アジア太平洋地域の食用肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Asia-Pacific Edible Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 243 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692039

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

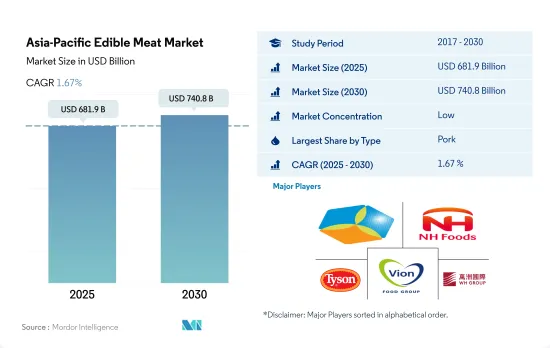

アジア太平洋地域の食用肉の市場規模は2025年に6,819億米ドルと推定され、2030年には7,408億米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは1.67%で成長します。

豚肉生産量の増加と鶏肉価格の低下が需要を促進

- アジア太平洋の赤身肉セグメントは、調査期間を通じて豚肉が大きくリードしており、2022年の市場金額シェアは鶏肉よりも13%多く、食肉の種類の中で2番目に消費されています。豚肉はまた、予測期間中に最も急速に成長する食肉タイプになると予測され、CAGR値は2.12%を記録します。これは主に豚肉の生産量の増加によるものです。豚肉はこの地域で最も生産されている食肉タイプであり、2021年から2022年にかけて国内生産量は24.3%増加しました。

- しかし、中国は高い需要により域内で最大の売上を生み出し、2022年には約5,390万トンを生産する最大の豚肉生産国です。APAC地域全体の1人当たり売上高は、2023年には117.50米ドルと算出され、販売額が増加しています。

- マトンは、予測期間中にCAGR値1.35%の高成長を遂げる可能性が高いです。持続可能でありながらカーボンフットプリントを削減する牧草飼育肉に対する消費者の嗜好により、マトンの需要が高まっています。外食産業は、新常態となりつつある在宅勤務の傾向により、ほとんどの人がマトンを手に入れる場所であり、加工・冷凍形態の需要を大きく牽引しています。例えばアジア太平洋では、人口の約50~60%がハイブリッド型で働いています。

- 鶏肉も市場で大きなシェアを占めており、予測期間中にCAGR値1.37%を記録すると予測されています。これは、この地域で鶏肉を多く入手できることと、赤身肉の価格より30~40%程度低い手頃な価格が市場を積極的に牽引しているためです。

中国が同地域最大の食用肉消費国

- アジア太平洋地域の食用肉市場は、2017年から2022年にかけて2.50%の正のCAGRで推移すると予測されました。中国、ベトナム、韓国など、この地域の主要国における高病原性鳥インフルエンザ(HPAI)の影響は、セグメントの成長に若干の影響を与えました。2022年12月、香港(Yuen Long)でHPAI亜型H5N1の再発が始まりました。2022年10月以降、1,460万羽以上の日本の家禽が、H5N1ウイルス血清型に関連するHPAIの発生によって直接影響を受けています。台湾では、2022年に20件の発生が325,700羽以上の商業用家禽に直接影響を与えました。

- 中国は主要な食肉消費国であり、予測期間中により大きな市場シェアを占めると予想されます。同国における食用肉の売上高は、2022年には前年比2.25%増加しました。中国は世界の食肉の28%を消費しており、世界の豚肉の約半分も消費しています。入手可能性の高さと人口の増加が、中国の食肉製品需要を牽引する主な要因です。豚肉は中国で最も広く消費されている肉の種類であり、2022年には中国の食用肉全体の50.07%を占めました。

- インドは予測期間中に最も急成長する国と予想され、金額ベースでCAGR 2.24%を記録します。インドでは、2022年時点で鶏肉が最も消費されています。インドの人口の約70%は非ベジタリアンです。2021~2022年の国内の食肉総生産量は約929万トンで、数量ベースの年間成長率は5.62%でした。インドは食肉の供給が豊富であり、同国の食肉加工産業は予測期間中に成長すると予想されます。

アジア太平洋地域の食用肉市場の動向

輸出需要の増加により主要生産国が成長

- アジア太平洋地域では、牛肉の主要生産国は中国、インド、オーストラリアで、2022年の数量シェアはそれぞれ38.71%、21.49%、9.28%でした。中国では、2022年の生産量は2021年比で2.74%増加しました。大規模農場を中心とした牛群の増加と、豚肉不足の継続に起因する旺盛な国内需要により、生産量は今後も伸びると予想されます。飼料コストの高騰と牛肉製品の低価格輸入は、中国の畜牛生産に影響を及ぼすと思われます。牛肉製品に対する消費者の需要は、通常のホテルやレストランでの取引にとどまらず、調理済み食品にまで拡大しています。

- インド市場は、輸出需要の拡大と国内消費のわずかな増加により、2022年には2021年比で約3.69%の伸びを示しました。2023年には、インドの牛肉消費量は7億7,900万kgとなり、2022年から1.84%増加すると予想され、これは主に手頃な価格設定によるものです。良質な食肉の供給と促進のため、国内の規制機関は、後方統合や契約栽培の促進を含め、農民協同組合が重要な役割を果たすよう奨励しています。

- 2023年3月、オーストラリアで食肉処理された牛の頭数は、前年比13.5%増の170万頭でした。2023年3月期の牛肉生産量は前年同期比11.3%増の52万4,335トンでした。2022年、オーストラリアは約190万トンの枝肉重量(cwt)の牛肉と子牛肉を生産し、同年、オーストラリアは牛肉と子牛肉の総生産量の67%を輸出しました。国内の豊富な放牧地が牧草牛の生産を支えました。2022年には270万頭の穀物肥育牛が市場に出回り、成牛の食肉処理頭数の47%を占めました。

牛肉価格は、大規模な生産基盤のおかげで、この地域では安定したペースで伸びています。

- 2022年、この地域の牛肉価格は2021年に比べ0.96%上昇しました。この価格上昇は、地政学的状況の過熱、世界の商品に対する供給の不均衡と需要、エネルギー価格の上昇、物流障壁に起因します。2023年の牛肉価格指数は低下し、6月には118.48に達し、2022年の同時期の135.83から低下し、この地域の牛肉価格は安定すると予想されます。

- 中国はアジア太平洋地域で最大の牛肉生産国であるため、中国の牛肉価格はアジア太平洋市場に大きな影響を与えます。中国の牛肉価格は、地域平均成長率1.40%に対し、レビュー期間を通じて平均2.02%で上昇しました。同国はまた、ブラジルからかなりの量の牛肉を輸入しており、主に工業化製品やその他の大衆料理の調理に使用されています。2023年には、国内生産の増加により輸入が減少し、価格が安定します。この地域の牛肉価格は祝祭シーズンに高騰します。インドネシアなどでは、2022年の牛肉価格は9.75米ドルから6.96米ドル/kgであったが、イードとラマダン期間中は11.84米ドル/kg前後でした。

- オーストラリアはこの地域の牛肉生産量のトップ3に入り、この地域の高級牛肉の主な供給源となっています。オーストラリアで年間生産される牛肉の60%以上が世界市場に輸出されます。市場におけるオーストラリア産若牛の価格は約2年間で132%も跳ね上がり、2021年10月には7.99米ドルに達しました。インドネシアやベトナムなどの国からの輸入業者は、オーストラリアの通貨高と牛の価格上昇が重なり、苦戦を強いられました。しかし、CIF(コスト、保険、運賃)の上昇にもかかわらず、インドネシアとベトナムの牛肉小売価格は堅調でした。

アジア太平洋地域の食用肉産業の概要

アジア太平洋地域の食用肉市場は断片化されており、上位5社で4.22%を占めています。この市場の主要企業は以下の通りです。 COFCO Corporation, NH Foods Ltd, Tyson Foods Inc., Vion Group and WH Group Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 牛肉

- 羊肉

- 豚肉

- 家禽類

- 生産動向

- 牛肉

- 羊肉

- 豚肉

- 家禽類

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タイプ

- 牛肉

- 羊肉

- 豚肉

- 家禽類

- その他の肉

- 形態

- 缶詰

- 生鮮・冷蔵

- 冷凍

- 加工

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オントレード

- オフトレード

- 国捌

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- その他アジア太平洋地域

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Bid Corporation Limited

- China Yurun Food Group Ltd

- COFCO Corporation

- Danish Crown AmbA

- Linyi Xincheng Jinluo Meat Products Co. Ltd

- NH Foods Ltd

- Tyson Foods Inc.

- Tonnies Holding ApS & Co. KG

- Vion Group

- Westfleisch SCE mbH

- WH Group Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 90331

The Asia-Pacific Edible Meat Market size is estimated at 681.9 billion USD in 2025, and is expected to reach 740.8 billion USD by 2030, growing at a CAGR of 1.67% during the forecast period (2025-2030).

Increase in pork production and lower poultry prices fueling the demand

- The Asia-Pacific red meat segment was majorly led by pork meat throughout the study period, with 13% more market value share than poultry meat, which was the second most consumed type of meat in 2022. Pork meat is also anticipated to be the fastest-growing meat type during the forecast period, registering a CAGR value of 2.12%. This can be mainly supported by its growing production rate. It was the most produced meat type in the region, with a hike of 24.3% in domestic production from 2021 to 2022, as the governments are investing in the advancement of the production technologies of pork meat and pig farming.

- However, China generates the largest sales within the region due to high demand and is the largest producer of pork, producing around 53.9 million metric tons in 2022. The overall revenue per person for the APAC region was calculated at USD 117.50 in 2023, which is increasing the sales value.

- Mutton is likely to witness a high-growing CAGR value of 1.35% during the forecast period. Due to consumer preference for grass-fed meat, which reduces carbon footprint while being sustainable, the demand for mutton is rising. The food service industry is where most people get their mutton due to the work-from-home trend, which is becoming a new normal and driving the demand for processed and frozen forms majorly. For instance, in Asia-Pacific, around 50-60% of the population is working in a hybrid model.

- Poultry meat also accounted for a significant share in the market, which is projected to register a CAGR value of 1.37% during the forecast period because of the high availability of chicken in the region and the affordable prices, which are around 30-40% lower than red meat prices, driving the market positively.

China is the largest consumer of edible meat in the region

- The edible meat market in Asia-Pacific was anticipated to register a positive CAGR of 2.50% during 2017-2022. The influence of highly pathogenic avian influenza (HPAI) in the major countries in the region, such as China, Vietnam, and South Korea, slightly impacted the segmental growth. In December 2022, the recurrence of HPAI subtype H5N1 started in Hong Kong (Yuen Long). Since October 2022, more than 14.6 million Japanese poultry have been directly impacted by HPAI outbreaks linked to the H5N1 virus serotype. In Taiwan, 20 outbreaks directly impacted more than 325,700 commercial birds in 2022.

- China is a major meat-consuming country and is expected to hold a larger market share during the forecast period. The sales of edible meat in the country increased by 2.25% in 2022 compared to the previous year. China consumes 28% of the world's meat, and it also consumes around half of all pork in the world. The high availability and growing population are the major factors driving the demand for meat products in China. Pork was the most widely consumed meat type in China and accounted for 50.07% of the total edible meat in China in 2022.

- India is anticipated to be the fastest-growing country in the forecast period, registering a CAGR of 2.24% on a value basis. In India, poultry meat was the most consumed meat as of 2022. Around 70% of the Indian population is non-vegetarian. The total meat production in the country was around 9.29 million tons during 2021-2022, with an annual growth rate of 5.62% by volume. India has an abundant supply of meat, and the meat processing industry in the country is anticipated to grow during the forecast period.

Asia-Pacific Edible Meat Market Trends

Major producing countries are observing growth owing to the increasing export demand

- In Asia-Pacific, the leading producers of beef were China, India, and Australia, with a volume share of 38.71%, 21.49% and 9.28% respectively, in 2022. In China, production grew by 2.74% in 2022 compared to 2021. The production is anticipated to grow in the future, driven by rising cattle herds, particularly on large farms, and strong domestic demand owing to the ongoing pork shortage. High feed costs and lower-cost imports of beef products would have an impact on China's cattle production. Consumer demand for beef products has grown beyond the normal hotel and restaurant trade to include ready-cooked meals.

- The Indian market saw a growth of around 3.69% in 2022 compared to 2021, owing to the growing export demand and marginally higher domestic consumption. In 2023, India was expected to consume 779 million kg of beef, an increase of 1.84% from 2022, driven largely by its affordable pricing. For the supply and promotion of quality meat, the regulatory bodies in the nation are encouraging farmers' cooperatives to play an important role, including the promotion of backward integration and contract farming.

- In March 2023, the number of cattle slaughtered in Australia increased 13.5% to 1.7 million compared to the previous year. Beef production in the March 2023 quarter increased 11.3% to 524,335 tons compared to the same period in 2022. In 2022, Australia produced approximately 1.9 million tons of carcass weight (cwt) of beef and veal, and in the same year, Australia exported 67% of its total beef and veal production. The plentiful grazing pasture in the country supported the production of grass-fed cattle. In 2022, 2.7 million grain-fed cattle were marketed, accounting for 47% of all adult cattle slaughtered.

Beef prices are growing at a steady pace in the region owing to the large production base

- In 2022, beef prices in the region were up by 0.96% compared to 2021. This rise in prices was owing to the heated geopolitical conditions, supply imbalance and demand for global commodities, increasing energy prices, and logistic barriers. The beef price index saw a decrease in 2023, reaching 118.48 in June and falling from 135.83 during the same period in 2022, which is anticipated to stabilize the beef prices in the region.

- The price of beef in China highly impacts the Asia-Pacific market, owing to China being the largest producer of beef in the region. The price of beef in China increased at an average of 2.02% throughout the review period compared to a regional average growth rate of 1.40%. The country also imports a good amount of beef from Brazil, which is mainly used in preparing industrialized products and other popular dishes. In 2023, the country saw a decrease in imports owing to the increase in local production, thus stabilizing the prices. The beef prices in the region experience a spike during the festive season. In countries like Indonesia, in 2022, beef prices ranged from USD 9.75 to USD 6.96/kg, whereas it was around USD 11.84/kg during Eid and Ramadan.

- Australia is among the top three producers of beef in the region and a major source of premium beef in the region. More than 60% of the beef produced annually in Australia is exported to the global market. The price of young Australian cattle in the market jumped by 132% in about two years, reaching USD 7.99 in October 2021. Importers from countries such as Indonesia and Vietnam struggled with a combination of a strong Australian currency and rising cattle prices. However, despite the rise in CIF (cost, insurance, and freight), retail beef prices were steady in both Indonesia and Vietnam.

Asia-Pacific Edible Meat Industry Overview

The Asia-Pacific Edible Meat Market is fragmented, with the top five companies occupying 4.22%. The major players in this market are COFCO Corporation, NH Foods Ltd, Tyson Foods Inc., Vion Group and WH Group Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Beef

- 3.1.2 Mutton

- 3.1.3 Pork

- 3.1.4 Poultry

- 3.2 Production Trends

- 3.2.1 Beef

- 3.2.2 Mutton

- 3.2.3 Pork

- 3.2.4 Poultry

- 3.3 Regulatory Framework

- 3.3.1 Australia

- 3.3.2 China

- 3.3.3 India

- 3.3.4 Japan

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Beef

- 4.1.2 Mutton

- 4.1.3 Pork

- 4.1.4 Poultry

- 4.1.5 Other Meat

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 Australia

- 4.4.2 China

- 4.4.3 India

- 4.4.4 Indonesia

- 4.4.5 Japan

- 4.4.6 Malaysia

- 4.4.7 South Korea

- 4.4.8 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Bid Corporation Limited

- 5.4.2 China Yurun Food Group Ltd

- 5.4.3 COFCO Corporation

- 5.4.4 Danish Crown AmbA

- 5.4.5 Linyi Xincheng Jinluo Meat Products Co. Ltd

- 5.4.6 NH Foods Ltd

- 5.4.7 Tyson Foods Inc.

- 5.4.8 Tonnies Holding ApS & Co. KG

- 5.4.9 Vion Group

- 5.4.10 Westfleisch SCE mbH

- 5.4.11 WH Group Limited

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

アジア太平洋地域の食用肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 243 Pages

- 納期

- 2~3営業日