|

市場調査レポート

商品コード

1550285

スペインのプラスチック包装フィルム:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Spain Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインのプラスチック包装フィルム:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

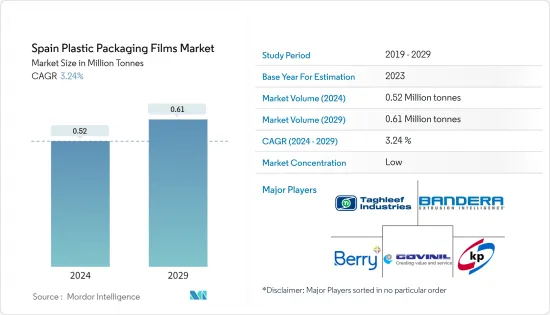

スペインのプラスチック包装フィルム市場規模は2024年に52万トンと推定され、2029年には61万トンに達し、予測期間(2024-2029年)のCAGRは3.24%で成長すると予測されます。

主なハイライト

- スペインの都市型ライフスタイルにより、便利な包装への需要が顕著に増加しています。消費者はますます軽量で使い勝手の良いものを選ぶようになっており、ベンダーは組織小売セクターの成長に対応するためにデザインを変更せざるを得なくなっています。フレキシブルパウチのような軽い素材に移行することで、ベンダーはこうした需要の変化に対応し、大幅な省エネ効果を享受しています。さらに、持続可能なパッケージング・ソリューションに向けた業界の動きは、環境に優しい製品を求める消費者の意識の高まりと共鳴しています。この連携は、包装情勢における技術革新と競合の激化に拍車をかける構えです。

- スペインの包装業界は、消費者がしばしば革新的な包装に包まれたプレミアム製品を選ぶ力を与えている好調な経済によって、力強い成長を目の当たりにしています。さらに、同国の多忙な専門職に牽引され、特にパウチ形式のコンパクトで持ち運びに便利なパッケージの需要が顕著に増加しています。この動向は単一分野に限定されるものではなく、食品、FMCG、食料品から化粧品に至るまで、あらゆる業界がパウチ包装の利用を拡大しようとしています。その結果、ソリューション・プロバイダーは市場での存在感を高め、より魅力的な製品を提供するために技術革新の努力を強めています。

- 消費者は、利便性と食品廃棄に対する意識の高まりから、賞味期限の長い製品を好むようになっています。プラスチックフィルム包装は優れたバリア性を誇り、湿気、酸素、光、その他品質や鮮度を損なう要因から商品を守る。そのため、飲食品から医薬品、パーソナルケア用品に至るまで、生鮮品の賞味期限を延ばす上で極めて重要なツールとなっています。フランスは、特に生鮮食品の小売部門において、使い捨てプラスチックへの依存に積極的に取り組んでいます。これを受けて、プラスチックフィルムとネットの使用を禁止する法律が最近制定されました。

- 欧州の経済回復と政策展開の一環として、「プラスチック課税」法が導入され、各EU加盟国で発生するリサイクルされないプラスチック包装廃棄物に料金をリンクさせています。スペインはこれに対し、2023年1月から適用される「再利用不可能なプラスチック包装に対する特別税」(法律7/2022)を制定しました。この税金は、廃棄物管理を強化し、土壌汚染と闘い、循環型経済を促進するために考案されました。スペイン全土に適用されるこの法律は、使い捨てプラスチック容器の製造業者、輸入業者、輸送業者に対し、素材の選択を見直すよう求めています。これらの厳しい措置は、スペインのプラスチック業界にとって注目すべき課題であり、環境への影響を削減し、循環型経済を先進させるというEUの広範な目標に沿ったもので、最終的にはパッケージングの革新と持続可能性を促進するものです。

- スペインは、特に生鮮食品の小売部門で、使い捨てプラスチックの広範な使用と積極的に闘っています。プラスチック廃棄物を削減し、持続可能な包装の採用を促進することを主な目的として、特にプラスチックフィルムとネットを対象とした法律が最近制定されました。その結果、この法律はスペインのプラスチック包装用フィルム市場を引き締め、この分野で確固たる地位を築いているメーカーやサプライヤーに直接的な影響を与えることになります。この法律は、循環型経済への幅広い後押しと一致し、生分解性で再利用可能な素材への移行を支持しています。この移行は、企業が更新された義務に沿った環境に配慮したソリューションを作ろうと努力するため、包装領域における技術革新を促進すると予想されます。

スペインのプラスチック包装フィルム市場動向

食肉、鶏肉、シーフード分野が大きな市場シェアを占める

- パウチ、袋、フィルム、ラップで提供されるプラスチックフィルム包装は、食肉、鶏肉、魚介類業界において、多様なカット、ポーションサイズ、包装形態に対応する汎用性を提供します。この汎用性により、ホールカットからソーセージやフィレなどの加工品まで、効率的な包装が可能になります。さらに、プラスチックフィルム包装は、保存期間の延長、製品の視認性の向上、汚染や腐敗に対する保護強化などの特典を提供し、メーカーや消費者に好まれる選択肢となっています。

- スペインでは近年、牛肉、豚肉、鶏肉、魚介類の消費と生産が著しく増加しています。この増加の背景には、消費者にやさしく、製品の保護を強化する包装に対する需要の高まりがあります。その結果、食肉、鶏肉、魚介類の包装は費用対効果が高く、実用的なソリューションとして台頭してきました。予測では、プラスチック包装の売上高は今後数年で増加します。この上昇は、主に衛生意識の高まりと、国内消費と輸出市場の両方にとって重要な、保存期間を延長し、食肉と鶏肉の本来の品質を維持する包装ソリューションの必要性に起因します。

- 2023年には、スペインでは家禽肉と食用内臓肉の輸出額が顕著に増加し、5億1,570万米ドルから5億5,130万米ドルに増加しました。この需要の急増は、輸送中の鮮度を確保するため、食肉包装に特殊プラスチック・フィルムを利用する動向を後押ししています。これらのプラスチック・フィルムは、汚染物質に対するバリアを提供し、食肉の保存期間を延長するように設計されており、輸送や保管中の品質維持に不可欠です。加えて、輸出額の増加は、スペイン産鶏肉製品に対する世界の食欲の高まりを反映しており、ひいては、国際基準と消費者の期待に応えるためにパッケージング技術の先進化が必要とされています。

- スペインは、魚と肉の消費量において、ポルトガルとノルウェーに次いで欧州第3位にランクされています。シーフード・カウンシルの調査によると、スペイン人の70%が週に2回、90%が少なくとも1回は魚を楽しんでいます。ヘイク、サーモン、タラ、ヒラメ、スズキ、マグロ、メカジキなどが好まれています。肉に関しては、スペイン農務省によれば、1人当たりの肉消費量は1日平均1349グラムです。鶏肉の消費量は1日平均38グラムで、豚肉と牛肉が僅差で続く。さらに、スペイン人は1日平均32グラムの加工肉を消費しており、調理済みまたは生ハムが人気です。このような消費動向の高まりは、メーカーが政府の規制に適合した革新的なプラスチックフィルム包装に投資する機会を与えています。

ポリエチレン・セグメントが市場で大きなシェアを占める見込み

- ポリエチレンは、柔軟性、高い防湿性、耐久性で有名で、低温下でも優れた性能を誇る。ポリエチレンの際立った特徴は、余分なコーティングを必要とせずに密封できる生来の能力にあります。ポリエチレンは、単独で使用しても、他の素材と組み合わせて使用しても、強力なバリア性を発揮します。さらに、その環境に優しい特性は包装フィルムメーカーの関心を集め、持続可能性への懸念に効果的に対応しています。

- ポリエチレン(PE)は、その多彩な物理的特性が評価され、スペインの主要プラスチック材料として台頭しました。ポリエチレンの人気は、同種のプラスチックとは一線を画す、コスト効率の高い生産に由来します。ポリエチレンは、一次包装用プラスチックの中で最も軟化点が低く、エネルギー消費を削減します。PEを補完するLDPEとLLDPEは、軟包装で顕著です。主にポリ袋、フィルム、ジオメンブレンの製造に使用されるポリエチレンは、その軽量な組成、部分的な結晶化度、耐薬品性、最小限の吸湿性、遮音性といった際立った特性で支持されています。

- 透明包装における製品の視認性がポリエチレン・フィルムの需要を牽引透明包装は消費者の購買決定において極めて重要な要素です。透明包装は多様な業界の購買者を惹きつけ、信頼を育み、売上を押し上げます。購入前に製品を見ることができる消費者は、より購買意欲をそそられます。そのため、ポリエチレンバリアフィルムのメーカーは現在、より大きな市場シェアを確保するために透明性を重視しています。

- ラップ、パウチ、袋状のポリエチレン包装は、特にスペインにおけるeコマースの台頭により、食品の鮮度を保つための重要な選択肢として浮上してきました。この種の包装は、食品を腐敗させることなく長期間鮮度を保つのに役立ち、これは輸送や配達中の品質維持に不可欠です。スペインのeコマース収益は、2022年第2四半期の163億米ドルから2023年第2四半期には184億米ドルに急増しました。この動向は、プラスチックフィルム包装の市場が急成長していることを浮き彫りにしています。プラスチックフィルム包装は、配送中の食品の鮮度維持に重要な役割を果たしています。eコマースが成長を続ける中、ポリエチレン製ラップ、パウチ、バッグのような効果的なパッケージング・ソリューションの需要は増加し、パッケージング業界のさらなる革新と発展を促進すると予想されます。

スペインのプラスチック包装フィルム産業概要

スペインのプラスチック包装フィルム市場は、Berry Global Inc.、Klockner Pentaplast、Luigi Bandera SpAなど、限られた世界的・地域的プレーヤーが半固定化しており、製品の差別化が低く、製品の普及が進み、競争が激しいことを特徴とする競争の激しい市場空間で注目を集めようと競い合っています。

2024年1月-ベリー世界は、従来のPVCフィルムに代わるリサイクル可能なポリエチレンクリンフィルムとして、Omni Xtraの改良版を発表しました。当初は果物、野菜、肉類、鶏肉、惣菜向けに開発された新しいOmni Xtra+フィルムは、耐衝撃性の向上、伸縮性の強化、より安定した延伸プロファイルを誇る。

2023年7月ダウとKlockner Pentaplastは共同で多層真空フィルムKP Flexivacを発表しました。この革新的な製品は特筆すべきマイルストーンを達成した:この革新的な製品は、リサイクルセンターCyclosHTPとリサイクルアライアンスInterserohの両方から100%リサイクル可能なPEとして認定されました。KP Flexivacは、骨付きの生肉や鶏肉のカット肉を包装するために特別に設計されています。密閉シールと堅牢なフィルムにより、最適な食品保護と安全性が確保され、サプライチェーン全体で品質が維持されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションへの需要の高まり

- 各業界における需要の高まりがプラスチックフィルム成長の可能性を示す

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(PP)(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料・スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他最終用途(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- Berry Global Inc.

- Klockner Pentaplast

- SUDPACK Holding GmbH

- Taghleef Industries

- Luigi Bandera SpA

- COMPLEJOS DE VINILO, SA

- EuropeaGroupFilm

- Innovative Film Solutions, SL

- POLIFILM GmbH

第8章 投資分析

第9章 市場の将来

The Spain Plastic Packaging Films Market size is estimated at 0.52 Million tonnes in 2024, and is expected to reach 0.61 Million tonnes by 2029, growing at a CAGR of 3.24% during the forecast period (2024-2029).

Key Highlights

- Spain's urban lifestyle is driving a notable uptick in the demand for convenient packaging. Consumers increasingly opt for lightweight, user-friendly options, compelling vendors to adapt their designs to cater to the growing organized retail sector. By transitioning to lighter materials, such as flexible pouches, vendors meet these changing demands and enjoy significant energy-saving benefits. Moreover, the industry's move toward sustainable packaging solutions resonates with the rising consumer consciousness for eco-friendly products. This alignment is poised to spur heightened innovation and competition within the packaging landscape.

- Spain's packaging industry is witnessing robust growth, driven by a strong economy that's empowering consumers to opt for premium products, often showcased in innovative packaging. Moreover, there's a notable uptick in the demand for compact, on-the-go packaging, especially in pouch formats, driven by the country's busy professionals. This trend isn't confined to a single sector; industries ranging from food, FMCG, and groceries to cosmetics are all set to increase their usage of pouch packaging. As a result, solution providers are intensifying their innovation efforts to enhance their market presence and offer more appealing products.

- Consumers increasingly favor products with longer shelf lives, motivated by convenience and a heightened awareness of food waste. Plastic film packaging boasts superior barrier properties and safeguards items from moisture, oxygen, light, and other factors that could compromise their quality and freshness. This makes it a crucial tool in extending the shelf life of perishable goods, ranging from food and beverages to pharmaceuticals and personal care items. France is actively addressing its reliance on single-use plastics, especially in the fresh produce retail sector. In response, a recent law has been enacted banning the use of plastic film and netting.

- As part of Europe's economic recovery and policy development, a "plastic levy" law has been introduced, linking fees to the non-recycled plastic packaging waste generated by each EU Member State. Spain responded by enacting the Special Tax on Non-Reusable Plastic Packaging (Law 7/2022), effective from January 2023. This tax was designed to enhance waste management, combat soil contamination, and promote a circular economy. Applicable across Spain, the law requires manufacturers, importers, and transporters of single-use plastic containers to reassess their material choices. These stringent measures present a notable challenge to Spain's plastics industry, aligning with the EU's broader goal of reducing environmental impact and advancing a circular economy, ultimately driving innovation and sustainability in packaging.

- Spain is actively combatting the widespread use of single-use plastics, particularly in the fresh produce retail sector. A recent law has been enacted, specifically targeting plastic film and netting, with the primary goal of slashing plastic waste and fostering the adoption of sustainable packaging. As a result, this legislation is set to tighten the market for plastic packaging films in Spain, directly impacting manufacturers and suppliers entrenched in this segment. Aligned with a broader push toward a circular economy, the law champions the shift to biodegradable and reusable materials. This transition is anticipated to fuel innovation within the packaging realm as businesses strive to craft eco-conscious solutions that align with the updated mandates.

Spain Plastic Packaging Films Market Trends

Meat, Poultry, And Seafood segment to Hold Significant Market Share

- Plastic film packaging, available in pouches, bags, films, and wraps, offers versatility in accommodating diverse cuts, portion sizes, and packaging formats in the meat, poultry, and fish industries. This versatility ensures efficient packaging, spanning from whole cuts to processed items like sausages and fillets. In addition, plastic film packaging provides benefits such as extended shelf life, improved product visibility, and enhanced protection against contamination and spoilage, making it a preferred choice for manufacturers and consumers.

- Spain has witnessed a notable surge in beef, pork, poultry, and seafood consumption and production in recent years. This uptick is fueled by a rising demand for packaging that is both consumer-friendly and enhances product protection. Consequently, meat, poultry, and seafood packaging has emerged as a cost-effective and practical solution. Forecasts suggest a rise in plastic packaging sales in the coming years. This uptick is primarily attributed to heightened hygiene awareness and the necessity for packaging solutions that prolong shelf life and maintain the inherent qualities of meat and poultry, which are crucial for both domestic consumption and export markets.

- In 2023, Spain saw a notable rise in the export value of poultry meat and edible offal, increasing from USD 515.7 million to USD 551.3 million. This surge in demand is driving a trend toward utilizing specialized plastic films for meat packaging, ensuring freshness during transit. These plastic films are designed to provide a barrier against contaminants and extend the shelf life of the meat, making them essential for maintaining quality during transportation and storage. In addition, the increased export value reflects a growing global appetite for Spanish poultry products, which in turn necessitates advancements in packaging technology to meet international standards and consumer expectations.

- Spain ranks third in Europe in terms of fish and meat consumption, trailing only Portugal and Norway. A Seafood Council survey reveals that 70% of Spaniards enjoy fish twice weekly, with 90% having it at least once. Hake, salmon, cod, sole, sea bass, tuna, and swordfish are favored fish. On the meat front, Spain's Ministry of Agriculture reports an average per capita meat consumption of 1349 grams daily. Poultry leads the meat choices, with an average daily consumption of 38 grams per person, closely followed by pork and beef. In addition, Spaniards consume an average of 32 grams of processed meat daily, with cooked or cured ham being the favorite. This rising consumption trend presents opportunities for manufacturers to invest in innovative plastic film packaging that complies with government regulations.

Polyethylene Segment Expected to Hold Significant Share in the Market

- Polyethylene, renowned for its flexibility, high moisture barrier, and durability, also boasts exceptional performance in low temperatures. Its standout feature lies in its innate ability to seal without needing extra coatings. Whether utilized independently or in conjunction with other materials, polyethylene creates a formidable barrier. Furthermore, its eco-friendly attributes garner heightened interest among packaging film manufacturers, effectively addressing sustainability concerns.

- Polyethylene (PE) emerged as the leading plastic material in Spain, valued for its versatile physical properties. Its popularity stems from its cost-effective production, distinguishing it from its plastic counterparts. Polyethylene has the lowest softening point among primary packaging plastics, reducing energy consumption. Complementing PE, LDPE, and LLDPE are prominent in the flexible packaging. Primarily used in crafting plastic bags, films, and geomembranes, polyethylene is favored for its lightweight composition, partial crystallinity, and standout attributes like chemical resistance, minimal moisture absorption, and sound insulation.

- Product Visibility in Transparent Packaging Drives Demand for Polythene Films. Transparent packaging is a pivotal factor in consumer purchasing decisions. It attracts buyers across diverse industries, fosters trust, and boosts sales. Consumers who can view the product before purchase are more inclined to make a purchase. Consequently, manufacturers of polyethylene barrier films are now emphasizing transparency to secure a more significant market share.

- Polyethylene packaging, in the form of wraps, pouches, and bags, has emerged as a significant choice for preserving food freshness, especially with the rise of e-commerce in Spain. This type of packaging helps keep food fresh for extended periods without spoilage, which is crucial for maintaining quality during transportation and delivery. The country's e-commerce revenue surged from USD 16.3 billion in Q2 2022 to USD 18.4 billion in Q2 2023. This trend underscores a burgeoning market for plastic film packaging, which plays a vital role in ensuring that food products remain fresh and intact during deliveries. As e-commerce continues to grow, the demand for effective packaging solutions like polyethylene wraps, pouches, and bags is expected to increase, driving further innovation and development in the packaging industry.

Spain Plastic Packaging Films Industry Overview

The Spain plastic packaging films market is semi-consolidated with limited global and regional players, such as Berry Global Inc., Klockner Pentaplast, Luigi Bandera SpA, and others vying for attention in a contested market space characterized by low product differentiation, growing product penetration, and high competition.

January 2024 -Berry Global unveiled an enhanced iteration of its Omni Xtra polyethylene cling film, positioning it as a certified recyclable substitute for conventional PVC options. Initially tailored for fruits, vegetables, meats, poultry, and deli items, the new Omni Xtra+ film boasts heightened impact resistance, enhanced elasticity, and a more consistent stretching profile.

July 2023 - Dow and Klockner Pentaplast have jointly introduced KP Flexivac, a multi-layer vacuum film. This innovative product has achieved a notable milestone: It has been certified as 100% recyclable PE by both the recycling center CyclosHTP and the recycling alliance Interseroh. KP Flexivac is designed explicitly to package bone-in fresh meat and poultry cuts. Its hermetical seal and robust film ensure optimal food protection and safety, maintaining quality across the entire supply chain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Rising Demand Across Industries Signals Growth Potential for Plastic Films

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation Towards Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-User Industry

- 6.2.1 Food

- 6.2.1.1 Candy & Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, And Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care & Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-use Industry Applications (Agricultural, Chemical, Etc)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- 7.1.2 Berry Global Inc.

- 7.1.3 Klockner Pentaplast

- 7.1.4 SUDPACK Holding GmbH

- 7.1.5 Taghleef Industries

- 7.1.6 Luigi Bandera SpA

- 7.1.7 COMPLEJOS DE VINILO, SA

- 7.1.8 EuropeaGroupFilm

- 7.1.9 Innovative Film Solutions, SL

- 7.1.10 POLIFILM GmbH