米国の家禽肉- 市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

United States Poultry Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 209 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692066

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

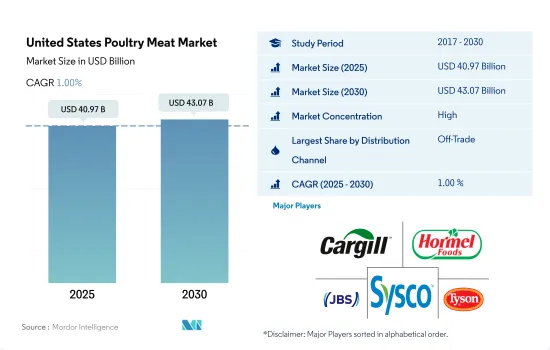

米国の家禽肉市場規模は2025年に409億7,000万米ドルと推定・予測され、2030年には430億7,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは1.00%で成長すると予測されます。

生産技術の向上と流通網の拡大が市場を牽引

- 市場は2017年から2022年にかけて金額ベースで28.64%の成長を観測しました。米国における家禽肉販売は、予測期間中、金額ベースでオフ・トレード・チャネルが支配的になると予想されます。これは、特に脂肪含量の低下と低価格に起因しています。国内生産量の増加といった要因も市場を後押ししています。これは、鳥類がより短時間で生産要件を満たすことを可能にする育種遺伝学の進歩や、飼料、食肉処理、加工技術の改善によるものです。

- 取引外の流通チャネルは、予測期間中に最も急速に成長し、金額ベースで1.25%の成長を記録すると予想されます。インテグレーター直営またはフランチャイズのチルド/冷凍家禽販売店の設立、既存の食品店への販売カウンターの設置、宅配サービスの提供など、家禽インテグレーターの新戦略が小売市場の成長を促しています。スーパーマーケットやオンラインショップも、チルド・冷凍家禽の小売販売の成長を支えています。コールドチェーンへのこうした投資は、加工家禽の成長のためのチャネルを生み出しています。冷凍家禽は、業界外の流通チャネルにおける主要セグメントです。冷凍鶏肉は、オフトレード・チャネルによる販売額の65.19%を占めています。

- オン・トレード・チャネルは2017年から2022年にかけて金額ベースで25.46%の成長を遂げました。フルサービス・レストランやクイックサービス・レストランのような業務用食品サービスが、業務用食品サービスよりも大きなシェアを占めています。チキン業界では新しいレストランのアイデアやアプローチも試みられています。例えば、2021年にバッファロー・ワイルド・ウィングスはバッファロー・ワイルド・ウィングス・ゴーと名付けられた店舗を立ち上げました。同店は持ち帰りやデリバリーに特化しています。同様に、Chick-fil-AはLittle Blue Menuという新しいバーチャルレストランのデリバリー専用ブランドを立ち上げました。

米国の家禽肉市場動向

家禽生産量の増加が市場成長を牽引

- 米国の家禽産業は世界最大の生産国であり、世界第2位の輸出国でもあります。同国の家禽肉(ブロイラー、その他の鶏肉、七面鳥)の消費量は、牛肉や豚肉など他の種類の肉よりも約45%多いです。家禽肉の生産額は、ブロイラーが68%、七面鳥が13%、鶏は1%未満です。

- 2021年の米国のブロイラー生産数は91億3,000万羽で、2020年から1%減少します。2021年に飼育された七面鳥は2億1,700万羽で、2020年から3%減少しました。2022年1月~9月の米国における七面鳥の食肉生産量は39億1,000万ポンドで、2021年の同時期から7%減少しました。しかし、七面鳥の生産量の減少は、ブロイラーの生産量の増加が上回りました。2022年に米国が販売した鶏(ブロイラーを除く)は約2億羽で、2021年から4%減少しました。卵は約1,110億個生産され、2021年の1,120億個から1%減少しました。ジョージア州、アラバマ州、アーカンソー州はブロイラーを生産する米国の主要州で、2022年にはそれぞれ12億9,89万羽、11億7,160万羽、10億5,130万羽/頭を占めました。野生のニワトリは通常1年に10~12個の卵を産むが、産卵の際に体が受けるストレスによってその数は制限されます。

- 養鶏業界全体の2022年の売上高は769億米ドルで、2021年から67%増加しました。ブロイラー鶏の売上は60%増、七面鳥の売上は21%増、卵の売上は122%増でした。2022年には、3つの業界すべてが値上げに見舞われたが、高病原性鳥インフルエンザ(HPAI)の出現は特に鶏卵と七面鳥業界に悪影響を及ぼしました。2021年から2022年にかけて、基準価格は七面鳥で25.9%、ブロイラーで38.9%上昇しました。

飼料価格の高騰が家禽肉価格を押し上げた

- 家禽セクターは2022年に発生した高病原性鳥インフルエンザ(HPAI)の影響を受けました。発生前の逼迫した供給と疾病に関連した供給不足により、鶏の卸売価格は11月に1ポンド当たり1.81米ドルと月平均で過去最高まで上昇し、2022年の第4四半期を通して価格は高止まりしました。2023年の最初の7週間の平均価格は1ポンドあたり1.72米ドルでした。2023年後半は価格が下落すると予想されるが、全米の七面鳥の平均価格は1ポンド当たり1.62米ドルとなり、2022年の平均1.55米ドルと比較されると予想されます。

- 米国の家禽価格は飼料コストの上昇により上昇しています。ロシアは世界のトウモロコシ輸出の17%を生産しています。またロシアは、鶏の飼料となるトウモロコシの生産に不可欠な3種類の主要肥料(窒素、リン、カリウム)の最大輸出国のひとつでもあります。ロシア・ウクライナ戦争は家禽の飼料コストを上昇させ、国内の家禽価格を高騰させました。

- その後の経済再開と成長によって供給が逼迫し、様々な形態や場所にある鶏胸肉の価格が上昇しました。2021年、骨なし・皮なしの鶏胸肉は1ポンド当たり3.45米ドルだったが、2022年には4.32米ドルに上昇しました。鶏胸肉、骨なしチキン、チキンレッグ、手羽先のような他のカットの需要が高いのは、主にKFC、Popeyes、Jollibee、Mcdonald'sのような外食事業者が特定の種類のカットを使用するためです。したがって、予測期間中に価格が上昇することが予想されます。

米国の家禽肉産業の概要

米国の家禽肉市場はかなり統合されており、上位5社で71.01%を占めています。この市場の主要企業は以下の通り。 Cargill Inc., Hormel Foods Corporation, JBS SA, Sysco Corporation and Tyson Foods Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 鶏肉

- 生産動向

- 鶏肉

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 缶詰

- 生鮮/冷蔵

- 冷凍

- 加工品

- 加工タイプ別

- デリミート

- マリネ/テンダー

- ミートボール

- ナゲット

- ソーセージ

- その他加工家禽

- 流通チャネル

- 非売品

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- 非売品

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BRF S.A.

- Cargill Inc.

- Continental Grain Company

- Foster Farms Inc.

- Hormel Foods Corporation

- JBS SA

- Mountaire Farms

- Perdue Farms Inc.

- Sysco Corporation

- Tyson Foods Inc.

- WH Group Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 90367

The United States Poultry Meat Market size is estimated at 40.97 billion USD in 2025, and is expected to reach 43.07 billion USD by 2030, growing at a CAGR of 1.00% during the forecast period (2025-2030).

The market is driven by improved production techniques and the expansion of distribution networks

- The market observed a growth of 28.64% by value from 2017 to 2022. The poultry meat sales in the United States are expected to be dominated by off-trade channels by value during the forecast period. This is owing, among other things, to its decreased fat content and lower price. Factors such as rising domestic production, attributed to advances in breeding genetics that allow birds to meet production requirements in a shorter amount of time and improvements in feed, slaughter, and processing technologies, are also boosting the market.

- The off-trade distribution channel is expected to be the fastest-growing channel during the forecast period and register a growth of 1.25% by value. New strategies from poultry integrators, such as setting up integrator-owned or franchised chilled/frozen poultry shops, putting sales counters in already-existing food stores, and offering home delivery, are encouraging growth in the retail market. Supermarkets and online stores are also supporting growth in the retail sales of chilled and frozen poultry products. These investments in the cold chain are creating channels for the growth of processed poultry. Frozen poultry is a major segment for the off-trade distribution channels. It holds 65.19% of sales through off-trade channels by value.

- The on-trade channel saw a growth of 25.46% by value from 2017 to 2022. Commercial foodservices like full-service and quick-service restaurants held a major share than institutional foodservices. New restaurant ideas and approaches are also being tried in the chicken industry. For instance, in 2021, Buffalo Wild Wings launched an outlet named Buffalo Wild Wings Go. It concentrates on takeaway and delivery. Similarly, Chick-fil-A launched a new virtual restaurant delivery-only brand called Little Blue Menu.

United States Poultry Meat Market Trends

Rising poultry production is driving the market growth

- The US poultry industry is the world's largest producer and second-largest exporter of poultry meat, as well as a major egg producer. The country's consumption of poultry meat (broilers, other chicken, and turkey) is about 45% higher than other meat types like beef or pork. Its combined poultry production value includes 68% from broilers, 13% from turkey, and less than 1% from chickens.

- In 2021, the United States produced 9.13 billion broilers, a 1% decline from 2020. The number of turkeys raised in 2021 was 217 million, down by 3% from 2020. Turkey's meat production in the United States during January-September 2022 was 3.91 billion pounds, which was 7% down from the same period in 2021. However, the decline in turkey production was outweighed by increases in broiler production. In 2022, the United States sold nearly 200 million chickens (excluding broilers), a decrease of 4% from 2021. About 111 billion eggs were produced, a 1% decrease from 112 billion in 2021. Georgia, Alabama, and Arkansas were the leading US states producing broilers and accounted for 1,298,900, 1,171,600, and 1,051,300 thousand per head of broilers, respectively, in 2022. Chickens in the wild usually lay 10-12 eggs a year, limited by the stress their bodies undergo when laying.

- Sales in the poultry industry as a whole totaled USD 76.9 billion in 2022, up 67% from 2021. Sales of broiler chicken climbed by 60%, turkey sales by 21%, and egg sales by 122%. In 2022, all three industries experienced price increases, with the emergence of highly pathogenic avian influenza (HPAI) having an especially negative effect on the egg and turkey industries. From 2021 to 2022, benchmark prices rose 25.9% for turkeys and 38.9% for broilers.

High feed prices elevated the prices of poultry meat

- The poultry sector was affected by the Highly Pathogenic Avian Influenza (HPAI) outbreak in 2022. With tight supplies before the outbreak and disease-related supply shortages, wholesale hen prices climbed to a record monthly average of USD 1.81 per pound in November, and prices remained elevated throughout the fourth quarter of 2022. Prices for the first seven weeks of 2023 had an average of USD 1.72 per pound. Although prices were expected to fall during the second half of 2023, the average national turkey hen price is expected to be USD 1.62 per pound, compared to an average of USD 1.55 in 2022.

- Chicken prices in the United States are rising due to higher feed costs. Russia produces 17% of the world's maize exports. Russia is also one of the largest exporters of the three main types of fertilizers (nitrogen, phosphorous, and potassium), which are essential to the production of corn used as feed for poultry. The Russia-Ukraine War consequently increased the feed costs for poultry, which escalated the prices of chicken meat in the country.

- The subsequent economic reopening and growth have tightened supplies and increased the prices for chicken breasts, which are in various forms and places. In 2021, boneless and skinless chicken breasts were USD 3.45 per and increased to USD 4.32 per pound in 2022. High demand for chicken breasts, boneless chicken, chicken legs, and other cuts like chicken wings is mainly due to the use of specific types of cuts by foodservice operators such as KFC, Popeyes, Jollibee, and Mcdonald's. Hence, it is anticipated to elevate the price during the forecast period.

United States Poultry Meat Industry Overview

The United States Poultry Meat Market is fairly consolidated, with the top five companies occupying 71.01%. The major players in this market are Cargill Inc., Hormel Foods Corporation, JBS SA, Sysco Corporation and Tyson Foods Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Poultry

- 3.2 Production Trends

- 3.2.1 Poultry

- 3.3 Regulatory Framework

- 3.3.1 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Canned

- 4.1.2 Fresh / Chilled

- 4.1.3 Frozen

- 4.1.4 Processed

- 4.1.4.1 By Processed Types

- 4.1.4.1.1 Deli Meats

- 4.1.4.1.2 Marinated/ Tenders

- 4.1.4.1.3 Meatballs

- 4.1.4.1.4 Nuggets

- 4.1.4.1.5 Sausages

- 4.1.4.1.6 Other Processed Poultry

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 BRF S.A.

- 5.4.2 Cargill Inc.

- 5.4.3 Continental Grain Company

- 5.4.4 Foster Farms Inc.

- 5.4.5 Hormel Foods Corporation

- 5.4.6 JBS SA

- 5.4.7 Mountaire Farms

- 5.4.8 Perdue Farms Inc.

- 5.4.9 Sysco Corporation

- 5.4.10 Tyson Foods Inc.

- 5.4.11 WH Group Limited

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

米国の家禽肉- 市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 209 Pages

- 納期

- 2~3営業日