欧州のプラスチック包装フィルム市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Europe Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550218

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

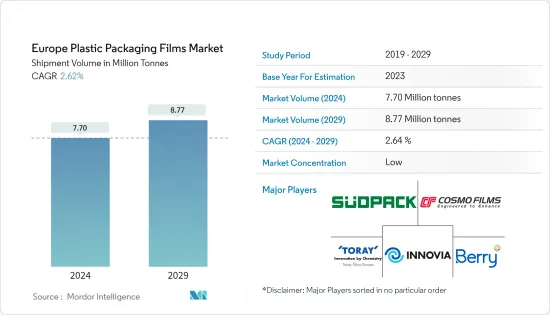

欧州のプラスチック包装フィルム市場規模(出荷量ベース)は、2024年の770万トンから2029年には877万トンに拡大し、予測期間(2024~2029年)のCAGRは2.62%と予測されます。

主なハイライト

- プラスチックフィルムはパーソナルケア製品のパッケージングにおいて重要な役割を果たしており、保存性を高め、破損を防ぎ、有効成分を保存することで、余分な防腐剤が不要になることも多いです。欧州のメーカーは最先端を走っており、酸素、湿気、香りを保護する先進ハイバリアフィルムを開発しています。これらのハイバリアフィルムは、製品の品質と効能を維持し、消費者に最適な状態で確実に届けるために不可欠です。

- 欧州のプラスチックフィルム市場は、食品包装用途の優位性を目の当たりにすることになると思われます。この変化は主に、硬質包装から軟質包装への移行を促進したダウンゲージングの動向の高まりに起因しています。バリアフィルムの需要急増は、肉、果物、野菜、魚介類を含む生鮮食品に対する食欲の増加に直接対応するものです。小売業者、製造業者、消費者のすべてが、製品の賞味期限の延長と包装廃棄物の削減を推進しており、この需要をさらに後押ししています。欧州のプラスチックコンバーター需要は、包装分野が39%という大きなシェアを占めています。

- 多様な物理的特性を持つポリエチレン(PE)は、最も普及しているプラスチック材料です。ポリエチレンの普及は、他のプラスチックとは一線を画す生産コスト効率の高さに起因しています。ポリエチレンは、一次包装用プラスチックの中で最も低い軟化点を誇り、省エネルギーにつながります。軟包装分野では、LDPE、HDPE、LLDPEがポリエチレンの主流となっています。

- 2024年3月、欧州連合理事会と欧州議会は、欧州連合の包装および包装廃棄物規則に関する交渉を終了しました。この法律は野心的な廃棄物削減目標を定め、EUで販売されるすべての包装にリサイクル可能で、リサイクル用のラベルを目立つように貼ることを義務付けています。また、包装サイズの小型化、プラスチック包装の最低再生利用率の義務化、再利用可能性の目標設定、特定の包装形態の禁止も行っています。これらの厳しい措置は、欧州のプラスチック部門にとって注目すべき課題です。この規制は、環境への影響を大幅に削減し、EU域内で循環型経済を促進することを目的としており、包装設計と材料における革新と持続可能性を奨励しています。

- 今後5年から10年の間に、欧州のプラスチックリサイクルは、規制当局からの圧力の高まりと、より環境意識の高い消費者層に後押しされ、大幅に急増する見通しです。政府と大手ブランドは、廃棄物を削減し、プラスチックのバリューチェーンの循環性を高めるための目標を継続的に改良しています。欧州のリサイクル業者の多くは、こうした目標を長い間目指してきたが、その成功はささやかなものだった。これは、化学業界各社がリサイクルへのアクセスを拡大し、最先端技術を採用し、持続可能性への取り組みを強化しようと努力しているにもかかわらず、です。

- さまざまな地域のメーカーが、新製品を開発するために研究開発に多額の投資を行い、施設を拡張しています。これには、リサイクル活動を製品開発戦略に組み込むことも含まれます。例えば、汎欧州イニシアチブの重要な担い手であるベリー・世界・グループのフレキシブル部門は、2024年3月に欧州の3施設でリサイクル能力を強化しました。この動きは、再生ポリマーのSustaneシリーズの生産を拡大するという、より広範なプロジェクトにおける戦略的ステップです。この構想は、再生プラスチックに関する同社の広範な世界ネットワークを活用することで、再生材料から作られた最高級フィルムに対する市場の旺盛な需要に応えるためのものです。

欧州プラスチック包装フィルム市場動向

食品分野が大きな市場シェアを占める

- プラスチックフィルムは、焼き菓子、ビスケット、冷凍食品、シーフード、チップス、スナック菓子、食肉、乳製品、ドライフルーツ、さらにはペットフードなど、多くの製品を包装するために欧州諸国で広く使用されています。欧州のバリアフィルム市場は、主に食品とペットフード部門に後押しされ、今後も成長する見通しです。この急成長は、健康、衛生、軽量性、環境への配慮を優先する消費者の包装嗜好の高まりに直接対応しています。

- 食品分野の各製品は、それぞれ独自の品質と包装要件を備えています。そのため、食品包装は包装から消費に至るまで適切な環境条件を維持することが不可欠です。柔軟性があり、溶剤を含まず、不透過性の共押出構造(単層または多層構造)を持つプラスチックフィルムは、包む食品と化学反応を起こさないように設計されています。これらのフィルムは、鉱物油や紫外線の移行を制限するだけでなく、食品が酸素、二酸化炭素、湿気と相互作用するのを防ぎます。特殊な素材から作られたこれらの硬いバリアは、食品の色、味、食感、香り、風味を保つのに役立っています。

- この地域における食品消費の増加は、多様な食品に合わせた様々なプラスチックフィルムの需要増加を支える重要な原動力となっています。この動向は、食品の安全性を確保し、賞味期限を延ばし、製品のプレゼンテーションを強化する、より優れたパッケージング・ソリューションの必要性によって後押しされています。消費者が健康志向を強め、利便性を求めるようになるにつれ、食品包装用プラスチックフィルム市場は拡大を続け、革新と成長の機会を提供しています。

- ドイツでは、食品への消費支出が顕著な上昇を見せ、消費動向のエスカレートに牽引されて2019年の1,766億4,000万米ドルから2023年には2,199億4,000万米ドルに上昇しました。この増加は、可処分所得の増加、食生活の嗜好の変化、人口の拡大などの要因に影響された多様な食品に対する需要の増加を反映しています。この動向は、食品関連企業や投資家にとって市場の潜在力が大きいことを示しています。

- プラスチックフィルムは、欧州の食品産業において、保存性を高め、湿気や酸素に対するバリアとして製品を外的要因から保護するという重要な役割を果たしています。斬新な用途に後押しされて進化する食品包装の需要は、包装材料により高い基準を設定しつつあります。重要な焦点は、より効果的なパッケージング・ソリューションを作り出すためのバリア性向上フィルムに対する差し迫った需要です。包装フィルムのバリア特性を向上させることは、食品の保存期間を延ばし、腐敗や損傷のリスクを軽減するために不可欠です。一般的なアプローチのひとつは、包装シートをPVDCまたはアルミニウムでコーティングし、バリア機能を強化することです。

- 包装業界のメーカーは、食品包装用に調整された革新的なプラスチックフィルムを導入し、製品の安全性と保存性を高めています。例えば、フレキシブル食品包装のサプライチェーンにまたがる企業が協力して、斬新なスナック包装を発表しました。この革新的なパッケージは、ペプシコのブランドであるSunbitesに使用されており、50%再生プラスチックで構成され、厳しい食品接触規制を満たしています。英国とアイルランドで発表されたこのパッケージは、先進的なリサイクルプロセスを用いて作られており、リサイクル素材が食品接触パッケージや医療機器に関するEU規制基準を満たしていることを保証しています。この最先端のPPフィルムを活用し、ペプシコ社は環境に優しいサンビッツ包装を英国で展開しました。この取り組みは、ペプシコ・ポジティブの一環であり、2030年までに欧州のクリスプ&チップスの袋から化石由来のバージンプラスチックを全廃することを目的としたプログラムです。

ドイツが市場で大きなシェアを占める見込み

- ドイツは欧州をリードする医薬品市場であり、米国、中国、日本に次いで世界第4位です。さらに、ドイツの医薬品セクターではフレキシブル包装の採用が急増しています。この変化は主に、酸素や湿気から医薬品を保護し、消費されるまで効能を維持する包装の能力によってもたらされています。

- 医薬品研究、販売、製造の拠点としてのドイツの評判は、その先駆的なイノベーション、「世界の薬局」としての歴史的地位、ヘルスケア製品に対する需要の高まりによって強化されています。欧州最大の医薬品市場は、人口動態の変化、慢性疾患の増加、予防・セルフケア対策の重視の高まりに後押しされ、ドイツ経済全体を上回っています。

- 例えば、軟包装のスペシャリストであるコベリス社は、2023年11月、医療機器用に特別に設計されたリサイクル可能な新しい熱成形フィルムを発表しました。ウィーンに本社を置く同社は、ドイツのデュッセルドルフで開催されたCompamed見本市で「Formpeel P」を初披露しました。この共押出フィルムは耐穿孔性があり、剥離可能なポリエチレン(PE)またはポリオレフィン(PO)ベースと組み合わせることができます。持続可能な蓋フィルムと組み合わせることで、ポリアミドを使用しないこれらのボトムフィルムは、医療用途において環境に優しい魅力的なパッケージング・ソリューションとなります。

- ドイツの人口が成熟するにつれ、食品の品質、健康、幸福を重視する方向に顕著な変化が見られます。この進化する考え方は、新しい食品動向や文化的影響に対する受容性と相まって、プラスチックフィルム包装に大きな機会をもたらす道を開いています。高品質で健康志向の食品に対する需要の高まりは、鮮度を保ち賞味期限を延長する先進パッケージング・ソリューションを必要としています。さらに、世界の料理動向の影響は、多様な消費者の嗜好に対応する包装デザインの革新を促しています。

- さらに、ドイツはインターネット普及の急増に牽引され、欧州で最も急成長しているeコマース市場の一つとして際立っています。2023年までに、ドイツにおけるeコマースの普及率はすでに80%に達しています。さらに、同国のオンライン人口は2020年の6,240万人から2025年には6,840万人に増加すると予測されています。注目すべきは、プラスチックフィルム包装がeコマース界で人気を集めていることです。その魅力は強化された保護と耐久性にあり、商品を破損やこぼれから効果的に保護し、束ねられた商品が無傷であることを保証します。

- さらに、ドイツの小売売上高は一貫した成長を見せています。2023年、ドイツの小売セクターの売上高は約7,037億8,000万米ドルで、2019年の5,911億2,000万米ドルから顕著な伸びを示しました。この急増は、プラスチックフィルムに対する需要の高まりを強調し、技術革新と持続可能性を重視する傾向が強まっていることを浮き彫りにしています。小売販売収入の継続的な増加は、ドイツの堅調な経済環境と消費者心理を反映しています。さらに、収益の増加は、世界の持続可能性の動向に合わせて、パッケージング技術、特に環境に優しいプラスチックフィルムの開発の先進化を推進しています。

欧州プラスチック包装フィルム産業の概要

欧州のプラスチック包装用フィルム市場は断片化されており、Innovia Films(CCL Industries Inc.)、TORAY FILMS EUROPE、Berry Global Inc.、SUDPACK Holding GmbH、Cosmo Filmsなど、複数の世界的・地域的プレーヤーが競争の激しい市場空間で注目を競っています。この市場の特徴は、製品の差別化が低いこと、製品の普及が進んでいること、競合が多いことです。

- 2024年7月:素材開発・製造の大手であるInnovia Filmsは、サステイナブル・フィルムのラインアップ拡充を発表しました。この拡張「アンコール」は二軸延伸ポリプロピレン(BOPP)フィルムに焦点を当て、特に食品接触用途に合わせたケミカルリサイクルポリマーの取り込みに重点を置いています。さらに、Innovia FilmsはPrevented Ocean Plasticと戦略的パートナーシップを結び、POP由来の素材を30%配合した新しいフィルム組成を実現しました。

- 2024年3月SUDPACKとSN Maschinenbauは共同で、スパウト付きのスタンドアップパウチ用のリサイクル可能なフィルムソリューションを発表しました。リシーラブルデザインが高く評価されているこれらのパウチは、フルーツピューレから高温充填や低温殺菌が必要なものまで、液体やペースト状の食品専用に作られています。SUDPACKは、このパウチがポリプロピレンベースのフィルムから作られているため、リサイクル基準を満たしていることを強調しています。さらに、このパウチにはPP製の注ぎ口があり、MENSHEN LoTUS技術が組み込まれているため、正確な熱分布と導電性の調整によってシームレスな接続が保証されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装ソリューションへの需要の高まり

- 様々な産業におけるプラスチックフィルム需要の増加が成長の可能性を示す

- 市場の課題

- プラスチックに対する政府の厳しい法律と規制

- 貿易シナリオ

- EXIMデータ

- 貿易分析(輸出入上位5カ国、価格分析、主要港など)

- 業界規制と政策と規格

- 技術情勢

- 価格動向分析

第6章 市場セグメンテーション

- タイプ別

- ポリプロピレン(PP)(二軸延伸ポリプロピレン(BOPP)、キャストポリプロピレン(CPP))

- ポリエチレン(低密度ポリエチレン(LDPE)、直鎖状低密度ポリエチレン(LLDPE))

- ポリエチレンテレフタレート(二軸延伸ポリエチレンテレフタレート(BOPET))

- ポリスチレン

- バイオベース

- PVC、EVOH、PETG、その他のフィルムタイプ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料、スパイス、スプレッド類、ソース、コンディメントなど)

- ヘルスケア

- パーソナルケア、ホームケア

- 工業包装

- その他エンドユーザー産業(農業、化学など)

- 食品

- 国別

- フランス

- ドイツ

- イタリア

- 英国

- スペイン

- ポーランド

第7章 競合情勢

- 企業プロファイル

- Innovia Films(CCL Industries Inc.)

- TORAY FILMS EUROPE

- Berry Global Inc.

- Klockner Pentaplast

- SUDPACK Holding GmbH

- Taghleef Industries

- SRF LIMITED

- Cosmo Films

- Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- Bauerschmidt Plastics GmbH

第8章 投資分析

第9章 市場の将来

目次

The Europe Plastic Packaging Films Market size in terms of shipment volume is expected to grow from 7.70 Million tonnes in 2024 to 8.77 Million tonnes by 2029, at a CAGR of 2.62% during the forecast period (2024-2029).

Key Highlights

- Plastic films play a crucial role in personal care product packaging, enhancing shelf life, preventing breakage, and preserving active ingredients, often eliminating the need for extra preservatives. European manufacturers are at the forefront, developing advanced high-barrier films that offer oxygen, moisture, and scent protection for their packaged goods. These high-barrier films are essential in maintaining the quality and efficacy of products, ensuring they reach consumers in optimal condition.

- The European plastic film market is poised to witness a dominance of food packaging applications. This shift is primarily attributed to the rising trend of downgauging, which has facilitated the move from rigid to flexible packaging. The surge in demand for barrier films is a direct response to the increasing appetite for fresh produce, including meat, fruits, vegetables, and seafood. Retailers, manufacturers, and consumers are all pushing for extended product shelf life and reduced packaging waste, further fueling this demand. The packaging segment dominated Europe's demand for plastics converters, capturing a significant 39% share.

- Due to its diverse physical properties, polyethylene (PE) is the most prevalent plastic material. Its widespread adoption can be attributed to its cost-efficiency in production, which sets it apart from other plastics. Polyethylene boasts the lowest softening point among primary packaging plastics, leading to energy savings. In the flexible packaging sector, LDPE, HDPE, and LLDPE emerge as the go-to variants of polyethylene.

- In March 2024, the Council of the European Union and the European Parliament concluded negotiations on the European Union's Packaging and Packaging Waste Regulation. This legislation establishes ambitious waste reduction targets, requiring all EU-sold packaging to be recyclable and prominently labeled for recycling. It also enforces smaller packaging sizes, mandates minimum recycled content for plastic packaging, sets reusability goals, and bans specific packaging formats. These stringent measures present a notable challenge to the European plastics sector. The regulation aims to significantly reduce environmental impact and promote a circular economy within the European Union, encouraging innovation and sustainability in packaging design and materials.

- Over the next five to ten years, European plastic recycling is poised for a significant surge, driven by mounting pressure from regulators and a more environmentally conscious consumer base. Governments and major brands are continually refining targets to reduce waste and enhance the circularity of the plastic value chain. While many European recyclers have long aimed for these goals, their success has been modest. This is despite efforts from chemical industry players to expand recycling access, adopt cutting-edge technologies, and ramp up sustainability initiatives.

- Manufacturers across various regions are heavily investing in R&D and expanding their facilities to develop new products. This includes integrating recycling activities into their product development strategies. For instance, Berry Global Group Inc.'s Flexibles division, a critical player in a pan-European initiative, bolstered the recycling capabilities in three European facilities in March 2024. This move is a strategic step in its broader project to scale up the production of its Sustane line of recycled polymers. The initiative is primed to cater to the surging market appetite for top-tier films crafted from recycled materials by tapping into the company's extensive global network for recycled plastics.

Europe Plastic Packaging Films Market Trends

Food Segment to Hold Significant Market Share

- Plastic films are extensively used in European nations to wrap many products: baked goods, biscuits, frozen foods, seafood, chips, snacks, meat, dairy, dry fruits, and even pet food. The European barrier film market is poised for growth in the future, primarily fueled by the food and pet food sectors. This surge directly responds to consumers' escalating packaging preferences, prioritizing health, hygiene, lightweight properties, and eco-friendliness.

- Each product in the food sector comes with its unique set of qualities and packaging requirements. Consequently, it's imperative that food packaging maintains the proper environmental conditions from the moment of packaging to consumption. With their flexible, solvent-free, and impermeable co-extruded structure (comprising single or multiple layers), plastic films are designed not to react chemically with the food they encase. These films go beyond limiting mineral oil and UV radiation migration; they prevent food from interacting with oxygen, carbon dioxide, or moisture. Crafted from specialized materials, these rigid barriers are instrumental in preserving the food's color, taste, texture, aroma, and flavor.

- Rising food consumption in the region is a crucial driver behind the increasing demand for various plastic films tailored to diverse food products. This trend is fueled by the need for better packaging solutions that ensure food safety, extend shelf life, and enhance product presentation. As consumers become more health-conscious and seek convenience, the market for plastic films in food packaging continues to expand, offering opportunities for innovation and growth.

- In Germany, consumer spending on food witnessed a notable rise, climbing from USD 176.64 billion in 2019 to USD 219.94 billion in 2023, driven by escalating consumption trends. This increase reflects a growing demand for diverse food products, influenced by factors such as higher disposable incomes, changing dietary preferences, and an expanding population. The trend indicates a robust market potential for food-related businesses and investors.

- Plastic films play a crucial role in the European food industry, enhancing shelf life and shielding products from external factors by serving as barriers against moisture and oxygen. Evolving food packaging demands, driven by novel applications, are setting higher standards for packaging materials. A key focus area is the pressing demand for enhanced barrier films to craft more effective packaging solutions. Improving the barrier properties of packaging films is essential to prolong food shelf life and mitigate the risks of spoilage and damage. One common approach is to coat the packaging sheet with either PVDC or aluminum, enhancing its barrier capabilities.

- Manufacturers in the packaging industry are introducing innovative plastic films tailored for food packaging, enhancing product safety and shelf life. For instance, companies spanning the flexible food packaging supply chain collaborated to introduce a novel snack packaging. This innovative packaging, used for Sunbites, a brand under PepsiCo, comprises 50% recycled plastic and meets stringent food contact regulations. The packaging, unveiled in the United Kingdom and Ireland, is crafted using an advanced recycling process that ensures the recycled materials meet EU regulatory standards for food-contact packaging and medical devices. Leveraging these cutting-edge PP films, PepsiCo rolled out the eco-friendly Sunbites packaging in the United Kingdom. This initiative is part of PepsiCo Positive, the company's program aimed at phasing out virgin fossil-based plastics from its European crisp and chip bags by 2030.

Germany Expected to Hold Significant Share in the Market

- Germany is Europe's leading pharmaceutical market and ranks fourth globally, trailing only the United States, China, and Japan. Moreover, the pharmaceutical sector in Germany has seen a surge in the adoption of flexible packaging. This shift is primarily driven by the packaging's ability to shield medications from oxygen and moisture, preserving their efficacy until consumption.

- Germany's reputation as a pharmaceutical research, sales, and manufacturing hub is bolstered by its pioneering innovations, historical status as the "world's pharmacy," and a rising demand for healthcare products. Europe's largest pharmaceutical market is outpacing the overall German economy, propelled by shifting demographics, a rise in chronic illnesses, and an increasing emphasis on preventive and self-care measures.

- For instance, Coveris, a specialist in flexible packaging, unveiled a new recyclable thermoforming film in November 2023 designed specifically for medical devices. The company, headquartered in Vienna, debuted 'Formpeel P' at the Compamed trade show in Dusseldorf, Germany. The co-extruded film is puncture-resistant and can be paired with either a peelable polyethylene (PE) or polyolefin (PO) base. When combined with a sustainable lidding film, these bottom films, free of polyamide, present a compelling eco-friendly packaging solution for medical applications.

- As the German population is maturing, there has been a notable shift toward valuing food quality, health, and well-being. This evolving mindset, coupled with a receptiveness to new food trends and cultural influences, is paving the way for significant opportunities in plastic film packaging. The increasing demand for high-quality, health-conscious food products necessitates advanced packaging solutions that preserve freshness and extend shelf life. Additionally, the influence of global culinary trends is driving innovation in packaging designs to cater to diverse consumer preferences.

- Further, Germany stands out as one of Europe's fastest-growing e-commerce markets, driven by a surge in internet adoption. By 2023, e-commerce penetration in Germany had already hit 80%. Moreover, the country's online population is projected to grow from 62.4 million in 2020 to 68.4 million by 2025. Notably, plastic film packaging is gaining traction in e-commerce circles. Its appeal lies in its enhanced protection and durability, effectively safeguarding products against breakage and spills and ensuring bundled items stay intact.

- Further, retail sales revenue in Germany has shown consistent growth. In 2023, the German retail sector generated approximately USD 703.78 billion in sales revenue, marking a notable increase from USD 591.12 billion in 2019. This surge underscores the rising demand for plastic film and highlights a growing emphasis on innovation and sustainability. The continuous growth in retail sales revenue reflects Germany's robust economic environment and consumer confidence. Additionally, the increased revenue has driven advancements in packaging technologies, particularly in the development of eco-friendly plastic films, aligning with global sustainability trends.

Europe Plastic Packaging Films Industry Overview

The European plastic packaging films market is fragmented, with several global and regional players, such as Innovia Films (CCL Industries Inc.), TORAY FILMS EUROPE, Berry Global Inc., SUDPACK Holding GmbH, and Cosmo Films, vying for attention in a contested market space. This market is characterized by low product differentiation, growing levels of product penetration, and high levels of competition.

- July 2024: Innovia Films, a leading material developer and producer, unveiled an expansion to its sustainable film lineup. This extension, Encore, focuses on biaxially oriented polypropylene (BOPP) films, emphasizing the incorporation of chemically recycled polymers specifically tailored for food-contact applications. Furthermore, Innovia Films has forged a strategic partnership with Prevented Ocean Plastic, resulting in a novel film composition integrating 30% of POP-sourced materials.

- March 2024: SUDPACK and SN Maschinenbau collaborated to introduce a recyclable film solution tailored for stand-up pouches featuring spouts. Lauded for their resealable design, these pouches are crafted explicitly for liquid or pasty foods, ranging from fruit purees to items requiring hot filling and pasteurization. SUDPACK emphasizes that the pouches are crafted from polypropylene-based films, thus meeting recyclability standards. Additionally, the pouches feature PP spouts, integrating MENSHEN LoTUS technology, ensuring a seamless connection through precise heat distribution and conductivity coordination.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Increasing Demand for Plastic Films Across Various Industries Indicates Growth Potential

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation Toward Plastic

- 5.3 Trade Scenario

- 5.3.1 EXIM Data

- 5.3.2 Trade Analysis (Top 5 Import-Export Countries, Price Analysis, and Key Ports, Among others)

- 5.4 Industry Regulation, Policy and Standards

- 5.5 Technology Landscape

- 5.6 Pricing Trend Analysis

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy and Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, and Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings and Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care and Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-user Industries (Agricultural, Chemical, Etc.)

- 6.2.1 Food

- 6.3 By Country

- 6.3.1 France

- 6.3.2 Germany

- 6.3.3 Italy

- 6.3.4 United Kingdom

- 6.3.5 Spain

- 6.3.6 Poland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Innovia Films (CCL Industries Inc.)

- 7.1.2 TORAY FILMS EUROPE

- 7.1.3 Berry Global Inc.

- 7.1.4 Klockner Pentaplast

- 7.1.5 SUDPACK Holding GmbH

- 7.1.6 Taghleef Industries

- 7.1.7 SRF LIMITED

- 7.1.8 Cosmo Films

- 7.1.9 Mitsubishi Polyester Film GmbH(Mitsubishi Chemical Group)

- 7.1.10 Bauerschmidt Plastics GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日