|

市場調査レポート

商品コード

1550303

オーストラリアとニュージーランドのプラスチック包装用フィルム市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Australia And New Zealand Plastic Packaging Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オーストラリアとニュージーランドのプラスチック包装用フィルム市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 108 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

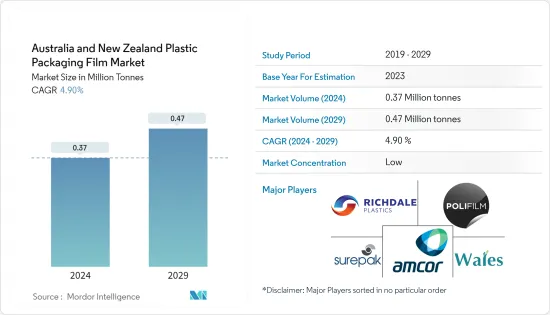

オーストラリアとニュージーランドのプラスチック包装用フィルム市場規模は、2024年には37万トンと推定され、2029年には47万トンに達し、予測期間(2024-2029年)のCAGRは4.90%で成長すると予測されます。

主なハイライト

- オーストラリアとニュージーランドのプラスチックフィルム包装市場は、様々な要因が重なって成長しています。軽量で利便性の高いパッケージングへの需要の高まり、持続可能性に関する消費者の意識の高まり、賞味期限と製品保護を強化する技術の先進化などです。その他の特典としては、飲食品、医薬品、パーソナルケアなど様々な業界で軟包装の採用が増加していることが挙げられます。

- プラスチックフィルム包装の多様な形状やサイズに適応する柔軟性、コスト効率、輸送のしやすさが成長を後押ししています。軟包装分野は、産業界が環境に優しい選択肢を重視し、消費者が利便性を重視することで、大幅な拡大が見込まれています。この成長の原動力は、持続可能なパッケージング・ソリューションに対する需要の高まり、材料技術の先進化、耐久性があり軽量なパッケージングを必要とするeコマースの人気の高まりです。

- 広大で多様な文化を持つオーストラリアは、成長意欲のある企業にとって数々のビジネス上の利点を誇っています。堅調な輸出と安定した金融システムは、オーストラリアがビジネス・オーナーにとって最良の選択肢であることを裏付けています。世界有数の富裕国であるオーストラリアは、特にアジア太平洋諸国との強い貿易関係を維持しています。地理的にも、これらの重要な市場に近接しているため、貿易上の優位性がさらに高まっています。オーストラリアとアジア太平洋諸国との貿易、投資、文化的結びつきは、長年にわたって深く根付いています。オーストラリアは、中国、日本、米国などの主要国やASEANなどの地域団体と重要な貿易協定を結んでいます。特筆すべきは、オーストラリアがアジア太平洋で最も急成長している包装市場のひとつであるということです。さらに、加工食品、生鮮食品、食肉部門は、健康志向の消費者動向と倫理的関心の高まりに後押しされて、増加の一途をたどっています。

- オーストラリアは、2025年までに再利用可能、リサイクル可能、または堆肥化可能な包装を100%達成すること、2025年までにプラスチック包装の70%をリサイクルまたは堆肥化すること、2025年までにすべての包装のリサイクル率を平均50%にすること、という4つの主要目標に焦点を当てた「2025年国家包装目標」を設定しました。これらの目標を達成するため、オーストラリアの各州・準州では、特に外食産業で使用される様々な使い捨てプラスチック製品の段階的廃止が進められています。オーストラリアの環境大臣は、循環型経済への移行を加速させるため、結束して新たな包装基準を策定しました。この取り組みには、全国的なリサイクル最低含有量の義務化、国内包装における有害化学物質の使用禁止などが含まれます。

- プラスチックは、海洋ごみの中でオーストラリアで最も重要かつ永続的な割合を占めており、プラスチック包装がその大部分を占めています。プラスチック生産におけるプラスチック包装の極めて重要な役割を認識することで、包装業界はより持続可能な慣行へと舵を切らざるを得なくなると思われます。この転換には、リサイクル可能な素材や生分解性素材への移行、リサイクル性を高めるための包装設計の見直し、代替包装ソリューションの模索などが含まれます。

オーストラリアとニュージーランドのプラスチック包装用フィルム市場動向

食品分野が大きな市場シェアを占める

- 消費者のライフスタイルが多忙なスケジュールに合わせて進化するにつれ、冷凍食品のような便利な食事オプションへの需要が急増しています。プラスチックフィルム包装は、手早く食事を準備するニーズに沿った開けやすいフォーマットを提供し、この物語において極めて重要です。リシーラブル・クロージャーやポーションサイズ・パックなどの追加機能は、消費者の利便性をさらに高めています。冷凍食品市場の成長は、プラスチックフィルム包装の需要を高めています。

- オーストラリアの都市部の顧客はますます便利な包装を好むようになり、使いやすく軽量なソリューションの需要に拍車をかけています。これに対してベンダーは、拡大する組織小売の情勢を先取りし、進化する消費者の嗜好に適応するために、設計を転換しています。このシフトの背景には、消費者体験を向上させ、持続可能性の目標に沿ったパッケージングに対するニーズがあります。プラスチックフィルムパウチに代表される、より軽い素材を採用することは、このような要求を満たし、大幅な省エネの利点を提供します。さらに、これらの素材は輸送コストと環境への影響を削減するため、メーカーと消費者にとって好ましい選択肢となります。

- 2023年には、オーストラリアの食品小売業界の年間売上高は1,118億米ドルを超え、2021年の1,015億米ドルから増加し、前年比で一貫した成長を示しています。食品小売業のこのような上昇軌道は、食品の品質を保ち、保存期間を延ばし、製品の体裁を整えるのに不可欠なプラスチックフィルム包装の需要を強調しています。増収は、消費者のニーズと嗜好に応えるこの分野の回復力と適応力を浮き彫りにしています。

- 食品メーカーは、軽量で保護性が高く、見た目に美しく、バリア性の高い包装をますます求めるようになっています。この動向は、プラスチックフィルム包装分野の売上を牽引すると予想されます。プラスチックフィルム包装に関連する多感覚的な体験は購買意欲をかき立て、市場の成長軌道を後押しします。さらに、プラスチックフィルム包装の多用途性と費用対効果により、メーカーに好まれ、市場の魅力をさらに高めています。

- オーストラリアはプラスチック包装の削減に積極的に取り組んでいるが、代替品と比べたその利点により、メーカーは生産を続けています。同国は野心的な2025年国家包装目標を定め、包装管理の持続可能な道筋を描いています。オーストラリアの食品業界と政府は、より環境に優しい包装アプローチを推進し、この目標を支持しています。この包括的な目標は、国内のすべての包装活動を対象としており、より持続可能な未来に向けた実質的な動きを示しています。

市場で大きなシェアを占めると予想されるポリエチレン・セグメント

- ポリエチレンは主に、ポリ袋、フィルム、ジオメンブレンなどの包装に使用されます。この熱可塑性樹脂は軽量で部分的に結晶性があり、高い耐薬品性、低吸湿性、遮音性を誇る。ポリエチレンの中でもLDPE(低密度ポリエチレン)はその柔軟性が際立っており、フィルム包装や断熱材に適しています。LDPEは、包装用フィルム、ゴミ袋、食料品袋から農業用マルチ、電線、ケーブルの断熱材まで、さまざまな用途に幅広く利用されています。HDPEよりも結晶化度が低いため、バリア性は若干低下するもの、よりソフトで柔軟な質感が得られます。

- LDPEは軟包装材として広く使用されており、手頃な価格と耐薬品性、耐油性で珍重されています。HDPEと異なり、LDPEは外観がやや白濁しているが、透明度は高いです。融点が低いLDPEは、高い熱安定性を必要とする用途では不利かもしれないが、低融点が好まれる場面では有利です。LLDPEは包装分野で広く使われているが、密度が低く、コモノマーが含まれているため、一次鎖に枝状の構造ができ、結晶化度が低下します。この変化は、ぼんやりした外観と、よりしなやかな質感につながります。LLDPEは、密度と厚みを合わせると、衝撃強さ、引張強さ、耐突き刺し性、伸びでLDPEを上回る。

- 消費者が便利な買い物を好むようになっていることは、スーパーマーケットや食料品店の売上が増加していることからも明らかです。買い物客は日々の買い物にこれらの店舗を利用するため、プラスチックフィルム包装の需要が急増しています。この包装は、使い勝手がよく、持ち運びに便利で、保管に適していることから支持されています。さらに、ポリエチレンフィルムは、生鮮品の保存期間の延長、輸送中の製品ダメージの軽減、視覚的アピールの強化などの特典を提供し、小売部門での採用をさらに促進しています。

- オーストラリアのスーパーマーケットと食料品小売市場は、ウールワース・グループとコールス・グループの大手2社が独占しています。ニューサウスウェールズ州とビクトリア州は人口が最も多いため、スーパーマーケットの数は国内で最も多いです。これらの大手スーパーマーケットと並んで、オーストラリアには、ドイツのチェーン店アルディ(Aldi)や個人経営のIGAなど、さまざまな食料品店があります。オーストラリアのスーパーマーケットおよび食料品小売部門の年間売上高は、一貫して成長を続けています。2021年の830億米ドルから、2023年には924億米ドルを突破します。オーストラリアのスーパーマーケット部門におけるこの上昇軌道は、需要の高まりを強調するだけでなく、プラスチックフィルム市場における機会も示唆しています。

オーストラリアとニュージーランドのプラスチック包装用フィルム産業概要

オーストラリアとニュージーランドのプラスチック包装用フィルム市場は断片化されており、Amcor Group GmbH、Surepak Pty Ltd、Richdale Plastics Pty Ltdなど、複数の世界的・地域的プレーヤーが競争の激しい市場空間で注目を集めようとしています。この市場の特徴は、製品の差別化が低く、製品の浸透度が高まり、競合が多いことです。

- 2024年2月- オーストラリアの大手飲食品ブランドであるキャドバリーは、世界の包装会社であるAmcorと提携し、約1,000トンの消費者再生プラスチックを確保しました。この動きは、バージン・プラスチックへの依存を減らすというキャドバリーの広範な戦略の一環です。2022年、キャドバリーはすでにオーストラリアで160gから185gのキャドバリーデイリーミルクファミリーブロックに使用されるプラスチックの30%(マスバランスベース)をリサイクル素材に移行しています。今回の合意により、キャドバリーはさらに推進し、オーストラリアで製造されるチョコレート・ブロック、バー、ピースの全製品において、再生プラスチックの使用を50%(マス・バランス・ベース)にすることを目標としています。この転換により、キャドバリーはこれらの製品に必要なバージン・プラスチックを半分に削減することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションへの需要の高まり

- 様々な産業におけるプラスチックフィルム需要の増加が成長の可能性を示す

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

- 業界の規制と政策、規格

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン[PP](二軸延伸ポリプロピレン[BOPP]、キャストポリプロピレン[CPP)

- ポリエチレン(低密度ポリエチレン[LDPE]、直鎖状低密度ポリエチレン[LLDPE)

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート[BOPET)

- ポリスチレン

- バイオベース

- ポリ塩化ビニル、エチレンビニルアルコール、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料、スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他エンドユーザー産業用途(農業、化学など)

- 食品

- 国別

- オーストラリア

- ニュージーランド

第7章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- Surepak Pty Ltd

- POLYEM Pty Ltd

- Richdale Plastics Pty Ltd

- Polywrap(Australia)

- Wales Industries Pty Ltd

- POLIFILM PROTECTION AUSTRALIA PTY LIMITED

- Dolphin Plastics

- Polyprint Packaging Ltd

- Allflex Packaging Ltd

- Integrated Packaging Group(IPG)

第8章 リサイクルと持続可能性の情勢

第9章 市場の将来

The Australia And New Zealand Plastic Packaging Film Market size is estimated at 0.37 Million tonnes in 2024, and is expected to reach 0.47 Million tonnes by 2029, growing at a CAGR of 4.90% during the forecast period (2024-2029).

Key Highlights

- The plastic film packaging market in Australia and New Zealand is thriving due to a confluence of factors. These include a growing appetite for lightweight and convenient packaging, heightened consumer consciousness regarding sustainability, and technological advancements that enhance shelf life and product protection. Additionally, the market benefits from the increasing adoption of flexible packaging in various industries, such as food and beverage, pharmaceuticals, and personal care.

- Plastic film packaging's flexibility in adapting to diverse shapes and sizes, cost efficiency, and ease of transport bolster its growth. The flexible packaging sector is set for significant expansion, with industries emphasizing eco-friendly options and consumers valuing convenience. This growth is driven by the increasing demand for sustainable packaging solutions, advancements in material technology, and the rising popularity of e-commerce, which requires durable and lightweight packaging.

- Australia, a large and culturally diverse nation, boasts numerous business advantages for growth-minded companies. Its robust exports and stable financial system underscore why it is a prime choice for business owners. As one of the world's wealthiest nations, Australia maintains strong trade connections, particularly with Asia-Pacific countries. Geographically, its proximity to these vital markets further enhances its trade advantages. Australia's trade, investment, and cultural ties with the Asia-Pacific nations are long-standing and deeply entrenched. The country has secured crucial trade agreements with key players, such as China, Japan, and the United States, as well as with regional entities like ASEAN. Notably, Australia stands out as one of the fastest-growing packaging markets in the Asia-Pacific. Moreover, its processed food, fresh produce, and meat sectors are on the rise, driven by health-conscious consumer trends and growing ethical concerns.

- Australia set its 2025 National Packaging Targets, focusing on four key objectives: achieving 100% reusable, recyclable, or compostable packaging by 2025; ensuring 70% of plastic packaging is recycled or composted by 2025; and aiming for an average of 50% recycled content in all packaging by 2025. Various single-use plastic items, especially those used in food service, are being phased out across different Australian states and territories to achieve these goals. The country's environmental ministers have united to craft new packaging standards, aiming to accelerate Australia's shift toward a circular economy. This initiative includes establishing nationwide minimum recycled content mandates and banning the use of harmful chemicals in domestic packaging.

- Plastics constitute Australia's most significant and enduring portion of marine litter, with plastic packaging driving a substantial part of this production. Acknowledging the pivotal role of plastic packaging in driving plastic production will likely compel the packaging industry to pivot toward more sustainable practices. This shift could encompass moving to recyclable or biodegradable materials, redesigning packaging for enhanced recyclability, or exploring alternative packaging solutions.

Australia and New Zealand Plastic Packaging Film Market Trends

Food Segment to Hold Significant Market Share

- As consumer lifestyles evolve to accommodate busier schedules, the demand for convenient meal options, like frozen foods, has surged. Plastic film packaging is pivotal in this narrative, providing easy-to-open formats that align with the need for quick meal preparation. Additional features, such as resealable closures and portion-sized packs, further elevate the convenience factor for consumers. The growing frozen food market has consequently heightened the demand for plastic film packaging.

- Australia's urban customers increasingly favor convenient packaging, spurring demand for user-friendly and lightweight solutions. In response, vendors are pivoting their designs to stay ahead in the expanding organized retail landscape, adapting to evolving consumer preferences. This shift is driven by the need for packaging that enhances the consumer experience and aligns with sustainability goals. Embracing lighter materials, notably plastic film pouches, meets these demands and offers substantial energy-saving advantages. Additionally, these materials reduce transportation costs and environmental impact, making them a preferred choice for manufacturers and consumers.

- In 2023, Australia's food retail industry generated an annual revenue exceeding USD 111.8 billion, up from USD 101.5 billion in 2021, showcasing consistent year-on-year growth. This upward trajectory in food retail has underscored the demand for plastic film packaging, essential for preserving food quality, extending shelf life, and enhancing product presentation. The increased revenue highlights the sector's resilience and adaptability in meeting consumer needs and preferences.

- Food manufacturers increasingly demand lightweight, protective, visually appealing, and high-barrier packaging. This trend is expected to drive sales in the plastic film packaging sector. The multi-sensory experience associated with plastic film packaging entices purchases and bolsters the market's growth trajectory. Additionally, the versatility and cost-effectiveness of plastic film packaging make it a preferred choice among manufacturers, further enhancing its market appeal.

- Despite Australia's active efforts to reduce plastic packaging, its benefits compared to alternatives have allowed manufacturers to continue their production. The country has established ambitious 2025 National Packaging Targets, charting a sustainable path for packaging management. The Australian food industry and the government are behind these targets, pushing for a greener packaging approach. These comprehensive targets cover all packaging activities within the nation, signaling a substantial move toward a more sustainable future.

Polyethylene Segment Expected to Hold Significant Share in the Market

- Polyethylene is primarily used in packaging, including plastic bags, films, and geomembranes. This thermoplastic resin is lightweight and partially crystalline, boasting high chemical resistance, low moisture absorption, and sound-insulating properties. Within the polyethylene family, LDPE (low-density polyethylene) stands out for its flexibility, making it a preferred choice for film packaging and electrical insulation. LDPE is extensively utilized in various applications, ranging from packaging films, trash, and grocery bags to agricultural mulch, wire, and cable insulation. Its lower crystallinity than HDPE results in a softer, more flexible texture, albeit with a slightly reduced barrier capability.

- LDPE is widely used in flexible packaging and is prized for its affordability and chemical and oil resistance. Unlike HDPE, LDPE has a slightly cloudy appearance but offers better clarity. With a lower melting point, LDPE might not fare well in applications requiring high heat stability, but it is a boon in scenarios where lower melting points are preferred. LLDPE, a prevalent choice in the packaging sector, also stands out for its lower density and the inclusion of comonomers, which introduce branch-like structures on its primary chain, thereby reducing crystallinity. This alteration leads to a hazy appearance and a more pliable texture. Notably, when matched for density and thickness, LLDPE surpasses LDPE in impact strength, tensile strength, puncture resistance, and elongation.

- Consumers' growing preference for convenient shopping experiences is evident in the uptick in supermarket and grocery store sales. With shoppers turning to these outlets for their daily needs, the demand for plastic film packaging is surging. This packaging is favored for its user-friendly, portable, and storage-friendly nature. Additionally, polyethylene film offers benefits such as extended shelf life for perishable goods, reduced product damage during transportation, and enhanced visual appeal, further driving its adoption in the retail sector.

- Two major players, the Woolworths Group and the Coles Group, dominate Australia's supermarket and grocery retail market. The states of New South Wales and Victoria, being the most populous, host the highest number of supermarkets in the country. Alongside these giants, Australia boasts various grocery outlets, including the German chain Aldi and the independently owned IGA stores. The annual revenue of Australia's supermarket and grocery retail sector has seen consistent growth. In 2023, the industry's revenue surpassed USD 92.4 billion, up from USD 83 billion in 2021. This upward trajectory in Australia's supermarket sector not only underscores rising demand but also hints at opportunities in the plastic film market.

Australia and New Zealand Plastic Packaging Film Industry Overview

The plastic packaging film market in Australia and New Zealand is fragmented, comprising several global and regional players like Amcor Group GmbH, Surepak Pty Ltd, and Richdale Plastics Pty Ltd, who are vying for attention in a contested market space. This market is characterized by low product differentiation, growing levels of product penetration, and high levels of competition.

- February 2024 - Cadbury, a leading food and beverage brand in Australia, partnered with Amcor, a global packaging company, to secure approximately 1000 tonnes of post-consumer recycled plastic. This move is part of Cadbury's broader strategy to reduce its reliance on virgin plastic. In 2022, Cadbury already transitioned 30% (on a mass balance basis) of the plastic used for its 160 g to 185 g Cadbury Dairy Milk family blocks in Australia to recycled materials. With this recent agreement, Cadbury is pushing further, targeting a 50% (on a mass balance basis) usage of recycled plastic across its entire range of chocolate blocks, bars, and pieces manufactured in Australia. This shift cuts Cadbury's virgin plastic requirements in half for these products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Increasing Demand for Plastic Films Across Various Industries Indicates Growth Potential

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation toward Plastic

- 5.3 Industry Regulation, Policy, and Standards

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene [PP] (Biaxially Oriented Polypropylene [BOPP], Cast Polypropylene [CPP])

- 6.1.2 Polyethylene (Low-density Polyethylene [LDPE], Linear Low-density Polyethylene [LLDPE])

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate [BOPET])

- 6.1.4 Polystyrene

- 6.1.5 Bio-based

- 6.1.6 Polyvinyl Chloride, Ethylene Vinyl Alcohol, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy and Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, and Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings and Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care and Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-user Industry Applications (Agricultural, Chemical, Etc)

- 6.2.1 Food

- 6.3 By Country

- 6.3.1 Australia

- 6.3.2 New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Surepak Pty Ltd

- 7.1.3 POLYEM Pty Ltd

- 7.1.4 Richdale Plastics Pty Ltd

- 7.1.5 Polywrap (Australia)

- 7.1.6 Wales Industries Pty Ltd

- 7.1.7 POLIFILM PROTECTION AUSTRALIA PTY LIMITED

- 7.1.8 Dolphin Plastics

- 7.1.9 Polyprint Packaging Ltd

- 7.1.10 Allflex Packaging Ltd

- 7.1.11 Integrated Packaging Group (IPG)