size in terms of shipment volume is expected to grow from 1.81 Million tonnes in 2024 to 2.57 Million tonnes by 2029, at a CAGR of 7.26% during the forecast period (2024-2029).

Key Highlights

- India's growing appetite for packaged food and the simultaneous upsurge in pharmaceutical production, aimed at bolstering the nation's medicine supply, are pivotal factors propelling the demand for plastic packaging films. This encompasses both flexible and rigid films.

- Plastic packaging films, made predominantly from polypropylene and polyethylene, offer excellent moisture protection. These films are used extensively in packaging food and beverage items, ranging from non-alcoholic drinks to meat and seafood products. Constant innovation is taking center stage in the food and beverage sector, driven by the surging demand for processed and packaged foods in India.

- The market faces significant challenges, primarily driven by the evolving regulatory standards in response to mounting environmental concerns. The Indian Government is actively addressing public awareness of plastic packaging waste by enacting stringent regulations to curb environmental harm and enhance waste management. This heightened awareness of single-use plastics' environmental repercussions prompts consumers to seek products with reduced environmental footprint and elevated sustainability standards.

- Flexible films offer many advantages, such as reducing production costs, enhancing sustainability, enabling easy recyclability, and more customization options. Since end users across the market are gravitating toward eco-friendly product packaging options, there is a robust shift in demand from rigid plastic packaging to lightweight and sustainable flexible films for packaging.

- With India witnessing a notable surge in milk production and consumption, the demand for flexible packaging in the dairy industry has soared. These solutions are tailored to meet the specific needs of the dairy industry, offering robust advantages.

- According to the USDA Foreign Agricultural Service, in 2023, India's domestic milk consumption surpassed 207 million metric tons, marking a rise from the previous year's 202 million metric tons. This trend is expected to continue in the coming years, contributing to the demand for flexible packaging films for dairy products. Flexible packaging films play a pivotal role in maintaining product freshness and prolonging shelf life in the dairy industry; thus, with the growth of the dairy industry, the demand for packaging films will also increase.

India Plastic Packaging Film Market Trends

Demand for BOPET Films is Expected to Increase

- BOPET (biaxially oriented polyethylene terephthalate), a polyester film produced from stretched PET, is utilized for its high tensile strength, chemical and dimensional stability, transparency, reflectivity, gas and fragrance barrier qualities, and electrical insulation. BOPET is a transparent, robust, and lightweight plastic that is used to produce a range of packaging materials for beverages, food, personal care, home care, medicines, and other consumer and industrial products.

- Food brands compete fiercely to differentiate their products on supermarket shelves crowded with similar offerings. Pouch packs and films are pivotal in this strategy, enhancing packaging appeal and bolstering brand recognition. According to Agriculture and Agri-Food Canada, in 2023, India's retail sales for chocolate pouches and films surpassed USD 250 million. By 2028, this figure is projected to soar to approximately USD 458 million, recording a CAGR of 12.3%. This indicates the expected demand for flexible pouches in India in the coming years.

- BOPET packaging films find prominent applications in the food industry, notably in stand-up and retort pouches, lidding films, and metalized films. The surge in the demand for these films is a response to the food industry's heightened concerns over shelf life extension and the imperative to curb food wastage throughout the supply chain.

- India Brand Equity Foundation (IBEF) reported that BOPET film has primary end applications in flexible packaging, representing about 60% of global consumption. The market is poised to see sustained dominance from Indian manufacturers, who are increasingly expanding their global footprint.

- Several companies are actively expanding their production capacities. In January 2023, Ester Industries Limited (Ester Filmtech Limited) inaugurated its new polyester (BOPET) film manufacturing plant in Telangana. Spanning 50 acres, this 48,000 MTPA unit was constructed at an estimated cost of INR 650 crores (USD 78.5 million). Once fully operational, the plant is projected to generate revenues of approximately INR 600 crores (USD 72.62 million).

Rising Demand From the Healthcare and Pharmaceutical Sectors Aids Market Growth

- Plastic films, known for their exceptional clarity and transparency, offer a clear view of healthcare products, facilitating easy inspection and elevating product presentation. Their flexibility allows seamless conversion into various packaging formats like pouches, sachets, blister packs, and labels, meeting a wide array of healthcare packaging requirements.

- Pharmaceutical and healthcare packaging encompasses containment, ensuring drug safety, and facilitating product identification for handling and delivery. It plays a pivotal role in marketing life-saving drugs, packaging liquid and dosage forms, surgical devices, blood products, powders, and various solid and semisolid medications; it helps preserve their quality over an extended period.

- Invest India projected that the Indian pharmaceutical industry will be valued at USD 65 billion in 2024. India is a key player in pharmaceutical exports, reaching over 200 countries. Notably, India fulfills more than half of Africa's generic drug needs, dominates 40% of the US generic market, and supplies a quarter of the UK's medications. Moreover, India commands a substantial 60% share in the global vaccine market, particularly excelling as a primary provider of DPT, BCG, and measles vaccines.

- In the past few years, especially after COVID-19, pharmaceutical and healthcare exports from India have gradually increased. However, with the escalating export trade from the country, there is a rising demand for high-oxygen barrier polymer films for packaging pharmacies and medical devices.

- According to the India Brand Equity Foundation (IBEF) report, in the financial year 2023, India emerged as the global leader in generic drug production, exporting pharmaceuticals valued at approximately USD 25.4 billion, a significant rise from USD 17.3 billion in 2018. Moreover, India's expanding middle-income group, coupled with a surge in exports demanding higher packaging standards, is driving a notable uptick in plastic film packaging demand, especially in the pharmaceutical sector.

India Plastic Packaging Film Industry Overview

India's plastic film packaging market is moderately fragmented. Major market players include UFlex Limited, Cosmo Films Limited, Jindal Poly Films, and Ecoplast Ltd. The market comprises major global and local players supplying raw materials and packaging services. The latest developments in packaging and film materials are shaping the market.

April 2024: UFlex Limited secured a long-term power purchase agreement (PPA) with Amplus Phoenix Private Limited. This agreement was specifically tailored for UFlex's packaging films plant in Karnataka. As part of its commitment to achieving net-zero emissions by 2035, or even earlier, UFlex aims to slash its carbon footprint by an estimated 19,000 tCO2e.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of Substitutes

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand For Light-Weight and Sustainable Packaging Across Industries

- 5.1.2 Robust Demand From the Food and Pharmaceutical Sector Aids Growth

- 5.2 Market Restraints

- 5.2.1 Stringent Government Policies Against the Use of Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene (Biaxially Oriented Polypropylene (BOPP), Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End User

- 6.2.1 Food

- 6.2.1.1 Candy & Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, And Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products

- 6.2.2 Healthcare

- 6.2.3 Personal Care & Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-use Industry

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Chiripal Poly Films

- 7.1.2 Cosmo Films Limited

- 7.1.3 UFlex Limited

- 7.1.4 Jindal Poly Films

- 7.1.5 Toray Advanced Film Co. Ltd

- 7.1.6 Ecoplast Ltd

- 7.1.7 TOPPAN Inc.

- 7.1.8 Sealed Air Corporation

- 7.1.9 Berry Global Inc.

- 7.1.10 Vishakha Polyfab Pvt Ltd

- 7.1.11 Supreme Industries Ltd

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日