欧州の家禽肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Poultry Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 244 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683912

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

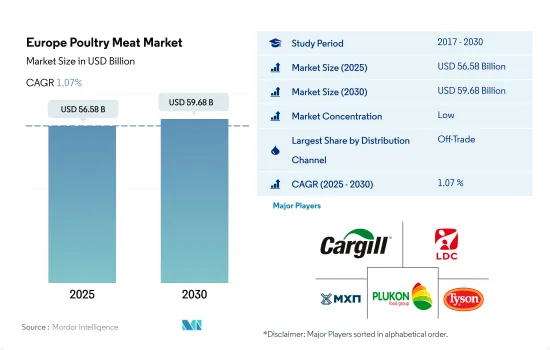

欧州の家禽肉市場規模は2025年に565億8,000万米ドルと推定・予測され、2030年には596億8,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは1.07%で成長すると予測されます。

観光客の増加が市場成長を後押し

- オフトレード・チャネルは欧州で最も急成長する流通チャネルであり、予測期間中に金額ベースでCAGR 0.96%を記録すると予測されます。この成長は主に、チキン・バイツ、チキン・チップス、ナゲット、テンダーロイン、チキン・ウィングなどの冷凍・加工食肉製品に対する需要の高まりに起因しています。これらの鶏肉製品は、Tyson Foods、Foster Farms、TGI Fridays、Avara Foodsといった様々なブランドのスーパーマーケットやオンラインストアで容易に入手できます。

- オン・トレード・チャネルを通じた鶏肉は、2017年から2022年にかけて金額ベースで2.99%のCAGRを記録し、予測期間中は金額ベースで0.81%のCAGRで推移すると予測されています。鶏肉販売は、外食店舗数の増加と消費者の外食需要により増加しています。外食産業は、その品質の高さから、主に冷凍鶏肉や加工鶏肉を仕入れています。2023年第1四半期にEU域内の観光宿泊施設で消費された宿泊数は約4億2,600万泊で、2022年同期比で28%増加しました。2023年1~3月期のホテル宿泊数は前年同期比で約7,600万泊増加した(32%増)。このように、観光客の増加が同地域の鶏肉販売に拍車をかけています。

- オンライン・チャネルのサブセグメントは、市場で最も急成長している非取引チャネルです。予測期間中のCAGRは金額ベースで6.40%と予測されます。これは、この地域におけるインターネット普及率の上昇に起因しています。オンラインショッピング利用者の数はここ数年で大幅に増加しています。2022年には、EU人口の約70~75%がオンラインショッピングに関与していました。約35%がレストラン、ファストフード・チェーン、ケータリング・サービスに食事を注文しています。

家禽肉消費の増加が市場成長を後押し

- 欧州では、鶏肉全体の販売額は2017~2022年の間に金額ベースでCAGR 3.99%を記録しました。この押し上げは主に、同地域全体での食肉消費の増加によるものです。同地域の鶏肉消費量は、小売およびHRI部門を通じた需要の増加により、2020年から2022年にかけて5.40%増加しました。長期的には、消費者の他の動物性タンパク質よりも鶏肉への嗜好が高まり、鶏肉消費の増加につながると予想されます。一般に、鶏肉は安く買えます。また、欧州の消費者は鶏肉がより健康的で手に入りやすく、調理も簡単だと考えています。

- 鶏肉は、ポーランド、ポルトガル、チェコ共和国、スコットランドのようなその他の欧州諸国で主に消費されています。2017年から2022年にかけて、残りの欧州の家禽肉市場は金額ベースで17.80%の成長を記録しました。家禽肉の生産は主に鶏のブロイラー(81%)とターキーのブロイラー(14%)で構成されており、これらは国内の食肉加工業界で需要があります。さらに、ポーランドの食肉加工産業は鶏肉ソーセージとパテの生産に特化しており、家禽肉市場の成長に寄与しています。

- オランダは欧州で最も急成長している市場と予想されます。予測期間中のCAGRは金額ベースで1.10%と予測されています。これは、同国における食鳥処理工場の増加によるものです。例えば、オランダには2023年時点で58の食鳥処理工場があり、2022年から1.8%増加しています。さらに、補助金や研究開発への投資といった政府の支援政策が、今後の鶏肉産業の成長をさらに後押しする可能性があります。

欧州の家禽肉市場の動向

生産コストの上昇と様々な疾病発生が鶏肉生産の妨げに

- 2022年、同地域の生産量は2021年比で1.62%の成長を遂げました。欧州は食鳥肉の主要輸出入国であり、世界の食鳥肉市場における主要貿易相手国になる過程にあります。新たな貿易取引の確立は、産業を拡大し、欧州経済を活性化させる鍵となります。EUの鶏肉生産量の98%はブロイラーであると推定されています。残りの2%は産卵鶏と雄鶏の肉です。ロシアの鶏肉生産は、2021年に0.89%の最小成長率を記録した後、回復しました。2022年の市場は2021年比で14.96%成長しました。ロシアの鶏肉産業は、生産コストの急上昇などの影響を受けています。ロシア市場における一部の飼料添加物の価格は、前年同期比で260%上昇しました。その結果、ロシア政府は前例のない生産量減少に歯止めをかけるため、養鶏業界に対して1,500万米ドルの補助金を承認しました。

- ドイツの家禽養殖産業は、農場から食肉処理場までの距離が短いことで有名です。家禽は厳格な衛生条件のもとで処理されます。処理には獣医の監督もつきます。ポーランドもこの地域の主要生産国です。ポーランドの鶏肉生産の大部分は、主に外食産業向けに輸出されています。

- ポーランドの鶏肉生産は、2023年には飼料コストとエネルギー・コストの上昇という大きな課題に直面すると予想されています。同産業は2~3ヵ月の短い生産サイクルで運営されており、外部要因に非常に敏感です。欧州食品安全機関(EFSA)によると、2022年6月現在、欧州36カ国で2,398件の高病原性鳥インフルエンザ(HPAI)が発生し、4,600万羽が殺処分されました。影響はアヒル、ターキー、産卵鶏で最も深刻でした。

生産コストの上昇とロシア・ウクライナ紛争による供給の途絶が価格上昇につながる

- 同地域の鶏肉価格は2017年から2022年にかけて11.53%上昇しました。同地域における鶏肉価格の高騰は、旺盛な需要、逼迫した供給、投入コストの高騰、全体的なインフレが重なった結果です。2022年、EUへの鶏肉の輸入はほぼ一定でした。英国、ブラジル、タイ、中国からの追加輸入が、2022年のロシアのウクライナへの軍事侵攻によってもたらされた輸入の損失を補いました。外食産業が制限を緩和して平常に戻ったため、2022年には鶏肉の価格が上昇し、欧州の鶏肉の輸入総額は1.5%上昇すると予測されます。

- EU域内の鶏肉価格の上昇は、ブラジルなどの競合他社がEU市場シェアを拡大するのに役立っています。ブラジルは2023年にEUへの鶏肉輸出を約35%増加させる見込みです。ウクライナは、ロシアとの戦争が続いているため関税が停止され、その恩恵を受け、EUへの輸出量は2022年には2021年よりも増加しました。

- 飼料コストも鶏肉価格を押し上げています。トウモロコシと大豆のコストは例年より高く、レストランや食料品店に並ぶ鶏肉価格を押し上げています。家禽飼料は家禽のファーム・ゲート・バリューの最大55%を占める。従って、鶏肉価格の上昇は、予測期間中、低所得世帯に不釣り合いな影響を与える可能性があります。EUにおける2023年上半期のブロイラー価格は、枝肉1.85米ドル/kgから4.27米ドル/kgまで幅があります。EUにおけるブロイラーの平均価格は、2023年上半期に前年比3%上昇しました。2023年6月、オランダの枝肉価格は1.81米ドル/kgと最も低く、デンマークの枝肉価格は4.45米ドル/kgと最も高かったです。

欧州の家禽肉産業の概要

欧州の家禽肉市場は断片化されており、上位5社で11.63%を占めています。この市場の主要企業は以下の通りです。Cargill Inc., Lambert Dodard Chancereul(LDC)Group, MKHP, PRAT, Plukon Food Group and Tyson Foods Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 鶏肉

- 生産動向

- 食鳥

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 缶詰

- 生鮮/冷蔵

- 冷凍

- 加工品

- 加工タイプ別

- デリミート

- マリネ/テンダー

- ミートボール

- ナゲット

- ソーセージ

- その他加工鶏肉

- 流通チャネル

- 非売品

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オントレード

- 非売品

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- 英国

- その他欧州

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- 2 Sisters Food Group

- Cargill Inc.

- Gruppa Cherkizovo, PAO

- JBS SA

- Lambert Dodard Chancereul(LDC)Group

- MKHP, PRAT

- PHW Group

- Plukon Food Group

- Rothkotter Group

- Societe Bretonne de Volaille

- Tyson Foods Inc.

- Veronesi Holding S.p.A.

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001602

The Europe Poultry Meat Market size is estimated at 56.58 billion USD in 2025, and is expected to reach 59.68 billion USD by 2030, growing at a CAGR of 1.07% during the forecast period (2025-2030).

Increased tourist arrivals propelling the market growth

- The off-trade channel is projected to be the fastest-growing distribution channel in Europe, registering a CAGR of 0.96% by value during the forecast period. This growth is primarily attributed to the growing demand for frozen and processed meat products, such as chicken bites, chicken chips, nuggets, tenderloins, and chicken wings. These poultry products are readily available in most supermarkets and online stores of various brands, such as Tyson Foods, Foster Farms, TGI Fridays, and Avara Foods.

- Poultry meat through on-trade channels registered a CAGR of 2.99% by value from 2017 to 2022 and is anticipated to register a CAGR of 0.81% by value during the forecast period. Poultry meat sales are increasing due to the rise in the number of foodservice outlets and consumers' demand for restaurant food consumption. Services primarily stock frozen and processed poultry meat due to their high quality. Around 426 million nights were spent at tourist accommodation establishments in the European Union in the first quarter of 2023, up by 28% compared with the same period in 2022. About 76 million more hotel nights were spent in the first three months of 2023 compared with one year earlier (+32%). Thus, the increased tourism is fueling the sales of poultry meat in the region.

- The online channel sub-segment is the fastest-growing off-trade channel in the market. It is projected to register a CAGR of 6.40% by value during the forecast period. This is attributed to the increased internet penetration rate in the region. The number of online shoppers has increased considerably over the last few years. In 2022, around 70-75% of the EU population were involved in online shopping. Around 35% ordered meals from restaurants, fast-food chains, and catering services.

Rising consumption of poultry meat boosting the market growth

- In Europe, the overall sales value of poultry meat registered a CAGR of 3.99% by value during 2017-2022. This boost was primarily due to the rising consumption of meat across the region. The region's chicken consumption grew by 5.40% from 2020 to 2022 as the demand through the retail and HRI sectors increased. Over the longer term, consumers' preferences for chicken over other animal proteins grew, which is expected to lead to increased consumption of poultry meat. Generally, it is cheaper to buy chicken meat. Chicken meat is also considered to be healthier, more accessible, and easier to prepare by consumers in Europe.

- Poultry meat is majorly consumed in the Rest of European countries, like Poland, Portugal, the Czech Republic, and Scotland. From 2017 to 2022, the Rest of European poultry meat market registered a growth of 17.80% by value. Poultry meat production consists mainly of chicken broilers (81%) and turkey broilers (14%), which are in demand in the domestic meat processing industry. In addition, the Polish meat processing industry specializes in producing poultry sausages and pates, contributing to the growth of the poultry meat market.

- The Netherlands is anticipated to be the fastest-growing market in Europe. It is projected to witness a CAGR of 1.10% in terms of value during the forecast period. This is attributed to the increasing number of poultry processing plants in the country. For instance, there were 58 poultry meat processing plants in the Netherlands as of 2023, an increase of 1.8% from 2022. Moreover, supportive government policies, such as subsidies and investments in research and development, may further boost the poultry industry's growth in the future.

Europe Poultry Meat Market Trends

Higher production costs and various disease outbreaks are hindering the poultry production

- In 2022, the region experienced a growth of 1.62% in production compared to 2021. Europe is a major importer and exporter of poultry meat, and it is in the process of becoming a major trading partner in the global poultry meat market. Establishing new trade deals is key to expanding the industry and boosting the European economy. An estimated 98% of all EU chicken production consists of broiler meat. The remaining 2% is derived from laying hens and cocks. The poultry production in Russia retrieved after a minimum growth of 0.89% in 2021. In 2022, the market grew by 14.96% compared to 2021. The Russian poultry industry is impacted by factors including a sharp rise in production costs. The price for some feed additives in the Russian market increased by 260% in a Y-o-Y comparison. As a result, the Russian government approved a USD 15 million subsidy to the poultry industry to halt the unprecedented drop in production.

- The German poultry production industry is famous for the short distances between farms and slaughterhouses. The poultry is processed under strict hygienic conditions. The processing is also subject to supervision by a vet. Poland is also a major producer in the region. A major share of Polish chicken meat production is exported primarily to the food service industry.

- Polish poultry production was expected to face significant challenges with higher feed and energy costs in 2023. The industry operates on a short 2-3-month production cycle, which is very reactive to outside events. According to the European Food Safety Authority (EFSA), as of June 2022, there had been 2,398 outbreaks of highly pathogenic avian influenza (HPAI) in 36 European countries, leading to the culling of 46 million birds. The impacts were most severe in ducks, turkeys, and laying hens.

Higher production costs and supply disruptions due to the Russia-Ukraine conflict are leading to price growth

- The prices of poultry in the region grew by 11.53% from 2017 to 2022. The poultry price hike in the region has resulted in a combination of strong demand, tight supply, high input costs, and overall inflation. In 2022, imports of poultry into the EU largely remained constant. Additional imports from the United Kingdom, Brazil, Thailand, and China compensated for the loss of imports brought on by Russia's military aggression on Ukraine in 2022. As the foodservice industry returned to normalcy with ease in restrictions, the price of poultry meat increased in 2022, with a projected 1.5% rise in the total European poultry imports.

- Higher local poultry prices in the EU are helping competitors, such as Brazil, to gain more EU market share. Brazil was also expected to export around 35% more poultry to the EU in 2023. Ukraine, which benefitted from a suspension of duties due to the ongoing war with Russia, was exporting to the EU at higher volumes in 2022 than in 2021.

- The cost of poultry feed is also driving the price of chicken. The costs of corn and soybeans have been higher than in previous years, boosting the price of chicken once it reaches a restaurant or grocery store. Animal feed accounts for up to 55% of the farm gate value of poultry. Therefore, higher-priced poultry may disproportionately impact lower-income families during the forecast period. The broiler prices in the EU during the first half of 2023 varied from USD 1.85/kg of carcass to USD 4.27/kg. The average prices of broilers in the EU grew by 3% in the first half of 2023 compared to the previous year. In June 2023, the Netherlands recorded the lowest price of USD 1.81/kg for carcasses, and Denmark had the highest price of USD 4.45/kg for carcasses.

Europe Poultry Meat Industry Overview

The Europe Poultry Meat Market is fragmented, with the top five companies occupying 11.63%. The major players in this market are Cargill Inc., Lambert Dodard Chancereul (LDC) Group, MKHP, PRAT, Plukon Food Group and Tyson Foods Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Poultry

- 3.2 Production Trends

- 3.2.1 Poultry

- 3.3 Regulatory Framework

- 3.3.1 France

- 3.3.2 Germany

- 3.3.3 Italy

- 3.3.4 United Kingdom

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Canned

- 4.1.2 Fresh / Chilled

- 4.1.3 Frozen

- 4.1.4 Processed

- 4.1.4.1 By Processed Types

- 4.1.4.1.1 Deli Meats

- 4.1.4.1.2 Marinated/ Tenders

- 4.1.4.1.3 Meatballs

- 4.1.4.1.4 Nuggets

- 4.1.4.1.5 Sausages

- 4.1.4.1.6 Other Processed Poultry

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

- 4.3 Country

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 United Kingdom

- 4.3.8 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 2 Sisters Food Group

- 5.4.2 Cargill Inc.

- 5.4.3 Gruppa Cherkizovo, PAO

- 5.4.4 JBS SA

- 5.4.5 Lambert Dodard Chancereul (LDC) Group

- 5.4.6 MKHP, PRAT

- 5.4.7 PHW Group

- 5.4.8 Plukon Food Group

- 5.4.9 Rothkotter Group

- 5.4.10 Societe Bretonne de Volaille

- 5.4.11 Tyson Foods Inc.

- 5.4.12 Veronesi Holding S.p.A.

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

欧州の家禽肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 244 Pages

- 納期

- 2~3営業日