|

市場調査レポート

商品コード

1550277

アジア太平洋のプラスチック包装フィルムの市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Asia Pacific Plastic Packaging Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のプラスチック包装フィルムの市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

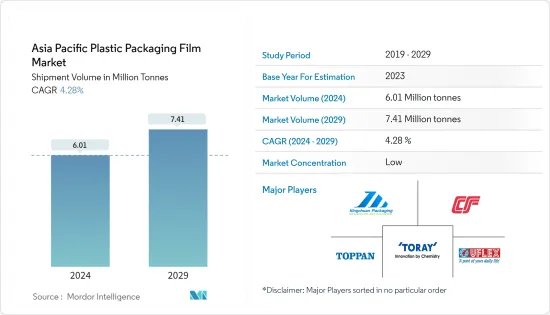

アジア太平洋のプラスチック包装フィルム市場規模(出荷量ベース)は、2024年の601万トンから2029年には741万トンに拡大し、予測期間(2024~2029年)のCAGRは4.28%と予測されます。

主なハイライト

- アジア太平洋地域は、今後数年間、世界のフレキシブルプラスチック包装市場を独占する見通しです。急速な都市化、可処分所得の増加、包装食品への食欲の高まりがこの成長の要因です。小売セクターの急速な拡大が市場を強化しています。eコマース・プラットフォームを通じて購入できる消費財の急増は、包装フィルムの必要性を高めています。これらのフィルムはeコマースにおいて極めて重要であり、製品の携帯性、安全性、耐久性を保証します。

- アジア太平洋は世界のプラスチックフィルム・シート市場において重要な位置を占めており、中でも中国が需要の先陣を切っています。中国とインドが安定した成長を見せていることから、アジア太平洋は世界的に主導的な地位を維持する構えです。調理済み食品の消費の急増が、安全で環境に配慮した包装への需要を促進しています。

- 飲食品業界はプラスチックフィルム包装の主要な消費者です。この業界は環境に配慮した包装ソリューションに軸足を移しています。市場は細分化されているが、大手企業は進化する消費者ニーズに応えるため、革新的でコスト効率の高いソリューションを積極的に生み出しています。

主なハイライト

- 2023年1月、Ester Industries Limited(Ester Filmtech Limited)は、Telangana州の新しいポリエステル(BOPET)フィルム製造施設の商業生産開始を発表しました。この48,000 MTPA工場は50エーカーの敷地に建設され、総工費は約650カロールインドルピー(7,850万米ドル)です。工場がピーク時の効率で稼動すれば、約600カロールインドルピー(7,262万米ドル)の収益が見込まれます。この新工場から生まれる製品は、主にフレキシブル・パッケージング分野で利用され、フレキシブル・パッケージング分野のバリューチェーン拡大に貢献します。

- アジア太平洋地域の小売セクターは活気に満ちており、スーパーマーケット、ハイパーマーケット、コンビニエンスストア、伝統的な店舗、オンラインプラットフォームなど、さまざまな形態があります。アジア太平洋地域は、世界有数の経済規模を誇り、急成長を遂げていることから、小売セクターは活況を呈しています。アジア太平洋地域では、小売セクターが軟包装フィルム市場の成長を促進する上で極めて重要な役割を果たすと考えられています。

- 同市場は、環境に対する不安の高まりによる規制基準の進化という課題に直面しています。プラスチック包装廃棄物に対する国民の意識を受けて、インドや中国のようないくつかの国の連邦政府は、環境への害を抑制し、廃棄物管理を強化するために厳しい規制を展開しています。こうした環境意識の高まりと、使い捨てプラスチックや持続不可能なビジネスモデルに対する懸念が相まって、消費者は環境フットプリントの少ない製品を求めるようになっています。

アジア太平洋プラスチック包装フィルム市場動向

BOPPフィルムの需要増加が市場成長を後押し

- 二軸延伸ポリプロピレン(BOPP)は薄いプラスチックフィルムで、横方向に機械的・手動的に延伸します。その汎用性の高さから、BOPPフィルムはこの地域で人気が急上昇しています。BOPPフィルムの用途は、清涼飲料水の6本パック、ボトルラベル、ビニール袋など多岐にわたる。BOPPフィルムは、その高い引張強度と強化された剛性で注目され、様々な日用品で定番となっています。

- BOPPはその優れた汎用性により、急速に成長しているフィルム素材です。ポリプロピレンフィルムとして、BOPPは蝋引き紙やアルミ箔の優れた代替品です。キャスト・ポリプロピレン(CPP)に比べ、高い引張強度、硬い弾性率、低い伸び、優れたガスバリア性、ヘイズの低減が特徴です。さらに、BOPPフィルムはマット、光沢、シルキーマットなど、さまざまな仕上げが可能です。

- BOPPフィルムは、医薬品や化粧品業界で幅広い用途があります。BOPPフィルムは密封性に優れ、効果的な酸素バリアとして機能します。インドと中国の製薬・化粧品産業が力強い成長を遂げていることから、BOPPフィルムの需要はさらに高まっています。特に、これらの分野で懸念されるのは酸化であり、BOPPフィルムはこの課題に巧みに対処しています。

- 中国国家統計局によると、中国における美容・化粧品の小売販売額は2019年の410億米ドルから2023年には569億4,000万米ドルに増加しました。この増加傾向は今後も続くと予想され、BOPPフィルムの需要が増加します。

- 複数の企業が市場での生産の拡大と成長に投資しています。BOPPバリアフィルムの市場は、包装、食品安全、輸送のための包装食品の需要の増加により増加しています。この業界では多額の投資が行われています。

- 2023年6月、東レは電気自動車(EV)分野の需要急増に対応するため、日本の茨城県にある土浦事業所で東レファンBOPPフィルムの生産能力を増強する予定です。2025年完成予定のこの増設により、生産能力は40%大幅に増加する見込みです。

インドでの需要増加が期待される

- インドの冷凍食品・スナック市場は、ライフスタイルの進化と消費者の嗜好の変化に後押しされて成長しています。冷凍野菜とスナックが圧倒的で、市場シェアの65%以上を占める。Mother Dairy、Venky's、McCain Foodsといった注目すべきブランドが市場をリードしています。特に冷凍スナックは、その利便性が支持され、家庭やオフィスでの急な買い物に最適な選択肢となっており、2桁台の力強い成長を遂げています。

- 世界包装機構(WPO)のトーマス・シュナイダー会長が強調したように、インドの包装市場は今後数年で大きく成長する見込みです。その背景には、清潔な水、安全な食品、医薬品への関心の高まりと、最先端のデジタル技術の迅速な導入があります。

- 広大で増加するインドの中間所得層と組織小売の拡大が、軟包装市場の成長を牽引しています。漁業や水産物輸出の増加もプラスチックフィルム包装の需要を押し上げています。

- インド準備銀行によると、2023年度のインドの魚介類輸出額は6,490億インドルピーを超え、前年度から大幅に増加しました。水産物と魚の輸出が徐々に増加するにつれて、バリア性の高いプラスチック包装フィルムの需要も増加すると思われます。

- 市場各社は、耐引裂性の強化、バーコードの鮮明度の向上、優れた荷重保持力、耐水性、衝撃強度の向上など、革新的な機能の統合にますます注力しています。小売セクターからの需要の急増、製品包装と流通・倉庫保管中の商品の安全性確保への重点の高まりは、ストレッチフィルム市場の極めて重要な成長触媒となる見通しです。

- 2024年4月、マハラシュトラ州ムンバイを拠点とする主要企業Chemco Groupは、全国的なストレッチフィルム需要の緩和に対応するため、最先端のストレッチフィルムラインを立ち上げ、市場での地位を強化しました。年間1,000トンを超える生産能力を誇るこの技術は、フィルムの品質に妥協することなく、増大する需要に対応することを可能にします。

アジア太平洋プラスチック包装フィルム産業の概要

アジア太平洋地域のプラスチック包装フィルム市場は適度に断片化されています。主な市場プレーヤーは、東レ・アドバンストフィルム、ベリー世界、UFlex Limitedなどです。同市場は、原材料や包装サービスを供給する大手およびローカルプレーヤーで構成されています。

- 2024年4月UFlex LimitedはAmplus Phoenix Private Limitedと長期売電契約(PPA)を締結。この契約は、カルナタカ州にあるUFlexの包装用フィルム工場に特化したものです。UFlexは、2035年またはそれ以前にネット・ゼロ・エミッションを達成するというコミットメントの一環として、推定19,000 tCO2eの大幅な削減を目指しています。

- 2024年3月トッパンホールディングスの完全子会社である凸版印刷は、インドのTOPPAN Speciality Films Private Limited(TSF)と共同で、二軸延伸ポリプロピレン(BOPP)を基材とする最先端のバリアフィルム「GL-SP」を発表しました。この革新的な製品は、トッパングループのGL BARRIER1シリーズのサステイナブルパッケージングソリューションのラインナップに加わります。トッパンとTSFは、2024年4月にGL-SPの販売を開始し、主にインドおよびその他のアジア市場におけるドライ商品の包装をターゲットとしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量で持続可能な包装に対する業界全体の需要の高まり

- 飲食品と医薬品セクターからの旺盛な需要が成長を促進

- 市場抑制要因

- プラスチック使用に対する政府の厳しい政策

- 貿易シナリオ

- EXIMデータ

- 貿易分析(輸出入上位5カ国)

- 業界の規制と政策、規格

- 技術情勢

- 価格動向分析

- プラスチック樹脂(現在の価格と過去の動向)

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品

- ヘルスケア

- パーソナルケア&ホームケア

- 工業用包装

- その他の最終用途産業

- 食品

- 国別

- 中国

- インド

- 日本

- タイ

- オーストラリア・ニュージーランド

- インドネシア

- ベトナム

第7章 競合情勢

- 企業プロファイル

- Toray Advanced Film Co. Ltd

- UFlex Limited

- Toppan Packaging Service Co. Ltd

- Kingchuan Packaging

- Cosmo Films Limited

- Berry Global Inc.

- Jindal Poly Films

- Innovia Films(CCL Industries Inc.)

- Sealed Air Corporation

- Futamura Chemical Co. Ltd

- Ecoplast Ltd.

- IFC Plastic Co. Ltd

- Victory Industries Pty Ltd

- Polyplex(Thailand)Public Company Limited

第8章 投資分析

第9章 市場機会と今後の動向

目次

Product Code: 50002889

The Asia Pacific Plastic Packaging Film Market size in terms of shipment volume is expected to grow from 6.01 Million tonnes in 2024 to 7.41 Million tonnes by 2029, at a CAGR of 4.28% during the forecast period (2024-2029).

Key Highlights

- Asia-Pacific is poised to dominate the global flexible plastic packaging market in the coming years. Rapid urbanization, escalating disposable incomes, and a rising appetite for packaged foods can be attributed to this growth. The retail sector's swift expansion is bolstering the market. The surge in consumer goods available through e-commerce platforms amplifies the need for packaging films. These films are crucial in e-commerce, ensuring products are portable, secure, and durable.

- Asia-Pacific is significant in the global plastic films and sheets market, with China spearheading the demand. With both China and India showing consistent growth, Asia-Pacific is poised to retain its leading position globally. The surge in the consumption of ready-to-eat meals is fueling the demand for safe and eco-conscious packaging.

- The food and beverage industry is a primary consumer of plastic film packaging. This industry is pivoting toward eco-conscious packaging solutions. The market exhibits fragmentation; major players are actively creating innovative, cost-effective solutions to cater to evolving consumer needs.

- In January 2023, Ester Industries Limited (Ester Filmtech Limited) announced the commencement of commercial production at Telangana's new polyester (BOPET) film manufacturing facility. The 48,000 MTPA unit spans 50 acres and costs around INR 650 crore (USD 78.5 million). When the factory operates at its peak efficiency, it is anticipated to provide revenue of about INR 600 crores (USD 72.62 million). The products resulting from this new unit will primarily be utilized in the flexible packaging sector and contribute to expanding the flexible packaging sector's value chain.

- The retail sector in the Asia-Pacific region is vibrant and varied, with a range of formats such as supermarkets, hypermarkets, convenience stores, traditional shops, and online platforms. Given that the region hosts some of the world's largest and swiftest-growing economies, its retail sector is thriving. In the Asia-Pacific region, the retail sector is poised to play a pivotal role in propelling the growth of the flexible packaging film market.

- The market faces challenges from evolving regulatory standards driven by mounting environmental apprehensions. In response to public awareness about plastic packaging waste, the federal governments of several countries like India and China are rolling out stringent regulations to curtail environmental harm and enhance waste management. This heightened environmental consciousness, coupled with concerns over single-use plastics and unsustainable business models, is prompting consumers to seek products with reduced environmental footprints.

Key Highlights

Asia Pacific Plastic Packaging Film Market Trends

The Rising Demand for BOPP Films Aids Market Growth

- Biaxially oriented polypropylene (BOPP) is a thin plastic film that undergoes mechanical and manual stretching through a cross-direction process. Due to its versatile properties, BOPP films have surged in popularity across the region. Their applications are universal, including soft drink six-packs, bottle labels, and plastic bags. Noteworthy for their high tensile strength and enhanced stiffness, BOPP films are a staple in various everyday products.

- BOPP is a rapidly growing film material due to its exceptional versatility. As a polypropylene film, BOPP is a superior substitute for waxed paper and aluminum foil. It has a higher tensile strength, a stiffer modulus, lower elongation, superior gas barrier properties, and reduced haze compared to cast polypropylene (CPP). Moreover, BOPP films are readily accessible in various finishes, including matte, glossy, and silky matte.

- BOPP films find extensive applications in the pharmaceutical and cosmetic industries. They excel in their sealing properties and act as an effective oxygen barrier. With India and China's pharmaceutical and cosmetic industries witnessing robust growth, the demand for BOPP films is further bolstered. Notably, a primary concern in these sectors is oxidation, a challenge that BOPP films adeptly combat.

- According to the National Bureau of Statistics of China, the retail sales value of beauty and cosmetic products in China increased from USD 41 billion in 2019 to USD 56.94 billion in 2023. This increasing trend is expected to continue in the upcoming years, increasing the demand for BOPP films.

- Several firms have invested in expanding and growing their production on the market. The market for BOPP barrier films has increased due to the growing demand for packaged food goods for packaging, food safety, and transportation. Significant investments are being made in the industry.

- In June 2023, Toray Industries, in response to the surging demand from the electric vehicle (EV) sector, is set to boost its production capacity for Torayfan BOPP film at its Tsuchiura facility in Japan's Ibaraki prefecture. The expansion, slated for completion in 2025, is expected to increase capacity by a significant 40%.

Demand is Expected to Increase in India

- The Indian frozen foods and snacks market is growing, propelled by evolving lifestyles and shifting consumer preferences. Frozen vegetables and snacks dominate, accounting for over 65% of the market share. Noteworthy brands such as Mother Dairy, Venky's, and McCain Foods lead the market. Frozen snacks, particularly, are experiencing robust double-digit growth, favored for their convenience, making them a go-to choice for impromptu home or office purchases.

- As Thomas Schneider, president of the World Packaging Organization (WPO), highlighted, the Indian packaging market is poised for substantial growth in the coming years. This can be attributed to the heightened emphasis on clean water, safe food, and pharmaceuticals, along with the swift adoption of cutting-edge digital technologies.

- The vast and increasing Indian middle-income group and the expansion in organized retail drive growth in the flexible packaging market. The growth of fishery and seafood exports also boosts the demand for converted plastic film packaging.

- According to the Reserve Bank of India, in fiscal year 2023, India's export value of fish and fishery products surpassed INR 649 billion, marking a substantial increase from the preceding year. With the gradual increase in fishery products and fish exports, the demand for high-barrier plastic packaging films would also increase.

- Market players are increasingly focusing on integrating innovative features such as enhanced tear resistance, improved barcode clarity, superior load retention, water resistance, and heightened impact strength. The surge in demand from the retail sector and an escalating emphasis on product packaging and ensuring goods' safety during distribution and warehousing are poised to be pivotal growth catalysts for the stretch films market.

- In April 2024, to address the easing demand for stretch films nationwide, Chemco Group, a key player based in Mumbai, Maharashtra, strengthened its market position with the launch of its cutting-edge stretch film line. This technology, boasting an annual production capacity exceeding 1,000 tons, empowers businesses to cater to the escalating demand without compromising film quality.

Asia Pacific Plastic Packaging Film Industry Overview

The Asia-Pacific plastic packaging film market is moderately fragmented. The major market players include Toray Advanced Film Co. Ltd, Berry Global Inc., and UFlex Limited. The market comprises major and local players supplying raw materials and packaging services.

- April 2024: UFlex Limited secured a long-term power purchase agreement (PPA) with Amplus Phoenix Private Limited. This agreement was specifically tailored for UFlex's packaging films plant in Karnataka. As part of its commitment to achieving net-zero emissions by 2035, or even earlier, UFlex aims to slash its carbon footprint by an estimated 19,000 tCO2e significantly.

- March 2024: TOPPAN Inc., a wholly owned subsidiary of TOPPAN Holdings Inc., in collaboration with India's TOPPAN Speciality Films Private Limited (TSF), unveiled GL-SP, a cutting-edge barrier film utilizing biaxially oriented polypropylene (BOPP) as its base. This innovative product is set to join the esteemed lineup of sustainable packaging solutions under the TOPPAN Group's GL BARRIER1 series. TOPPAN and TSF commenced sales of GL-SP in April 2024, targeting the packaging of dry goods primarily in the Indian and other Asian markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of Substitutes

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand For Light-Weight and Sustainable Packaging Across Industries

- 5.1.2 Robust Demand From the Food, Beverage and Pharmaceutical Sector Aids Growth

- 5.2 Market Restraints

- 5.2.1 Stringent Government Policies Against the Use of Plastic

- 5.3 Trade Scenario

- 5.3.1 EXIM Data

- 5.3.2 Trade Analysis (Top 5 Import-Export Countries)

- 5.4 Industry Regulation, Policy, and Standards

- 5.5 Technology Landscape

- 5.6 Pricing Trend Analysis

- 5.6.1 Plastic Resins (Current Pricing and Historic Trends)

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene (Biaxially Oriented Polypropylene (BOPP), Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End User

- 6.2.1 Food

- 6.2.1.1 Candy & Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, And Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products

- 6.2.2 Healthcare

- 6.2.3 Personal Care & Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-use Industry Applications

- 6.2.1 Food

- 6.3 By Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

- 6.3.4 Thailand

- 6.3.5 Australia and New Zealand

- 6.3.6 Indonesia

- 6.3.7 Vietnam

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Toray Advanced Film Co. Ltd

- 7.1.2 UFlex Limited

- 7.1.3 Toppan Packaging Service Co. Ltd

- 7.1.4 Kingchuan Packaging

- 7.1.5 Cosmo Films Limited

- 7.1.6 Berry Global Inc.

- 7.1.7 Jindal Poly Films

- 7.1.8 Innovia Films (CCL Industries Inc.)

- 7.1.9 Sealed Air Corporation

- 7.1.10 Futamura Chemical Co. Ltd

- 7.1.11 Ecoplast Ltd.

- 7.1.12 IFC Plastic Co. Ltd

- 7.1.13 Victory Industries Pty Ltd

- 7.1.14 Polyplex (Thailand) Public Company Limited