|

市場調査レポート

商品コード

1550294

ベトナムのプラスチック包装フィルム市場:シェア分析、産業動向、成長予測(2024年~2029年)Vietnam Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ベトナムのプラスチック包装フィルム市場:シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

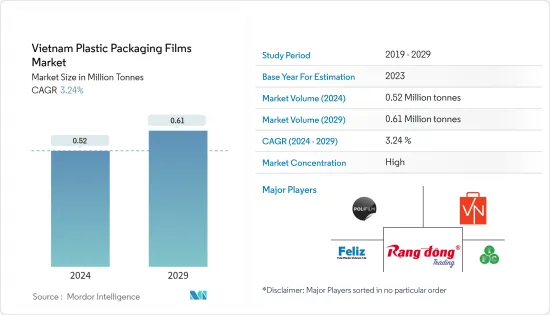

ベトナムのプラスチック包装フィルム市場規模は2024年に52万トンと推定され、2029年には61万トンに達し、予測期間(2024-2029年)のCAGRは3.24%で成長すると予測されます。

主なハイライト

- ベトナムは、有望な投資見通しと潜在的なパートナーシップで外資系企業を引きつけ、依然として最有力候補です。ベトナムは、堅調な経済、戦略的位置づけ、投資家に優しい政策に支えられ、様々な産業において外国直接投資(FDI)の道標となっています。

主なハイライト

- 統計総局(GSO)の報告によると、ベトナムでは外国投資が顕著に増加し、その額は2023年から4.5%増の92億7,000万米ドルに達しました。特筆すべきは、2024年の最初の4ヶ月間で62億8,000万米ドルのFDIを誘致し、5年ぶりの高水準を記録したことです。

- 外国直接投資は、多くの場合、生産設備の拡張や近代化に使用できる資本をもたらします。FDIが増加すれば、ベトナムのプラスチック包装フィルムメーカーは生産能力を強化し、効率を向上させ、国内外の需要を満たすために生産量を増やすことができます。

- アジアにおけるベトナムの戦略的立地と主要航路への近さも、輸出を重視するベトナムメーカーにとって好都合です。ベトナムの海岸線は約3,200kmに及び、114の港が点在しています。この広大な海岸線は、国の貿易・輸送部門において重要な役割を果たしており、国内外の海上活動を促進しています。

主なハイライト

- ベトナムの立地と広大な海岸線、多数の港は、輸出志向の製造業にとって理想的なハブとなっています。ベトナムに進出する外資系企業が増えるにつれ、生産されたプラスチック包装フィルムは近隣諸国やその他の世界市場に容易に輸出できるようになり、業界の成長を後押ししています。

- プラスチック廃棄物とその環境への影響に対する認識と懸念の高まりは、プラスチックの生産と使用に対する規制強化につながっています。こうした規制の遵守はコスト増につながり、持続可能な慣行や素材への投資を必要とします。

主なハイライト

- ベトナムが大きな外国投資を誘致している一方で、中国、インド、タイなどこの地域の他の国々も強力なプラスチック包装産業を有しています。ベトナムの製造業者にとって、これらの確立された市場と競争することは困難です。

ベトナムのプラスチック包装フィルム市場動向

ポリエチレンセグメントが著しい成長を遂げる見込み

- ChemOrbisによると、2024年1月19日に終わる週のベトナムのLDPEフィルム輸入価格は1020-1,100米ドル/トンの範囲と評価されました。一方、HDPEフィルムは1010~1,070米ドル/トン、LLDPEフィルムは970~1,050米ドル/トンとなった。前週と比較すると、LDPEフィルムは50~100米ドル/トン、HDPEフィルムは20~50米ドル/トン、LLDPEフィルムは横ばいもしくは最大20米ドル/トンの値上がりとなった。

- 価格上昇、特にLDPEフィルムの大幅な高騰は、ポリエチレンフィルムに対する旺盛な需要を示しています。食品、農業、消費財などの分野での消費増がこの需要を牽引する可能性があります。旺盛な需要は、それに対応するためにメーカーが生産を増強することで市場の成長を支えます。

- プラスチック輸入の増加は、包装フィルムの製造に必要なポリエチレンのような原材料の入手可能性の拡大を示唆しています。この供給の増加は、地元メーカーの生産能力を支え、需要増への対応や新市場の開拓を可能にします。

- 2023年6月に発表されたベトナム統計局の記事によると、2022年のベトナムの一次形態のプラスチック輸入額は約124億米ドルで、2017年の75億8,000万米ドルから顕著な急増を示しました。

- 大幅な輸入額は、より高品質またはより高度な形態のプラスチックへの投資を反映している可能性もあります。より優れた原材料へのアクセスは、ポリエチレン包装フィルムの品質と性能の向上につながり、食品、医薬品、消費財などの様々な産業にとってより魅力的なものとなります。

著しい成長を見せる食品セグメント

- 小売売上高の急増は、個人消費の増加を示しています。可処分所得が増えれば、消費者は包装商品を含む様々な製品を購入する可能性が高くなります。その結果、食品、飲食品、その他の消費財に使用されるプラスチック包装フィルムの需要が増加します。

- ベトナムの統計総局は2023年7月発行の報告書で、ベトナムの小売総売上高は2022年に13%急増し、1,920億米ドルに達したと報告しています。この成長は、8.02%という過去最高のGDP成長率に後押しされた国内消費の復活によって推進されました。

- この移行は主に、中産階級の急速な成長と、若年層が多いという2つの要因によって推進されています。コンビニエンスストア、コーヒーショップ、スナック菓子店など、小売業や接客業が盛んになるにつれて、プラスチック包装フィルムの需要は大幅に増加する見込みです。

- 同国における食品消費の増加は小売業界の成長に直接影響を及ぼしており、プラスチック包装フィルムメーカーがベトナムを東南アジアにおける重要な市場と見なす好機となっています。

- 同国における食品消費の増加は、プラスチック包装フィルムに代表される様々な包装形態に対する大きな需要を支える主要な原動力となっています。例えば、ベトナム統計総局によると、同国の飲食品消費は2019年に260億7,000万米ドルであり、2024年には513億6,000万米ドルに増加すると予測されています。

ベトナムのプラスチック包装フィルム産業概要

ベトナムのプラスチック包装フィルム市場は統合されており、以下のような大手企業が数社あります。 Rang Dong Long An Plastic Joint Stock Company, Polifilm Vietnam, IFC Plastic, Feliz Plastic Vietnam, and Vietnam Packing Group occupying most of the market share. Several companies in Vietnam are forging alliances and engaging in mergers to bolster their market presence.

- 2023年10月東南アジア最大のBOフィルムメーカーであるA.J. Plast PLCの子会社A.J. Plast(Vietnam)は、ベトナムのビンズン省に最新鋭の二軸延伸プラスチックフィルム生産施設を開設しました。A.J.プラストPLCは、ASEAN地域の総合化学メーカーであるSCGCと密接な関係にあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 環境意識の高まりによる拡大生産者責任(EPR)の支持

- 市場抑制要因

- 市場成長の課題となる代替包装オプション

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(二軸延伸ポリプロピレン(BOPP)とキャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)と直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料、スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業用包装

- その他のエンドユーザー産業用途(農業、化学など)

- 食品

第7章 競合情勢

- 企業プロファイル

- Rang Dong Long An Plastic Joint Stock Company

- Polifilm Vietnam Co. Ltd

- IFC Plastic Co. Ltd

- Feliz Plastic Vietnam Co. Ltd

- Vietnam Packing Group

- Bao Ma Production & Trading Co. Ltd

- Nan Ya Plastics Corporation

- A.J. Plast(Vietnam)Co. Ltd

第8章 リサイクルと持続可能性の展望

第9章 市場の将来展望

The Vietnam Plastic Packaging Films Market size is estimated at 0.52 Million tonnes in 2024, and is expected to reach 0.61 Million tonnes by 2029, growing at a CAGR of 3.24% during the forecast period (2024-2029).

Key Highlights

- Vietnam remains a top choice for foreign enterprises, drawing them in with its promising investment prospects and potential partnerships. Vietnam is a beacon for foreign direct investment (FDI) across various industries, bolstered by a robust economy, strategic positioning, and investor-friendly policies.

- Vietnam saw a notable uptick in foreign investment, with figures hitting USD 9.27 billion, a 4.5% rise from 2023, as the General Statistics Office (GSO) reported. Notably, the nation attracted an estimated USD 6.28 billion in FDI in the first four months of 2024, marking a five-year high.

- Foreign direct investments often bring in capital that can be used to expand and modernize production facilities. With an increase in FDI, Vietnamese plastic packaging film manufacturers can enhance their production capabilities, improve efficiency, and increase output to meet both domestic and international demand.

- Vietnam's strategic location in Asia and proximity to major regional shipping lanes also position the nation's manufacturers well to maintain a strong focus on exports. The country boasts a coastline stretching around 3,200 kilometers, dotted with 114 seaports. This extensive coastline plays a crucial role in the nation's trade and transportation sectors, facilitating both domestic and international maritime activities.

- Vietnam's location and extensive coastline with numerous seaports make it an ideal hub for export-oriented manufacturing. As more foreign enterprises set up operations in Vietnam, the plastic packaging films produced can easily be exported to neighboring countries and other global markets, driving growth in the industry.

- Increasing awareness and concern about plastic waste and its environmental impact are leading to stricter regulations on plastic production and usage. Compliance with these regulations can increase costs and require investments in sustainable practices and materials.

- While Vietnam is attracting significant foreign investment, other countries in the region, such as China, India, and Thailand, also have strong plastic packaging industries. Competing with these established markets can be challenging for Vietnamese manufacturers.

Key Highlights

Key Highlights

Key Highlights

Vietnam Plastic Packaging Films Market Trends

Polyethylene Segment Is Expected to Witness Significant Growth

- ChemOrbis reported that for the week ending January 19, 2024, LDPE film import prices in Vietnam were assessed in the range of USD 1020-1100/ton. Meanwhile, HDPE film prices ranged from USD 1010-1070/ton, and LLDPE film prices stood at USD 970-1050/ton, all on a CIF basis. Compared to the prior week, LDPE film prices surged by USD 50-100/ton, HDPE film saw an increase of USD 20-50/ton, and LLDPE film remained stable or rose by up to USD 20/ton.

- The price increases, especially the significant spike in LDPE film prices, indicate strong demand for polyethylene films. Rising consumption in sectors such as food, agriculture, and consumer goods could drive this demand. Strong demand supports market growth as manufacturers ramp up production to meet it.

- The rise in plastic imports suggests a greater availability of raw materials, such as polyethylene, necessary for manufacturing packaging films. This increased supply can support the production capacity of local manufacturers, enabling them to meet higher demand and explore new markets.

- An article by the General Statistics Office of Vietnam, published in June 2023, reported that in 2022, Vietnam's imports of plastic in primary form were valued at around USD 12.4 billion, marking a notable surge from USD 7.58 billion in 2017.

- The significant import value may also reflect investments in higher-quality or more advanced forms of plastic. Access to better raw materials can lead to improvements in the quality and performance of polyethylene packaging films, making them more attractive to various industries, such as food, pharmaceuticals, and consumer goods.

Food Segment to Show Significant Growth

- The surge in retail sales indicates a rise in consumer spending. With higher disposable incomes, consumers are more likely to purchase a variety of products, including packaged goods. This, in turn, increases the demand for plastic packaging films used in food, beverages, and other consumer goods.

- Vietnam's General Statistical Office reported in its July 2023 publication that Vietnam's total retail sales surged by 13% in 2022, reaching USD 192 billion. This growth was propelled by a resurgence in domestic consumption, buoyed by the country's record-high GDP growth of 8.02%.

- This transition is chiefly propelled by two factors: the swift growth of the middle class and the country's predominantly youthful population. With convenience stores, coffee shops, snack outlets, and the more comprehensive retail and hospitality landscape thriving, the demand for plastic packaging films is poised for a significant upswing.

- The rising consumption of food in the country has directly influenced the growth of the retail industry, presenting a lucrative opportunity for plastic packaging film manufacturers to view Vietnam as a significant market in Southeast Asia.

- The country's increasing consumption of food is the primary driver behind the significant demand for various packaging modes, notably plastic packaging films. For instance, according to the General Statistics Office of Vietnam, the country's food and beverage consumption was USD 26.07 billion in 2019, and it is forecasted to increase to USD 51.36 billion by 2024.

Vietnam Plastic Packaging Films Industry Overview

The plastic packaging films market in Vietnam is consolidated, with a few major players such as Rang Dong Long An Plastic Joint Stock Company, Polifilm Vietnam Co. Ltd, IFC Plastic Co. Ltd, Feliz Plastic Vietnam Co. Ltd, and Vietnam Packing Group occupying most of the market share. Several companies in Vietnam are forging alliances and engaging in mergers to bolster their market presence.

- October 2023: A.J. Plast (Vietnam) Co. Ltd, a subsidiary of A.J. Plast PLC, the largest producer of BO film in Southeast Asia, marked the opening of its state-of-the-art biaxially oriented plastic film production facility in Binh Duong province, Vietnam. A.J. Plast PLC is closely affiliated with SCGC, a prominent player in integrated chemicals within the ASEAN region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Environmental Consciousness Fuels Embrace of Extended Producer Responsibility (EPR)

- 5.2 Market Restraints

- 5.2.1 Alternative Packaging Options Challenging the Market's Growth

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene (Biaxially Oriented Polypropylene (BOPP) and Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE) and Linear low-density Polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy and Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, and Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings and Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care and Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-user Industry Applications (Agricultural, Chemical, etc.)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Rang Dong Long An Plastic Joint Stock Company

- 7.1.2 Polifilm Vietnam Co. Ltd

- 7.1.3 IFC Plastic Co. Ltd

- 7.1.4 Feliz Plastic Vietnam Co. Ltd

- 7.1.5 Vietnam Packing Group

- 7.1.6 Bao Ma Production & Trading Co. Ltd

- 7.1.7 Nan Ya Plastics Corporation

- 7.1.8 A.J. Plast (Vietnam) Co. Ltd