欧州の食用肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Edible Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 266 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690976

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

欧州の食用肉の市場規模は2025年に1,930億米ドルと推定され、2030年には2,011億米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは0.83%で成長する見込みです。

調理済み食肉需要の高まりが市場を後押し

- 豚肉は欧州で消費される主要な食肉であり、2022年の豚肉売上は前年比1.57%増加しました。2021年、欧州の豚肉市場は生産量の増加に関連した大きな動向を経験しました。生産拡大を続けるEU市場のリーダーはスペイン、デンマーク、オランダです。2022年の欧州の豚肉供給量は需要を大幅に上回りました。その結果、豚肉消費量は欧州全域、特に南部で増加しました。しかし、枝肉価格の低下と中央欧州におけるアフリカ豚熱(ASF)の追加発生の脅威が、今後の市場の成長を妨げる可能性があります。

- 牛肉消費は主に、欧州全域における調理済み食肉製品の需要によって牽引されています。欧州では、サンドイッチ、ビーフスティック、ベーコン、ビーフジャーキー、豚皮のような簡便食品に対する需要の増加により、牛肉加工品の需要が高まっています。牛肉加工品は予測期間中にCAGR値1.68%を記録すると予測されています。BRF SA、Cargill Inc.、Danish Crown Amba、Tyson Foods Inc.が欧州で加工牛肉を提供する主要企業です。

- マトンはこの地域で最も急成長している食肉セグメントであり、予測期間中のCAGR値は0.91%を記録すると予測されています。欧州連合には7,000万頭以上の羊と山羊がいる(羊85%、山羊15%)。ギリシャ、スペイン、フランス、ルーマニアは欧州の主要な羊肉生産地です。この地域で消費される羊肉の約20%は輸入されています。ニュージーランドは、他の欧州諸国が必要とする羊肉の約89%を供給しています。欧州では、ラム(生後1年未満の羊の肉)の方が通常のマトン(生後3年未満の羊の肉)よりも人気があります。

鶏肉と豚肉の消費が市場を牽引

- 欧州の食用肉売上高は長年安定した成長を遂げており、2018年から2022年にかけて8.97%増加しています。ロシア、フランス、ドイツが消費動向を支配しています。2022年の同地域の家畜頭数でも、ロシア(1,856万頭)が動向をリードし、フランス(1,778万頭)、ドイツ(1,130万頭)、スペイン(663万頭)が続きます。豚肉は欧州で最も消費されている肉類です。

- 欧州では、イタリアが食用肉市場で最も急成長しています。予測期間中、金額ベースでCAGR 1.20%を記録すると予測されています。この増加は主にイタリアにおける豚肉消費の増加によるものです。イタリアは2022年の豚肉市場シェアにおいて、他の肉類と比較して金額ベースで約41.96%を占めました。イタリアで飼育されている豚の70%以上は北部で飼育されているが、農場の規模が小さいため、中南部の農場の74%がこの産業に従事しています。また、豚肉業界では、トレーサビリティ、透明性、食品の安全性を高めるため、センサーを活用したデータ分析とブロックチェーン技術の活用が進んでいます。

- 欧州の食用肉市場は、予測期間中に0.32%のCAGRで推移すると予測されています。この低い進行は、欧州諸国における食肉消費の減少に起因しています。欧州人の46%近くが、2022年には前年よりも肉を食べる量が減ったと報告しています。しかし、他の国の中には、その食文化が原因でこの動向にまだ追いついていない国もあります。植物性の肉には十分な風味と栄養がないと考える文化もあります。彼らは肉を適切な食事であり、栄養源であると考えています。また、植物性食品は高価すぎる、調理が難しい、見た目に魅力がない、と考える人もいます。

欧州の食用肉市場の動向

ロシア・ウクライナ紛争にもかかわらず、ロシアは依然としてこの地域の主要な牛肉生産国です。

- 2022年の欧州の牛肉生産量は、価格低下と牛群減少により前年比0.98%減少しました。欧州で生産される牛肉の約40%はロシア、フランス、ドイツが占めています。欧州委員会は、EU加盟国または地域の牛肉の平均市場価格が一定期間にわたって1トン当たり2,416米ドルを下回った場合、公的介入を用いて牛肉価格を下支えする計画を持っています。欧州委員会は、平均価格の下落や生産コストの大幅な変動があった場合、また、業界にとって不利なマージンの大幅な変動を引き起こすもうひとつの要因である、民間の貯蔵支援に補助金を提供することができます。EUはまた、牛肉業界の生産者団体に対する特定の免除措置を通じて、牛肉農家を支援しています。

- ロシアは2022年に15.96%のシェアを占め、この地域の主要な牛肉生産国となりました。この成長は、国家による牛肉産業支援のための例外的な措置によって促進されました。その措置には、畜産業者への生産コストの払い戻し、若い家畜の購入、施設の技術的近代化、畜産分野での業務改善などがあります。生産者には、飼料、設備、動物用医薬品の購入、畜産施設の建設と近代化のための融資が提供されます。

- オランダの2022年の生産量は最低の42万9,640トンでした。オランダの全国肉牛頭数は、EUの牧草地リン酸塩制限の超過により、過去3年間常に減少しています。2022年の肉牛頭数は8.4%減の369万頭でした。政府は畜産の減少を通じて排出量を削減しようとしているが、これは国内の肉牛産業に悪影響を及ぼします。

飼料コストの上昇と変種牛のと畜頭数の減少が地域の牛肉価格変動につながっている

- 2019年から2022年にかけて、牛肉価格は低水準で推移する一方、サプライチェーンの混乱により牛肉卸売価格が上昇したため、牛肉価格は5.34%上昇しました。牛肉の全サービス販売は、プレミアムカットであっても外食販売の増加により回復し、総消費量の3%増につながりました。2021年には、末端肉用牛として飼育される哺乳牛が24万5,000頭(2.3%減)減少し、牛肉価格の上昇につながりました。不十分な施設、衛生対策、食肉処理場での家畜の不適切な取り扱いが、牛肉の微生物汚染をさらに悪化させ、食中毒病原体の人へのトランスミッションにつながる可能性があります。

- 飼料費の高騰も、2022年第1四半期の牛肉価格の26%上昇に寄与しました。投入コスト、特に飼料の高騰は、主に集約型畜産農家で、飼料コストが農場の収益性に大きな影響を与えるため、屠殺頭数の増加や枝肉重量の低下を招く可能性があります。食糧および食肉価格の上昇により、この地域の牛肉消費量は2022年には1人当たり10.3 kgに減少する(0.3%減)。この動向は2022年も続き、全体ではマイナス0.9%に達する可能性が高いです。

- 欧州では2021年から2023年にかけて非常に高い食品価格インフレが発生したため、食肉に対する消費者の需要は、個人の健康と環境に対する意識の高まりと相まって、一貫して減少しています。価格の高騰と需要の減少により、欧州の多くの国で牛肉生産が減少しました。例えば、2022年にはイタリアで20%の生産減が見られ、スペインとドイツはそれぞれ6%と1%の減少を報告しました。フランスは1%の生産増を記録し、オランダは9%の牛肉生産増を記録しました。

欧州食用肉産業の概要

欧州食用肉市場は細分化されており、上位5社で10.15%を占めています。この市場の主要企業は以下の通りです。Cargill Inc., Danish Crown AmbA, Tyson Foods Inc., Vion Group and WH Group Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 牛肉

- 羊肉

- 豚肉

- 家禽類

- 生産動向

- 牛肉

- 羊肉

- 豚肉

- 家禽類

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タイプ

- 牛肉

- 羊肉

- 豚肉

- 家禽類

- その他の肉

- 形態

- 缶詰

- 生鮮・冷蔵

- 冷凍

- 加工

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンラインチャネル

- スーパーマーケットとハイパーマーケット

- その他

- オントレード

- オフトレード

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- 英国

- その他欧州

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BRF S.A.

- Cargill Inc.

- Danish Crown AmbA

- Dawn Meats

- Gruppa Cherkizovo, PAO

- Heck!Food Ltd

- Hormel Foods Corporation

- JBS SA

- Mitsubishi Corporation

- NH Foods Ltd

- Nomad Foods Limited

- Tyson Foods Inc.

- Vion Group

- WH Group Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 90079

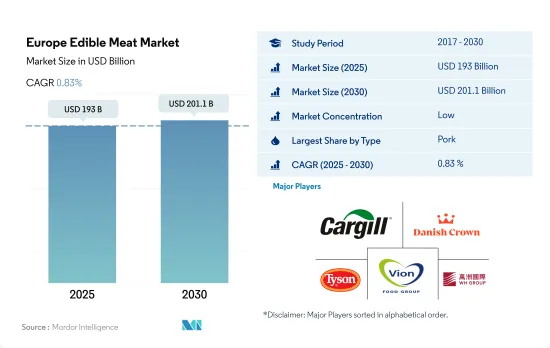

The Europe Edible Meat Market size is estimated at 193 billion USD in 2025, and is expected to reach 201.1 billion USD by 2030, growing at a CAGR of 0.83% during the forecast period (2025-2030).

The rise in demand for ready-to-eat meat favors the market

- Pork is the major type of meat consumed in Europe, and the sales of pork increased by 1.57% in 2022 compared to the previous year. In 2021, the European pork meat market experienced a major trend related to rising output. EU market leaders continuing to expand production are Spain, Denmark, and the Netherlands. The supply of pork in Europe was significantly greater than the demand in 2022. As a result, pork consumption increased across Europe, particularly in the south. However, lower carcass prices and the threat of additional African Swine Fever (ASF) outbreaks in Central Europe may hamper the growth of the market in the future.

- Beef consumption is mainly driven by the demand for ready-to-eat meat products across Europe. In Europe, the demand for processed beef is rising due to increased demand for convenient food like sandwiches, beef sticks, bacon, beef jerky, and pork rinds. Processed beef is projected to register a CAGR value of 1.68% during the forecast period. BRF SA, Cargill Inc., Danish Crown Amba, and Tyson Foods Inc. are the key players that offer processed beef in Europe.

- Mutton is the fastest-growing segment of meat in the region, and it is projected to record a CAGR value of 0.91% during the forecast period. There are over 70 million sheep and goats in the European Union (85% sheep and 15% goats). Greece, Spain, France, and Romania are the major mutton-producing areas in Europe. Around 20% of the mutton that is consumed in the region is imported. New Zealand supplies around 89% of the mutton requirement in all other European countries. The meat from lamb (sheep meat, less than one year) is more popular than regular mutton (sheep meat, less than three years) in Europe.

Poultry and pork meat consumption is driving the market

- Edible meat sales in Europe have seen stable growth over the years, increasing by 8.97% from 2018 to 2022. Russia, France, and Germany dominate the consumption trend. In 2022, these countries also dominated the livestock population count in the region, with Russia (18.56 million) leading the trend, followed by France (17.78 million), Germany (11.3 million), and Spain (6.63 million). Pork is the most consumed meat type in Europe.

- In Europe, Italy is the fastest-growing edible meat market. It is projected to register a CAGR of 1.20% by value during the forecast period. This increase was mainly due to the increased pork consumption in Italy. Italy accounted for about 41.96% by value of the pork market share in 2022 compared to other meat types. More than 70% of pigs grown in Italy are bred in the north, while 74% of farms in the center-south are in the industry due to the small size of the farms. The pork industry also increasingly utilizes data analytics and blockchain technology, utilizing sensors to enhance traceability, transparency, and food safety.

- The European edible meat market is projected to record a value CAGR of 0.32% during the forecast period. The lower progression can be attributed to reduced meat consumption in European countries. Nearly 46% of Europeans reported eating less meat in 2022 than the previous year. However, some other countries are yet to catch up with this trend due to their food cultures. Some cultures believe that plant-based meat lacks adequate flavor and nutrition. They consider meat as a proper meal and a good source of nutrition. Some people also believe plant-based foods are too expensive, difficult to prepare, or visually less appealing.

Europe Edible Meat Market Trends

Despite the Russia-Ukraine conflict, Russia remains a major beef producer in the region

- In 2022, beef production in Europe declined by 0.98% compared to the previous year, owing to reduced pricing and herd reductions. Russia, France, and Germany accounted for roughly 40% of the beef produced in Europe. The European Commission has plans to use public intervention to support beef prices if the average market price of beef in an EU country or region drops below USD 2,416 per ton over a selected period. The European Commission may provide grants for private storage aid if there is a drop in average prices or a substantial change in production costs, another factor that causes significant changes in margins damaging to the industry. The EU also supports beef farmers through specific exemptions for producer organizations in the beef industry.

- Russia was the major beef producer in the region in 2022, with a share of 15.96% in 2022. This growth was facilitated by exceptional measures taken by the state to support the industry. Some of the measures include reimbursing livestock breeders for the costs of their production, purchasing young animals, technological modernization of facilities, and improving work in the field of livestock breeding. Producers are offered loans for the purchase of fodder, equipment, veterinary drugs, and the construction and modernization of livestock facilities.

- The Netherlands had the lowest production of 429,640 tons in 2022. The Dutch national cattle inventory has constantly declined in the last three years due to the exceeding EU pasture phosphate limits. In 2022, beef cattle numbers declined by 8.4% to 3,690,000 heads. The government has been trying to reduce emissions through a decrease in livestock farming, which negatively impacts the country's beef industry.

Increasing cost of feed and decline in slaughter of variants of cows are leading to price fluctuations of beef in the region

- During 2019-2022, the price of beef grew by 5.34% due to supply chain disruptions that caused a rise in wholesale beef prices while cattle prices remained low. The whole service sale of beef recovered due to a rise in foodservice sales, even of premium cuts, leading to a 3% rise in total consumption. In 2021, the decline in suckler cows, which are bred for terminal beef, by 245,000 heads (-2.3%) led to increasing beef prices. Inadequate facilities, hygiene measures, and improper handling of the animals at the slaughterhouses further aggravate the microbial contamination of beef, which can result in the transmission of foodborne pathogens to humans

- The rising feed costs also contributed to the increase in beef prices by 26% during the first quarter of 2022. High input costs, particularly for feed, may result in additional slaughtering and lower carcass weights, primarily on intensive cattle farms where feed costs will have a greater impact on farm profitability. Due to the rising food and meat prices, the region's beef consumption decreased to 10.3 kg per capita in 2022 (-0.3%). This trend was likely to continue in 2022, reaching -0.9% in the overall context.

- Owing to very high food price inflation during 2021-2023 in Europe, consumer demand for meat has been consistently declining, coupled with higher awareness about individual health and the environment. Due to the high prices and declining demand, beef production across many countries in Europe observed a decline. For instance, in 2022, Italy saw a production slump of 20%, followed by Spain and Germany reporting falls of 6% and 1%, respectively. France recorded a 1% increase in production, while the Netherlands recorded an increase in beef production by 9%.

Europe Edible Meat Industry Overview

The Europe Edible Meat Market is fragmented, with the top five companies occupying 10.15%. The major players in this market are Cargill Inc., Danish Crown AmbA, Tyson Foods Inc., Vion Group and WH Group Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Beef

- 3.1.2 Mutton

- 3.1.3 Pork

- 3.1.4 Poultry

- 3.2 Production Trends

- 3.2.1 Beef

- 3.2.2 Mutton

- 3.2.3 Pork

- 3.2.4 Poultry

- 3.3 Regulatory Framework

- 3.3.1 France

- 3.3.2 Germany

- 3.3.3 Italy

- 3.3.4 United Kingdom

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Beef

- 4.1.2 Mutton

- 4.1.3 Pork

- 4.1.4 Poultry

- 4.1.5 Other Meat

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Italy

- 4.4.4 Netherlands

- 4.4.5 Russia

- 4.4.6 Spain

- 4.4.7 United Kingdom

- 4.4.8 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 BRF S.A.

- 5.4.2 Cargill Inc.

- 5.4.3 Danish Crown AmbA

- 5.4.4 Dawn Meats

- 5.4.5 Gruppa Cherkizovo, PAO

- 5.4.6 Heck! Food Ltd

- 5.4.7 Hormel Foods Corporation

- 5.4.8 JBS SA

- 5.4.9 Mitsubishi Corporation

- 5.4.10 NH Foods Ltd

- 5.4.11 Nomad Foods Limited

- 5.4.12 Tyson Foods Inc.

- 5.4.13 Vion Group

- 5.4.14 WH Group Limited

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

欧州の食用肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 266 Pages

- 納期

- 2~3営業日