アジア太平洋の家禽肉- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Asia-Pacific Poultry Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 241 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692065

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

アジア太平洋の家禽肉市場規模は2025年に1,755億米ドルと推定され、2030年には1,876億米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは1.34%で成長します。

都市化の進展とインターネットの普及が市場の売上を促進

- 2021年から2022年にかけて、取引外チャネルを通じた家禽肉販売全体は1.68%増加しました。アジア太平洋市場では、中国が2022年の家禽肉販売額で市場の40%以上を占め、圧倒的なシェアを占めています。2018年、アフリカ豚熱(ASF)の豚肉への影響により、人々はより多くの家禽肉を消費するようになり、需要が増加しました。ブラジル、タイ、ポーランド、ロシアからの輸入も2019年には2018年比で32%増加し、家禽肉価格の低下と入手可能性の向上に貢献しました。過去2年間で2倍に上昇した可処分所得の増加により、外食施設やその他のオフトレード流通チャネルを通じた家禽肉販売も増加しています。

- 2022年には、家禽肉販売の流通チャネルの中でオン・トレード・セグメントが優位を占めていました。2020年から2022年にかけて、販売額は10.3%の伸びを記録しました。アジア市場は多くのホテル、レストラン、施設(HRI)によって支配されています。中国自体、930万以上のケータリング・アウトレットを占め、2021年から2022年にかけて1.2%の上昇を記録しました。こうした要因から、オン・トレード・セグメントが主要なシェア値を占めています。

- 予測期間中、オンライン・チャネルはオフ・トレード・チャネルの中でCAGR値7.43%と最も急成長すると予測されています。これは、アジア太平洋地域で2021年時点で約29億6,000万人に達したインターネットユーザーの増加によるものです。インドのBigBasketやGrofers、アマゾンのような食料品宅配サイトは、その高度な宅配システムと支払い方法によって人気を博しており、このセグメントの成長を後押ししています。オン・トレード・チャネルでさえ、オンライン・プレゼンスを持つなど、ハイブリッド・モデルに移行しつつあり、市場をさらに牽引しています。

生産量の増加により地域で増加する家禽肉消費

- アジア太平洋市場では、2017年~2022年の家禽肉全体の販売額は金額ベースで4.10%のCAGRを記録しました。この増加は主に、この地域全体、特に東南アジアとオセアニアにおける食肉消費の増加によるものです。これらの国々の主食には、炭水化物と肉(主に家禽肉)の形のタンパク質が含まれています。2021年には、アジア太平洋の11カ国が合わせて100万トンを超える鶏肉を生産し、中国が1,470万トンの鶏肉を生産してトップに立ちました。さらに、アジア太平洋は小鳥を生産しており、鶏の約40%が加工されています。

- 2022年のアジア太平洋家禽肉市場では、中国が最大の数量シェアを占めました。中国の鶏肉産業は、アフリカ豚フィーバーの発生による深刻なタンパク質不足により拡大しました。しかしここ数年、家畜を襲ったアフリカ豚熱により、中国では食用豚の利用が激減しました。その結果、中国における鶏肉の生産と消費は2021年に12%増加しました。より健康的な選択肢として認識されている家禽肉は、中国の食肉メニューの第2位にランクされ、2021年には2,500万トンが消費されます。

- インドはアジア太平洋で最も急成長する市場になると予想されます。予測期間中の金額ベースのCAGRは3.61%と予測されます。インドにおける家禽肉の消費量は、レビュー期間中に19.8%増加しました。家禽肉の価格も他の種類の肉に比べて比較的安定しており、リーズナブルです。同国では、TenderCuts、Meatigo、Liciousのような食肉宅配会社が増加しており、家禽肉消費の拡大に大きく寄与しています。

アジア太平洋の家禽肉市場動向

生産者は生産性を向上させるため、先進技術による統合農業に注力しています。

- 同地域の家禽肉生産は、2017年から2022年にかけて18.66%という緩やかな成長率を示しました。同地域で労働問題が深刻化する中、同地域のメーカーは自動化に投資しています。自動給餌、自動飲水、自動換気システムはすでに一般的であるが、多くは自動巣システムへの投資を開始しています。すでに食肉処理場を持つメーカーは、さらなる処理に投資しています。2022年には、アジア太平洋における最大の家禽肉生産国は中国であり、そのシェアは48.66%、次いでインドが10.29%、インドネシアが8.49%でした。中国の家禽生産量は2017年から2022年に23.35%増加しました。中国で最も人気のある家禽品種には、白色ブロイラー、黄色ブロイラー、ハイブリッド、元層などがあります。鶏肉生産に占める白羽ブロイラーの割合は増加し、黄羽ブロイラーの生産は減少すると予想されます。

- インドの家禽肉部門は、2017年から2022年の間に30.08%成長し、この地域で第2位の家禽肉生産国です。インドの家禽肉生産の大部分は、独立系の比較的小規模な生産者によって占められています。同市場には、国内の一部地域で生産量のシェアを拡大しつつある総合的な大規模生産者も存在します。東南アジア諸国もまた、市場の成長を後押しする上で非常に重要な役割を果たしています。価格は上昇しているもの、東南アジアの養鶏の見通しは楽観的です。一般に、この地域の養鶏生産の約50%は集約的な中規模から大規模の商業農場で行われており、残りは数十羽の鶏、ガチョウ、アヒル、トルコを飼う小規模農家の裏庭で飼育されています。

- 2019年の家禽肉価格は3.32%の大幅上昇となりました。アフリカ豚熱の蔓延は豚の個体数を減少させ、豚肉価格を押し上げます。その結果、この地域最大の家禽肉市場である中国では、人々がより高価な豚肉から家禽肉に切り替えたため、供給不足による鶏肉価格の高騰が見られました。2016年以降、鳥インフルエンザの発生により米国とフランスからの鶏肉輸入が禁止された結果、中国は鶏肉不足に陥りました。それ以来、同国は消費者に家禽肉をリーズナブルな価格で提供しようと努力してきたが、2019年に悪化した鶏の品薄状態が続き、不満を募らせていました。2017年以降、中国の家禽肉供給量は0.34%しか増加しておらず、増大する需要を満たすことができないです。

- レビュー期間中、家禽肉価格は平均して年率2.48%の伸び率で上昇しました。家禽肉価格が常に高騰しているのは、ウクライナ戦争、鳥インフルエンザ、インフレが原因です。マレーシアでは、ウクライナ戦争が始まって以来70%上昇した輸入家畜飼料のコストが、生産コストを押し上げる主な要因となっています。

- 家禽肉需要の増加により、マレーシアはこの地域で最も急成長している家禽肉産業となっています。そのためマレーシア政府は、急増する需要に対応するため、2022年6月1日から月間360万羽の鶏の輸出を禁止することを計画し、国内供給の確保が重要な要素となりました。輸出禁止措置の施行に先立ち、政府は鶏肉の価格規制を何度も試みており、2月には標準鶏肉の上限価格を8.90リンギ/kg、ドレス家禽肉の上限価格を9.90リンギ/kgに設定しました。

アジア太平洋の家禽肉産業の概要

アジア太平洋の家禽肉市場は断片化されており、上位5社で7.65%を占めています。この市場の主要企業は以下の通り。 Cargill Inc., Charoen Pokphand Foods Public, New Hope Liuhe, Suguna Foods Private Limited and Tyson Foods Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 家禽肉

- 生産動向

- 食鳥

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 缶詰

- 生鮮/チルド

- 冷凍

- 加工品

- 加工タイプ別

- デリミート

- マリネ/テンダー

- ミートボール

- ナゲット

- ソーセージ

- その他加工家禽肉

- 流通チャネル

- 非売品

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- 非売品

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- その他のアジア太平洋

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Baiada Poultry Pty Limited

- BRF S.A.

- Cargill Inc.

- Charoen Pokphand Foods Public Co. Ltd

- Dayong Group

- Foster Farms Inc.

- Fujian Sunner Development Co. Ltd

- Inghams Group Limited

- New Hope Liuhe Co. Ltd

- NH Foods Ltd

- Suguna Foods Private Limited

- Tyson Foods Inc.

- Wen's Food Group Co. Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

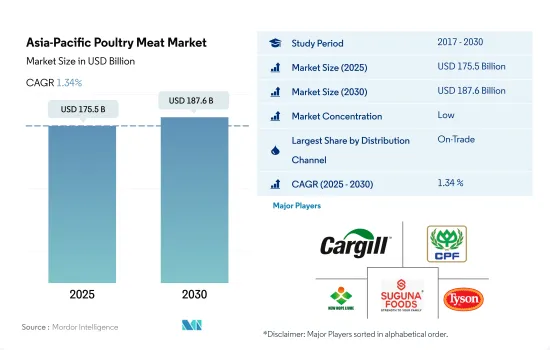

The Asia-Pacific Poultry Meat Market size is estimated at 175.5 billion USD in 2025, and is expected to reach 187.6 billion USD by 2030, growing at a CAGR of 1.34% during the forecast period (2025-2030).

Rising urbanization and internet penetration propelling market sales

- The overall sales of poultry meat through off-trade channels increased by 1.68% from 2021 to 2022. In the Asia-Pacific market, China dominated poultry meat sales by value, accounting for more than 40% of the market in 2022. The demand increased as, in 2018, the African Swine Fever's (ASF) influence on pork pushed people to consume more poultry meat. Imports from Brazil, Thailand, Poland, and Russia also increased by 32% in 2019 compared to 2018, which helped lower poultry prices and increased availability. The sales of poultry meat through foodservice establishments and other off-trade distribution channels have also increased due to increased disposable incomes, which have risen by two times in the past two years.

- In 2022, the on-trade segment was dominating among distribution channels for the sales of poultry meat. It registered a hike of 10.3% in sales value from 2020 to 2022. The Asian market is dominated by a number of hotels, restaurants, and institutions (HRI). China itself accounted for more than 9.3 million catering outlets, recording a 1.2% rise from 2021 to 2022. Due to these factors, the on-trade segment holds the major share value.

- During the forecast period, online channels are projected to witness the fastest-growing CAGR value of 7.43% among off-trade channels. This is due to the increasing number of internet users, which reached around 2.96 billion as of 2021 in Asia-Pacific. Grocery delivery sites like BigBasket and Grofers in India and Amazon have gained popularity due to their advanced delivery systems and payment methods, which are propelling the segment's growth. Even on-trade channels are shifting to hybrid models, including having an online presence, further driving the market.

Consumption of poultry meat rising in the region due to increased production

- In the Asia-Pacific market, the overall sales value of poultry meat registered a CAGR of 4.10% by value during 2017-2022. This increase was primarily due to the rising consumption of meat across the region, especially in Southeast Asia and Oceania. The staple diets in these countries include carbohydrates and protein in the form of meat, primarily poultry. In 2021, 11 Asia-Pacific countries together produced more than a million metric tons of chicken meat, with China leading the way by producing 14.7 million metric tons of chicken meat. Moreover, Asia-Pacific produces smaller birds, with about 40% of chickens being processed.

- China accounted for the largest volume share in the Asia-Pacific poultry meat market in 2022. The chicken industry in China has expanded due to the severe protein shortage caused by the African Swine Fever outbreak. Over the past few years, however, Chinese use of pigs for food dropped precipitously due to the African Swine Fever that ravaged livestock. As a result, the production and consumption of chicken meat in China grew by 12% in 2021. Poultry, which is perceived as a healthier option, ranks number two on China's meat menu, with 25 million tons consumed in 2021.

- India is expected to become the fastest-growing market in Asia-Pacific. It is projected to witness a CAGR of 3.61% in terms of value during the forecast period. The consumption volume of poultry in India increased by 19.8% during the review period. The price of poultry meat is also relatively stable and reasonable compared to other meat types. The increasing number of meat delivery companies in the country, like TenderCuts, Meatigo, and Licious, is largely contributing to the growth of poultry meat consumption.

Asia-Pacific Poultry Meat Market Trends

Producers are focusing on integrated farming with advanced technologies to increase productivity

- Poultry production in the region grew at a moderate rate of 18.66% between 2017 and 2022. With the growing labor problems in the region, manufacturers in the region are investing in automation. While automatic feeding, drinking, and ventilation systems are already common, many have started to invest in automatic nest systems. Manufacturers who already have slaughterhouses are investing in further processing. In 2022, the largest producer of poultry in Asia-Pacific was China, with a share of 48.66%, followed by India and Indonesia with 10.29% and 8.49%, respectively. The production of poultry in China increased by 23.35% in 2022 since 2017. In China, some of the most popular poultry breeds include white broiler, yellow broiler, hybrid, and ex-layer. The share of white feather broilers in chicken production is expected to increase, while yellow feather broiler production is expected to decline.

- India's poultry sector was the second-largest poultry producer in the region, which grew by 30.08% between 2017 and 2022. The majority of Indian poultry production is accounted for by independent and relatively small-scale producers. The market also has integrated large-scale producers accounting for a growing share of output in some regions of the nation. Southeast Asian countries also play a very important role in boosting the market's growth. The outlook for poultry farming in Southeast Asia is optimistic, although prices have risen. In general, around 50% of the poultry production in the region takes place on intensive medium to large-scale commercial farms, and the remaining are raised in back yards of small farmers who keep a few dozen chickens, geese, ducks, or turkeys.

- There was a significant increase in poultry prices, by 3.32%, in 2019. The spread of African swine fever decimates the pig population, driving up the price of pork. As a result, China, the region's largest poultry market, saw a spike in chicken prices due to a supply shortfall as people switched to chicken from more expensive pork. Since 2016, China has had a chicken shortage as a result of a prohibition on chicken imports from the United States and France due to the outbreak of avian flu. Since then, the country has worked hard to offer poultry meat to its consumers at a reasonable price but has been frustrated by the continued scarcity of chickens, which worsened in 2019. Since 2017, China's chicken supply has only risen by 0.34%, making it unable to meet the growing demand.

- On average, the price of poultry increased at a yearly growth rate of 2.48% during the review period. The constant surge in the price of poultry is attributed to the war in Ukraine, bird flu, and inflation. In Malaysia, the cost of imported livestock feed, which has risen by 70% since the war in Ukraine started, is the main factor driving up production costs.

- The rise in poultry demand makes Malaysia the fastest-growing poultry industry in the region. Accordingly, to cater to the surging demand, the Malaysian government planned to ban the export of 3.6 million chickens per month starting on June 1, 2022, with safeguarding local supplies being a key factor. Prior to enacting the export ban, the government made many attempts to regulate the price of chicken, including setting ceiling pricing in February for standard chicken at MYR 8.90/kg and dressed chicken at MYR 9.90/kg.

Asia-Pacific Poultry Meat Industry Overview

The Asia-Pacific Poultry Meat Market is fragmented, with the top five companies occupying 7.65%. The major players in this market are Cargill Inc., Charoen Pokphand Foods Public Co. Ltd, New Hope Liuhe Co. Ltd, Suguna Foods Private Limited and Tyson Foods Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Poultry

- 3.2 Production Trends

- 3.2.1 Poultry

- 3.3 Regulatory Framework

- 3.3.1 Australia

- 3.3.2 China

- 3.3.3 India

- 3.3.4 Japan

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Canned

- 4.1.2 Fresh / Chilled

- 4.1.3 Frozen

- 4.1.4 Processed

- 4.1.4.1 By Processed Types

- 4.1.4.1.1 Deli Meats

- 4.1.4.1.2 Marinated/ Tenders

- 4.1.4.1.3 Meatballs

- 4.1.4.1.4 Nuggets

- 4.1.4.1.5 Sausages

- 4.1.4.1.6 Other Processed Poultry

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 South Korea

- 4.3.8 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Baiada Poultry Pty Limited

- 5.4.2 BRF S.A.

- 5.4.3 Cargill Inc.

- 5.4.4 Charoen Pokphand Foods Public Co. Ltd

- 5.4.5 Dayong Group

- 5.4.6 Foster Farms Inc.

- 5.4.7 Fujian Sunner Development Co. Ltd

- 5.4.8 Inghams Group Limited

- 5.4.9 New Hope Liuhe Co. Ltd

- 5.4.10 NH Foods Ltd

- 5.4.11 Suguna Foods Private Limited

- 5.4.12 Tyson Foods Inc.

- 5.4.13 Wen's Food Group Co. Ltd

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 241 Pages

- 納期

- 2~3営業日