|

市場調査レポート

商品コード

1550219

イタリアのプラスチック包装フィルム:市場シェア分析、産業動向、成長予測(2024年~2029年)Italy Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアのプラスチック包装フィルム:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

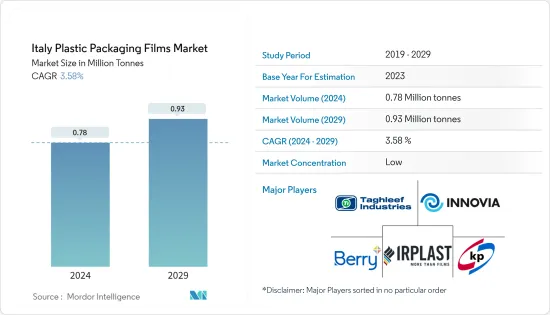

イタリアのプラスチック包装フィルム市場規模は2024年に78万トンと推定され、2029年には93万トンに達し、予測期間(2024-2029年)のCAGRは3.58%で成長すると予測されます。

主なハイライト

- イタリアの包装セクターは、経済的課題を乗り越えてきただけでなく、他の多くの重要産業よりも優れた業績を上げてきました。近年は、食品包装や高級品の大手企業に後押しされ、顕著に進歩しています。特に、プラスチックフィルム包装は、その品質、柔軟性、バリア機能、印刷機能、環境への優しさ、充実したサービス提供が評価され、食品分野での採用が急増しています。技術の先進化と持続可能なパッケージング・ソリューションに対する消費者の需要の高まりが、この成長をさらに後押ししています。

- イタリアの包装セクターは、経済的課題を乗り越えてきただけでなく、他の多くの重要な産業よりも優れた業績を上げてきました。近年は、食品包装や高級品の大手企業に後押しされ、顕著に先進パッケージングが進んでいます。この成長は、技術革新、戦略的投資、持続可能性への注力によるものです。特に、プラスチックフィルム包装は、その品質、柔軟性、バリア機能、印刷機能、環境に優しい、充実したサービス提供が評価され、食品分野での採用が急増しています。さらに、消費者の嗜好の変化や規制要件への適応能力も、市場での地位をさらに強固なものにしています。

- さらに、イタリアの都会的なライフスタイルが、便利なパッケージに対する需要の顕著な上昇を促しています。消費者はますます軽量で使い勝手の良いものを選ぶようになり、ベンダーは組織化された小売セクターの成長に対応できるようなデザインへの転換を迫られています。フレキシブルパウチのような軽い素材に移行することで、ベンダーはこうした需要の変化に対応し、大幅な省エネ効果を享受しています。さらに、持続可能なパッケージング・ソリューションに向けた業界の動きは、消費者の意識の高まりや環境に優しい製品への嗜好と共鳴しています。この一致は、包装情勢における技術革新と競合の激化に拍車をかける態勢を整えています。

- 単一使用プラスチック指令(SUPD)を実施するイタリアの立法令は、2022年に施行されました。SUPDとは大きく異なり、イタリア政令はより柔軟なプラスチックの定義を提供し、特定の使い捨てプラスチック(SUP)の禁止を延期し、特定の生分解性素材と堆肥化可能素材に適用除外を認めています。その結果、この法律はイタリアのプラスチック包装フィルム市場を引き締め、この分野で確固たる地位を築いているメーカーやサプライヤーに直接的な影響を与えることになります。この法律は、循環型経済への幅広い推進に沿い、生分解性で再利用可能な材料の採用を促進することを目的としています。この移行は、企業が新たな規制基準を満たすために環境に優しいソリューションに軸足を移すことで、包装分野での技術革新に拍車をかけると思われます。

- 同地域ではプラスチック包装に関する厳しい法律が施行されているが、賢明な企業はこうした規制を技術革新の足がかりと考えています。最先端のリサイクル方法を開拓し、バイオベースのプラスチックフィルムを導入することで、企業は環境規制に沿い、持続可能なソリューションに飢えた市場でニッチを切り開く。この2つのアプローチは、規制上の要求を満たすとともに、拡大する消費者層の共感を呼び、ブランドイメージを高めて市場拡大に弾みをつける。

イタリアのプラスチック包装フィルム市場動向

食品分野が大きな市場シェアを占める

- プラスチックフィルムはイタリアの食品産業において、保存性を高め、湿気や酸素などの外的要因から製品を保護する重要な役割を担っています。新たな用途によって進化する食品包装の需要は、仕様の改善を後押ししています。重要な焦点は、より堅牢なパッケージングを実現するための先進バリアフィルムの開発です。包装フィルムのバリア特性を向上させることは、食品の保存期間を延ばし、腐敗や損傷のリスクを軽減するために不可欠です。

- イタリアの食欲の高まりは、様々な食品に合わせた特殊プラスチックフィルムの需要増加の重要な原動力となっています。食品の安全性を確保し、賞味期限を延ばし、製品の視覚的魅力を高めるパッケージングに対するニーズが、この需要増に拍車をかけています。消費者が健康と利便性を重視するにつれて、食品包装のプラスチックフィルム市場は大幅な上昇を経験しており、技術革新と市場拡大の扉を開いています。

- さらに、材料科学と製造技術の進歩により、業界はより持続可能で効率的なプラスチックフィルムソリューションの出現を目の当たりにしており、市場の成長をさらに後押ししています。食料品を購入する際のeコマースへのシフトが加速していることも、耐久性と信頼性の高いパッケージング・ソリューションへのニーズを高めています。

- さらにイタリアでは、焼き菓子、菓子類、コンビニエンス・フードへの嗜好が高まっており、軟包装、特にポリエチレン・バリア・フィルムへのニーズが高まっています。ポリエチレンバリアフィルムは、その水分バリア機能で知られ、製品の賞味期限を延ばす上で極めて重要です。イタリアの消費者は入手しやすい包装を好むため、プラスチックフィルムソリューションは、特に調理済み食品やコンビニエンス食品において、圧倒的な選択肢となっています。

- 2023年には、イタリアでは家庭外での食品への支出が12%急増し、総額995億米ドルに達しました。この回復は、COVID-19パンデミックの影響からの回復を示すものでした。家庭外での食品消費の増加は、外食の頻度を高める方向への消費者行動の変化を示しています。逆に、家庭で消費される食品への支出は、2021年の1,839億米ドルから2023年には最高値の2,110億米ドルに達します。家庭での食品支出のこの増加は、家庭料理への嗜好の持続を反映しています。家庭外食品消費と家庭内食品消費の両分野では、消費者の需要を満たすためにそれぞれ異なる包装ソリューションが必要となるため、この動向はさまざまな食品包装ニーズにおけるプラスチックフィルムの需要に大きな影響を与えるとみられます。

バイオプラスチックセグメントが市場で大きなシェアを占める見込み

- バイオプラスチックはその環境に優しい性質が評価され、安全な代替包装を提供しています。バイオプラスチックの特定の種類は、容易な生分解性を誇っています。広く採用されており、食品や医薬品から飲食品まで、様々な製品の包装に応用されています。食用だけでなく、ナプキンやティッシュのような非食品にも利用されています。さらに、食品を包むのに欠かせない段ボールや紙、コップやお皿の材料としても、バイオプラスチックは重要な役割を果たしています。バイオプラスチックの多用途性は、フレキシブル包装とルーズフィル包装の間でシームレスに移行することで発揮されます。

- イタリアでは、プラスチック袋の製造にバイオプラスチックの採用が急増しています。これらの環境に優しい袋は、特に有機廃棄物の収集に広く利用されています。その用途は、病院、ホテル、レストラン、商業施設、小売店、家庭など多岐にわたる。さらに、いくつかの地方自治体がバイオプラスチックの利用を推奨しています。

- イタリアのバイオプラスチック包装材の消費量は増加しており、2022年には7万9,200トンに達します。この増加は、持続可能なパッケージング・ソリューションへの傾向の高まりを反映しています。2022年から2025年にかけては、環境意識の高まりと環境に優しい素材への規制支援により、さらに10%の成長が見込まれます。バイオプラスチックへのシフトは、より環境に優しい代替品を求める消費者の需要や、バイオプラスチック技術の進歩も影響しており、これらの素材はコストと性能の面で従来のプラスチックとの競合を高めています。

- イタリアの環境規制の強化とプラスチック汚染に対する意識の高まりは、近い将来バイオプラスチックの需要を急増させると思われます。プラスチック廃棄物を削減するための政府の厳しい政策と、持続可能な代替品に対する消費者の嗜好は、バイオプラスチック市場をさらに強化すると予想されます。さらに、バイオプラスチックの技術や生産プロセスの進歩により、様々な産業でバイオプラスチックの魅力が高まり、採用が進むと予想されます。

イタリアのプラスチック包装フィルム産業概観

イタリアのプラスチック包装フィルム市場は断片化されており、Irplast SpA、Berry Global Inc.、Klockner Pentaplast、SUDPACK Holding GmbHなど、複数の世界的・地域的プレーヤーが、製品の差別化が低く、製品の普及が進み、競争が激しいことを特徴とする競合市場において、注目度を競っています。

- 2024年1月ベリー世界はOmni Xtraポリエチレンクリンフィルムの改良版を発表し、従来のPVC代替品としてリサイクル可能であることを証明しました。当初は果物、野菜、肉類、鶏肉、惣菜向けに開発された新しいOmni Xtra+フィルムは、高い耐衝撃性、強化された伸縮性、より安定した延伸プロファイルを誇る。

- 2023年7月ダウとKlockner Pentaplastは共同で多層真空フィルムKP Flexivacを発表。この革新的な製品は特筆すべきマイルストーンを達成しました。リサイクルセンターCyclosHTPとリサイクルアライアンスInterserohから100%リサイクル可能なPEとして認定されました。KP Flexivacは、骨付きの生肉や鶏肉のカット肉を包装するために特別に設計されています。密封シールと堅牢なフィルムにより、最適な食品保護と安全性が確保され、サプライチェーン全体にわたって品質が維持されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションへの需要の高まり

- 各業界における需要の高まりがプラスチックフィルム成長の可能性を示す

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(PP)(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料、スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他最終用途(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- Irplast SpA

- Innovia Films(CCL Industries Inc.)

- Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- Berry Global Inc.

- Klockner Pentaplast

- SUDPACK Holding GmbH

- Taghleef Industries

- Jindal Films Europe

- SRF LIMITED

- VALTEC ITALIA SRL

- Cartonal Italia SpA

- Luigi Bandera SpA

- IDEALPLAST SRL

- COMPLEJOS DE VINILO SA

- POLIFILM GmbH

第8章 投資分析

第9章 市場の将来

The Italy Plastic Packaging Films Market size is estimated at 0.78 Million tonnes in 2024, and is expected to reach 0.93 Million tonnes by 2029, growing at a CAGR of 3.58% during the forecast period (2024-2029).

Key Highlights

- The packaging sector in Italy has not only weathered economic challenges but has also outperformed many other vital industries. It has notably advanced in recent years, propelled by leading players in food packaging and luxury goods. Notably, plastic film packaging is witnessing a surge in adoption within the food sector, lauded for its quality, flexibility, barrier features, print capabilities, eco-friendliness, and enhanced service offerings. Technological advancements and increasing consumer demand for sustainable packaging solutions further support this growth.

- The packaging sector in Italy has not only weathered economic challenges but has also outperformed many other vital industries. It has notably advanced in recent years, propelled by leading players in food packaging and luxury goods. This growth is attributed to innovations, strategic investments, and a focus on sustainability. Notably, plastic film packaging is witnessing a surge in adoption within the food sector, lauded for its quality, flexibility, barrier features, print capabilities, eco-friendliness, and enhanced service offerings. Additionally, the sector's ability to adapt to changing consumer preferences and regulatory requirements has further solidified its position in the market.

- Further, Italy's urban lifestyle is driving a notable uptick in the demand for convenient packaging. Consumers increasingly opt for lightweight, user-friendly options, compelling vendors to adapt their designs to cater to the growing organized retail sector. By transitioning to lighter materials, such as flexible pouches, vendors meet these changing demands and enjoy significant energy-saving benefits. Moreover, the industry's move toward sustainable packaging solutions resonates with the rising consumer consciousness and preference for eco-friendly products. This alignment is poised to spur heightened innovation and competition within the packaging landscape.

- The Italian Legislative Decree, which implemented the Single-Use Plastic Directive (SUPD), came into force in 2022. Diverging significantly from the SUPD, the Italian Decree offers a more flexible plastic definition, postpones the ban on certain single-use plastics (SUPs), and grants exemptions for specific biodegradable and compostable materials. Consequently, this legislation is set to tighten the market for plastic packaging films in Italy, directly impacting manufacturers and suppliers entrenched in this segment. Aligned with a broader push toward a circular economy, the law aims to promote the adoption of biodegradable and reusable materials. This transition will spur innovation within the packaging sector as companies pivot toward eco-friendly solutions to meet the new regulatory standards.

- Although the region enforces strict laws on plastic packaging, savvy companies see these regulations as a springboard for innovation. By pioneering cutting-edge recycling methods and introducing bio-based plastic films, firms align with environmental mandates and carve out a niche in a market hungry for sustainable solutions. This dual approach satisfies regulatory demands and resonates with a growing consumer base, bolstering brand image and fueling market expansion.

Italy Plastic Packaging Films Market Trends

Food Segment to Hold Significant Market Share

- Plastic films are crucial in Italy's food industry, enhancing shelf life and shielding products from external factors like moisture and oxygen. Evolving food packaging demands, driven by new applications, are pushing for improved specifications. A critical focus is developing advanced barrier films to create more robust packaging. Improving the barrier properties of packaging films is essential to prolonging food shelf life and mitigating spoilage and damage risks.

- Italy's growing appetite for food is a crucial driver behind the rising demand for specialized plastic films tailored to different food products. This upsurge is fueled by the need for packaging that ensures food safety, extends shelf life, and enhances product visual appeal. As consumers place a higher premium on health and convenience, the plastic film market in food packaging is experiencing a significant uptick, opening doors for innovation and market expansion.

- Moreover, with advancements in material science and manufacturing technologies, the industry is witnessing the emergence of more sustainable and efficient plastic film solutions, further bolstering market growth. The escalating shift toward e-commerce for grocery purchases also amplifies the need for durable and trustworthy packaging solutions.

- Further, in Italy, a growing preference for baked goods, confectionery, and convenience foods is fueling the need for flexible packaging, particularly polyethylene barrier films. These films, known for their moisture-barrier capabilities, are pivotal in prolonging product shelf life. With Italian consumers favoring easily accessible packaging, plastic film solutions are the dominant choice, especially for ready-to-eat and convenience foods.

- In 2023, Italy saw a 12% surge in household spending on food outside the home, reaching a total of USD 99.5 billion. This rebound marked a recovery from the effects of the COVID-19 pandemic. The increase in out-of-home food consumption indicates a shift in consumer behavior towards dining out more frequently. Conversely, spending on food consumed at home hit a high of USD 211 billion in 2023, up from USD 183.9 billion in 2021. This rise in at-home food expenditure reflects a sustained preference for home-cooked meals. This trend is poised to significantly impact the demand for plastic films in various food packaging needs, as both sectors-out-of-home and at-home food consumption require different packaging solutions to meet consumer demands.

Bioplastic Segment Expected to Hold Significant Share in the Market

- Lauded for their eco-friendly nature, bioplastics offer a safe packaging alternative. Specific variants of bioplastics boast easy biodegradability. Widely adopted, they find applications in packaging various products, from food and medicines to beverages. Beyond edibles, they extend their utility to non-food items such as napkins and tissues. Moreover, bioplastics play a pivotal role in crafting materials like cardboard and paper, which are essential for food wrapping, and in producing cups and plates. Their versatility shines as they seamlessly transition between flexible and loose-fill packaging solutions.

- The adoption of bioplastics for plastic bag production is surging in Italy. These eco-friendly bags find widespread utility, especially in collecting organic waste. Their applications span diverse settings, including hospitals, hotels, restaurants, commercial establishments, retail outlets, and households. Moreover, several regional governments have joined in, endorsing the utilization of bioplastics for such initiatives.

- Italy's bioplastic packaging consumption has risen, reaching 79.20 thousand tons in 2022. This increase reflects a growing trend toward sustainable packaging solutions. Projections indicate a further 10% growth from 2022 to 2025, driven by heightened environmental awareness and regulatory support for eco-friendly materials. The shift toward bioplastics is also influenced by consumer demand for greener alternatives and advancements in bioplastic technology, which have made these materials more competitive with traditional plastics in terms of cost and performance.

- Italy's increasing environmental regulations and heightened awareness of plastic pollution are set to drive a surge in demand for bioplastics in the near future. The government's stringent policies to reduce plastic waste and consumer preference for sustainable alternatives are further expected to bolster the bioplastics market. Additionally, advancements in bioplastic technology and production processes are expected to enhance the material's appeal and adoption across various industries.

Italy Plastic Packaging Films Industry Overview

The Italian plastic packaging films market is fragmented, with several global and regional players, such as Irplast SpA, Berry Global Inc., Klockner Pentaplast, and SUDPACK Holding GmbH, vying for attention in a contested market space characterized by low product differentiation, growing product penetration, and high competition.

- January 2024: Berry Global unveiled an enhanced iteration of its Omni Xtra polyethylene cling film, positioning it as a certified recyclable substitute for conventional PVC options. Initially tailored for fruits, vegetables, meats, poultry, and deli items, the new Omni Xtra+ film boasts heightened impact resistance, enhanced elasticity, and a more consistent stretching profile.

- July 2023: Dow and Klockner Pentaplast jointly introduced KP Flexivac, a multi-layer vacuum film. This innovative product has achieved a notable milestone. It has been certified as 100% recyclable PE by the recycling center CyclosHTP and the recycling alliance Interseroh. KP Flexivac is designed explicitly to package bone-in fresh meat and poultry cuts. Its hermetical seal and robust film ensure optimal food protection and safety, maintaining quality across the entire supply chain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Rising Demand Across Industries Signals Growth Potential for Plastic Films

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation Toward Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy and Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, and Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings and Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care and Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-use Industry Applications (Agricultural, Chemical, Etc.)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Irplast SpA

- 7.1.2 Innovia Films (CCL Industries Inc.)

- 7.1.3 Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- 7.1.4 Berry Global Inc.

- 7.1.5 Klockner Pentaplast

- 7.1.6 SUDPACK Holding GmbH

- 7.1.7 Taghleef Industries

- 7.1.8 Jindal Films Europe

- 7.1.9 SRF LIMITED

- 7.1.10 VALTEC ITALIA SRL

- 7.1.11 Cartonal Italia SpA

- 7.1.12 Luigi Bandera SpA

- 7.1.13 IDEALPLAST SRL

- 7.1.14 COMPLEJOS DE VINILO SA

- 7.1.15 POLIFILM GmbH