|

市場調査レポート

商品コード

1939053

中国のペットフード:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)China Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のペットフード:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

概要

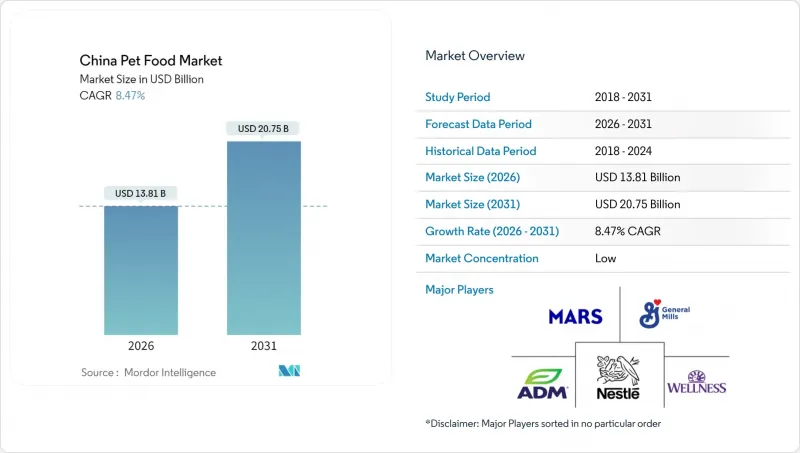

中国のペットフード市場は、2025年に127億3,000万米ドルと評価され、2026年の138億1,000万米ドルから2031年までに207億5,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは8.47%と見込まれます。

プレミアム製品の開発、消費者直販モデルの革新、機能性重視のポジショニングにより平均販売価格が上昇する一方、都市化と可処分所得の増加がペット飼育世帯の拡大を促進しています。国内メーカーは高利益率のおやつ分野で価値を獲得すべくフリーズドライ製品の生産能力を拡大し、ライブコマースは商品発見から購入までのプロセスを短縮することで、ニッチブランドが多国籍企業と直接競合することを可能にしています。表示や原材料のトレーサビリティに関する規制強化は消費者の信頼を強化し、価格に敏感な第三級市場においてもプレミアム・治療食のシェア拡大に寄与しています。原材料コストの変動やカーボンニュートラル対応のコストは利益率を抑制する一方、技術革新やサプライチェーンの多様化を促進しています。

中国ペットフード市場の動向と洞察

猫・犬用フードのプレミアム化加速

2024年にはプレミアム製品が18~22%拡大しました。ペットオーナーが限定原料・有機・獣医師推奨の処方へ移行したためで、標準的なドライフードより40~60%高価格帯となっています。トップ層の消費者は製品選択において、食品安全認証や消化・アレルギー管理をサポートする昆虫由来・植物性などの新規タンパク源を重視しています。農業農村部が発表した明確な飼料安全基準では、タンパク質の品質とトレーサビリティの規範が規定され、小売業者が高級ラインを自信を持って販売できるようになりました。このプレミアム化の波は、ペット1頭あたりの平均支出額を増加させることで中国ペットフード市場を押し上げ、メーカーが高価格設定を正当化する調査や包装の改良に投資するよう促しています。世帯収入の増加により価格格差が縮小し、ソーシャルメディアが動向拡散を加速させる中、第2層市場への波及効果は既に顕著です。したがって、プレミアム化の潮流は、ブランドメーカーにとって販売数量の安定と利益率拡大の両方を支える基盤となっております。

DTC(ダイレクト・トゥ・カスタマー)型デジタルネイティブペットフードブランドの台頭

デジタルネイティブ企業は、2024年にTmall、JD、小紅書(シャオホンシュ)のオンラインストア限定販売により約12~15%のシェアを獲得しました。これらのプラットフォームでは、当日配送とデータ駆動型のパーソナライゼーションがリピート購入を促進しています。定期購入バンドルは在庫リスクを低減し予測可能なキャッシュフローをもたらす一方、双方向ライブ配信は従来のマスメディア広告では実現できないコミュニティエンゲージメントを強化します。消費者レビューエコシステムは透明性と迅速な製品改良を促進し、スタートアップ企業がわずか6週間で新SKUを展開することを可能にしています。JDロジスティクスや菜鳥ネットワークとの物流提携により、ラストマイルコストを削減し、生鮮食品・生食製品のコールドチェーン網を拡大しています。こうした動きにより、中国のペットフード市場では、ブランド価値がATL(Above-The-Line)広告からデジタル親密度や顧客生涯価値分析へと移行する構造的変化が生じています。既存の多国籍企業は、既存の小売チャネルを損なうことなくDTC(Direct-to-Consumer)ノウハウを獲得するため、合弁事業や少数株主投資で対応しています。

家禽・魚粉原料価格の変動性

2024年には鳥インフルエンザによる供給障害や漁獲枠の不透明感から、タンパク質原料価格が15~25%変動しました。これにより小売価格の選択的値上げが行われ、需要の弾力性が損なわれるリスクが生じています。家禽ミールは1トン当たり8,500元(1,200米ドル)でピークに達した後、7,200元(1,015米ドル)まで下落しましたが、先物契約は依然として少なく、スポット購入を余儀なくされています。魚粉は季節的な高値で1万6,000元(2,255米ドル)に達し、包装のアップグレードに既に投資しているメーカーを圧迫しています。ブランド各社は変動リスクをヘッジするため昆虫タンパク質やエンドウ豆濃縮物への多角化を進めておりますが、配合変更サイクルが研究開発リソースを吸収しております。中国のペットフード市場は数量ベースでは成長を維持しているもの、コストを完全に転嫁できないバリューブランドでは利益率が縮小傾向にあります。

セグメント分析

フード製品は2025年時点で中国ペットフード市場規模の60.02%を占め、圧倒的な市場リーダーシップを維持しております。これは日常的なペット栄養における必須性、および価格帯を問わず幅広い消費者へのアクセス可能性を反映したものです。この重要な市場ポジションは、主に「ペットの品種・サイズ・年齢に関わらず、大半の飼い主にとって日常的な購入品である」という事実によって支えられております。

2031年までの同セグメントのCAGR9.21%は、消費者が基本的なドライフードから、新規タンパク質、機能性成分、ライフステージ対応を特徴とする専門的な配合製品へ移行するプレミアム化動向の恩恵を受けています。ドライペットフード、特にキブル形式は、利便性、保存安定性、多頭飼い世帯におけるコスト効率の高さから最大のサブセグメントを占めています。一方、ウェットペットフードは、都市化が進む中で、偏食傾向のあるペットや柔らかい食感を必要とする高齢ペット向けに、分量管理が容易で嗜好性を高めた製品への需要が増加し、成長が加速しています。

中国ペットフード市場レポートは、ペットフード製品別(フード、ペット用栄養補助食品/サプリメント、ペット用おやつ、ペット用医療食)、ペット別(猫、犬、その他のペット)、流通チャネル別(コンビニエンスストア、オンラインチャネル、専門店、スーパーマーケット/ハイパーマーケット、その他のチャネル)に分類されています。市場予測は金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリーおよび主要な調査結果

第4章 主要業界動向

- ペットの飼育数

- 猫

- 犬

- その他のペット

- ペット関連支出

- 消費者の動向

第5章 供給と生産の動向

- 貿易分析

- 原料動向

- バリューチェーン及び流通チャネル分析

- 規制の枠組み

- 市場促進要因

- 猫・犬用飼料におけるプレミアム化の加速

- DTC(Direct-to-Customer)デジタルネイティブペットフードブランドの台頭

- 機能性/治療的栄養のポジショニングの拡大

- 大手小売業者によるヒューマングレード原料調達義務化

- 地方都市における国内フリーズドライ生産能力の拡大

- エキゾチックペット向け飼料の越境ライブ配信コマース

- 市場抑制要因

- 家禽・魚粉原料の価格変動性

- 表示表示に関する規制当局の監視強化

- 手作り生食による競合の激化

- カーボンニュートラル工場のコンプライアンスコスト

第6章 市場規模と成長予測(価値と数量)

- ペットフード製品

- フード

- 製品別

- ドライペットフード

- ペット用ドライフード別

- キブル

- その他のドライペットフード

- ペット用ドライフード別

- ウェットペットフード

- ドライペットフード

- 製品別

- ペット用栄養補助食品/サプリメント

- 製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質およびペプチド

- ビタミン・ミネラル

- その他の栄養補助食品

- 製品別

- ペット用おやつ

- 製品別

- カリカリおやつ

- デンタルおやつ

- フリーズドライ・ジャーキーおやつ

- ソフトで噛みごたえのあるおやつ

- その他のおやつ

- 製品別

- ペット用医療食

- 製品別

- 糖尿病

- 消化器系サポート

- 口腔ケア用フード

- 腎臓用

- 尿路疾患

- 肥満用ダイエットフード

- 皮膚用ダイエットフード

- その他の獣医用ダイエットフード

- 製品別

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他の販売チャネル

第7章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- Brand Positioning Matrix

- Market Claim Analysis

- 企業概況

- 企業プロファイル.

- Mars, Incorporated

- General Mills Inc.

- ADM

- Nestle(Purina)

- Affinity Petcare S.A

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- PLB International Inc.

- Virbac

- Alltech

- Schell & Kampeter, Inc.(Diamond Pet Foods Inc.)

- Shanghai Enova Pet Products Co. Ltd

- Shanghai Navarch Pet Products Co. Ltd

- Tianjin Ringpu Bio-Pharmacy Co. Ltd

- Tongwei Pet Food

- Wellpet China