|

市場調査レポート

商品コード

1693530

欧州の微量栄養素肥料の市場シェア分析、産業動向、成長予測(2025年~2030年)Europe Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の微量栄養素肥料の市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

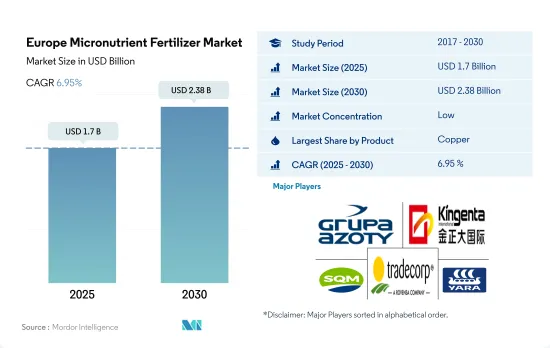

欧州の微量栄養素肥料の市場規模は2025年に17億米ドルと推定され、2030年には23億8,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは6.95%で成長します。

亜鉛がこの地域の微量栄養素肥料市場を独占

- 欧州ではロシアが微量栄養素肥料の大半を占め、欧州の微量栄養素肥料市場の24.2%を占めています。さらに、2023~2030年の間にCAGR 7.0%を記録すると予測されています。

- 形態別では、特殊タイプの微量栄養素市場が2022年に最も大きく、市場金額の62.6%を占め、畑作物に主に適用され87.0%でした。技術的・科学的進歩の増加に伴い、特殊肥料の用途は主に畑作物に使用されています。従来型肥料の微量栄養素市場は37.3%を占め、この肥料の用途は畑作物が中心で88.8%でした。

- 栄養素のタイプ別では、亜鉛がこの地域の微量栄養素肥料市場を独占し、2022年の市場金額の29.2%を占めました。亜鉛は植物酵素系の主要成分です。亜鉛は様々な種類の酵素の活性化を助け、炭水化物代謝を促進し、次いで銅が26.4%、モリブデンが15.7%を占めます。微量栄養素肥料はこの地域では葉面散布が主流で、2022年の市場額の65.0%を占め、次いで施肥が34.9%です。

- 植物や土壌における微量栄養素の欠乏は着実に増加しており、欧州連合(EU)では大きな懸念材料となっています。土壌の健全性の枯渇、高価値作物の栽培面積の着実な増加、より高い生産性の要求、先進的肥料に関する意識の向上とその採用の増加といった要因が、2023~2030年にかけて微量栄養素肥料の地域市場を牽引すると予想されます。

フランスは欧州で最大の微量栄養素肥料市場です。

- 2022年、フランスは欧州の微量栄養素肥料市場でトップの座を占め、2億1,840万米ドルに相当する14.1%の大きな金額シェアを獲得しました。フランスの農業従事者は土壌における微量栄養素の欠乏の重要性を認識するようになり、微量栄養素肥料の需要急増につながっています。

- ロシアは2022年に1億4,930万米ドル、9.6%の市場シェアを獲得し、欧州の主要微量栄養素肥料市場に浮上しました。微量栄養素の中では、亜鉛ベースの肥料がロシア市場を独占し、総量の28.2%を占めました。

- ウクライナは欧州の微量栄養素肥料市場の13.8%を占め、2022年の市場規模は2億1,410万米ドルです。同国の同年の微量栄養素肥料の消費量は6万1,200トンでした。特筆すべきは、ウクライナ市場はCOVID-19の大流行がもたらす課題の中でも一貫した成長を示していることです。

- 欧州の微量栄養素肥料の消費は、熱波や進行中のエネルギー危機による逆風に直面する可能性があります。しかし、農業従事者が先端技術や肥料、特に特殊微量栄養素の変種を受け入れつつあることが原動力となり、市場は成長する態勢を整えています。

- 欧州の微量栄養素肥料市場は、土壌の健康状態の悪化、高価値作物の栽培拡大、生産性向上の追求、肥料の入手可能性の増大といった要因によって推進されるものと考えられます。

欧州の微量栄養素肥料市場動向

国内需要と輸出需要を満たすため、畑作物の栽培面積は着実に増加しています。

- 欧州では、菜種、小麦、ライ麦、ライ小麦などの畑作物が主要冬作物であり、トウモロコシ、ひまわり、米、大豆は夏作物です。大麦は冬用と春用の両方が広く出回っています。欧州における主要食用作物の収穫面積は、主に人口増加と食用穀物需要の増加により、着実に増加しています。畑作物は2017年に7万8,500haを占め、2022年には10万8,000haに増加します。

- 欧州連合の2022年の普通小麦収穫量は2億8,270万トンで、これは全穀物収穫量の54.0%に相当します。これは2020年より1,100万トン多く、9.3%の増加でした。この増加は、収穫面積の増加(5.6%増の2,180万ヘクタール)と見かけの収量の改善を反映しています。

- 2019~2022年にかけて、この地域内の収穫面積は34%減少しました。この全体的な減少にもかかわらず、トウモロコシ/メイズの栽培面積は11%、小麦の栽培面積は2%それぞれ増加し、他の畑作物の栽培面積は同期間に減少しました。2023~2030年にかけて、農業従事者は収量を向上させ、近年観察された収穫面積の全体的減少の影響を緩和することを目的として、肥料の使用量を増加させると予想されます。

- そのため、農業従事者は増大する需要を満たすために収量と穀物生産量を向上させなければならないというプレッシャーが高まっており、また畑作物全体の栽培面積が増加していることから、肥料市場は2023~2030年の間に大きく成長すると予想されます。

亜鉛はこの地域で最も使用される微量栄養素肥料となっている

- 欧州の土壌における微量栄養素の欠乏は、浸出損失、過度の降雨、浅い土壌プロファイルなどの要因に起因します。2022年、欧州の畑作物への微量栄養素の平均施用量は3.85kg/ヘクタールでした。2022年には、亜鉛、銅、鉄、マンガン、ホウ素が最も高い市場規模を占め、そのシェアはそれぞれ38.28%、25.09%、13.68%、11.68%、4.168%、0.021%です。マンガンの平均施用量は9.33kg/haで、この地域の微量栄養素肥料の総消費量の11.68%を占めています。マンガンの不足は、大豆、小麦、サトウキビ、トウモロコシのような主要畑作作物の生産を著しく阻害しています。

- 作物の中では、小麦、ソルガム、大豆、綿花が微量栄養素肥料の主要消費者で、トウモロコシとコメのシェアは小さかりました。2022年には小麦がトップで、マンガンを11.54kg/ha、亜鉛を5.87kg/ha、銅を6.60kg/ha消費しました。亜鉛はこの地域で最も広く使われている微量栄養素肥料として浮上し、2022年の総消費量の38.28%を占め、平均施用量は5.72kg/haです。銅、鉄、ホウ素がそれに続き、平均施用量はそれぞれ6.31kg/ha、3.70kg/ha、1.50kg/haです。

- 微量栄養素は、作物にバランスのとれた栄養を供給する上で重要な役割を果たしており、欠乏すると作物の生育に支障をきたします。その結果、欧州における微量栄養素肥料の市場は、土壌の微量栄養素欠乏症の蔓延がエスカレートしていることが大きな燃料となって、成長を目の当たりにしています。

欧州の微量栄養素肥料産業概要

欧州の微量栄養素肥料市場はセグメント化されており、上位5社で21.44%を占めています。この市場の主要企業は、Grupa Azoty S.A.(Compo Expert)、Kingenta Ecological Engineering Group、Sociedad Quimica y Minera de Chile SA、Trade Corporation International、Yara International ASAなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑設備のある農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品

- ホウ素

- 銅

- 鉄

- マンガン

- モリブデン

- 亜鉛

- その他

- 適用方法

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 生産国

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- AGLUKON Spezialduenger GmbH & Co.

- Fertiberia

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Sociedad Quimica y Minera de Chile SA

- Trade Corporation International

- Valagro

- Verdesian Life Sciences

- Yara International ASA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Europe Micronutrient Fertilizer Market size is estimated at 1.7 billion USD in 2025, and is expected to reach 2.38 billion USD by 2030, growing at a CAGR of 6.95% during the forecast period (2025-2030).

Zinc dominates the micronutrient fertilizers market in the region

- In Europe, Russia accounted for the majority of micronutrient fertilizers, holding 24.2% of the value of Europe's micronutrient fertilizer market. Moreover, it is anticipated to register a CAGR of 7.0% between 2023 and 2030.

- By form, the specialty type micronutrient market was the largest in 2022, accounting for 62.6% of the market value, and was majorly applied to field crops at 87.0%. With increased technological and scientific advancements, specialty fertilizer applications are primarily used for field crops. The conventional type fertilizer micronutrient market accounted for 37.3%, and this fertilizer application was majorly applied to field crops at 88.8%.

- By nutrient type, zinc dominated the micronutrient fertilizers market in the region, accounting for 29.2% of the market value in 2022. Zinc is a major component of plant enzyme systems. Zinc aids in the activation of various types of enzymes, boosting carbohydrate metabolism, followed by copper at 26.4%, and molybdenum accounting for 15.7%. Micronutrient fertilizers are mostly applied through foliar application in the region, accounting for 65.0% of the market value in 2022, followed by fertigation at 34.9%.

- Micronutrient deficiency in plants and soil has been steadily increasing and has become a major cause of concern in the European Union. Factors such as depleting soil health, steadily increasing area under high-value crops, the requirement for higher productivity, and improved awareness about advanced fertilizers and their increasing adoption are expected to drive the regional market for micronutrient fertilizers between 2023 and 2030.

France is the largest micronutrient fertilizer market in the European region.

- In 2022, France held the top spot in the Europe's micronutrient fertilizer market, commanding a significant 14.1% value share, equivalent to USD 218.4 million. French farmers are increasingly recognizing the significance of micronutrient deficiencies in their soils, leading to a surge in demand for these fertilizers.

- Russia emerged as the leading micronutrient fertilizer market in Europe, capturing a market share of 9.6% and a value of USD 149.3 million in 2022. Among the micronutrients, zinc-based fertilizers dominated the Russian market, comprising 28.2% of the total volume.

- Ukraine accounted for 13.8% of the European micronutrient fertilizer market, valued at USD 214.1 million in 2022. The country consumed 61.2 thousand metric tons of these fertilizers in the same year. Notably, the Ukrainian market has exhibited consistent growth, even amidst the challenges posed by the COVID-19 pandemic.

- Europe's micronutrient fertilizer consumption might face headwinds from heatwaves and an ongoing energy crisis. However, the market is poised for growth, driven by farmers' increasing embrace of advanced technologies and fertilizers, particularly specialty micronutrient variants.

- The European micronutrient fertilizer market is set to be propelled by factors such as deteriorating soil health, expanding cultivation of high-value crops, the pursuit of enhanced productivity, and the growing availability of fertilizers.

Europe Micronutrient Fertilizer Market Trends

The cultivation area of field crops is steadily rising to meet domestic needs and export demand

- Field crops, such as rapeseed, wheat, rye, and triticale, are the main winter crops in Europe, while maize, sunflowers, rice, and soybean are summer crops. Both winter and spring types of barley are widely available. The area harvested under major food crops in Europe has been steadily increasing, primarily due to the growing population and increasing demand for food grains. Field crops accounted for 78.5 thousand ha in 2017, which increased to 108 thousand ha in 2022.

- The European Union harvested 282.7 million tons of common wheat in 2022, the equivalent of 54.0% of all cereal grains harvested. This was 11.0 million tons more than in 2020, an increase of 9.3%. This upturn reflected a rise in the area harvested (up 5.6% to 21.8 million hectares) and improved apparent yields.

- Between 2019 and 2022, there was a notable 34% decline in the harvested area within the region. Despite this overall reduction, the areas dedicated to corn/maize and wheat cultivation experienced increases of 11% and 2%, respectively, while the acreages for other field crops decreased during the same period. It is anticipated that farmers will augment their fertilizer usage during the 2023-2030 period, aiming to enhance yields and mitigate the impact of the overall decrease in harvested areas observed in recent years.

- Therefore, with rising pressure on farmers to improve yield and grain production to meet the growing demand and with the overall field crop cultivation area increasing, the fertilizer market is expected to grow significantly during the 2023-2030.

Zinc has become the most used micronutrient fertilizer in the region

- Micronutrient deficiencies in European soils stem from factors such as leaching losses, excessive rainfall, and shallow soil profiles. In 2022, the average application of micronutrients for field crops in Europe stood at 3.85 kg/hectare. In 2022, zinc, copper, iron, manganese, and boron commanded the highest market values, with shares of 38.28%, 25.09%, 13.68%, 11.68%, 4.168%, and 0.021%, respectively. Manganese, with an average application rate of 9.33 kg/ha, led the pack, accounting for 11.68% of the total micronutrient fertilizer consumption in the region. Its scarcity severely hampers the production of key field crops like soy, wheat, sugarcane, and maize.

- Among the crops, wheat, sorghum, soybean, and cotton were the major consumers of micronutrient fertilizers, while corn and rice had a smaller share. In 2022, wheat topped the charts, consuming 11.54 kg/ha of manganese, 5.87 kg/ha of zinc, and 6.60 kg/ha of copper. Zinc emerged as the most widely used micronutrient fertilizer in the region, accounting for 38.28% of the total consumption in 2022, with an average application rate of 5.72 kg/ha. Copper, iron, and boron followed with average application rates of 6.31, 3.70, and 1.50 kg/ha, respectively.

- Micronutrients play a crucial role in providing balanced nutrition to crops, and their deficiency can hinder crop growth. As a result, the market for micronutrient fertilizers in Europe is witnessing growth, significantly fueled by the escalating prevalence of soil micronutrient deficiencies.

Europe Micronutrient Fertilizer Industry Overview

The Europe Micronutrient Fertilizer Market is fragmented, with the top five companies occupying 21.44%. The major players in this market are Grupa Azoty S.A. (Compo Expert), Kingenta Ecological Engineering Group Co., Ltd., Sociedad Quimica y Minera de Chile SA, Trade Corporation International and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Netherlands

- 5.4.5 Russia

- 5.4.6 Spain

- 5.4.7 Ukraine

- 5.4.8 United Kingdom

- 5.4.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 AGLUKON Spezialduenger GmbH & Co.

- 6.4.2 Fertiberia

- 6.4.3 Grupa Azoty S.A. (Compo Expert)

- 6.4.4 Haifa Group

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Sociedad Quimica y Minera de Chile SA

- 6.4.7 Trade Corporation International

- 6.4.8 Valagro

- 6.4.9 Verdesian Life Sciences

- 6.4.10 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms