|

市場調査レポート

商品コード

1550292

タイのプラスチック包装フィルム:市場シェア分析、産業動向、成長予測(2024年~2029年)Thailand Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイのプラスチック包装フィルム:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 106 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

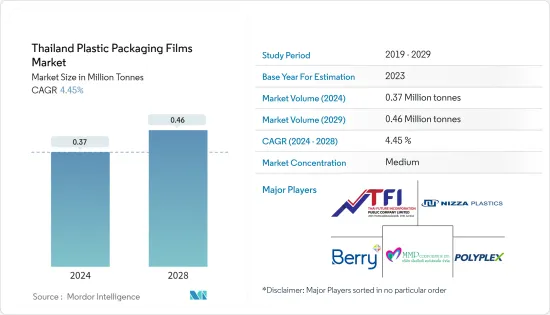

タイのプラスチック包装用フィルム市場規模は2024年に37万トンと推定され、2029年には46万トンに達し、予測期間(2024-2029年)のCAGRは4.45%で成長すると予測されます。

主なハイライト

- タイの包装産業は、消費者が独創的な包装を施された高級品を好むようになった堅調な経済に後押しされ、著しい成長を遂げています。さらに、特にパウチ形式など、持ち運びに便利なパッケージのニーズが急増しており、国の活気ある専門職が拍車をかけています。食品、FMCG、食料品から化粧品に至るまで、幅広い分野でパウチ包装の採用が進んでいます。その結果、各プロバイダーは市場での地位を強化し、ますます魅力的な商品を提供するため、技術革新の努力を強めています。

- さらに、タイの都会的なライフスタイルが、便利なパッケージに対する需要の急増に拍車をかけています。消費者は軽量で使い勝手の良い選択肢を好むため、ベンダーは拡大する組織小売セグメント向けにデザインを調整するよう促しています。フレキシブルパウチのような素材へのシフトは、進化する需要に応え、大幅な省エネをもたらします。さらに、業界の持続可能なパッケージングへの軸足は、環境に優しい製品に対する消費者の嗜好の高まりと合致しており、パッケージング分野における技術革新と競合の激化の舞台となっています。

- さらに、マレーシア、ミャンマー、ラオス、カンボジアと国境を接し、東南アジアの中心に位置するタイの戦略的な立地は、国際的な投資家の注目の的となっています。中国やインドといった主要市場に近いことも、その魅力をさらに高めています。重要な海路の交差点として、タイは地域の商業ハブとしての地位も固めています。このような地理的優位性は、タイのパッケージング部門を著しく後押しし、幅広いプラスチックフィルムに対するニーズの高まりを裏付けています。

- タイの天然資源環境省は、2027年までにプラスチック廃棄物の完全リサイクルを達成すると予測しています。この目標は、同省の2018年から2030年までのプラスチック廃棄物管理ロードマップに詳述されている、プラスチック使用量削減のための政府の包括的計画の要です。このロードマップは、増大する使い捨てプラスチック廃棄物への懸念に直接応えるものです。これらの厳しい措置はタイのプラスチック部門に大きな課題を突きつけるものだが、環境フットプリントの削減と循環型経済の推進という国の広範な目標に沿ったものです。これはひいては、包装におけるイノベーションと持続可能性を促進するものと期待されます。

- タイはまた、特に生鮮食料品の小売部門で横行する使い捨てプラスチックの使用を抑制するために、断固とした措置を講じています。プラスチックフィルムとネットに焦点を当てた最近の法律は、プラスチック廃棄物の削減と持続可能な包装の実践を大幅に促進することを目的としています。その結果、この法律はタイのプラスチック包装フィルム市場を引き締め、メーカーやサプライヤーに直接的な影響を与えることになります。この法律は、循環型経済への幅広い推進に伴い、生分解性と再利用可能な素材への軸足を提唱しています。このシフトは、企業が新しい環境に優しい義務に適応するにつれて、パッケージングの技術革新を促進すると予想されます。

タイのプラスチック包装用フィルム市場動向

食品分野が大きな市場シェアを占める

- タイの食品包装分野は、パッケージ食品に対する世界の食欲の高まりとフードデリバリー分野の急成長に後押しされて拡大しています。特に、インテリジェントで革新的なパッケージングを含む持続可能性と最先端技術が、極めて重要な動向として脚光を浴びています。さらに、政府の優遇措置は、技術的に強化された付加価値の高いパッケージング・ソリューションの創造と生産を後押ししています。

- タイの食品包装セクターは、特に冷凍食品と加工食品の分野で急成長を遂げており、将来の大きな成長が見込まれています。世界的に見て、フィルム包装は最も急成長している産業のひとつです。特に、乾燥食品、冷凍食品、ソース、調味料などのパッケージング・ソリューションに注力する企業による投資と技術革新の高まりが、プラスチック・フィルム包装の需要をさらに促進しています。

- タイの消費者はスーパーマーケットや食料品店に引き寄せられ、便利な買い物を好む傾向が顕著です。これらの店舗が日常的な買い物の目的地となっているため、包装に対する需要は、使いやすさ、持ち運びやすさ、保管の利便性を優先したソリューションへとシフトしています。この動向は、迅速で効率的な買い物体験を求める現代消費者の多忙なライフスタイルに後押しされています。2023年には、タイの包装食品売上高は注目すべき159億5,000万米ドルに達し、2021年の143億7,000万米ドルから着実に上昇します。この成長は、消費者の嗜好の進化に合わせて、保存期間が長く調理が簡単な包装食品への依存度が高まっていることを反映しています。

- さらに、外出先での消費、世帯の小規模化、利便性への嗜好の高まりが、タイの現代的なライフスタイルに道を開いています。これに対し、プラスチックフィルム包装がソリューションとして台頭し、軽量で持ち運びができ、リシーラブルなオプションを提供することで、こうしたダイナミクスに合致しています。このタイプの包装は、忙しい消費者にとって重要な鮮度を保ち、保存期間を延ばす能力において特に有利です。シングルサーブやポーションコントロールのフォーマットは、利便性と正確な分量を優先する消費者に対応し、人気を博しています。さらに、プラスチックフィルム包装は汎用性が高いため、革新的なデザインやブランディングが可能で、顧客の獲得と維持を目指すメーカーの間で人気の高い選択肢となっています。

市場で大きなシェアを占めると予想されるPolytheneセグメント

- プラスチックフィルム包装業界は、特に冷凍食品や加工食品などのセグメントで急成長を遂げており、将来性も有望視されています。特に、パウチ包装はタイからの食品輸出で最も急成長しているセグメントのひとつとなっています。特に乾燥食品、冷凍食品、ソース、調味料などのパッケージング・ソリューションに注力している企業は、投資の増加と革新的なアプローチによってプラスチックフィルム包装の需要を増やしています。

- ポリエチレン(PE)はタイの主要プラスチック素材として台頭し、その汎用性の高い物理的特性が評価されています。費用対効果の高い生産により、他のプラスチック素材とは一線を画しています。特にPEは、一次包装用プラスチックの中で最も軟化点が低く、エネルギー消費の削減につながります。ポリエチレンの変種であるLDPEとLLDPEは、軟包装に広く使用されています。ポリエチレンの人気は、その軽量な組成、部分的な結晶構造、耐薬品性、最小限の吸湿性、効果的な遮音性といった重要な特性から生じています。

- また、様々な地域における冷凍食品産業の成長は、市場にプラスの影響を与えると予想されます。RTE(Ready-to-Eat)食品の需要増加、使用の利便性、輸出用プラスチックフィルムの費用対効果は、タイ市場の成長を支える主な要因です。タイからの食品輸出額は2021年に301億5,000万米ドルであったが、2023年には384億2,000万米ドルに増加し、輸出の動向と包装用プラスチックフィルムの需要の増加を示しています。この成長は、パッケージング技術の先進化、パッケージ食品に対する消費者の嗜好の高まり、小売チェーンの拡大がさらに後押ししており、これらが食品輸出分野におけるプラスチックフィルムの需要を牽引しています。

- タイでは近年、牛肉、豚肉、鶏肉、魚介類の消費と生産が顕著に増加しています。この急増は、消費者にとって魅力的なパッケージングと製品の安全性の確保という2つのニーズに支えられています。その結果、食肉と水産物用の包装ソリューションは、費用対効果が高く実用的なものとして台頭してきました。予測によると、プラスチック包装の売上は今後数年で急激に増加する傾向にあり、その主な理由は、衛生面が重視されるようになったことと、国内市場だけでなく世界市場でも不可欠な、保存期間を延ばし、肉や鶏肉の重要な特性を保持する包装へのニーズが高まったことです。

- タイの食肉・食品メーカーは、軽量で保護性が高く、見た目に美しく、バリア性の高いプラスチックフィルム包装をますます求めるようになっています。この輸出包装の販売動向は、さらに活発化すると予想されます。さらに、食品包装における多感覚体験の重視の高まりは、世界の衝動買いを促進し、それによって市場を強化しています。このようなパウチ、バッグ、ラップの需要の増加は、密封技術の先進化とともに、より高速な生産と充填を可能にする新しい包装機械など、いくつかの要因に関連しています。

- タイでは、加工食品に対する需要の高まりと、利便性を求める消費者の嗜好の高まりが、フレキシブル包装の必要性を高めています。米国農務省のデータによると、タイの生活費が上昇するにつれて、食品小売に対する消費者の支出も増加しています。さらに、タイの加工食品輸出は2023年には輸出総額の54%を占め、プラスチックフィルムの市場成長の主要因となっています。

タイのプラスチック包装フィルム産業概要

タイのプラスチック包装フィルム市場は、Berry Global Inc.、Thai Future Incorporation Public Company Limited、Polyplex(Thailand)Public Company Limitedなどの限られた世界的・地域的プレーヤーが、製品の差別化が低く、製品の普及が進み、競争が激しいことを特徴とする競合市場において、注目を集めようと競い合っています。

- 2023年9月- 持続可能性へのこだわりを強調するベリー世界は、食品用低密度ポリエチレン(LLDPE)フィルムを発表しました。このフィルムは、消費者使用後の再生プラスチック(PCR)を30%以上使用しています。Berry Globalは、このエコフレンドリーなオプションでフィルムの品揃えを増やすことで、特に食品包装における持続可能性の誓約を守る手段をブランドに提供します。PCR-LLDPEフィルムは、ベーカリーおよび冷凍食品セクター向けに作られ、現在ベリーのフレキシブルフィルムのラインアップの一部となっています。これらのフィルムは、スタンドアップパウチ、プレメイドバッグ、ロールストック形式で使用され、縦型および横型のフォーム、フィル、シール(VFFSおよびHFFS)包装方式に対応しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションに対する需要の高まり

- 多様な産業における需要の急増がプラスチックフィルムの成長可能性を示唆

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(PP)(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料・スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他最終用途(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- Thai Future Incorporation Public Company Limited

- Nizza Plastic Company LTD.

- Polyplex(Thailand)Public Company Limited

- SRF LIMITED

- Kim Pai Co., Ltd.

- New Modern Superpack Co., Ltd.

- SHRINKFLEX(THAILAND)PCL

- Berry Global Inc.

- MMP Corporation Ltd.

- NARAI PACKAGING(THAILAND)LTD.

第8章 投資分析

第9章 市場の将来

The Thailand Plastic Packaging Films Market size is estimated at 0.37 Million tonnes in 2024, and is expected to reach 0.46 Million tonnes by 2029, growing at a CAGR of 4.45% during the forecast period (2024-2029).

Key Highlights

- Thailand's packaging industry is experiencing significant growth, buoyed by a robust economy enabling consumers to gravitate towards premium products, frequently presented in inventive packaging. Additionally, there's a pronounced surge in the need for convenient, on-the-go packaging, notably in pouch formats, spurred by the nation's bustling professionals. This shift isn't limited to any one sector; sectors spanning food, FMCG, and groceries to cosmetics are poised to elevate their adoption of pouch packaging. Consequently, providers are ramping up their innovation endeavors to bolster their market standing and deliver increasingly attractive offerings.

- Further, Thailand's urban lifestyle is fueling a surge in the demand for convenient packaging. Consumers favor lightweight, user-friendly options, prompting vendors to tailor their designs for the expanding organized retail segment. Shifting to materials like flexible pouches meets evolving demands and brings substantial energy-saving advantages. Furthermore, the industry's pivot towards sustainable packaging aligns with the growing consumer preference for eco-friendly products, setting the stage for increased innovation and competition in the packaging sector.

- Moreover, Thailand's strategic location at the heart of Southeast Asia, bordering Malaysia, Myanmar, Laos, and Cambodia, has made it a focal point for international investors. Its proximity to major markets such as China and India has further heightened its appeal. As a crossroads for vital sea routes, Thailand has also solidified its position as a regional commerce hub. These geographical advantages have notably boosted the country's packaging sector, underscoring a rising need for a wide array of plastic films.

- Thailand's Ministry of Natural Resources and Environment projects that the nation will achieve full plastic waste recycling by 2027. This target is a cornerstone of the government's overarching plan to reduce plastic use, detailed in the ministry's plastic waste management roadmap from 2018 to 2030. The roadmap directly responded to escalating concerns over the mounting volume of single-use plastic waste. While these stringent measures pose a significant challenge to Thailand's plastics sector, they align with the nation's broader objective of lessening its environmental footprint and promoting a circular economy. This, in turn, is expected to foster innovation and sustainability in packaging.

- Thailand is also taking decisive steps to curb the rampant use of single-use plastics, especially in its fresh produce retail sector. A recent law honing in on plastic film and netting aims to reduce plastic waste and promote sustainable packaging practices significantly. Consequently, this legislation is poised to tighten the market for plastic packaging films in Thailand, directly impacting manufacturers and suppliers. The law advocates for a pivot to biodegradable and reusable materials in line with the broader drive towards a circular economy. This shift is expected to drive innovation in packaging as businesses adapt to the new eco-friendly mandate.

Thailand Plastic Packaging Films Market Trends

Food segment to Hold Significant Market Share

- Thailand's food packaging sector is expanding, propelled by a surging worldwide appetite for packaged foods and the burgeoning food delivery segment. Notably, sustainability and cutting-edge technologies, including intelligent and innovative packaging, are gaining prominence as pivotal trends. Furthermore, government incentives have bolstered the creation and production of tech-enhanced, value-added packaging solutions.

- Thailand's food packaging sector is witnessing rapid growth, especially in the context of frozen and processed foods, which presents significant future growth prospects. Globally, film packaging has emerged as one of the fastest-growing industries. Notably, heightened investments and innovations from companies focusing on packaging solutions, spanning dry foods, frozen items, sauces, and condiments, have further fueled the demand for plastic film packaging.

- Thailand's consumers gravitate towards supermarkets and grocery stores, signaling a clear preference for convenient shopping. With these outlets becoming go-to destinations for daily purchases, the demand for packaging is shifting towards solutions prioritizing ease of use, portability, and storage convenience. This trend is driven by the busy lifestyles of modern consumers who seek quick and efficient shopping experiences. In 2023, Thailand's packaged food sales hit a noteworthy USD 15.95 billion, steadily climbing from USD 14.37 billion in 2021. This growth reflects the increasing reliance on packaged foods, which offer longer shelf life and ease of preparation, aligning with evolving consumer preferences.

- Further, on-the-go consumption, smaller households, and a growing preference for convenience pave the way for modern lifestyles in Thailand. In response, plastic film packaging has emerged as a solution, offering lightweight, portable, and resealable options that align with these dynamics. This type of packaging is particularly advantageous for its ability to preserve freshness and extend shelf life, which is crucial for busy consumers. Single-serve and portion-controlled formats have gained traction, catering to consumers who prioritize convenience and precise portions. Additionally, the versatility of plastic film packaging allows for innovative designs and branding opportunities, making it a popular choice among manufacturers aiming to attract and retain customers.

Polythene Segment Expected to Hold Significant Share in the Market

- The plastic film packaging industry is witnessing rapid growth, especially in segments like frozen and processed foods, with promising prospects. Notably, pouch packaging has emerged as one of the fastest-growing segments for the export of food products from Thailand. Companies, particularly those focusing on packaging solutions for dry foods, frozen items, sauces, and condiments, are increasing the demand for plastic film packaging through increased investments and innovative approaches.

- Polyethylene (PE) has emerged as the leading plastic material in Thailand, lauded for its versatile physical properties. Its cost-effective production distinguishes it from its plastic counterparts. Notably, PE stands out with the lowest softening point among primary packaging plastics, leading to reduced energy consumption. LDPE and LLDPE, variants of PE, are found to be extensively used in flexible packaging. Widely utilized in crafting plastic bags, films, and even pouches, polyethylene's popularity stems from its lightweight composition, partial crystalline structure, and critical attributes like chemical resistance, minimal moisture absorption, and effective sound insulation.

- Also, the growth of the frozen food industry across various regions is anticipated to impact the market positively. Rising demand for Ready-to-Eat (RTE) food, convenience of use, and cost-effectiveness of plastic films for export are primary factors supporting the market's growth in Thailand. The Value of Food Products Exported from Thailand was USD 30.15 billion in 2021, which increased to USD 38.42 billion in 2023, showing the growing trend of export and requirement of plastic films for packaging. This growth is further supported by advancements in packaging technology, increased consumer preference for packaged foods, and the expansion of retail chains, which collectively drive the demand for plastic films in the food export sector.

- Thailand has witnessed a notable uptick in beef, pork, poultry, and seafood consumption and production in recent years. This surge is underpinned by a dual need: appealing packaging for consumers and ensuring product safety. Consequently, packaging solutions for meat and seafood have emerged as both cost-effective and pragmatic. Forecasts suggest a sharp uptrend in plastic packaging sales in the coming years, primarily attributed to a heightened emphasis on hygiene and the rising need for packaging that prolongs shelf life and retains the crucial attributes of meat and poultry, essential for both domestic and global markets.

- Meat and food manufacturers in Thailand increasingly seek lightweight, protective, visually appealing, and high-barrier plastic film packaging. A boost is expected in this trend of export packaging sales. Additionally, the rising emphasis on multi-sensory experiences in food packaging drives impulse global purchases, thereby bolstering the market. This uptick in demand for pouches, bags, and wraps can be linked to several factors, including new packaging machinery that enables higher production and filling speeds, alongside advancements in sealing techniques.

- In Thailand, the rising demand for processed foods and the increasing consumer preference for convenience drive the need for flexible packaging. Data from the US Department of Agriculture highlights that as living costs in Thailand rise, consumer spending on food retail also increases. Furthermore, Thailand's processed food exports, accounting for 54% of its total exports in 2023, are a key driver of market growth for plastic films.

Thailand Plastic Packaging Films Industry Overview

The Thailand plastic packaging films market is semi-consolidated with limited global and regional players, such as Berry Global Inc., Thai Future Incorporation Public Company Limited, Polyplex (Thailand) Public Company Limited, and others vying for attention in a contested market space characterized by low product differentiation, growing product penetration, and high competition.

- September 2023 - Berry Global, emphasizing its dedication to sustainability, has unveiled food-grade low-density polyethylene (LLDPE) films. These films boast at least 30% post-consumer recycled plastic (PCR). By augmenting its film range with this eco-friendly option, Berry Global equips brands with a means to honor their sustainability pledges, particularly in food packaging. The PCR-LLDPE films, tailored for the bakery and frozen food sectors, are now part of Berry's flexible film lineup. These films are applied in stand-up pouches, premade bags, and roll stock formats, catering to vertical and horizontal form, fill, and seal (VFFS and HFFS) packaging methods.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Rising Demand for Lightweight Packaging Solutions

- 5.1.2 Surging Demand Across Diverse Industries Signals Growth Potential for Plastic Films

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation towards Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-User Industry

- 6.2.1 Food

- 6.2.1.1 Candy & Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, And Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care & Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-use Industry Applications (Agricultural, Chemical, Etc)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Thai Future Incorporation Public Company Limited

- 7.1.2 Nizza Plastic Company LTD.

- 7.1.3 Polyplex (Thailand) Public Company Limited

- 7.1.4 SRF LIMITED

- 7.1.5 Kim Pai Co., Ltd.

- 7.1.6 New Modern Superpack Co., Ltd.

- 7.1.7 SHRINKFLEX (THAILAND) PCL

- 7.1.8 Berry Global Inc.

- 7.1.9 MMP Corporation Ltd.

- 7.1.10 NARAI PACKAGING (THAILAND) LTD.