北米の食用肉:市場シェア分析、産業動向&統計、成長予測(2025年~2030年)

North America Edible Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 260 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692084

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

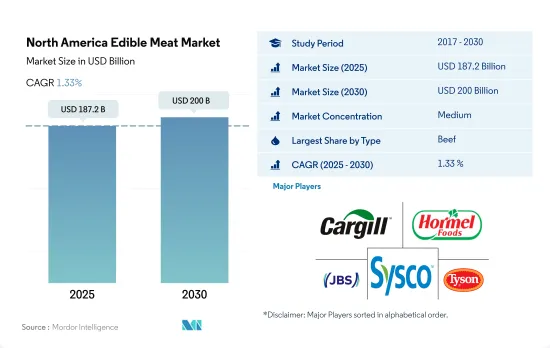

北米の食用肉市場規模は2025年に1,872億米ドルと予測され、2030年には2,000億米ドルに達し、予測期間中(2025年~2030年)のCAGRは1.33%で成長すると予測されています。

鶏肉の費用対効果が顧客を惹きつけている

- 北米の食用肉市場を牽引しているのは牛肉であり、2022年の金額ベースの成長率は最も高く、予測期間中のCAGRは1.37%と予想されます。同国では牛肉の需要が極めて高く、2022年には前年比4.6%増の約201億米ドル相当の牛肉が小売市場で販売されました。ランチョンミート、ソーセージ、ホットドッグ、ハム・ベーコン、ビーフジャーキーは、米国で最も消費されている牛肉加工品です。

- 羊と子羊の生産量の減少は、価格の上昇を伴っており、これが生産コスト増の原因となっています。2022年の生産価格は、この地域の他のどの食肉よりも15~20%高いです。供給不足と価格高騰が羊肉と羊羊肉の消費を減少させ、その成長を妨げています。

- 鶏肉は2022年に北米地域で2番目のシェアを占め、予測期間中に金額ベースで1.15%のCAGRで推移すると予測されます。米国は、2022年時点で5億1,300万羽を超える家禽と2億1,600万羽を超える七面鳥を擁する大規模な家禽産業を有しています。

- 2022年には合計91億7,000万羽のブロイラーが生産され、2021年からわずかに増加しました。全体として、2022年の生体重ブロイラーの生産量は589億ポンドに達し、2021年からわずかに増加しました。2022年に生産された七面鳥は71億米ドルで、前年の58億9,000万米ドルから21%増加しました。鶏肉は他の食肉に比べ手ごろな価格であるため、消費者、特に費用対効果の高い蛋白源を求める人々にとって魅力的な選択肢となっています。Cargill, Incorporated、Hormel Foods Corporation、Sysco Corporation、Tyson Foods Inc.

先端技術が牛肉販売を牽引

- 米国は、2019年から2022年にかけて販売額が約14.81%増加したことから、レビュー期間中、食用肉の主要市場シェアを占めました。この増加は主に米国における牛肉消費の増加によるものです。牛肉は2022年の市場シェアの約68.86%を他の肉類と比較して占めました。2022年の牛肉消費量は59.1ポンドと推定され、過去10年間で最高となりました。さらに、牛肉業界ではデータ分析とブロックチェーン技術の活用も進んでおり、センサーを利用してトレーサビリティ、透明性、食品の安全性を高めています。

- メキシコは、2022年の食用肉市場で2番目の主要シェアを占めました。過去数年間、米国からメキシコへの輸出が着実に増加していることから、予測期間中のCAGRは1.57%を記録すると予測されています。この輸出増加は、北米自由貿易協定(NAFTA)とメキシコの食肉消費拡大が後押ししています。メキシコは、米国産豚肉と鶏肉の輸出量では最大の市場であり、米国産牛肉の輸出量では第2位の市場です。メキシコで豚肉の輸入と生産が増加するにつれ、人々は牛肉よりも安価な豚肉を好むようになりました。

- カナダは比較的成長率が鈍く、予測期間中のCAGRは1.04%(金額ベース)です。豚肉の生産は、ソーセージや各種チルド肉など、カナダの食肉製品の約70%を占めています。カナダの食肉加工施設は、生肉、冷凍肉、牛肉調製品、燻製肉、生肉、調理肉、ソーセージ、あらゆる冷食肉など、多種多様な食肉製品に関わっています。

北米の食用肉市場の動向

需要の増加と輸入の減少が生産を押し上げる

- 牛肉市場は、歴史的な期間中、生産コストの上昇によって大きな影響を受けました。生産コストの上昇は主に乾燥条件によるものです。しかし、2022年の同地域の牛肉生産量は2021年に比べ1.25%増加しました。過去数年間の北米西部の干ばつは、この地域の生産に悪影響を与えました。家畜に十分な餌を確保することが困難なため、カナダ西部からメキシコ北部の州まで、家畜を飼育する農家は損失を被っています。家畜に与える飼料を北米の他の地域から購入している農家もあります。

- カナダは米国に次いで北米第2位の牛肉生産国です。2022年の生産シェアはカナダが5.46%、米国が50.15%です。牛群の減少にもかかわらず、生牛の輸入はカナダの食肉生産にプラスの影響を与えます。2022年には、水分レベルが牛の取引を監視する上で極めて重要な要素になると思われます。カナダで干ばつが収まっても米国で干ばつが続けば、より多くの牛が北へ移動するかもしれないです。

- カナダと米国における牛群の減少と子牛の収量の減少により、北米の牛肉供給は長期的に逼迫しています。2022年1月1日、カナダでは肉牛在庫は5年連続で1%減の350万頭となりました。カナダでは農場の61%が47頭未満で、肉牛は59万6,419頭と牛群の16%を占めています。2023年1月1日現在の米国の全牛と子牛の合計は8,930万頭で、2022年1月1日の9,210万頭を3%下回りました。米国は世界最大の肥育牛産業であることに加え、世界最大の牛肉消費国でもあります。

小売需要の増加が牛肉卸売のニーズを押し上げ、市場成長を牽引

- 近年、小売需要の高まりが牛肉卸売のニーズを押し上げ、牛肉価格の上昇につながりました。2021年以降、牛肉小売価格はほぼ安定しており、月次価格の12ヵ月移動平均は2022年4月以降、ポンド当たり7.25米ドルを超えています。2022年の牛肉生産量が過去最高を記録し、国民1人当たりの牛肉消費量が58.9ポンドと2010年以来最大であることを考えると、これは牛肉需要が旺盛であることを示唆しています。2022年の全生鮮牛肉の小売価格は平均でポンド当たり7.30米ドルとなり、これは過去最高価格であり、2021年の価格を5.1%上回りました。テンダーロインとリブロースは前年比12%から15%上昇し、中間肉の価格が引き続き卸売価格を支配しています。

- 小売価格と同様、牛肉卸売価格も2022年の大半は小さなレンジ内で変動しています。3月以降、チョイス牛肉箱詰めの平均価格は261.77米ドル/重量で、週の最高値は272.48米ドル/重量、最低値は246.31米ドル/重量で、幅は26.17米ドル/重量です。非常に旺盛な卸売需要を受け、2021年のチョイスビーフ箱詰め価格は平均279.81米ドル/重量で、週ごとの最高値は347.02米ドル/重量、最低値は206.73米ドル/重量、年間レンジは140.29米ドル/重量でした。

- しかし、加工工場はパンデミック中も2021年も続く労働力不足に苦しみ、流行前と同じペースで食肉を加工する能力が制限されました。このような生産量の減少は、消費者やレストランからの牛肉需要の増加によるもので、そのため価格が上昇しました。地域の労働力不足は2021年も続き、2021年9月の労働力率は61.6%と、2020年1月の63.4%から低下しました。

北米の食用肉産業の概要

北米の食用肉市場は適度に統合されており、上位5社で47.08%を占めています。この市場の主要企業は以下の通り。 Cargill Inc., Hormel Foods Corporation, JBS SA, Sysco Corporation and Tyson Foods Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 牛肉

- マトン

- 豚肉

- 家禽類

- 生産動向

- 牛肉

- 羊肉

- 豚肉

- 家禽類

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タイプ

- 牛肉

- マトン

- 豚肉

- 家禽類

- その他の食肉

- 形態

- 缶詰

- 生鮮・冷蔵

- 冷凍

- 加工

- 流通チャネル

- オフ・トレード

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- オフ・トレード

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米

第5章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Cargill Inc.

- Continental Grain Company

- Foster Farms Inc.

- Hormel Foods Corporation

- JBS SA

- Marfrig Global Foods S.A.

- NH Foods Ltd

- OSI Group

- Perdue Farms Inc.

- Sysco Corporation

- The Clemens Family Corporation

- The Kraft Heinz Company

- Tyson Foods Inc.

- Vion Group

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 90392

The North America Edible Meat Market size is estimated at 187.2 billion USD in 2025, and is expected to reach 200 billion USD by 2030, growing at a CAGR of 1.33% during the forecast period (2025-2030).

Cost-effectiveness of poultry meat is attracting customers

- The North American edible meat market is driven by beef, which had the highest growth rate by value in 2022, and it is expected to register a CAGR of 1.37% over the forecast period. In the country, demand for beef is extremely high, and in 2022, around USD 20.1 billion worth of beef was sold at retail markets, up 4.6% Y-o-Y. Luncheon meat, sausages, hot dogs, hams and bacon, and beef jerky are the most popular processed beef products consumed in the United States.

- The decrease in sheep and lamb production has been accompanied by higher prices, which have been responsible for the greater production costs. Production is priced 15-20% higher than any other meat in the region in 2022. Shortages in supply and high prices diminished the consumption of sheep and lamb and prevented their growth.

- Poultry meat held the second major share in the North American region in 2022 and is anticipated to register a CAGR of 1.15% by value during the forecast period. The United States has an extensive poultry industry, with more than 513 million poultry and over 216 million turkeys as of 2022.

- In total, 9.17 billion broilers were produced in 2022, up slightly from 2021. Overall, the production of live-weight broilers in 2022 amounted to 58.9 billion pounds, up from 2021, a slight increase. Turkeys produced in 2022 were valued at USD 7.10 billion, up 21% from the previous year's figure of USD 5.89 billion. The affordability of chicken compared to other meat types makes it an attractive option for consumers, especially those who are looking for cost-effective protein sources. Cargill, Incorporated, Hormel Foods Corporation, Sysco Corporation, Tyson Foods Inc., and WH Group Limited are among the major players operating in the poultry market in the United States.

Advanced technologies are driving the sales of beef

- The United States held the major market share of edible meat during the review period, as the sales value increased by about 14.81% from 2019 to 2022. This increase was majorly due to the increased beef consumption in the United States. Beef accounted for about 68.86% of the market share in 2022 compared to other meat types. In 2022, beef consumption was estimated at 59.1 pounds, the highest since the last decade. Moreover, the beef industry is also increasingly utilizing data analytics and blockchain technology, using sensors to enhance traceability, transparency, and food safety.

- Mexico held the second major share in the edible meat market in 2022. It is projected to record a CAGR of 1.57% during the forecast period due to the steadily growing US exports to Mexico over the past few years. This increase in exports is boosted by the North American Free Trade Agreement (NAFTA) and Mexico's growing meat consumption. Mexico has the largest market, by volume, for US pork and poultry and the second-largest market for US beef exports. As pork imports and production increased in Mexico, people began preferring less expensive pork over beef.

- Canada is experiencing a comparatively slower growth rate, registering a CAGR of 1.04% by value during the forecast period owing to the slow population growth. The production of pork accounts for about 70% of Canadian meat products, e.g., sausages and various types of chilled meat. Canada's meat processing facilities are involved in a large variety of meat products, which include fresh and frozen meat, beef preparations, smoked, cured, or prepared meats, sausages, and any cold meat.

North America Edible Meat Market Trends

Growing demand and reduced imports are boosting production

- The beef market was highly impacted by increased production costs during the historical period. The rise in production cost was primarily because of the dry conditions. However, beef production in the region was up by 1.25% in 2022 compared to 2021. Drought in locations throughout western North America during the past few years negatively impacted the region's production. Due to difficulty in locating enough food for their animals, farmers who rear cattle are losing money in regions ranging from western Canada to the states of northern Mexico. Some farmers buy feed for their livestock from other parts of North America.

- Canada is the second-largest beef producer in North America after the United States. The production share of Canada and the United States in 2022 was 5.46% and 50.15%, respectively. Despite a dwindling cow herd, live cattle imports positively affect Canadian meat production. In 2022, moisture levels were likely to be a crucial aspect in monitoring the trading of cattle. More cattle may be moved north if the drought subsides in Canada but continues in the United States.

- The declining cow herd and a smaller calf yield in Canada and the United States are resulting in long-term and tighter beef supplies in North America. On January 1, 2022, in Canada, beef cow inventories were down by 1% for the fifth consecutive year to 3.5 million heads. In Canada, 61% of farms have less than 47 cows, with 596,419 beef cows, 16% of the herd. All cattle and calves in the United States as of January 1, 2023, totaled 89.3 million heads, 3% below the 92.1 million heads on January 1, 2022. In addition to having the world's largest-fed cattle industry, the United States is also the world's largest consumer of beef, primarily high-value, grain-fed beef.

Rising retail demand boosted the need for wholesale beef and drove market growth

- The rising retail demand has boosted the need for wholesale beef in recent years, which led to higher beef prices. Since 2021, retail beef prices have been largely stable, and the 12-month moving average of monthly prices has exceeded USD 7.25 USD per pound since April 2022. Given the record beef production in 2022 and the greatest per-capita beef consumption since 2010, at 58.9 pounds, this suggests a strong beef demand. Retail prices for all fresh beef averaged USD 7.30 per pound in 2022, which was a record-high price and an increase of 5.1% above prices in 2021. Tenderloins and ribeyes are up 12% to 15% Y-o-Y, and middle meat prices continue to dominate wholesale prices.

- Like retail prices, wholesale boxed beef prices have fluctuated within a small range for most of 2022. Since March, Choice boxed beef has had an average price of USD 261.77/cwt, with a weekly high and minimum of 272.48/cwt and USD 246.31/cwt, respectively, for a range of USD 26.17/cwt. Following very strong wholesale demand, Choice boxed beef prices averaged USD 279.81/cwt in 2021, with weekly maximums of USD 347.02/cwt, weekly minimums of USD 206.73/cwt, and annual ranges of USD 140.29/cwt.

- However, processing plants struggled with labor shortages that continued during the pandemic and in 2021, limiting their ability to process meat at the same rate as before the outbreak. This decline in production was due to the increasing demand for beef from consumers and restaurants, thus boosting the prices. The regional labor shortage continued in 2021, with a labor force participation rate of 61.6% in September 2021, down from 63.4% in January 2020.

North America Edible Meat Industry Overview

The North America Edible Meat Market is moderately consolidated, with the top five companies occupying 47.08%. The major players in this market are Cargill Inc., Hormel Foods Corporation, JBS SA, Sysco Corporation and Tyson Foods Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Beef

- 3.1.2 Mutton

- 3.1.3 Pork

- 3.1.4 Poultry

- 3.2 Production Trends

- 3.2.1 Beef

- 3.2.2 Mutton

- 3.2.3 Pork

- 3.2.4 Poultry

- 3.3 Regulatory Framework

- 3.3.1 Canada

- 3.3.2 Mexico

- 3.3.3 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Beef

- 4.1.2 Mutton

- 4.1.3 Pork

- 4.1.4 Poultry

- 4.1.5 Other Meat

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 Canada

- 4.4.2 Mexico

- 4.4.3 United States

- 4.4.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Cargill Inc.

- 5.4.2 Continental Grain Company

- 5.4.3 Foster Farms Inc.

- 5.4.4 Hormel Foods Corporation

- 5.4.5 JBS SA

- 5.4.6 Marfrig Global Foods S.A.

- 5.4.7 NH Foods Ltd

- 5.4.8 OSI Group

- 5.4.9 Perdue Farms Inc.

- 5.4.10 Sysco Corporation

- 5.4.11 The Clemens Family Corporation

- 5.4.12 The Kraft Heinz Company

- 5.4.13 Tyson Foods Inc.

- 5.4.14 Vion Group

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

北米の食用肉:市場シェア分析、産業動向&統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 260 Pages

- 納期

- 2~3営業日