|

市場調査レポート

商品コード

1692569

家禽肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Poultry Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 家禽肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 437 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

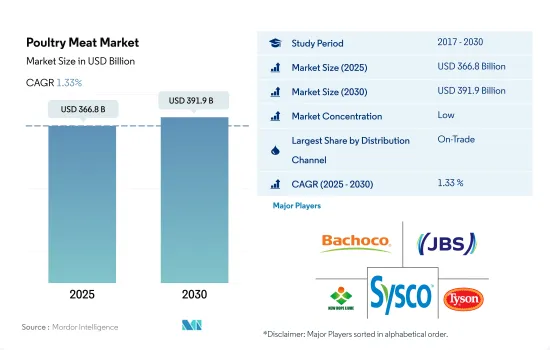

家禽肉市場規模は2025年に3,668億米ドルと推定・予測され、2030年には3,919億米ドルに達し、予測期間中(2025-2030年)のCAGRは1.33%で成長すると予測されます。

レストランでの家禽肉需要の増加がオン・トレード・チャネルでの売上を押し上げる

- 2020年から2022年にかけて、スーパーマーケットやインターネット小売店など、様々な商取引外のチャネルを通じた家禽肉売上は金額ベースで5%増加しました。環境と健康への懸念による消費者の食動向の変化により、冷凍家禽肉と加工家禽肉の売上が急増しました。さらに、英国とEUによる家禽肉の購入は、外食産業の回復とHPAIの発生による生産量の伸びの制限によって後押しされ、今後数年間でEU離脱前の貿易水準に達する可能性が高いです。UAEはブラジルの家禽肉輸出の約10%を吸収しています。

- オン・トレード・チャネルは食鳥肉市場における主要流通チャネルであり、2020年から2022年にかけて金額ベースで11.85%の成長を記録します。外食店舗数の増加と消費者の外食需要により、家禽肉の売上は増加しています。2022年には9億6,000万人以上の観光客が海外旅行し、パンデミック流行前の3分の2(66%)が回復したことになります。

- オフ・トレード・チャネルは、予測期間中に金額ベースで1.72%の成長を記録し、最も急成長する流通チャネルになると予測されます。これは主に、チキンバイツ、チキンチップス、ナゲット、テンダーロイン、チキンウィングなど、冷凍・加工食肉製品の幅広い商品展開に起因します。これらの家禽肉製品は、Tyson Foods、Foster Farms、ITC Master Chef、Suguna Chickenといった様々なブランドのスーパーマーケットやオンラインショップで簡単に入手できます。これらの売上は、世界の都市化の動向と、2022年時点で約50億人に達するインターネット・ユーザーの増加によって伸びています。

家禽肉の手頃な価格と市場への投資の増加が市場の成長を促進する

- 世界の家禽肉市場全体の成長は、2017年から2022年にかけて金額ベースでCAGR 4.50%を観測しました。豚肉や羊肉など他の食肉価格の上昇により、消費者の家禽肉へのシフトが高まっています。都市化と可処分所得の増加も市場成長を後押ししています。タンパク質需要の増加に伴い、国民は家禽肉のような持続可能で安価なタンパク質源を求めるようになっています。

- アジア太平洋は2017年から2022年までの金額ベースのCAGRが4.95%で市場を独占しました。同地域の都市人口の増加が、同地域の高い消費量に寄与しています。入手可能性の増加は同地域の低価格化に貢献し、予測期間中の家禽肉消費を押し上げると予測されます。中国のような市場では、製品への胸肉の利用を増やそうとしているため、鳥全体の利用が増え、ダークミートとホワイトミートの価格差が縮小しています。同地域の1人当たり消費量は他の主要消費地域と比べてまだ低いため、消費拡大の余地が残されています。

- アフリカは家禽肉を消費する最も急成長している地域と予測され、予測期間中のCAGRは金額ベースで3.17%と予測されます。同地域では鶏肉需要は所得弾力性があり、低所得層が多いことから、同大陸の数十の市場で家禽肉は依然として高級品です。クイック・サービス・レストランの増加や政府・民間企業による投資の増加が家禽肉需要を牽引しています。例えば、ガーナ政府は2023年、家禽肉産業を活性化させ、家禽肉輸入への依存度を下げるため、家禽肉産業に5億4,100万米ドルを投資することを約束しました。

世界の家禽肉市場動向

ブラジルは国内外からの需要により生産量が大きく伸びると予想される

- 調査期間中、世界の家禽肉生産量は変動的な伸びを示し、2022年には前年比1.83%の割合で増加しました。飼料費とエネルギー費の高騰が世界的に収益性に影響を及ぼしているが、食費が上昇する中で消費者が手ごろな価格の動物性タンパク質を求めているため、旺盛な需要が拡大に拍車をかけています。最大の家禽肉生産地域はアジア太平洋で、2022年の世界総生産量の40.75%を占める。

- 中国を除くすべての主要生産国が利益を上げ、ブラジルが最も成長します。中国では、ホワイトフェザーの生産量の伸びがイエローフェザーの生産量の減少を相殺するため、生産量は停滞すると思われます。2023年には、中国の消費者がより多様な蛋白質の食事に切り替えるため、手頃な価格の家禽肉製品、特に白羽鶏の需要が増加すると予想されます。タイの生産量は、国内消費の回復の遅れと、飼料用穀物や日齢雛の供給障害による生産コストの高騰が予想されるにもかかわらず、3%の成長が見込まれます。これらの要因により、成長率はCOVID-19流行前の平均を下回るとみられます。

- ブラジルの生産成長は、国内需要と世界需要に牽引されます。2021年の家禽肉生産量は1,434万トンです。ロシアとメキシコも、旺盛な国内需要により伸びると思われます。EUの生産量は、高病原性鳥インフルエンザ(HPAI)の発生に起因するエネルギーコストの上昇により、わずかな増加にとどまると予想されます。生産自動化、遺伝子組み換え、バイオセキュリティの進歩等の技術の導入により、食鳥処理業者の歩留まりは上昇すると予想されます。サイバー・フィジカル・システムと無線通信技術の統合により、食鳥処理効率を向上させ、原料歩留まりを最適化することができます。

安価なタンパク質としての家禽肉需要の高まりが、世界の価格上昇を後押ししています。

- 家禽の価格は、2017年と比較して2022年には11.31%大幅に上昇しました。供給不足が鶏肉価格の上昇を招いた。家禽肉価格を押し上げるもう一つの要因は、鶏肉飼料のコストです。以前と比べ、トウモロコシと大豆のコストはかなり高くなっており、そのためレストランや食料品店に届くと鶏肉の価格を押し上げています。鶏肉の価格、特に鶏胸肉の価格は、需要の増加、供給の逼迫、サプライチェーンの変化により急騰しています。レストランからの需要が特定の家禽肉の供給を圧迫しているため、鶏肉の卸売価格は上昇を続けています。

- 2024年には、飼料価格の下落が予想されるため、米国のブロイラー生産量は再び増加すると予想されるが、ブロイラー価格はわずかな減少にとどまる可能性があります。2023年のターキーの予想価格は上半期は横ばいだったが、2024年は高病原性鳥インフルエンザ(HPAI)からの生産回復が続くため、価格は下がると予想されます。2023年4月のコンパウンドブロイラーの全国平均卸売価格は140.15セント/ポンドで、2022年4月より27セント/ポンド下落したが、2023年3月より10セント上昇しました。4月の冷凍ターキーの平均卸売価格は169.93セント/ポンドでした。これは2023年に見られた横ばい傾向が続いており、最近の年間を通しての上昇とは対照的です。

- 米国、ブラジル、EUに次ぐ第4位の輸出国であるタイでは、2022年上半期に1kgあたり1.82米ドルとなり、半年で3分の1の上昇となりました。ブラジルの冷凍鶏肉卸売価格は2023年5月にキロ当たり2.12米ドルで、10年平均の2倍以上でした。

家禽肉業界の概要

家禽肉市場は細分化されており、上位5社で15.31%を占めています。この市場の主要企業は以下の通り。 Industrias Bachoco SA de CV, JBS SA, New Hope Liuhe, Sysco Corporation and Tyson Foods Inc.(アルファベット順)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 家禽肉

- 生産動向

- 食鳥

- 規制の枠組み

- オーストラリア

- バーレーン

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イタリア

- 日本

- クウェート

- メキシコ

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 缶詰

- 生鮮/冷蔵

- 冷凍

- 加工品

- 加工タイプ別

- デリミート

- マリネ/テンダー

- ミートボール

- ナゲット

- ソーセージ

- その他加工家禽肉

- 流通チャネル

- 非売品

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- 非売品

- 地域

- アフリカ

- 形態別

- 流通チャネル別

- 国別

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 形態別

- 流通チャネル別

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- その他アジア太平洋地域

- 欧州

- 形態別

- 流通チャネル別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- 英国

- その他欧州

- 中東

- 形態別

- 流通チャネル別

- 国別

- バーレーン

- クウェート

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他中東

- 北米

- 形態別

- 流通チャネル別

- 国別

- カナダ

- メキシコ

- 米国

- その他北米

- 南米

- 形態別

- 流通チャネル別

- 国別

- アルゼンチン

- ブラジル

- その他南米地域

- アフリカ

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BRF S.A.

- Cargill Inc.

- Charoen Pokphand Foods Public Co. Ltd

- Continental Grain Company

- Fujian Sunner Development Co. Ltd

- Hormel Foods Corporation

- Industrias Bachoco SA de CV

- JBS SA

- Koch Foods Inc.

- New Hope Liuhe Co. Ltd

- Sysco Corporation

- The Kraft Heinz Company

- Tyson Foods Inc.

- Wen's Food Group Co. Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92393

The Poultry Meat Market size is estimated at 366.8 billion USD in 2025, and is expected to reach 391.9 billion USD by 2030, growing at a CAGR of 1.33% during the forecast period (2025-2030).

Increasing demand for poultry meat at restaurants boosting sales through on-trade channels

- Poultry meat sales grew by 5% by value from 2020 to 2022 through various off-trade channels, including supermarkets and internet retailers. Frozen and processed poultry meat sales soared due to the shift in consumer eating trends due to environmental and health concerns. Furthermore, poultry purchases by the United Kingdom and the European Union are likely to reach the pre-Brexit trade level over the coming years, boosted by foodservice recovery and limited production growth due to HPAI outbreaks. Strong domestic demand is driving an increase in poultry meat purchases in the UAE, which is also absorbing around 10% of Brazil's total poultry meat exports.

- The on-trade channel is the major distribution channel in the poultry meat market, registering a growth of 11.85% by value from 2020 to 2022. Poultry meat sales are increasing due to growth in the number of foodservice outlets and consumers' demand for restaurant food. The sales are also in line with increased tourism spending, as in 2022, there were over 960 million tourists traveling internationally, meaning two-thirds (66%) of pre-pandemic numbers were recovered.

- The off-trade channel is projected to be the fastest-growing distribution channel, registering a growth of 1.72% by value during the forecast period. It is primarily attributed to the wide range of product availability of frozen and processed meat products, such as chicken bites, chicken chips, nuggets, tenderloins, and chicken wings. These poultry products are easily available in most supermarkets and online stores of various brands, such as Tyson Foods, Foster Farms, ITC Master Chef, and Suguna Chicken. These sales are growing due to urbanization trends worldwide and the increase in internet users, which reached around 5 billion as of 2022.

Affordability of poultry meat and growing investments in the market will propel the market's growth

- The overall growth of the global poultry meat market observed a CAGR of 4.50%, by value, from 2017 to 2022. The increase in other meat prices, like pork and mutton, has resulted in a rising shift in consumers toward poultry meat. The increasing urbanization and disposable incomes also propel the market growth. With the rise in the demand for protein, the population is seeking sustainable and cheaper protein sources like poultry meat.

- Asia-Pacific dominated the market with a CAGR of 4.95%, by value, from 2017 to 2022. The growing urban population in the region contributed to the high consumption in the region. An increase in availability helps lower prices in the region, which is anticipated to boost the consumption of poultry meat during the forecast period. Markets like China are trying to increase the use of breast meat in products, thus making more use of the entire bird and decreasing the price gap between dark meat and white meat. The region's per capita consumption is still low compared to other major consuming regions, thus leaving space to increase consumption.

- Africa is predicted to be the fastest-growing region that consumes poultry meat, with a projected CAGR of 3.17%, by value, during the forecast period. Chicken demand is income elastic in the region, and it remains a luxury good across dozens of markets on the continent, given low-income levels. The rise in the number of quick-service restaurants and the increase in the number of investments from government and private players is driving the demand for poultry meat. For instance, in 2023, the Government of Ghana committed to investing USD 541 million into the poultry industry to revitalize it and reduce the nation's reliance on poultry imports.

Global Poultry Meat Market Trends

Brazil is anticipated to experience a strong growth in production owing to domestic and international demand

- The global production of poultry saw variable growth during the study period, increasing at a rate of 1.83% in 2022 compared to the previous year. While elevated feed and energy costs have globally impacted profitability, the expansion is fueled by strong demand, as consumers seek affordable animal proteins amidst rising food costs. The largest poultry-producing region is Asia-Pacific, representing 40.75% of the total global production volume in 2022.

- All major producers except China are set to make profits, with Brazil witnessing the most growth. Production in China will stagnate as growth in white feather production offsets a decline in yellow feather production. The demand for affordable chicken products, particularly white-feathered chicken, is expected to increase in 2023 as Chinese consumers switch to a more diverse protein diet. Thai production is set to grow by 3% despite the expected slow recovery in domestic consumption and high production costs caused by supply disruptions for feed grains and day-old chicks. These factors will keep the growth rate below pre-COVID-19 pandemic averages.

- Brazil's production growth will be driven by domestic and global demand. In 2021, it produced 14.34 million tons of poultry meat. Russia and Mexico are also likely to grow due to strong domestic demand. EU production is expected to be only slightly higher due to rising energy costs resulting from outbreaks of highly pathogenic avian influenza (HPAI). The yield for poultry processors is expected to rise with the implementation of technology in production automation, genetical modification, biosecurity advancements, etc. It can improve poultry processing efficiency and optimize material yield through the integration of cyber-physical systems and wireless communication technologies.

Growing poultry demand as a cheaper protein is propelling the prices worldwide

- Prices for poultry significantly increased by 11.31% in 2022 compared to 2017. There was a supply shortage, which caused chicken prices to increase. Another factor driving the price of chicken is the cost of poultry feed. Compared to previous years, the cost of corn and soybeans has been quite high, thus boosting the price of chicken once it reaches a restaurant or grocery store. Poultry prices, particularly chicken breast prices, have skyrocketed due to increasing demand, tighter supply, and a changing supply chain. Wholesale chicken prices continue to rise as demand from restaurants puts pressure on the supply of certain cuts of poultry.

- In 2024, US broiler production is expected to increase again as feed prices are expected to decrease, but broiler prices may decrease only slightly. Projected turkey prices in 2023 remained unchanged for the first half of the year, but prices are expected to decrease in 2024 as production continues to recover from highly pathogenic avian influenza (HPAI). The national wholesale price for compound broilers averaged 140.15 cents/lb in April 2023, which was down by 27 cents/lb from April 2022 but up by 10 cents from March 2023. In April, the average wholesale price for frozen whole turkeys was 169.93 cents/lb. This continues the flattening trend seen in 2023, as opposed to the recent increase throughout the year.

- In Thailand, the fourth-biggest exporter after the United States, Brazil, and the European Union, the price of birds was USD 1.82 per kilogram during the first half of 2022, depicting a one-third increase in six months. Wholesale frozen chicken prices in Brazil were USD 2.12 per kilogram on May 2023, which was more than double their 10-year average.

Poultry Meat Industry Overview

The Poultry Meat Market is fragmented, with the top five companies occupying 15.31%. The major players in this market are Industrias Bachoco SA de CV, JBS SA, New Hope Liuhe Co. Ltd, Sysco Corporation and Tyson Foods Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Poultry

- 3.2 Production Trends

- 3.2.1 Poultry

- 3.3 Regulatory Framework

- 3.3.1 Australia

- 3.3.2 Bahrain

- 3.3.3 Canada

- 3.3.4 China

- 3.3.5 France

- 3.3.6 Germany

- 3.3.7 India

- 3.3.8 Italy

- 3.3.9 Japan

- 3.3.10 Kuwait

- 3.3.11 Mexico

- 3.3.12 Oman

- 3.3.13 Qatar

- 3.3.14 Saudi Arabia

- 3.3.15 United Arab Emirates

- 3.3.16 United Kingdom

- 3.3.17 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Canned

- 4.1.2 Fresh / Chilled

- 4.1.3 Frozen

- 4.1.4 Processed

- 4.1.4.1 By Processed Types

- 4.1.4.1.1 Deli Meats

- 4.1.4.1.2 Marinated/ Tenders

- 4.1.4.1.3 Meatballs

- 4.1.4.1.4 Nuggets

- 4.1.4.1.5 Sausages

- 4.1.4.1.6 Other Processed Poultry

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

- 4.3 Region

- 4.3.1 Africa

- 4.3.1.1 By Form

- 4.3.1.2 By Distribution Channel

- 4.3.1.3 By Country

- 4.3.1.3.1 Egypt

- 4.3.1.3.2 Nigeria

- 4.3.1.3.3 South Africa

- 4.3.1.3.4 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 By Form

- 4.3.2.2 By Distribution Channel

- 4.3.2.3 By Country

- 4.3.2.3.1 Australia

- 4.3.2.3.2 China

- 4.3.2.3.3 India

- 4.3.2.3.4 Indonesia

- 4.3.2.3.5 Japan

- 4.3.2.3.6 Malaysia

- 4.3.2.3.7 South Korea

- 4.3.2.3.8 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 By Form

- 4.3.3.2 By Distribution Channel

- 4.3.3.3 By Country

- 4.3.3.3.1 France

- 4.3.3.3.2 Germany

- 4.3.3.3.3 Italy

- 4.3.3.3.4 Netherlands

- 4.3.3.3.5 Russia

- 4.3.3.3.6 Spain

- 4.3.3.3.7 United Kingdom

- 4.3.3.3.8 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 By Form

- 4.3.4.2 By Distribution Channel

- 4.3.4.3 By Country

- 4.3.4.3.1 Bahrain

- 4.3.4.3.2 Kuwait

- 4.3.4.3.3 Oman

- 4.3.4.3.4 Qatar

- 4.3.4.3.5 Saudi Arabia

- 4.3.4.3.6 United Arab Emirates

- 4.3.4.3.7 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 By Form

- 4.3.5.2 By Distribution Channel

- 4.3.5.3 By Country

- 4.3.5.3.1 Canada

- 4.3.5.3.2 Mexico

- 4.3.5.3.3 United States

- 4.3.5.3.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 By Form

- 4.3.6.2 By Distribution Channel

- 4.3.6.3 By Country

- 4.3.6.3.1 Argentina

- 4.3.6.3.2 Brazil

- 4.3.6.3.3 Rest of South America

- 4.3.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 BRF S.A.

- 5.4.2 Cargill Inc.

- 5.4.3 Charoen Pokphand Foods Public Co. Ltd

- 5.4.4 Continental Grain Company

- 5.4.5 Fujian Sunner Development Co. Ltd

- 5.4.6 Hormel Foods Corporation

- 5.4.7 Industrias Bachoco SA de CV

- 5.4.8 JBS SA

- 5.4.9 Koch Foods Inc.

- 5.4.10 New Hope Liuhe Co. Ltd

- 5.4.11 Sysco Corporation

- 5.4.12 The Kraft Heinz Company

- 5.4.13 Tyson Foods Inc.

- 5.4.14 Wen's Food Group Co. Ltd

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms