|

市場調査レポート

商品コード

1550224

フランスのプラスチック包装フィルム:市場シェア分析、産業動向、成長予測(2024年~2029年)France Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスのプラスチック包装フィルム:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 112 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

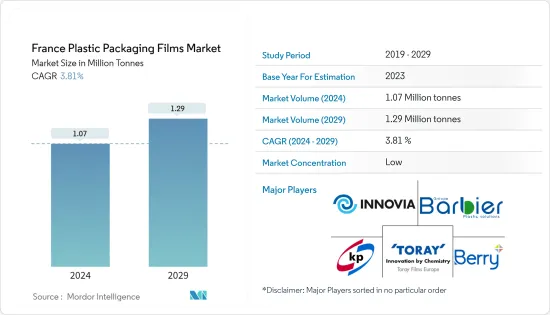

フランスのプラスチック包装用フィルム市場規模は2024年に107万トンと推定され、2029年には129万トンに達し、予測期間(2024-2029年)のCAGRは3.81%で成長すると予測されます。

主なハイライト

- フランスの包装業界は、消費者が革新的で個性的な包装のプレミアム製品を好むようになった好景気に後押しされ、力強い成長を遂げています。加えて、コンパクトで持ち運びに便利なパッケージ、特にパウチ包装の需要が急増しています。パウチ包装に対するこの需要の高まりは、単一のセクターに限定されるものではないです。食品、FMCG、食料品、化粧品などの業界は、この包装スタイルの採用を大幅に拡大する構えです。その結果、ソリューション・プロバイダーは、より魅力的な製品を提供することで市場での存在感を高めるため、技術革新の取り組みを強化しています。

- フランスの都市型ライフスタイルは、便利なパッケージングに対する需要の急増に拍車をかけています。消費者は軽量で使い勝手の良い選択肢を求めており、ベンダーは拡大するベンダー情勢の中で優位に立つため、デザインの軸足を移す必要に迫られています。フレキシブルパウチのような軽量素材の採用は、このような進化する需要に対応し、大幅な省エネのメリットを提供します。さらに、持続可能なパッケージング・ソリューションへのシフトは、環境に優しい製品を好む消費者の意識の高まりと一致しています。この動向は、包装ベンダー間のさらなる技術革新と競合を促進すると予想されます。

- 実用性、携帯性、持続可能性、ユーザーエクスペリエンスの向上に対する消費者の嗜好は、軟包装市場におけるプラスチックフィルム需要の高まりを後押ししています。こうした動向の進展に伴い、プラスチックフィルムパッケージング業界は、今日の消費者や企業のますます多様化するニーズに応えるべく、技術革新を進める態勢を整えています。このイノベーションには、プラスチックフィルム包装が市場競争力と環境に優しい選択肢であり続けるための、材料、生産プロセス、デザインの先進化が含まれると予想されます。

- さらに、消費者は利便性と食品廃棄物削減への関心の高まりから、賞味期限が延長された製品に惹かれています。プラスチックフィルム包装はその優れたバリア特性により、湿気、酸素、光、その他品質や鮮度を損なう可能性のある要素から商品を保護します。その結果、飲食品から医薬品、パーソナルケアに至るまで、生鮮品の賞味期限を延ばす上で極めて重要な役割を担っています。フランスでは、特に生鮮食品の小売において、使い捨てプラスチックが広く使用されています。これを抑制するため、新法はプラスチックフィルムとネットを禁止しています。

- この法律は、プラスチック廃棄物を削減し、持続可能な代替包装を大幅に促進することを目的としています。その結果、この法律は国内のプラスチック包装用フィルム市場を縮小させ、この市場セグメントに依存しているメーカーやサプライヤーに影響を与えることになります。この法律は、生分解性で再利用可能な材料の使用を奨励し、循環型経済への移行を目指す広範なイニシアチブの一環です。このシフトは、企業が新規制に準拠した環境に優しいソリューションを開発しようとするため、包装業界の技術革新を促進すると予想されます。

- このシナリオでは、国内で事業を展開するメーカーが研究開発投資を拡大し、新製品を革新・導入するために施設を拡張します。特筆すべきは、2024年3月、汎欧州的な取り組みの主要企業であるベリー・世界・グループのフレキシブルズ部門が、欧州の3つの施設でリサイクル能力を強化したことです。この動きは、再生ポリマーのSustaneシリーズの生産を強化するという、より大きな戦略の一環です。同社は、再生プラスチックの広大な世界ネットワークを活用し、再生材料から作られたプレミアムフィルムへの需要の高まりに応えることを目指しています。

フランスのプラスチック包装用フィルム市場動向

ポリエチレンセグメントが大きな市場シェアを占める

- 柔軟性、高い防湿性、耐久性で知られるポリエチレンは、低温下でも優れた性能を発揮します。ポリエチレンは、コーティング剤なしでも効果的に密封できることが特徴です。ポリエチレンは、単独で使用しても、他の素材と組み合わせて使用しても、強力なバリアとなります。さらに、ポリエチレンの環境に優しい特性は包装フィルムメーカーの注目を集め、業界が持続可能性を重視するようになっていることを物語っています。ポリエチレンは、食品包装、農業用フィルム、工業用包材など、さまざまな用途に使用できるため、幅広い分野で好まれています。ポリエチレンはリサイクル可能であり、プラスチック廃棄物の削減に貢献することから、市場におけるその魅力はさらに高まっています。

- ポリエチレン(PE)は、その汎用性の高い物理的特性により、この地域のプラスチック市場を独占しています。ポリエチレンの人気は、同種のプラスチックとは異なる特徴である、コスト効率の高い生産に由来します。特に、PEは一次包装用プラスチックの中で最も軟化点が低く、エネルギー消費量を削減できます。軟包装分野では、PEと並んでLDPEとLLDPEが有名です。ポリ袋、フィルム、ジオメンブレンに広く使用されているポリエチレンの魅力は、軽量で部分的に結晶構造を持ち、耐薬品性、低吸湿性、遮音性といった際立った特徴にあります。

- 欧州におけるポリエチレン価格の下落は、フランスのポリエチレン製バリアフィルムメーカーにとって有利な成長の道をもたらしています。こうした価格低下により、メーカーは利幅を拡大することができ、潜在的な収益急増につながります。安価な原材料による節約分を研究開発に振り向けることで、製品の品質と革新性を高めることができます。この価格競争力を武器に、メーカーはより競争力のある価格で顧客を魅了することで、市場シェアを維持・拡大する態勢を整えています。

- 製品の視認性は、消費者の選択を形成する上で極めて重要な役割を果たします。透明包装、特にポリテープフィルムは、様々な産業で需要が高まっています。この急増は、消費者が購入前に製品を視覚的に評価することを好み、信頼を醸成するだけでなく売上を押し上げる要因となっていることが背景にあります。その結果、ポリエチレンバリアフィルムのメーカーは現在、市場での存在感を高めるために透明性を重視しています。

- 飲食品分野では、製品の品質と鮮度をアピールする透明包装の重要性は疑う余地がないです。フランスでは、eコマースへの取り組みが加速していることもあり、パッケージング活動が顕著に増加しています。フランスのeコマース売上高は、2020年の1,214億米ドルから2023年には1,730億米ドルに増加しました。この上昇は主に、飲食品、医薬品、消費財などのセクターで、特にeコマース配送のために、透明包装ソリューションへの嗜好が高まっていることによる。透明包装は製品の視覚的魅力を高め、購入前に製品を確認できるようにすることで消費者の信頼を築く。さらに、オンラインショッピングの増加により、輸送中の製品の安全性と顧客満足度を確保するために、耐久性があり、視覚に訴える包装を使用する必要があります。

食品セグメントが市場で大きなシェアを占めると予想される

- 国内における食欲の高まりは、様々な食品に対応する特殊プラスチックフィルムの需要を促進する重要な要因となっています。この急増は主に、食品の安全性を提供し、賞味期限を延ばし、製品の美観を向上させる包装の追求によってもたらされています。消費者がますます健康と利便性を優先するようになる中、食品包装のプラスチックフィルム市場は顕著な上昇しており、革新と拡大の道を提示しています。さらに、材料科学と製造技術の進歩は、より持続可能で効率的なプラスチックフィルムの開拓を可能にし、市場の成長をさらに促進しています。また、食料品の買い物にeコマースの採用が増加していることも、堅牢で信頼性の高いパッケージング・ソリューションに対する需要の高まりに寄与しています。

- さらに、フランスのスーパーマーケットやハイパーマーケットにおける消費財の販売増加も、市場の需要を後押ししています。食品におけるプラスチックフィルムのニーズの急増や、冷凍食品や野菜を保護する必要性の高まりなどの主な要因は、今後数年間におけるプラスチックフィルムの需要を促進します。加えて、環境に優しく軽量なプラスチックフィルムへの意欲の高まりは、市場成長の有望な道を提供しています。

- 2023年4月から2024年3月にかけて、フランスのスーパーマーケットとハイパーマーケットにおける乳製品以外の生鮮食品の売上高は約165億5,700万米ドルに達しました。これに僅差で乳飲料が255億7,400万米ドル、砂糖入り食品が238億200万米ドル、冷凍食品が68億6,890万米ドルで続く。この期間の総売上高は1,462億5,190万米ドルでした。スーパーマーケットやハイパーマーケットにおける様々な食品や非食品に対する需要の高まりは、プラスチックフィルム市場が利便性、品質、持続可能性、ブランド訴求といった消費者の嗜好に合致する道を開いています。

- フランスのプラスチックフィルム市場は、拡大する飲食品産業、消費支出の増加、eコマース部門の急増に牽引され、予測期間中に安定した成長を遂げる構えです。包装食品と飲食品の需要の増加とオンラインショッピングによる利便性が、この市場の拡大に大きく寄与しています。さらに、プラスチックフィルム技術と持続可能なパッケージング・ソリューションの先進化は、市場の成長をさらに促進すると予想されます。

フランスのプラスチック包装フィルム産業概要

フランスのプラスチック包装フィルム市場は断片化されており、Innovia Films(CCL Industries Inc)、Berry Global Inc、Klockner Pentaplast、Cosmo Filmsなど複数の世界的・地域的プレーヤーが、製品の差別化が低く、製品の普及が進み、競争が激しいことを特徴とする競争の激しい市場空間で注目度を競っています。

- 2024年6月Trioworld GroupはSopal SASの全株式を取得し、フランスのPalamy SAS(パラミー)とBaudet et Rene Jean Emballage SAS(BRJ)を買収します。これらの企業はフランス市場の主要企業で、パン、冷凍食品、様々な消費者向けパッケージング・ニーズ向けの高性能パッケージング・ソリューションを専門としています。

- 2024年1月ベリー世界はOmni Xtraポリエチレンクリンフィルムの改良版を発表し、従来のPVC代替品としてリサイクル可能であることを証明しました。当初は果物、野菜、肉類、鶏肉、惣菜向けに開発された新しいOmni Xtra+フィルムは、耐衝撃性の向上、伸縮性の強化、より安定した延伸プロファイルを誇っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションへの需要の高まり

- 様々な産業におけるプラスチックフィルム需要の増加が成長の可能性を示す

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(PP)(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料、スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケアとホームケア

- 工業包装

- その他のエンドユーザー産業(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- TORAY FILMS EUROPE

- Innovia Films(CCL Industries Inc.)

- Berry Global Inc.

- Klockner Pentaplast

- SUDPACK Holding GmbH

- DUO PLAST AG

- SRF LIMITED

- Groupe Barbier

- Surfilm Packaging

- Trioworld Industrier AB

- AEP GROUP

第8章 投資分析

第9章 市場の将来

The France Plastic Packaging Films Market size is estimated at 1.07 Million tonnes in 2024, and is expected to reach 1.29 Million tonnes by 2029, growing at a CAGR of 3.81% during the forecast period (2024-2029).

Key Highlights

- The French packaging industry is experiencing robust growth, propelled by a buoyant economy empowering consumers to gravitate toward premium products, often presented in innovative and distinctive packaging. Additionally, the surge in demand for compact, on-the-go packaging, especially prevalent in pouch formats, is fueled by the country's busy professionals juggling hectic lifestyles. This heightened demand for pouch packaging is not limited to a single sector; industries like food, FMCG, groceries, and cosmetics are poised to ramp up their adoption of this packaging style significantly. Consequently, solution providers are ramping up their innovation efforts to bolster their market presence by offering more enticing products.

- The urban lifestyle in France is fueling a surge in demand for convenient packaging. Consumers seek lightweight, user-friendly options, prompting vendors to pivot their designs to stay ahead in the expanding organized retail landscape. Embracing lighter materials, like flexible pouches, meets these evolving demands and offers substantial energy-saving advantages. Additionally, the shift toward sustainable packaging solutions aligns with the increasing consumer awareness and preference for environmentally friendly products. This trend is expected to drive further innovation and competition among packaging vendors.

- Consumer preferences for practicality, portability, sustainability, and enhanced user experiences fuel the rising demand for plastic film in the flexible packaging market. As these trends evolve, the plastic film packaging industry is poised to innovate, catering to the increasingly diverse needs of today's consumers and businesses. This innovation is expected to include advancements in materials, production processes, and design to ensure that plastic film packaging remains a competitive and environment-friendly option in the market.

- Further, consumers are gravitating toward products with extended shelf lives, driven by convenience and a growing concern for reducing food waste. With its superior barrier properties, plastic film packaging shields items from moisture, oxygen, light, and other elements that can compromise their quality and freshness. As a result, it is pivotal in prolonging the shelf life of perishable items, spanning from food and beverages to pharmaceuticals and personal care. France continues to grapple with the prevalent use of single-use plastics, notably in the retail of fresh produce. To curb this, a new law prohibits plastic film and netting.

- This legislation aims to reduce plastic waste and significantly promote sustainable packaging alternatives. Consequently, this legislation is poised to constrict the market for plastic packaging films in the country, impacting manufacturers and suppliers who rely on this market segment. The law is part of a broader initiative to transition toward a circular economy, encouraging the use of biodegradable and reusable materials. This shift is expected to drive innovation in the packaging industry as companies seek to develop eco-friendly solutions that comply with the new regulations.

- In this scenario, manufacturers operating in the country ramp up R&D investments and expand their facilities to innovate and introduce new products. Notably, in March 2024, Berry Global Group Inc.'s Flexibles division, a key player in a pan-European effort, enhanced recycling capabilities in three of its European facilities. This move is part of a larger strategy to boost production of its Sustane line of recycled polymers. The company aims to meet the rising demand for premium films made from recycled materials, leveraging its vast global network for recycled plastics.

France Plastic Packaging Films Market Trends

Polyethylene Segment to Hold Significant Market Share

- Polyethylene, known for its flexibility, high moisture barrier, and durability, also boasts exceptional performance in low temperatures. It distinguishes itself by sealing effectively, even without added coatings. Whether utilized independently or in conjunction with other materials, polyethylene creates a formidable barrier. Furthermore, its eco-friendly attributes garner attention from packaging film manufacturers, underscoring the industry's growing focus on sustainability. The material's versatility extends to various applications, including food packaging, agricultural films, and industrial wrappings, making it a preferred choice across multiple sectors. Its ability to be recycled and its contribution to reducing plastic waste further enhance its appeal in the market.

- Polyethylene (PE) dominates the plastic landscape in the region due to its versatile physical properties. Its popularity stems from its cost-effective production, a distinguishing feature from its plastic counterparts. Notably, PE boasts the lowest softening point among primary packaging plastics, reducing energy consumption. Alongside PE, LDPE and LLDPE are prominent in the flexible packaging sector. Widely used in crafting plastic bags, films, and geomembranes, polyethylene's appeal lies in its lightweight, partially crystalline structure and standout features like chemical resistance, low moisture absorption, and sound insulation.

- Reduced polyethylene prices in Europe are creating a lucrative growth avenue for polyethylene barrier film manufacturers in France. With these price drops, manufacturers can bolster their margins, leading to a potential revenue surge. The savings from cheaper raw materials can be channeled back into R&D, elevating product quality and innovation. Armed with this pricing edge, manufacturers stand poised to retain and expand their market share by enticing customers with more competitive pricing.

- Product visibility plays a pivotal role in shaping consumer choices. Transparent packaging, particularly in the form of polythene films, is witnessing heightened demand across diverse industries. This surge is fueled by consumers' preference for visually assessing products before buying, a factor that not only fosters trust but also boosts sales. Consequently, producers of polyethylene barrier films are now placing a premium on transparency to bolster their market presence.

- In the food and beverage sector, the importance of transparent packaging, which showcases product quality and freshness, is unmistakable. France has witnessed a notable uptick in packaging activities, a surge further fueled by the country's escalating e-commerce endeavors. E-commerce sales revenue in France climbed from USD 121.4 billion in 2020 to USD 173 billion in 2023. This uptick was primarily driven by the growing preference for transparent packaging solutions across sectors like food and beverage, pharmaceuticals, and consumer goods, especially for e-commerce deliveries. Transparent packaging enhances the visual appeal of products and builds consumer trust by allowing them to see the product before making a purchase. Additionally, the rise in online shopping has necessitated using durable and visually appealing packaging to ensure product safety and customer satisfaction during transit.

Food Segment Expected to Hold Significant Share in the Market

- The country's growing appetite for food is a crucial catalyst propelling the demand for specialized plastic films catering to various food items. This surge is primarily driven by the quest for packaging that provides food safety, prolongs shelf life, and elevates product aesthetics. With consumers increasingly prioritizing health and convenience, the plastic film market in food packaging is witnessing a notable upswing, presenting avenues for innovation and expansion. Additionally, advancements in material science and manufacturing technologies enable the development of more sustainable and efficient plastic films, further driving market growth. The increasing adoption of e-commerce for grocery shopping also contributes to the rising demand for robust and reliable packaging solutions.

- Moreover, the rising sales of consumer goods in French supermarkets and hypermarkets are poised to bolster market demand. Key drivers, such as the surging need for plastic films in food and the growing necessity for protecting frozen food and vegetables, are set to propel the demand for plastic films in the coming years. Additionally, the increasing appetite for eco-friendly and lightweight plastic films offers a promising avenue for market growth.

- From April 2023 to March 2024, sales of non-dairy fresh food in French supermarkets and hypermarkets reached approximately USD 16,557 million. Dairy beverages closely followed this at USD 25,574 million, sugary foods at USD 23,802 million, and frozen foods at USD 6,868.9 million. The total sales for the period accounted for USD 146,251.9 million. This increasing demand for various food and non-food products in supermarkets and hypermarkets is paving the way for the plastic film market to align with consumer preferences for convenience, quality, sustainability, and brand appeal.

- The French plastic film market is poised for steady growth during the forecast period, driven by the expanding food and beverage industries, rising consumer spending, and the surge in the e-commerce sector. The increasing demand for packaged food and beverages and the convenience offered by online shopping significantly contribute to this market's expansion. Additionally, advancements in plastic film technology and sustainable packaging solutions are expected to propel market growth further.

France Plastic Packaging Films Industry Overview

The French plastic packaging films market is fragmented, with several global and regional players, such as Innovia Films (CCL Industries Inc.), Berry Global Inc., Klockner Pentaplast, and Cosmo Films, vying for attention in a contested market space characterized by low product differentiation, growing product penetration, and high competition.

- June 2024: Trioworld Group inked a deal to purchase all shares of Sopal SAS, effectively acquiring the French firms Palamy SAS (Palamy) and Beaudet et Rene Jean Emballage SAS (BRJ). These companies are key players in the French market, specializing in high-performance packaging solutions for bread, frozen food, and various consumer packaging needs.

- January 2024: Berry Global unveiled an enhanced iteration of its Omni Xtra polyethylene cling film, positioning it as a certified recyclable substitute for conventional PVC options. Initially tailored for fruits, vegetables, meats, poultry, and deli items, the new Omni Xtra+ film boasts heightened impact resistance, enhanced elasticity, and a more consistent stretching profile.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Increasing Demand for Plastic Films Across Various Industries Indicates Growth Potential

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation Toward Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy and Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, andnd Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings and Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care and Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-user Industries (Agricultural, Chemical, Etc.)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TORAY FILMS EUROPE

- 7.1.2 Innovia Films (CCL Industries Inc.)

- 7.1.3 Berry Global Inc.

- 7.1.4 Klockner Pentaplast

- 7.1.5 SUDPACK Holding GmbH

- 7.1.6 DUO PLAST AG

- 7.1.7 SRF LIMITED

- 7.1.8 Groupe Barbier

- 7.1.9 Surfilm Packaging

- 7.1.10 Trioworld Industrier AB

- 7.1.11 AEP GROUP