|

市場調査レポート

商品コード

1693552

中東・アフリカの微量栄養素肥料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Middle East & Africa Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの微量栄養素肥料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 188 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

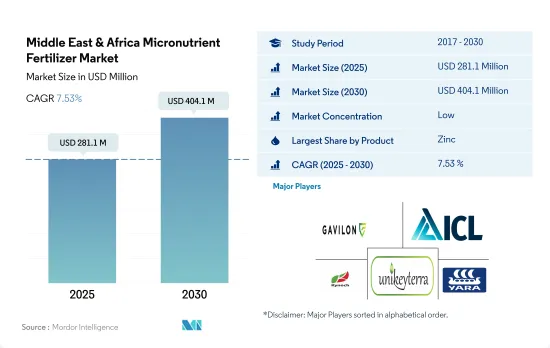

中東・アフリカの微量栄養素肥料の市場規模は2025年に2億8,110万米ドルと推定・予測され、2030年には4億410万米ドルに達し、予測期間(2025~2030年)のCAGRは7.53%で成長すると予測されます。

栄養不足の増加により微量栄養素肥料の需要が拡大

- 同地域の微量栄養素市場は堅調な成長が予測され、2023~2030年のCAGRは7.3%と推定されます。特に、この地域では植物における鉄と亜鉛の欠乏が増加しており、植物の健康を強化するための微量栄養素肥料の需要が高まっている

- 2022年には、亜鉛と鉄が市場を独占し、それぞれ市場金額の31.4%と23.9%を占めました。これらの微量栄養素は植物の成長に不可欠であり、土壌中の欠乏は作物の収量低下に関係しています。過去10年間、土壌中の鉄と亜鉛の欠乏が市場成長の主要促進要因となってきました。

- 微量栄養素の欠乏は、穀物、油糧種子、豆類、野菜のような集約的に栽培される作物で一般的に観察されます。その結果、農業従事者は特に畑作物において、微量栄養素の散布にますます目を向けるようになっており、2022年の微量栄養素市場は、市場金額の71.3%を占めました。

- 土壌における微量栄養素の欠乏が深刻化していることが、収量減少の主要因となっています。特にアフリカの土壌では、硫黄、亜鉛、ホウ素、銅などの二次栄養素や微量栄養素の欠乏が見られます。肥料によってこれらの栄養素不足のバランスをとることは、収量を向上させるだけでなく、土壌の健康を維持することにもなり、今後数年間の市場の極めて重要な促進要因になります。

- その結果、微量栄養素肥料の市場規模は、2023~2030年の間にCAGRが3.8%と予測され、着実な成長が見込まれます。

人口の増加と食糧不安に対する懸念の高まりが微量栄養素肥料市場を促進する

- 中東・アフリカの微量栄養素肥料市場は、中東・アフリカの肥料市場全体の約5.1%を占め、2022年の市場規模は約4億8,260万米ドルでした。水不足と気温の上昇にもかかわらず、この地域の多くの国は農業に依存しています。ナイジェリア、サウジアラビア、エジプトは、この地域の主要な農業生産国のひとつです。

- ナイジェリアはこの地域最大の農業生産国です。ナイジェリアの農地面積は6,860万ヘクタールで、トウモロコシ、キャッサバ、ギニアコーン、ヤムイモ、キビ、コメが2022年の主要作物です。ナイジェリアは2022年のアフリカの微量栄養素肥料市場の12.6%を占めます。

- この地域では葉面施肥法が微量栄養素施肥法として最も利用されており、2022年の市場金額の約43.6%を占めます。

- その他の中東・アフリカは、この地域における微量栄養素肥料の最大市場の一つです。その他の中東・アフリカは、この地域の微量栄養素肥料市場全体の約52.7%を占め、2022年の市場規模は約1億4,820万米ドルです。その他の中東・アフリカの主要農業生産者はエジプト、アルジェリア、モロッコ、イラクです。

- 特にトルコ、ナイジェリア、サウジアラビアなどの国々では、亜鉛欠乏が深刻な問題となっています。亜鉛だけで微量栄養素肥料市場全体の約46.2%を占め、2022年には約2億2,310万米ドルとなりました。

- 農業地域全体における微量栄養素の不足が、この地域の微量栄養素肥料市場を牽引しています。

中東・アフリカの微量栄養素肥料の市場動向

浸食による天水地と灌漑地の両方の劣化は、作物栽培の課題となっています。

- 中東・アフリカでは、トウモロコシ、コメ、ソルガム、大豆などの畑作物は通常4月から5月にかけて作付けされ、収穫は9月から10月にかけて行われます。しかし、この地域の農業セクタは大きな課題に直面しています。土地と水資源は乏しく、天水灌漑地は風や水による浸食で荒廃しており、持続不可能な農法がそれを悪化させています。畑作が農業の大半を占め、この地域の農地全体の90%を占めています。2022年、この地域の畑作物栽培面積は2億4,900万ヘクタールに達し、2017年から3.9%増加しました。トウモロコシだけがかなりのシェアを占め、畑作物総面積の17.8%を占めます。小麦栽培も顕著な増加を見せ、2017~2022年の間に4.6%増加しました。具体的には、この地域のトウモロコシ栽培面積は2022年に4,430万ヘクタールに達します。

- アフリカでは、ナイジェリアが最大のソルガム生産者としてトップに立ち、エチオピアが僅差でこれに続きます。ソルガムきびは主要な穀物作物として際立っており、ナイジェリアにおける穀物生産高全体の50%に貢献し、穀物作付面積の約45%を占めています。ソルガムきびは干ばつや湛水に強く、多様な土壌条件に適応することから、中東・アフリカの乾燥地帯で好まれる主食作物として位置づけられ、食料と所得の安定を確保しています。

- 過去10年間で、この地域の人口は23%以上増加しています。生産能力が限られているにもかかわらず、予測では食料輸入の増加を示しています。しかし、農業は堅調を維持し、耕作地は拡大しています。

マンガンを多く含む酸性土壌は、湿潤な環境条件下では鉄欠乏症を引き起こします。

- 植物の栄養は、成長に不可欠な微量栄養素に依存しています。微量栄養素が不足すると、植物の成長が妨げられ、収量が減少します。ホウ素、銅、マンガン、亜鉛、コバルトのような微量元素を含む微量栄養素肥料は、それぞれ様々なレベルで植物にとって極めて重要です。2022年、この地域の畑作物はマンガン、銅、亜鉛の需要が大きく、消費量はそれぞれ10.8kg/ヘクタール、7.14kg/ヘクタール、6.73kg/ヘクタールです。

- 2022年、アフリカの畑作物の総栽培面積は2億2,830万ヘクタールでした。注目すべきは、大豆、菜種、綿花、ソルガムなどの作物の平均養分施用量が最も多く、4.44kg/ヘクタールから4.34kg/ヘクタールであったことです。商業農業が盛んなことで知られる南アフリカは、農業において微量栄養素に大きく依存しています。土壌分析が一般的で、その後、微量栄養素を肥料に混ぜたり、葉面散布したりするなどの是正措置がとられます。

- 特に大豆は、2022年の平均養分消費率が最も高く、マンガンを12.15kg/ヘクタール、銅を7.2kg/ヘクタール利用しています。葉面散布によって、この地域は小麦や他の畑作物に影響を与えるマンガンの欠乏にも対処しています。この地域の湿潤な環境に多い酸性土壌は、しばしば鉄欠乏を引き起こし、葉面散布や鉄キレート剤の散布によって改善されます。こうした課題に取り組むため、葉面散布による微量栄養素の散布が増加しており、この傾向は2023~2030年の期間も続くと予想されます。

中東・アフリカの微量栄養素肥料産業の概要

中東・アフリカの微量栄養素肥料市場はセグメント化されており、上位5社で30.27%を占めています。この市場の主要企業は、Gavilon South Africa(MacroSource、LLC)、ICL Group Ltd、Kynoch Fertilizer、Unikeyterra Chemical、Yara International ASAなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑設備のある農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品

- ホウ素

- 銅

- 鉄

- マンガン

- モリブデン

- 亜鉛

- その他

- 適用方法

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 生産国

- ナイジェリア

- サウジアラビア

- 南アフリカ

- トルコ

- その他の中東・アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Azra Group AS

- Gavilon South Africa(MacroSource, LLC)

- ICL Group Ltd

- Kynoch Fertilizer

- Unikeyterra Chemical

- Yara International ASA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Middle East & Africa Micronutrient Fertilizer Market size is estimated at 281.1 million USD in 2025, and is expected to reach 404.1 million USD by 2030, growing at a CAGR of 7.53% during the forecast period (2025-2030).

Demand for micronutrient fertilizers is growing due to increasing nutrient deficiency

- The micronutrient market in the region is projected to witness robust growth, with an estimated CAGR of 7.3% between 2023 and 2030. Notably, deficiencies of iron and zinc in plants are on the rise in the region, amplifying the demand for micronutrient fertilizers to bolster plant health.

- In 2022, zinc and iron dominated the market, accounting for 31.4% and 23.9% of the market value, respectively. These micronutrients are crucial for plant growth, and their deficiencies in soil have been linked to lower crop yields. Over the past decade, iron and zinc deficiencies in soils have been the primary drivers of the growth of the market.

- Micronutrient deficiencies are commonly observed in intensively cultivated crops like cereals, oilseeds, pulses, and vegetables. Consequently, farmers are increasingly turning to micronutrient applications, especially in field crops, which dominated the micronutrient market in 2022, capturing 71.3% of the market value.

- The escalating micronutrient deficiency in soils is a key factor contributing to yield declines. African soils, in particular, exhibit deficiencies in secondary and micronutrients, including sulfur, zinc, boron, and copper. Balancing these nutrient deficiencies through fertilizers not only enhances yields but also sustains soil health, making it a pivotal driver for the market in the coming years.

- As a result, the micronutrient fertilizer market volume is anticipated to witness steady growth, with a projected CAGR of 3.8% during the period of 2023-2030.

The growing population and increasing concerns regarding food insecurity propel the micronutrient fertilizer market

- The Middle East & African micronutrient fertilizer market accounted for about 5.1% of the overall Middle East & African fertilizer market, valued at about USD 482.6 million in 2022. Despite water scarcity and higher temperatures, many countries in the region depend on agriculture. Nigeria, Saudi Arabia, and Egypt are some of the major agricultural producers in the region.

- Nigeria is the largest agricultural producer in the region. Nigeria has 68.6 million hectares of agricultural land area, with maize, cassava, guinea corn, yam beans, millet, and rice being the major crops in 2022. Nigeria accounted for 12.6% of the African micronutrient fertilizer market in 2022.

- The foliar method of fertilizer application is the most used method for micronutrient application in the region, accounting for about 43.6% of the market value in 2022.

- The Rest of Middle East & Africa is one of the largest markets for micronutrient fertilizers in the region. The Rest of Middle East & Africa accounted for about 52.7% of the total micronutrient fertilizer market in the region, valued at about USD 148.2 million in 2022. The major agricultural producers in the Rest of Middle East & Africa are Egypt, Algeria, Morocco, and Iraq.

- Among micronutrient fertilizers, zinc is the most applied micronutrient, as zinc deficiency is a severe problem in the region, particularly in countries like Turkey, Nigeria, and Saudi Arabia. Zinc alone accounted for about 46.2% of the total micronutrient fertilizer market, valued at about USD 223.1 million in 2022.

- The deficiency of micronutrients in the overall agricultural area drives the micronutrient fertilizer market in the region.

Middle East & Africa Micronutrient Fertilizer Market Trends

Deterioration of both rain-fed and irrigated lands due to erosion pose a challenge in crop cultivation.

- In the Middle East & Africa, field crops such as corn, rice, sorghum, and soybeans are typically planted between April and May, with harvests taking place in September and October. However, the agricultural sector in this region faces significant challenges. Land and water resources are scarce and rain-fed and irrigated lands are deteriorating due to erosion from wind and water, which is exacerbated by unsustainable farming practices. Field crops dominate the agricultural landscape, occupying 90% of the total agricultural land in the region. In 2022, the region's field crop cultivation area reached 249 million hectares, marking a 3.9% increase from 2017. Corn alone commands a substantial share, accounting for 17.8% of the total field crop area. Wheat cultivation also saw a notable rise, with a 4.6% increase between 2017 and 2022. Specifically, the region's corn cultivation area reached 44.3 million hectares in 2022.

- In Africa, Nigeria takes the lead as the largest sorghum producer, closely followed by Ethiopia. Sorghum stands out as the primary cereal crop, contributing to 50% of the total cereal output in Nigeria and occupying approximately 45% of the cereal cropland. Sorghum's resilience to drought and waterlogging, coupled with its adaptability to diverse soil conditions, positions it as the preferred staple crop in the drier regions of the Middle East & Africa, ensuring both food and income security.

- Over the past decade, the region has witnessed a population growth of over 23%. Despite limited production capacity, the forecast indicates a rise in food imports. However, the agricultural industry has remained robust, with an expanding footprint in terms of cultivated land.

The acidic soils with high manganese content, under moist environmental conditions, results in iron deficiency

- Plant nutrition relies on micronutrients, which are essential for growth. Insufficient micronutrients can hinder plant growth and reduce yields. Micronutrient fertilizers containing trace elements like boron, copper, manganese, zinc, and cobalt are crucial for plants, each at varying levels. In 2022, field crops in the region had a significant demand for manganese, copper, and zinc, with consumption rates of 10.8 kg/hectare, 7.14 kg/hectare, and 6.73 kg/hectare, respectively.

- In 2022, Africa had a total field crop cultivation area of 228.3 million hectares. Notably, crops like soybean, rapeseed, cotton, and sorghum had the highest average nutrient application rates, ranging from 4.44 kg/hectare to 4.34 kg/hectare. South Africa, known for its prominent commercial farming sector, heavily relies on micronutrients in agriculture. Soil analysis is a common practice, followed by corrective measures like incorporating micronutrients into fertilizers or using foliar applications.

- Soybean, in particular, stood out in 2022 with the highest average nutrient consumption rates, utilizing 12.15 kg/hectare of manganese and 7.2 kg/hectare of copper. Through foliar applications, the region also addresses manganese deficiencies, which impact wheat and other field crops. The acidic soils, prevalent in the region's moist environment, often lead to iron deficiencies, remedied by foliar sprays or iron chelate applications. To tackle these challenges, micronutrients are increasingly being applied via foliar sprays, a trend expected to continue during the 2023-2030 period.

Middle East & Africa Micronutrient Fertilizer Industry Overview

The Middle East & Africa Micronutrient Fertilizer Market is fragmented, with the top five companies occupying 30.27%. The major players in this market are Gavilon South Africa (MacroSource, LLC), ICL Group Ltd, Kynoch Fertilizer, Unikeyterra Chemical and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product

- 5.1.1 Boron

- 5.1.2 Copper

- 5.1.3 Iron

- 5.1.4 Manganese

- 5.1.5 Molybdenum

- 5.1.6 Zinc

- 5.1.7 Others

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Nigeria

- 5.4.2 Saudi Arabia

- 5.4.3 South Africa

- 5.4.4 Turkey

- 5.4.5 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Azra Group AS

- 6.4.2 Gavilon South Africa (MacroSource, LLC)

- 6.4.3 ICL Group Ltd

- 6.4.4 Kynoch Fertilizer

- 6.4.5 Unikeyterra Chemical

- 6.4.6 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms