|

市場調査レポート

商品コード

1693534

アジア太平洋の微量栄養素肥料:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia-Pacific Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の微量栄養素肥料:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 223 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

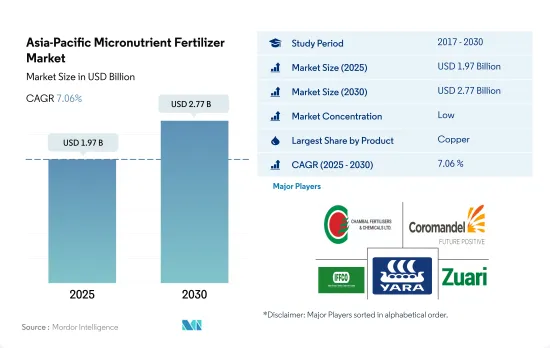

アジア太平洋の微量栄養素肥料の市場規模は、2025年には19億7,000万米ドルと推定され、2030年には27億7,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは7.06%で成長する見込みです。

意識の高まりと農業生産における重要性が、この地域の市場を牽引する可能性があります。

- ホウ素はこの地域で最も消費されている微量栄養素であり、2022年の消費量シェアは26.5%でした。ホウ素消費の大部分は、この地域の土壌に起因するもので、この土壌は含水率が低く、窒素レベルが高いため、植物によるホウ素の取り込みが制限され、ホウ素微量栄養素の利用が増加しています。

- アジア太平洋では、亜鉛が消費量の点で第2位の市場シェアを占め、そのシェアは26.2%、2022年の数量は15万9,100トンでした。亜鉛は植物の成長と開発に重要な役割を果たすため、今後数年間は需要の増加が続くと予想されます。

- 銅は2022年のアジア太平洋の微量栄養素市場の28.6%を占めます。少量でも必要とされる重要な微量栄養素です。成長中の多くの重要な植物反応において触媒として働き、タンパク質形成において重要な役割を果たします。

- 鉄はこの地域で3番目に消費量の多い微量栄養素であり、2022年には全微量栄養素の中で20.8%のシェアを占めます。鉄は多くの酵素を含み、葉緑素形成の触媒として働くため、植物の成長と開発に重要な役割を果たします。土壌中の鉄欠乏の増加は、市場の成長を促進すると予想されます。

- したがって、より高い収量と生産性の必要性、作物栽培における微量栄養素の重要性に関する農業従事者の知識の高まりといった要因のおかげで、この地域の微量栄養素市場は2023~2030年の間にCAGR 6.8%で成長すると予想されます。

栄養不足と栄養不良問題に関する農業従事者の意識の高まりが市場を牽引する可能性

- 2022年には、インドと中国がアジア太平洋の微量栄養素肥料市場の支配的参入企業に浮上し、それぞれ市場シェアの41.7%と31.7%を獲得しました。科学環境センター(CSE)は、インドの土壌欠乏症に注目し、ホウ素が47%、鉄が37%、亜鉛が39%と最も顕著であることを明らかにしました。これは、銅とマンガンの欠乏という点ではインドの方が優れているもの、この地域の主要市場となっています。

- 中国政府は肥料の過剰使用の重大性を認識し、"肥料使用増加ゼロのための行動計画"を導入しました。この規制によって、微量栄養素の変種を含む肥料の使用は抑制されました。その結果、特に畑作セグメントでの微量栄養素の成長率は、CAGR 3.8%という小幅なものにとどまりました。

- 研究では一貫して、韓国、マレーシア、台湾などの国々におけるホウ素欠乏の蔓延が強調されてきました。この欠乏は、火山性、酸性、石灰質の土壌で特に顕著で、ピーナッツ、大豆、パパイヤ、柑橘類などの作物に大きな影響を与えています。その結果、ホウ素微量栄養素肥料の市場が急増しています。

- アジア太平洋食品肥料技術センターは、硫酸鉄0.5%、硫酸マンガン0.1%、硫酸銅0.1%などの微量栄養素を葉面散布することで、作物の欠乏症状が効果的に緩和されることを確認しています。

- 食糧安全保障の確保が急務であることから、アジア太平洋における微量栄養素肥料の需要は、2023~2030年の間に6.8%の堅調なCAGRで推移すると予測されています。

アジア太平洋の微量栄養素肥料の市場動向

主要成長作物の栽培が大幅に拡大し、肥料市場の成長が見込まれる

- アジア太平洋では、畑作物が栽培面積全体の95%以上を占めています。米、小麦、トウモロコシがこの地域で生産される主要な畑作作物であり、2022年の総栽培面積の約38%を占めます。耕作面積の増加は、同国における肥料使用の必要性を高めると予想されます。

- 中国、インド、パキスタン、オーストラリアを含むアジア太平洋は、世界最大の小麦生産国のひとつです。中国とインドは、世界最大の小麦生産国であり消費国でもあります。小麦はこの地域の主要な主食のひとつであり、需要と消費の増加を牽引しています。特に、小麦の栽培面積は2018~2022年にかけて63万8,600ha増加しました。2022年、中国は1億3,800万トンの小麦生産を占め、世界最大の小麦生産国となり、インドは1億300万トンの小麦生産を記録しました。

- コメはこの地域で最大の畑作作物です。その栽培面積だけで2022年の全農地面積の約16.44%を占めています。コメはアジアと太平洋のほとんどの地域で主食となっています。中国は2022年に1億4,700万トンの米を生産し、インドは1億2,400万トンの米を収穫すると予測されています。また、インドは1億900万トンを消費する一方、世界最多の1,950万トンを輸出すると予想されました。

- 畑作物に対する国内外の需要の急増は、畑作物専用の耕作面積の拡大を促しています。この耕作地の大幅な増加は、2023~2030年の期間を通じてアジア太平洋の肥料市場に直接的かつプラスの影響を与えると予想されます。

2022年の平均養分施用量は菜種/カノーラが9.2kg/ヘクタールで最も多い

- 高収量作物の養分除去速度が加速しているため、微量栄養素の需要が近年伸びています。微量栄養素の欠乏はアジア太平洋で蔓延しており、この欠乏の影響を受けている主要地域のひとつです。亜鉛、マンガン、銅は、畑作物に主に施用される養分の主要な種類で、2022年にはそれぞれ12kg/ヘクタール、9.1kg/ヘクタール、7.2kg/ヘクタールを占めると推定されます。

- 新興諸国の農業関係者の間では、微量栄養素肥料を使用する利点についての認識が不足しており、これらの肥料の購入に関連するコストが高いことが、この地域における微量栄養素肥料の成長を制限する要因となっています。

- 作物タイプ別では、2022年の平均養分施用量が最も多いのは菜種/カノーラで9.2kg/ヘクタール、次いでトウモロコシ/メイズが6.7kg/ヘクタール、コメが5.4kg/ヘクタールです。特定の微量栄養素の影響は、作物や地域によって異なります。例えば小麦の場合、主要微量栄養素の欠乏は銅とマンガンです。中国、インド、日本などの国々では、小麦ではホウ素とモリブデンが欠乏していることが確認されています。同様に菜種/カノーラでも、主要欠乏は亜鉛、マンガン、銅です。

- 農業従事者が作付けヘクタールあたりからより多くの収穫を得ることを目指しているため、作物生産における微量栄養素の人気は近年急速に高まっています。微量栄養素の欠乏が多く、作物に対する需要が増加しているため、農業従事者は土壌の健全性を高め、作物の生産性を向上させるために微量栄養素を多く採用するようになりました。

アジア太平洋の微量栄養素肥料産業概要

アジア太平洋の微量栄養素肥料市場はセグメント化されており、上位5社で28.85%を占めています。この市場の主要企業は、Chambal Fertilizers & Chemicals Ltd、Coromandel International Ltd.、Indian Farmers Fertiliser Cooperative Limited、Yara International ASA、Zuari Agro Chemicals Ltdなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑設備のある農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品

- ホウ素

- 銅

- 鉄

- マンガン

- モリブデン

- 亜鉛

- その他

- 適用方法

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 生産国

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Chambal Fertilizers & Chemicals Ltd

- Coromandel International Ltd.

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- ICL Group Ltd

- Indian Farmers Fertiliser Cooperative Limited

- Yara International ASA

- Zuari Agro Chemicals Ltd

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Asia-Pacific Micronutrient Fertilizer Market size is estimated at 1.97 billion USD in 2025, and is expected to reach 2.77 billion USD by 2030, growing at a CAGR of 7.06% during the forecast period (2025-2030).

Growing awareness and their importance in the agriculture production may drive the market in the region

- Boron was the most consumed micronutrient in the region, with a consumption volume share of 26.5% in 2022. The majority of boron consumption is attributed to the region's soils, which have reduced water content and higher nitrogen levels that limit boron uptake by plants, leading to increased utilization of boron micronutrients.

- In Asia-Pacific, zinc held the second-largest market share in terms of consumption, with a share of 26.2% and a volume of 159.1 thousand metric tons in 2022. The demand for zinc is anticipated to continue rising in the coming years due to its vital role in the growth and development of plants.

- Copper accounted for 28.6% of the Asia-Pacific micronutrient market's value in the region in 2022. It is an important micronutrient needed in small quantities. It acts as a catalyst in many important plant reactions during growth and plays a key role in protein formation.

- Iron was the third most-consumed micronutrient fertilizer in the region, accounting for a 20.8% share among all micronutrients in 2022. Iron plays an important role in a plant's growth and development as it contains many enzymes and acts as a catalyst in chlorophyll formation. The growing iron deficiency in the soil is expected to fuel the growth of the market.

- Hence, owing to factors like the need for higher yield and productivity and the growing knowledge among farmers about their importance in crop cultivation, the market for micronutrients in the region is anticipated to grow between 2023 and 2030 with a value CAGR of 6.8%.

Nutrient deficiencies and growing awareness among farmers regarding malnutrition problems may drive the market

- In 2022, India and China emerged as the dominant players in the Asia-Pacific micronutrient fertilizer market, capturing 41.7% and 31.7% of the market share, respectively. The Centre for Science and Environment (CSE) highlighted India's soil deficiencies, with boron, iron, and zinc being the most prominent, at 47%, 37%, and 39% respectively. This makes India the leading market in the region, although it fares better in terms of copper and manganese deficiencies.

- Recognizing the gravity of fertilizer overuse, the Chinese government introduced the "Action Plan for the Zero Increase of Fertilizer Use." This regulation has curtailed the usage of fertilizers, including micronutrient variants. Consequently, the growth rate of micronutrients, especially in the field crops segment, has been limited to a modest CAGR of 3.8%.

- Studies have consistently highlighted the prevalence of boron deficiency in countries like Korea, Malaysia, and Taiwan. This deficiency is particularly pronounced in volcanic, acidic, and calcareous soils, significantly impacting crops like peanuts, soybeans, papaya, and citrus. As a result, the market for boron micronutrient fertilizers has witnessed a surge.

- The Food and Fertilizer Technology Centre for the Asian and Pacific Region has observed that applying micronutrients through the foliar mode, such as 0.5% iron sulfate, manganese sulfate, and 0.1% copper sulfate, at the recommended dosages, effectively mitigates crop deficiency symptoms.

- Given the imperative of ensuring food security, the demand for micronutrient fertilizers in Asia-Pacific is projected to register a robust CAGR of 6.8% during 2023-2030.

Asia-Pacific Micronutrient Fertilizer Market Trends

The significant expansion in the cultivation of major growing crops is anticipated to boost the growth of the fertilizers market

- Field crop cultivation dominates the Asia-Pacific region, accounting for more than 95% of the total crop area. Rice, wheat, and corn are the major field crops produced in the region, together accounting for about 38% of the total crop area in 2022. The rising area under cultivation is expected to increase the need for fertilizer usage in the country.

- The Asia-Pacific region, which include China, India, Pakistan, and Australia, is among the world's largest wheat producers. China and India are also the world's largest wheat producers and consumers. Wheat is one of the major staple foods of this region, driving the increase increase in demand and consumption. Notably, the area under wheat cultivation increased by 638.6 thousand ha from 2018 to 2022. In 2022, China accounted for the production of 138 million metric tons of wheat, making it the largest wheat producer in the world, and India recorded wheat production of 103 million metric tons.

- Rice is the largest cultivated field crop in the region. Its cultivation alone accounted for about 16.44% of the total agricultural land in 2022. Rice is the staple food of Asia and most parts of the Pacific region. China was projected to produce 147 million tons of rice, and India was expected to harvest 124 million tons of rice in 2022. India was also expected to consume 109 million tons while exporting a world-leading 19.5 million tons.

- The surge in both domestic and international demand for field crops has prompted an expansion in the cultivation area dedicated to these crops. This significant increase in cultivated land is expected to have a direct and positive impact on the Asia-Pacific fertilizer market throughout the 2023-2030 period.

Rapeseed/canola accounted for the highest average nutrient application rate of 9.2 kg/hectare in 2022

- The demand for micronutrients has grown in recent years due to the accelerated rates of nutrient removal in high-yielding crops. Micronutrient deficiency is widespread in Asia-Pacific, which is one of the major regions affected by this deficiency. Zinc, manganese, and copper are estimated to be the major types of nutrients applied largely for field crops, accounting for 12 kg/hectare, 9.1 kg/hectare, and 7.2 kg/hectare, respectively, in 2022.

- The lack of awareness about the benefits of using micronutrient fertilizers among the farming community in developing countries and the high cost associated with the purchase of these fertilizers are some of the factors limiting the growth of micronutrient fertilizers in the region.

- By crop type, rapeseed/canola accounted for the highest average nutrient application rate of 9.2 kg/hectare in 2022, followed by corn/maize and rice, accounting for 6.7 kg/hectare and 5.4 kg/hectare, respectively. The impact of specific micronutrients differs among crops and across the region. For instance, in the case of wheat, the major micronutrient deficiencies are copper and manganese. In countries like China, India, and Japan, boron and molybdenum are identified as deficient in wheat. Similarly, in rapeseed/canola, the major deficiencies are zinc, manganese, and copper.

- As farmers aim to get more out of every planted hectare, the popularity of micronutrients in the production of crops has increased rapidly in the recent past. High micronutrient deficiency and increasing demand for crops have encouraged farmers to adopt more micronutrients to increase soil health and enhance crop productivity.

Asia-Pacific Micronutrient Fertilizer Industry Overview

The Asia-Pacific Micronutrient Fertilizer Market is fragmented, with the top five companies occupying 28.85%. The major players in this market are Chambal Fertilizers & Chemicals Ltd, Coromandel International Ltd., Indian Farmers Fertiliser Cooperative Limited, Yara International ASA and Zuari Agro Chemicals Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 Bangladesh

- 5.4.3 China

- 5.4.4 India

- 5.4.5 Indonesia

- 5.4.6 Japan

- 5.4.7 Pakistan

- 5.4.8 Philippines

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Chambal Fertilizers & Chemicals Ltd

- 6.4.2 Coromandel International Ltd.

- 6.4.3 Grupa Azoty S.A. (Compo Expert)

- 6.4.4 Haifa Group

- 6.4.5 ICL Group Ltd

- 6.4.6 Indian Farmers Fertiliser Cooperative Limited

- 6.4.7 Yara International ASA

- 6.4.8 Zuari Agro Chemicals Ltd

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms