|

市場調査レポート

商品コード

1630344

ポリプロピレン包装フィルム:市場シェア分析、産業動向、成長予測(2025~2030年)Polypropylene Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリプロピレン包装フィルム:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

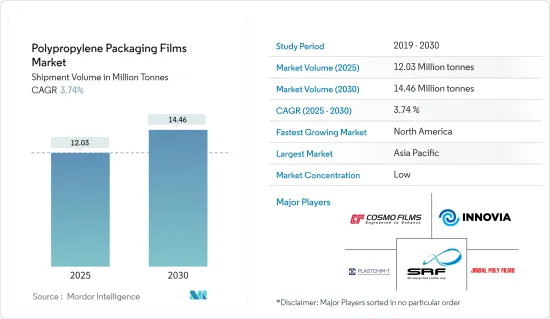

出荷量ベースのポリプロピレン包装フィルム市場規模は、予測期間中(2025~2030年)にCAGR 3.74%で、2025年の1,203万トンから2030年には1,446万トンに成長すると予測されます。

軟質プラスチック包装は、ポリプロピレン包装フィルム市場の著しい成長セグメントの1つです。プラスチックの最良の品質を組み合わせ、少ない材料で幅広い保護特性を与える包装フィルムは、食品と食品に関連しないその他の製品の付加価値と市場性を高めるものです。

包装産業は、消費者の要求の変化に対応するために絶えず適応しています。可処分所得の増加や中間層の急増といった主要要因が、消費財、飲食品、工業製品など様々なセグメントにおけるポリプロピレン包装フィルムの需要に拍車をかけています。

さらに、持続可能性がますます重視されるようになり、従来の硬質包装ソリューションが革新的で環境に優しい軟質プラスチック包装に取って代わられつつあります。このシフトは、ユーザーフレンドリーな包装や製品保護強化への意欲の高まりと相まって、ポリプロピレン包装フィルムの需要を高めることになると考えられます。

ポリプロピレンは、PEよりも融点が高く、多くの用途に使用できることから、軟質包装セグメントで牽引役となっています。さらに、再利用可能な包装から使い捨て包装への世界のシフトは、ポリプロピレンフィルムの需要を強化すると予想されています。

製品の保存期間を延ばすフィルムに対する需要の高まりが、ポリプロピレン包装フィルム市場の成長を後押ししています。また、環境に優しい代替包装材が容易に入手できるようになったことで、ポリプロピレンフィルムの用途が広がり、市場の拡大にさらに拍車をかけています。

2024年4月、AmcorとKimberly Clarkは提携し、30%リサイクル材料を使用したEco Protect紙おむつの新包装をペルーで発売しました。この低アレルギー性紙おむつ包装は、植物由来の繊維から作られ、リサイクル材料を含むため、持続可能性が促進されます。Amcorは、Kimberly Clarkのためにこの革新的な包装の設計と製造を主導し、循環型経済へのコミットメントを強調しました。

しかし、市場は、パンデミックの影響によるサプライチェーンと製造施設の大きな混乱に悩まされています。加えて、エネルギー危機による原料費の高騰が市場成長の潜在的脅威となっています。

ポリプロピレン包装フィルムの市場動向

BOPPフィルムが大きな成長を遂げる

- BOPPフィルムは、機械的・手作業的な延伸プロセスを経てクロス方向に延伸されます。共押出構造を特徴とするこのフィルムは、透明、不透明、金属化が可能です。BOPPフィルムの多様性と利点は、包装産業において金属缶やカートンの代替品となる可能性を秘めています。BOPPフィルムは、蝋引き紙やアルミ箔の優れた代替品であり、高い引張強度、低い伸び、優れたガスバリア性、剛性の向上、ヘイズの低減を実現します。

- 実用的なソリューションと便利な輸送を求める消費者の需要に後押しされ、BOPPフィルムの需要が急増しています。食品包装の厳しい要件を考えると、BOPPフィルムは需要増加の態勢を整えています。

- BOPP単層ウェブやラミネートは、石鹸や歯ブラシのような商品を包むために、パーソナルケアや家庭用ケア産業で一般的に使用されています。それ以外にも、このフィルムは卓越した耐薬品性、平坦な表面積、UVカットを誇っています。リサイクル可能で無害なため、人気と需要が高まっています。さらに、水蒸気、油、グリースに対する強固なバリアを記載しています。

- BOPPフィルムは、その密封能力と酸素バリアとしての役割から、製薬産業や化粧品産業でますます好まれています。この動向は、2023年の世界の化粧品市場における北米のシェアが29%であることからも明らかです。

- 特筆すべきは、BOPPフィルムは他のプラスチックフィルムよりも環境フットプリントが小さいことです。融点が低いため、加工時のエネルギー消費量が少なくて済みます。BOPPフィルムはポリエチレンとのラミネートが容易で、幅広いポリオレフィン化学グループの一員として幅広いリサイクル性を維持しています。

- ポリプロピレン包装フィルム市場の主要企業は、BOPPフィルムの生産を強化しています。例えば、トッパンは2024年3月、環境に優しい革新的なバリアフィルム「GL-SP」をインドで発売すると発表しました。インドのTOPPAN Speciality Films(TSF)と共同で開発されたこの製品は、二軸延伸ポリプロピレン(BOPP)をベースとしています。

アジア太平洋が最大の市場シェアを占める

- アジア太平洋ではプラスチック材料へのアクセスが便利であることが、ポリプロピレン包装フィルムの成長を大きく後押ししています。同地域では、プラスチック包装の使用動向が高まっています。India Brand Equity Foundationの2024年7月の報告書によると、インド商工省はインド西部のプラスチック消費量が47%を占め、北部が23%、南部が21%と続くと強調しています。この消費を牽引している主要産業は、自動車、包装、電化製品などです。中国はプラスチック包装の極めて重要な市場として際立っているが、その成長を妨げる可能性のある法規制の禁止という課題に直面しています。

- 包装食品や調理済み食品の需要増とeコマースの急速な拡大が、ポリプロピレン包装フィルムの需要を押し上げています。飲食品、医薬品、パーソナルケアなどの産業では、軟質包装ソリューションへの傾斜がますます強まっています。ポリプロピレンフィルムの魅力は、その優れたバリア性、耐久性、視覚的魅力にあり、様々な包装用途に理想的です。

- 急増する中産階級と組織小売業の台頭は、軟包装産業の成長にとって重要な触媒です。特定の世界包装要件を伴う輸出急増は、包装産業をさらに活性化させています。アジア太平洋の包装情勢を支配しているプラスチック軟包装は、伝統的硬質包装ユーザーの間でさえシフトを確認しています。ポリプロピレン包装フィルムの拡大の顕著な原動力は、便利な包装と合理的なラミネート量で提供される製品に対する消費者の嗜好です。

- 食品加工産業への投資拡大や農作物の廃棄を最小限に抑える取り組みにより、包装された食品や野菜の需要が増加し、ポリプロピレン包装フィルムのニーズが高まっている

- カナダ農業食糧省の報告によると、即席麺を含む中国の包装食品の売上高は、2026年までに約166億6,000万米ドルに達すると予測されています。このデータは、同国の加工包装食品市場が一貫して上昇傾向にあることを示しています。この動向は今後も続き、ポリプロピレン包装フィルムの需要にプラスの影響を与えると予想されます。

ポリプロピレン包装フィルム産業概要

ポリプロピレン包装フィルム市場は、国内外を問わず多くの参入企業がビジネスを展開しているため競合が激しいです。市場はセグメント化されています。Jindal Poly Films Ltd、CCL Industries(Innovia Films)、Cosmo Films Ltd、SRF Limited、Plastchim-Tなど、ポリプロピレン包装フィルム市場の主要企業は、潜在的な混乱に対処し、長期的な持続的成長を確保するため、新製品の開発と機敏なビジネスモデルの採用に注力しています。市場の主要開発をいくつか発表します。

2024年5月Plastchim-TはManucor SpAを買収し、BOPPの生産量と軟質包装の専門知識を大幅に獲得しました。この買収により、生産能力は年間20万トンとなり、欧州の輸送・配送ネットワークが強化されます。

2024年3月:プラスチックメーカーであるInteplast Groupは、サウスカロライナ州Gray Court、テキサス州Lolita、テネシー州Morristownにある3つのBOPPフィルム工場でISCC PLUS認証を取得。この認証により、Inteplastは北米で初めてISCC PLUS認証を取得したBOPPフィルムメーカーのひとつとなります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 費用対効果の高い包装形態への需要の高まり

- 軟質包装の要件に道を開く環境規制

- 包装食品市場の成長

- 市場抑制要因

- 原料価格の変動

第6章 COVID-19の市場への影響

第7章 市場セグメンテーション

- タイプ別

- BOPP

- CPP

- 用途別

- 食品

- 飲料

- 医薬品・医療

- 工業用

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- アジア

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第8章 競合情勢

- 企業プロファイル

- Plastchim-T

- Jindal Poly Films Ltd

- CCL Industries(Innovia Films)

- SRF Limited

- Cosmo Films Ltd

- Amcor PLC

- UFlex Limited

- Taghleef Industries LLC

- Berry Global Inc.

- Polyplex Corporation Limited

- ProAmpac LLC

- Inteplast Group

- Toray Plastics(America)Inc.

- Profol GmbH

- Napco National

- Oben Holding Group

第9章 投資分析

第10章 今後の動向

The Polypropylene Packaging Films Market size in terms of shipment volume is expected to grow from 12.03 million tonnes in 2025 to 14.46 million tonnes by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

Flexible plastic packaging is one of the significant growing segments of the polypropylene packaging film market. Packaging films, which combine the best qualities of plastics to give a wide range of protective characteristics while using little material, are an added value and marketability for foodstuffs and other products not related to food.

The packaging industry continually adapts to meet the changing demands of consumers. Key drivers, such as rising disposable incomes and a burgeoning middle-class population, fuel the demand for polypropylene packaging films across various sectors, including consumer goods, food and beverages, and industrial products.

Moreover, with an increasing emphasis on sustainability, traditional rigid packaging solutions are being replaced by innovative, eco-friendly, flexible plastic packaging. This shift, combined with a growing appetite for user-friendly packaging and enhanced product protection, is set to elevate the demand for polypropylene packaging films.

Polypropylene has gained traction in the flexible packaging domain, primarily due to its higher melting point than PE, making it versatile for numerous applications. Additionally, the global shift from reusable to disposable packaging is anticipated to bolster the demand for polypropylene films.

The rising demand for films that extend product shelf life is propelling the growth of the polypropylene packaging film market. Also, the easy availability of eco-friendly packaging alternatives is broadening the applications of polypropylene films, further fueling market expansion.

In April 2024, Amcor and Kimberly Clark teamed up to launch a new packaging for their Eco Protect diapers in Peru, featuring 30% recycled materials. This hypoallergenic diaper packaging is made from plant-based fibers and includes recycled materials, promoting sustainability. Amcor took the lead in designing and producing this innovative packaging for Kimberly Clark, underscoring the commitment to a circular economy.

However, the market grapples with significant disruptions in its supply chain and manufacturing facilities, a fallout from the pandemic. Additionally, soaring raw material costs due to the energy crisis pose a potential threat to market growth.

Polypropylene Packaging Films Market Trends

BOPP Films to Witness Major Growth

- BOPP films undergo mechanical and manual stretching through a cross-direction process. These films, featuring coextruded structures, can be transparent, opaque, or metalized. The versatility and benefits of BOPP films position them as potential replacements for metal cans and cartons in the packaging industry. BOPP films are excellent alternatives to waxed paper and aluminum foil, offering higher tensile strength, lower elongation, superior gas barriers, increased stiffness, and reduced haze.

- Driven by consumer demand for practical solutions and convenient transport, BOPP films are witnessing a surge in demand. Given the stringent requirements in food packaging, BOPP films are poised for increased demand, mainly because they help preserve food's nutritional properties until consumption.

- Commonly used in the personal and household care industry, BOPP monolayer webs and laminates wrap items like soap and toothbrushes. Beyond this, the film boasts exceptional chemical resistance, a flat surface area, and UV protection. Its recyclability and non-toxic emissions have fueled its rising popularity and demand. Moreover, it offers robust barriers against water vapor, oil, and grease.

- Due to their sealing capabilities and role as an oxygen barrier, BOPP films are increasingly favored in the pharmaceutical and cosmetic industries. This trend is underscored by North America's 29% share of the global cosmetic market in 2023.

- Notably, BOPP films present a smaller environmental footprint than other plastic films. Their low melting point translates to reduced energy consumption during transformation. BOPP films easily laminate with polyethylene and maintain wide recyclability as part of the broader polyolefin chemical group.

- Key players in the polypropylene packaging films market are ramping up BOPP film production. For example, in March 2024, Toppan announced the upcoming launch of "GL-SP", an innovative eco-friendly barrier film, in India. Developed in collaboration with India's TOPPAN Speciality Films (TSF), this product is based on biaxially oriented polypropylene (BOPP).

Asia-Pacific Holds the Largest Market Share

- Convenient access to plastic materials in Asia-Pacific significantly fuels the growth of polypropylene packaging films. The region sees a rising trend in plastic packaging usage. According to a July 2024 report by the India Brand Equity Foundation, the Ministry of Commerce and Industry highlights that Western India accounts for 47% of plastic consumption, followed by Northern India at 23% and Southern India at 21%. The key industries driving this consumption include automotive, packaging, and electronic appliances. While China stands out as a pivotal market for plastic packaging, it faces challenges from legislative bans that could hinder its growth.

- Rising demand for packaged and ready-to-eat foods, coupled with the rapid expansion of e-commerce, propels the demand for polypropylene packaging films. Industries such as food and beverages, pharmaceuticals, and personal care increasingly lean toward flexible packaging solutions. The appeal of polypropylene films lies in their superior barrier qualities, durability, and visual allure, making them ideal for various packaging applications.

- The burgeoning middle class and the rise of organized retailing are significant catalysts for the growth of the flexible packaging industry. The export surge, which comes with specific global packaging requirements, has further invigorated the packaging industry. Dominating the Asia-Pacific packaging landscape, plastic flexible packaging is witnessing a shift even among traditional rigid packaging users. A notable driver for the expansion of polypropylene packaging films is the consumer preference for convenient packaging and products offered in reasonable laminate quantities.

- With growing investments in the food processing industry and initiatives to minimize agricultural crop waste, the demand for packaged food and vegetables is set to rise, subsequently boosting the need for polypropylene packaging films.

- As reported by Agriculture and Agri-Food Canada, sales of packaged foods in China, including instant noodles, are projected to reach around USD 16.66 billion by 2026. The data shows a consistent upward trend in the country's processed and packaged food market. This trend is expected to continue, positively impacting the demand for polypropylene packaging films in the coming years.

Polypropylene Packaging Films Industry Overview

The polypropylene packaging films market is competitive because of the presence of many players running their businesses within national and international boundaries. The market is fragmented. The major companies in the polypropylene packaging films market, such as Jindal Poly Films Ltd, CCL Industries (Innovia Films), Cosmo Films Ltd, SRF Limited, and Plastchim-T, are focusing on developing new products and adopting agile business models to address potential disruptions and ensure sustained long-term growth. Some of the key developments in the market are:

May 2024: Plastchim-T acquired Manucor SpA, gaining significant BOPP volume and expertise in flexible packaging. This acquisition boosts the production capacity to 200,000 tons annually and strengthens Europe's transportation and delivery network.

March 2024: Inteplast Group, a plastics manufacturer, secured ISCC PLUS verification for its three BOPP film facilities located in Gray Court, South Carolina; Lolita, Texas; and Morristown, Tennessee. This certification positions Inteplast as one of the first North American BOPP film producers to achieve ISCC PLUS recognition.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand of Cost-effective Packaging Formats

- 5.1.2 Environmental Regulation Paving Way for Flexible Packaging Requirements

- 5.1.3 Growth in Packaged Food Markets

- 5.2 Market Restraints

- 5.2.1 Fluctuation in Raw Material Prices

6 IMPACT OF COVID-19 ON THE MARKET

7 MARKET SEGMENTATION

- 7.1 By Type

- 7.1.1 BOPP

- 7.1.2 CPP

- 7.2 By Application

- 7.2.1 Food

- 7.2.2 Beverage

- 7.2.3 Pharmaceutical and Healthcare

- 7.2.4 Industrial

- 7.2.5 Other Applications

- 7.3 By Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 United Kingdom

- 7.3.2.2 Germany

- 7.3.2.3 France

- 7.3.3 Asia

- 7.3.3.1 China

- 7.3.3.2 India

- 7.3.3.3 Japan

- 7.3.4 Australia and New Zealand

- 7.3.5 Latin America

- 7.3.6 Middle East and Africa

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Plastchim-T

- 8.1.2 Jindal Poly Films Ltd

- 8.1.3 CCL Industries ( Innovia Films)

- 8.1.4 SRF Limited

- 8.1.5 Cosmo Films Ltd

- 8.1.6 Amcor PLC

- 8.1.7 UFlex Limited

- 8.1.8 Taghleef Industries LLC

- 8.1.9 Berry Global Inc.

- 8.1.10 Polyplex Corporation Limited

- 8.1.11 ProAmpac LLC

- 8.1.12 Inteplast Group

- 8.1.13 Toray Plastics (America) Inc.

- 8.1.14 Profol GmbH

- 8.1.15 Napco National

- 8.1.16 Oben Holding Group